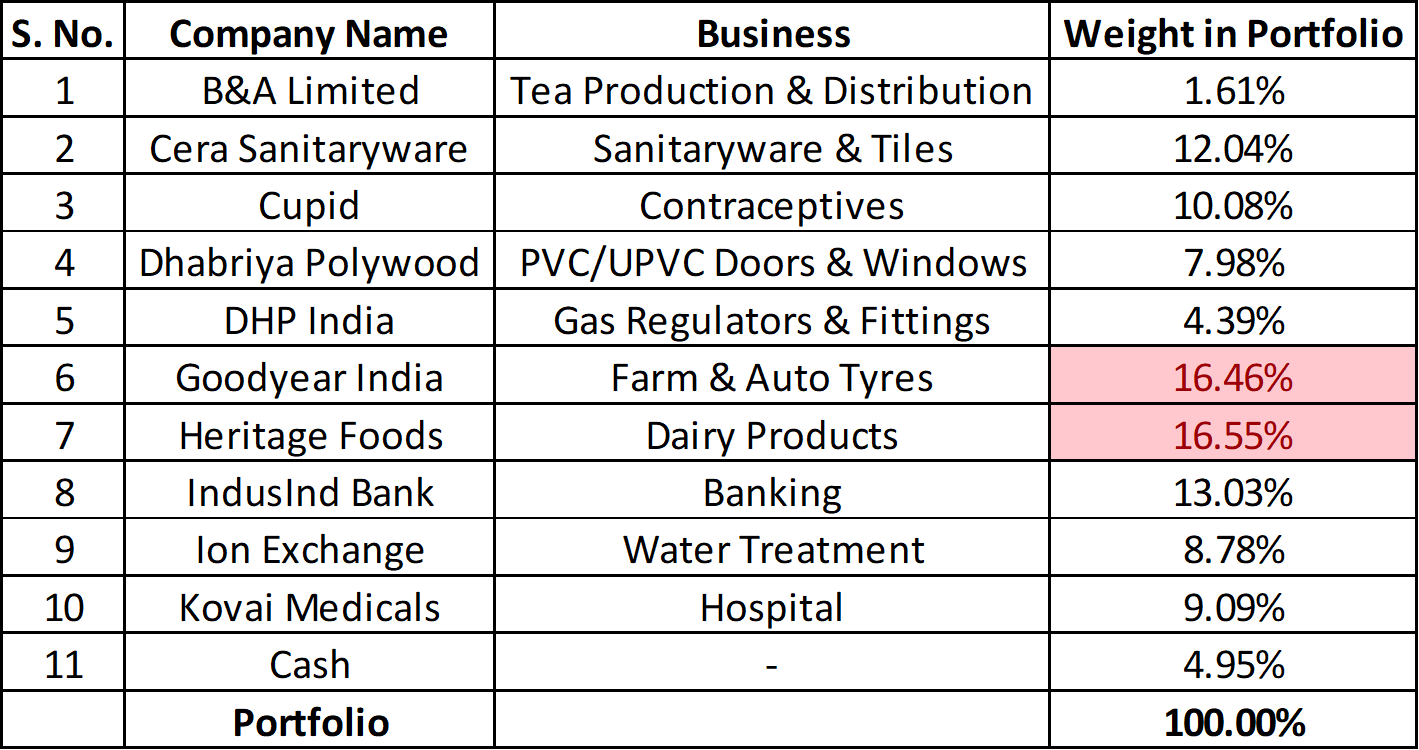

Pre-election update on PF. I have invested most of my leftover cash yesterday in a flurry of last minute purchases. This is how the PF looks like now:

The latest entry is, of course, IndusInd Bank. A few key points on why I invested here:

-

First off, I understand that there are risks here. Otherwise, a good bank like IndusInd has no reason to correct ~30%+ from the top. The key risk being the exposure to ILFS and other questionable loans to Essel, ADAG, DHFL and Zee. At this point, I’d say the situation is like a ‘mini Yes Bank’. One more minor risk is the succession. Mr. Ramesh Sobti has been amazing so far. But as per RBI’s latest ruling, he has to step down owing to age.

-

The exposure to ILFS is around Rs. 3000 Crore, out of which 70% for Rs. 2000 Crore and 25% for Rs. 1000 Crore has been provided (So, that’s Rs. 1650 Crores). Ex-ILFS, the exposure to the above mentioned questionable groups is ~Rs. 3600 Crores (Approx). Apart from all this, I assume there are other NPAs amounting to ~Rs.1000 Crores (Approx). In all, ~Rs. 6000 Crores can be expected as losses in the future. Since RBI is tightening the screws around bad loans recognition, I should hope that more provisioning will be on the way. And that’s good.

-

I have indeed performed a valuation of IndusInd. I have yet to make some adjustments for accuracy. But in short, I believed that IndusInd provided value even after accounting for 100% of the NPAs and a 30% Margin of Safety. I will post it here if I manage to knock out the kinks.

-

I should hope that the brand in IndusInd and their size of operations should easily attract a good MD/CEO.

-

The expected merger with Bharat Financial should bring in more scale. The key to the merger (Well, to most mergers) is how quick the integration happens. We’ll just have to wait and see that.

Also increased stake in Heritage Foods a bit.

-

Decent results QoQ, considering it was winter. Winter is often low pickings for pure milk players. Cows produce lower milk in winter. Sellers instead have to rely on a mix of cow and buffalo milk, buffalo milk being costlier than cow’s milk by quite a bit. Excellent results YoY, but this is largely due to huge one-off in September results.

-

Again, a considerable risk I see is tomorrow’s results in Andhra Pradesh. Mr. YS Jagan has promised to reopen Chittoor Dairy and provide Rs. 4 subsidy to milk farmers in Andhra, should he come to power. Andhra’s treasury wouldn’t really allow this (At least not in a hurry), but if he comes to power and manages to pull it off, it could play a spoilsport for Heritage. Situations like this is why Margin of Safety exists. But any way, my thesis for investing in Heritage is based on growth outside of Andhra and growth in VADP, which is beyond politics in AP. I guess we will have to wait and see whether my expectations are valid or not.

Increased token stakes in Cupid, Dhabriya Polywood and Ion Exchange. Cupid’s upcoming result should be especially interesting. Last quarter, the stock fell off a bit because of supposedly “bad” results. The truth was that some accounting adjustment has been made and the next (This) quarter result should reflect the excluded sales from the previous quarter. So, we should see a supposedly “massive” increase in Sales, Profit and Cashflows. It will be amusing to see the market react to that.

Shortlist currently looks like this: Ambika Cotton, Avenue Supermarts, CCL Products, Cyient, DFM Foods, Eicher Motors, Godrej Consumer Products, HDFC AMC, Indian Terrain, L&T Technology, Maruti Suzuki, Motherson Sumi, MRF, NESCO, Oriental Carbon, PSP Projects and Shemaroo Entertainment.

However, what with only a small fraction of cash left over, I’m not hopeful of any near-term purchases unless I find some really amazing deal (In my PF, shortlist or otherwise). Mostly, I’d be trying to save up as much as possible and bring back the cash position to ~20%, which is my comfort level.

Tomorrow should be very interesting and perhaps the week after that. I’m personally going to sit back and watch the marching band. Ta-ta!