Maybe this much is sufficient to answer. Amines growth in India and shortage is expected to continue till FY23 (from a recent BAL earnings presentation).

See:

1 Like

Hi,

I noticed two cases of promoter’s relatives selling shares recently. Any thoughts on this?

Disc: I completely exited booking profits earlier. I had plans to re-enter.

Thanks in advance,

Anto

1 Like

Hi,

Promoter’s relative’s dumping again. Please see here,

https://www.bseindia.com/stock-share-price/diamines-chemicals-ltd/DIAMINESQ/500120/disclosures-insider-trading-2015/

Any thoughts on this?

Thanks,

Anto

1 Like

And again selling,

https://www.bseindia.com/stock-share-price/diamines-chemicals-ltd/DIAMINESQ/500120/disclosures-insider-trading-2015/

I wouldn’t worry because there is no change in promoter & promoter group shareholding pattern,

1 Like

The change will reflect in updated SHP, which will be filled by company. Currently we have SHP of 30th June on link shared by you

Hi any update on the company ? The stock seems to be falling quite a bit from its highs of Rs. 557+

I can see that stock is taking support at 340 level since last 1.5 months. This is also 50% of Fib level. during last week Nifty tumble, it tested 38.2% Fib level and bounced back very quickly to 50% fib level. RSI of the stock is also decent and shows that its oversold. looking at this technical indicators, i have taken position in this stock since last 1 month with an avg of 357 Rs. and will be adding more at dip. See my technical analysis below. please correct if i have misunderstood any part.

1 Like

While reading the AR, I got a feeling that they are the only players in India . But Balaji seems much bigger than them., This seems like a company thats not investing in capacity for growth and just chugging along, doing a very good biz (ROE, ROCE are excellent) , paying good dividend… Reading all of your comments above, growth seems only to come from market expansion - organic …

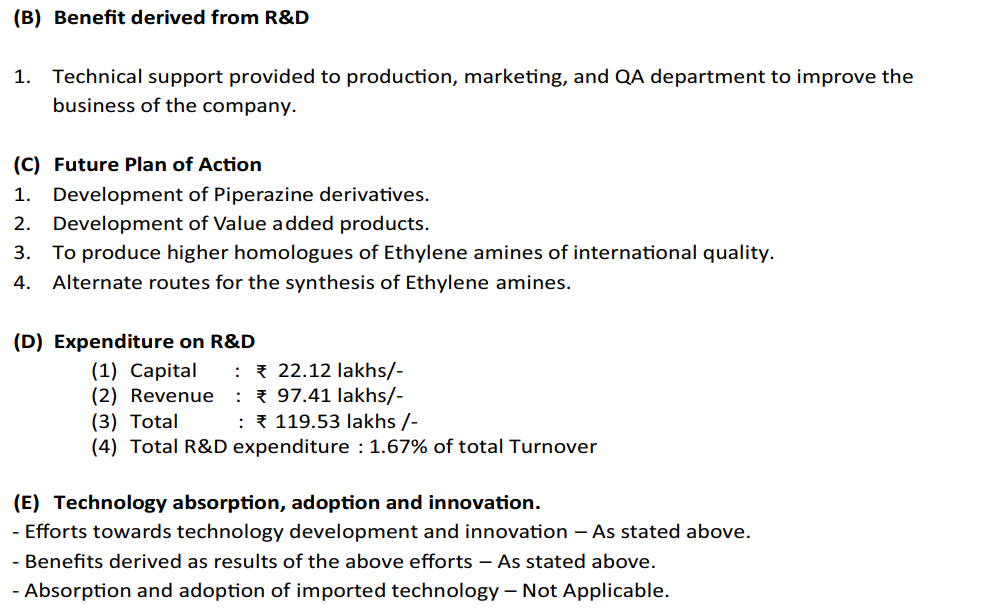

in the AR, they talk about 1.67% R&D Investment - for some product development , but nothing that talks about specifics here.

I hope these guys use their technology and experience and start investing , start communicating more transparently …

At the moment, there are much better opportunities for growth out there…

6 Likes

Thanks Vikas for the detailed views on the company. with the company posting poor numbers this quarter and the correction today, what is your current view for the company.

Does it still look investable?

I did not post in this thread to avoid cluttering but did post in my PF thread about the change in my capital allocation. I exited this when it looked fully valued to me, since I had more alternatives in mind which were better priced for growth. The problem here was management’s non-disclosure in general and about the expansion plans in particular. The only reason to stay invested would have been a fast growth by expansion. Margins generally will fade with time, back to historic averages. Do not know what happened since.

PS: my PF thread is here: The Anti-Portfolio

4 Likes

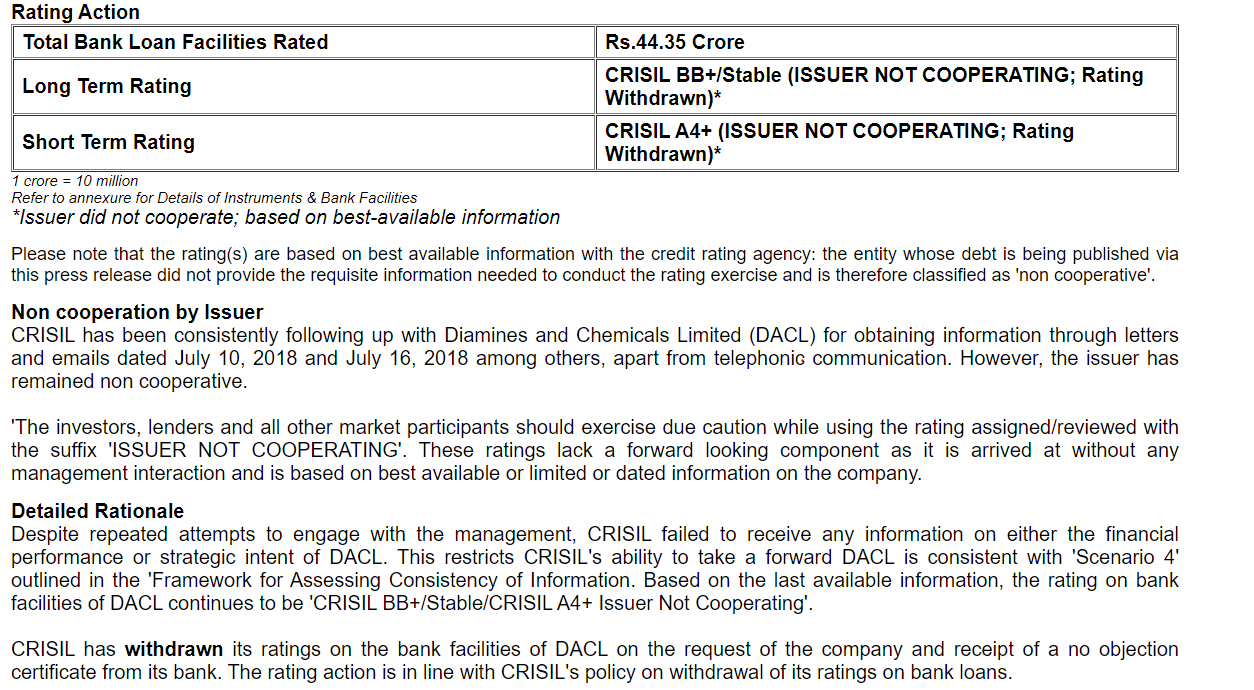

I noticed that this company has not been cooperating with Crisil, leading Crisil to withdraw their rating in 2018

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Diamines_and_Chemicals_Limited_August_09_2018_RR.html

I am curious to understand how this should be interpreted. I understand that the company has been mostly debt free since 2018. But the non cooperative approach It still seems fishy and unethical to me, causing me the doubt the integrity of management. This also leads me to question if I can trust their financial numbers at face value.

Any thoughts on how to read this situation?

1 Like

Hi Sayeed,

I think there is nothing much to read here, this is rating agencies continuous job and there is no obligation on the company side to give all the data that they have requested. Rating agencies usually work for institutions who lends, they rely on rating agencies vetting of business debts and other parameters, lenders use this report to take decisions on financing the company. If there is no such requirement these agencies still keep giving a periodical update. Some companies give the necessary info when they think their position is strong on the balance sheet side. This will work a s catalyst on companies stock price.

3 Likes

@vikas_sinha a year later, this is so true. I listened to the AGM while trying to understand this company better, and the management comes across as very fragile. They’re afraid of disclosing expansion details lest their competitors find out. For the same reasons, they don’t disclose their end market, nor their supply contracts. If the major advantage you have over your competitors is fairly basic information, that’s a losing model.

I thought you’d be interested as the information you were searching for a year ago is now in public domain. The EC for their 10x capacity expansion came through, and sheds light on new products. Sharing it here for anyone who comes across this company later on.

Disclosure - not invested.

14 Likes

5 Likes

Hi, if any member attended the AGM of Diamines, kindly share notes.

Thanks in advance.

1 Like

Short note on Diamines Chemicals

Short note on Diamines Chemicals.pdf (394.2 KB)

9 Likes

It is amazing to see its operating margins. Best in this industry.

DIAMINES is the Sole manufacturer of Ethyleneamines & it’s Derivatives,

manufacturing products for agriculture, pulp and paper, paint and coatings, adhesives, oilfield and gas treatment, polyurethane catalyst, electronics, as well as pharmaceuticals, and textile.

Diamines is in the process of completing expansion.

Balaji sp chemicals capacity - 3700 MT / month and Diamines will be 2250 MT/ month and Balaji expect peak revenue of 450- 500 cr from that capacity.

Accordingly Diamines chemicals can generate around 250 cr revenue with peak utilization.

The present sales is only Rs 66 cr for FY 2022.

@vikas_sinha Vikas Ji Pls share your views.

Thanks

4 Likes

Thanks for enumerating the data but I feel the promise of capex is extremely slow to realize, to the extent that they have had to renew the EC for the expansion project. This does not look that good to me, currently all the progress is locked up in land and buildings only. If pace of capacity addition is slow, and then utilization is also slow, then we might end up with no special growth at all.

There was an exact same promise in Kanchi, thankfully in its first ever investor interaction the management clearly stated growth of 15% to 20% only and 8 years for full revenue realization. I sold 65% of my holdings during that con call, after having waited for 2 years for capex to finish. Valuations were at peak and margins too. (I did not sell fully because the price data pointed to peak quarter ahead)

4 Likes

Thanks vikas ji

I looked at the Balance sheet of FY 22 and in Fixed assets there is a huge jump.

Hope management comes up with clarification in the next investor presentation/ Board meeting.