Intro:

Diamines and Chemicals Ltd (DACL/Diamines) is a Vadodara-based based speciality chemical player and is the one of few manufacturers of ethyleneamines in India. The company enjoys barriers to entry based on technology and its long existence in the market. However, there are concerns on product concentration and limited visibility on long-term business growth. Though it seems well positioned to benefit from the upcoming growth opportunity.

https://www.screener.in/company/500120/

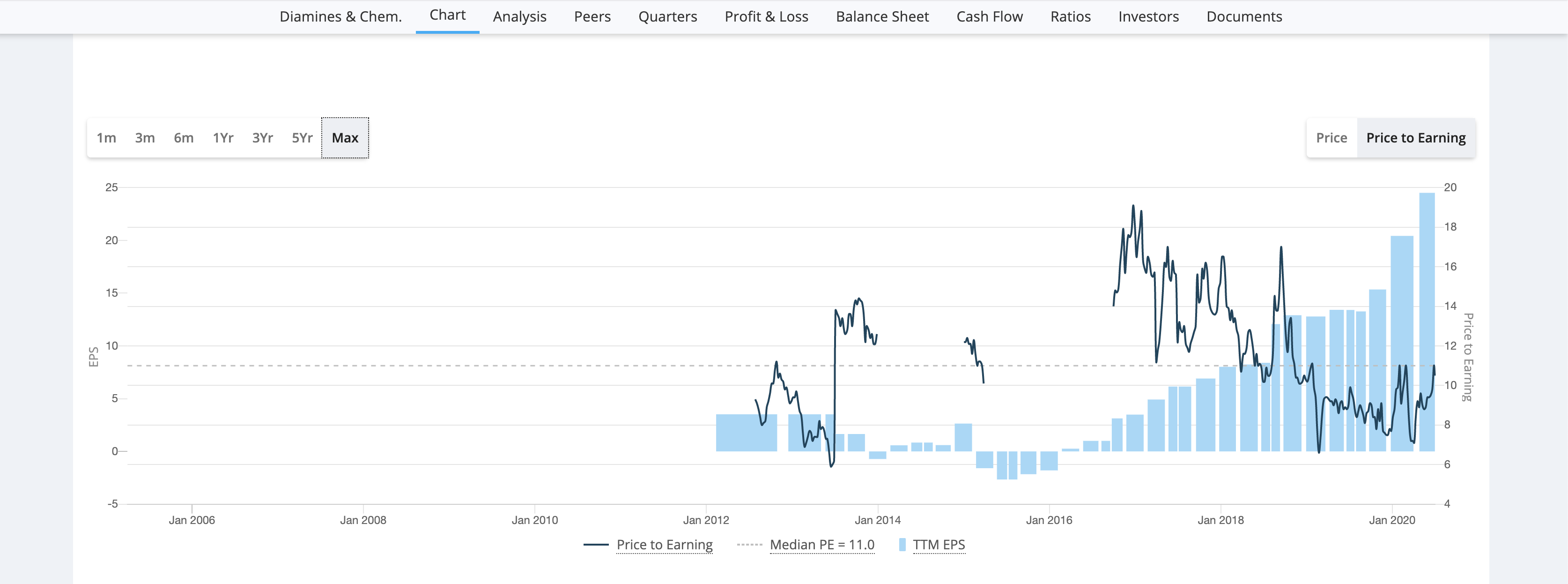

Mkt cap = 200 Cr, PE 10.

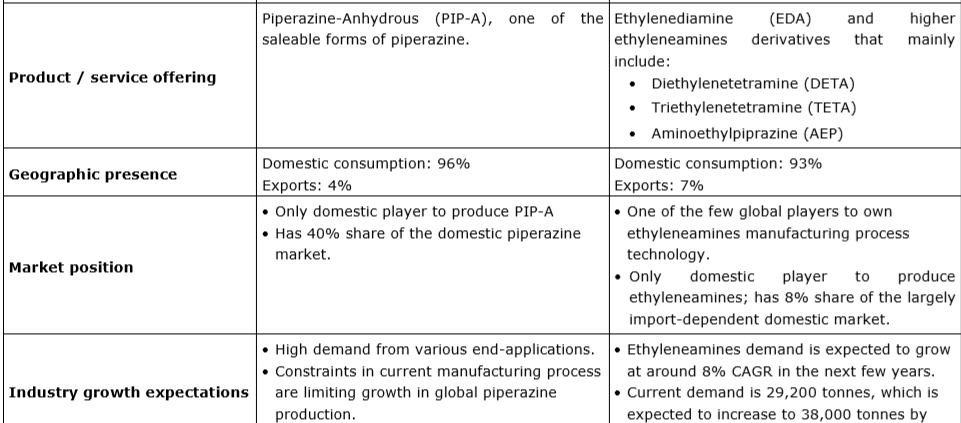

Diamines can benefit from ethyleneamines’ growing domestic market, Diamines is one of few established player in the domestic ethyleneamines market and holds ~40% share in the domestic piperazine (a sub-segment of ethyleneamines) market. With the Indian ethyleneamines market expected to grow at ~8% CAGR in the next few years and piperazine likely to benefit from domestic pharma growth, Diamines is well positioned to tap this opportunity.

Discovery:

Looking at chemical players (due to continued move of business from China), found the Alkyl Amines to be a promising bet, the company shares the promoter group with DACL, but there was a re-organization of ownership and the concerns were split off about a year ago, with a non-compete agreement. Amit M Mehta, took exclusive control, by relinquishing share in Alkyl Amines.

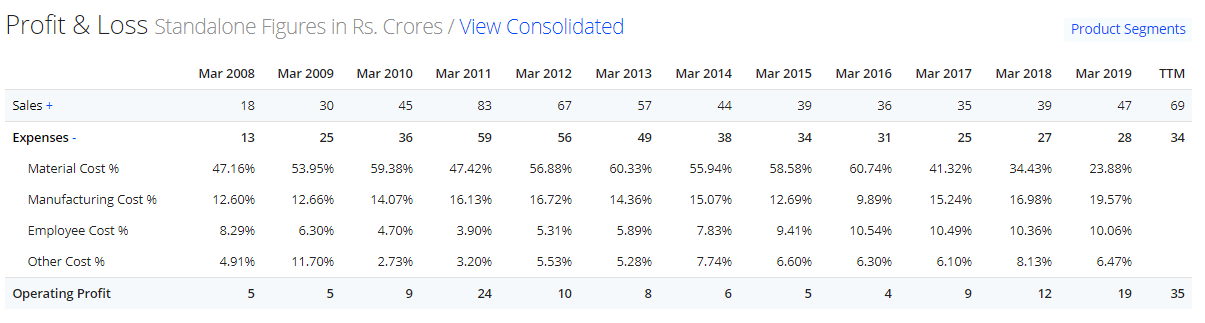

My understanding is that the Ethyl Amines are higher margin and have better process moat than Methyl Amines. Found the growth trajectory having good momentum and valuation seemed reasonable. The margins have recently become 4x compared to the 2013-2016 period. The company was in focus in 2011 but did not deliver on promised growth, it is a small player and can get crushed by imports by big players, which seems to have occurred then.

Main use of commodity products of the company seem to be deployed in Pharma and the competition seems to be mainly from China.

More details:

AR 2019 page#26 seems to show the company can be challenged due to over-supply, but it seems to have managed quite well since then and the reason might be deploying the unused capacity (of EDC) to make new sets of chemicals in demand. This EDC tech was cutting edge in 2011 but is obsolete now.

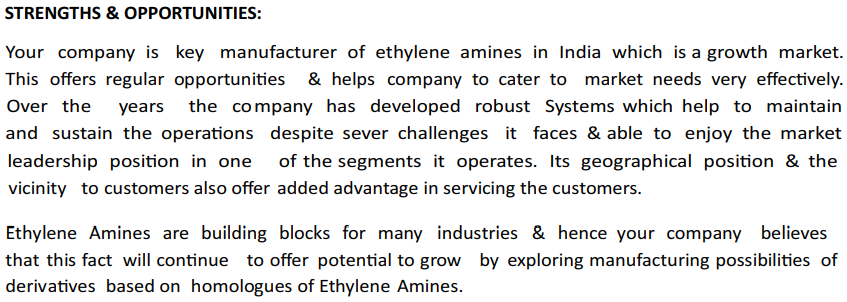

Overall management quality seems ok. This extract of the AR seems well written:

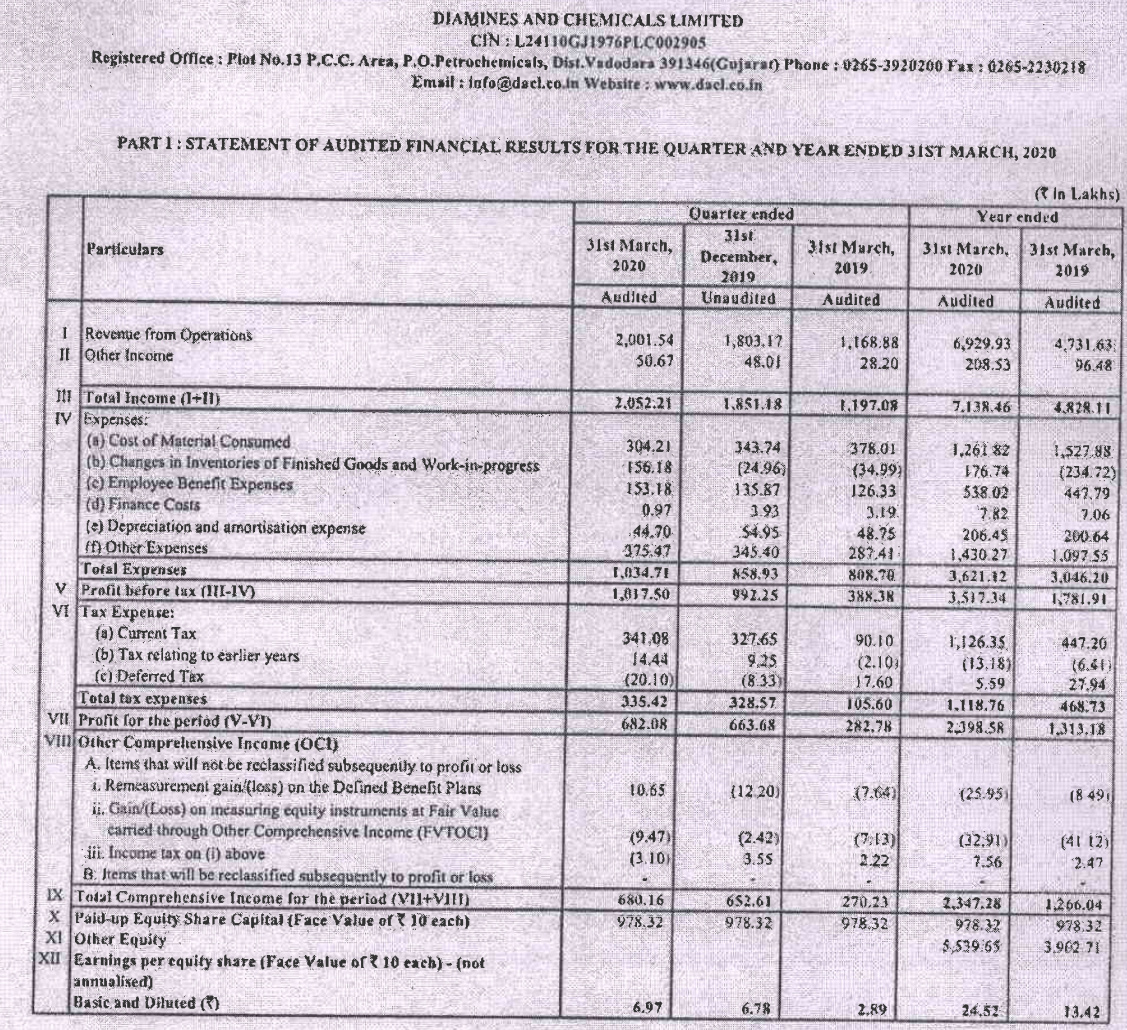

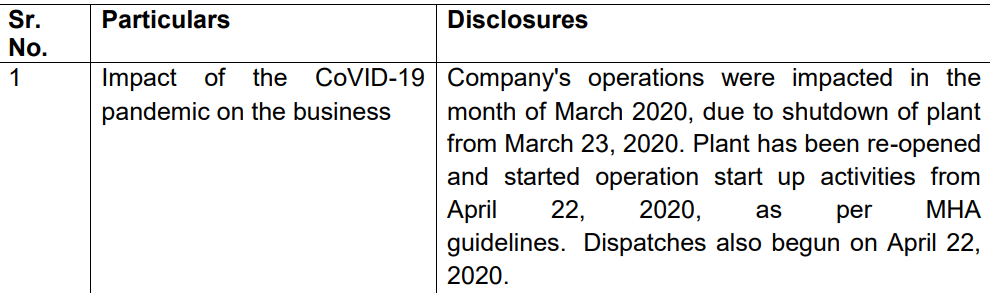

This is an excellent disclosure of the COVID-19 impact:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/386a5d5d-77ab-4e97-9db6-3841ffd3ed8f.pdf

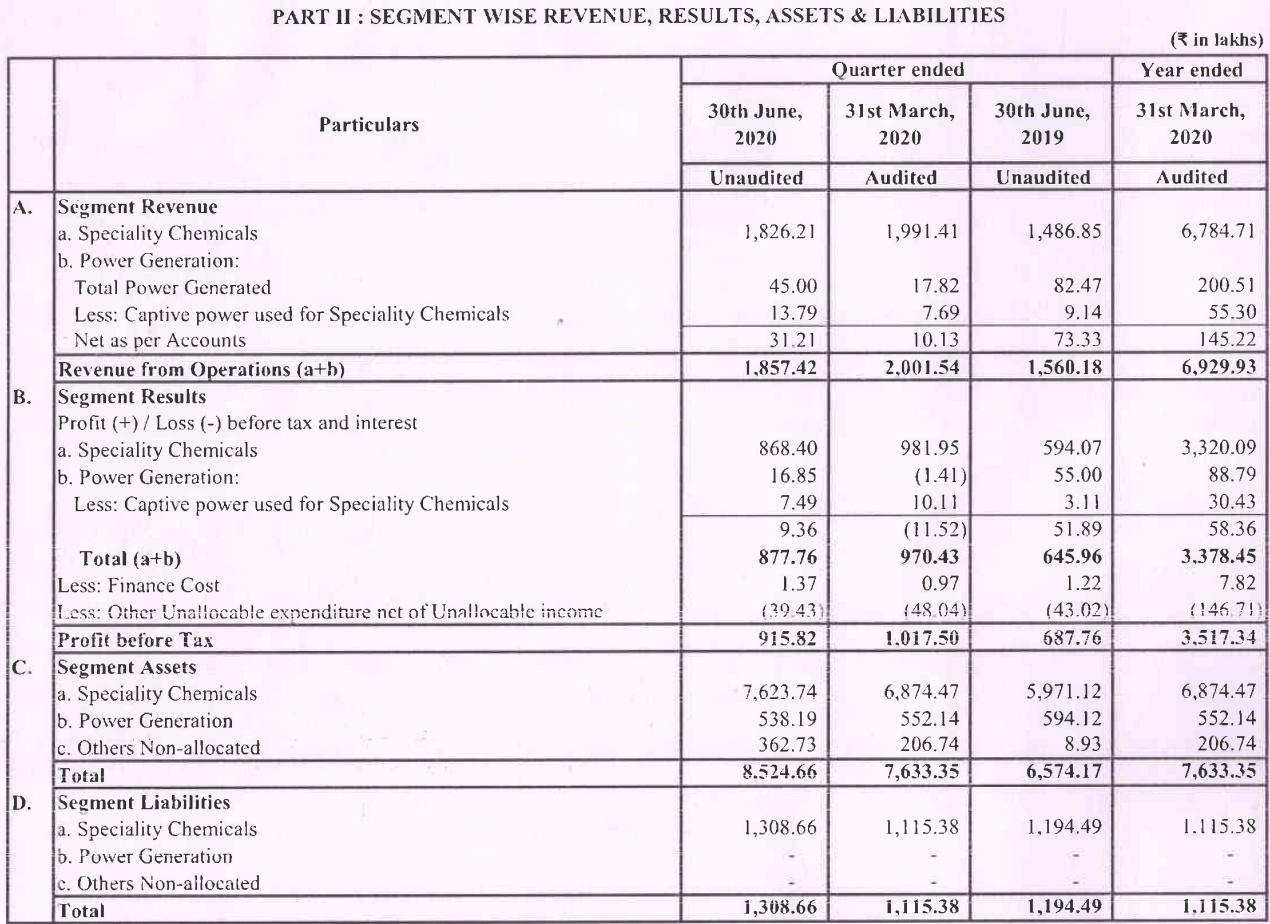

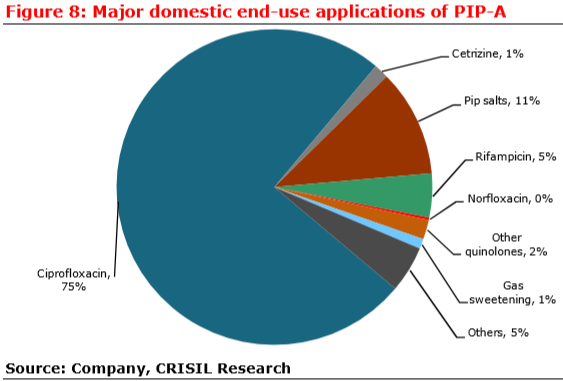

70% revenue is contributed by Piperazine (PIP-A) and 30% by assorted Ethylamines (EDA).

The market:

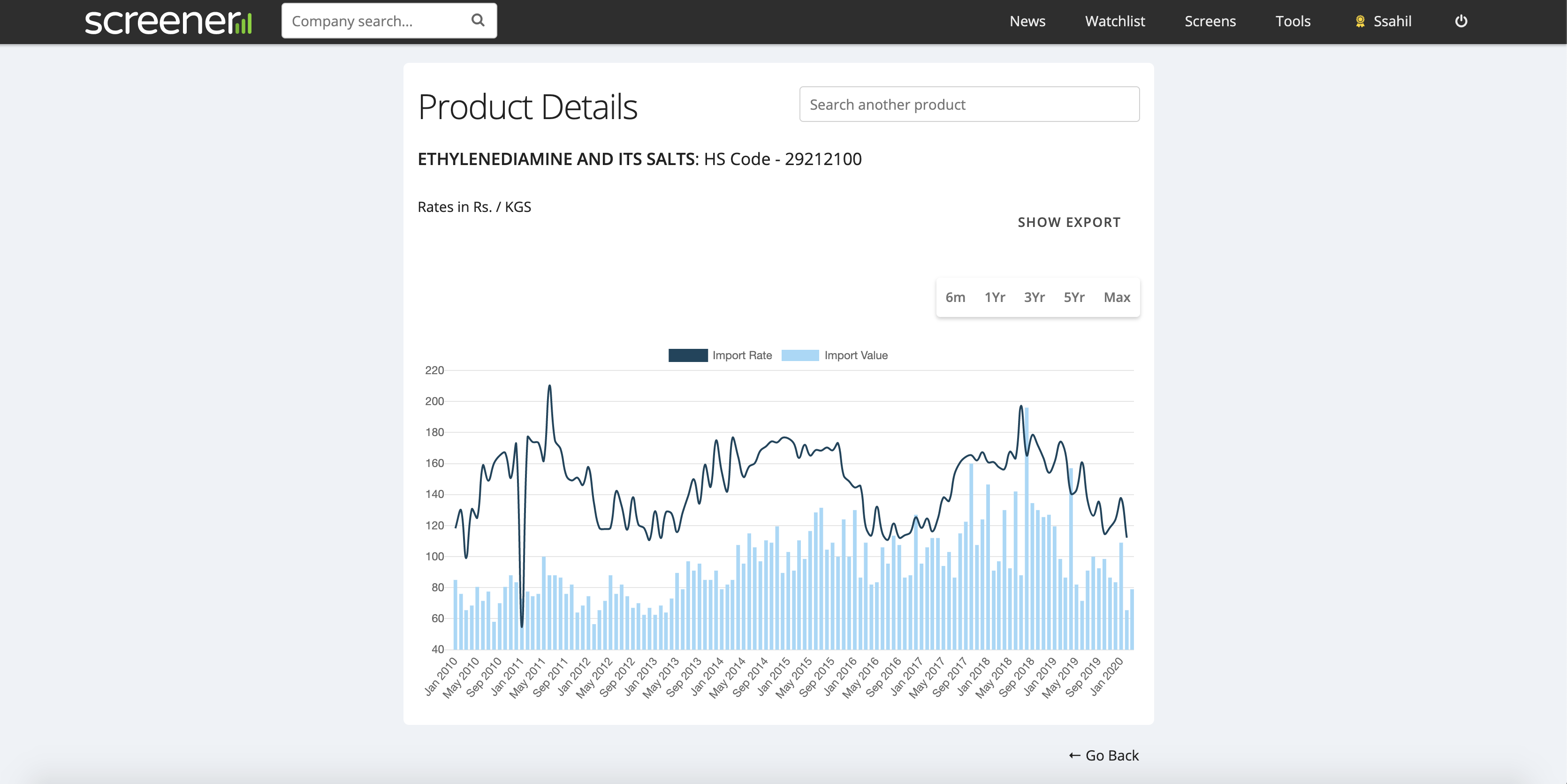

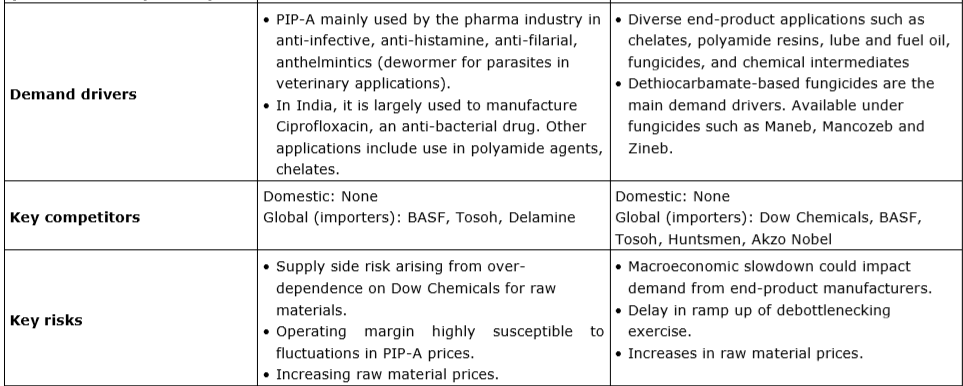

PIP-A is mainly used by Pharma to manufacture Ciprofloxacin. EDA etc. used mainly for Fungicides, and its derivative EDTA in Pharma as chelating agent.

As per CRISIL the company seems to have a very restricted USP due to small size and lack of import restrictions, this may rapidly change if Atma-Nirbhar bharat special focus on Pharma and intermediates really takes off. But something seems to have changed structurally since 2016 to kick the company on a strong performance uptrend.

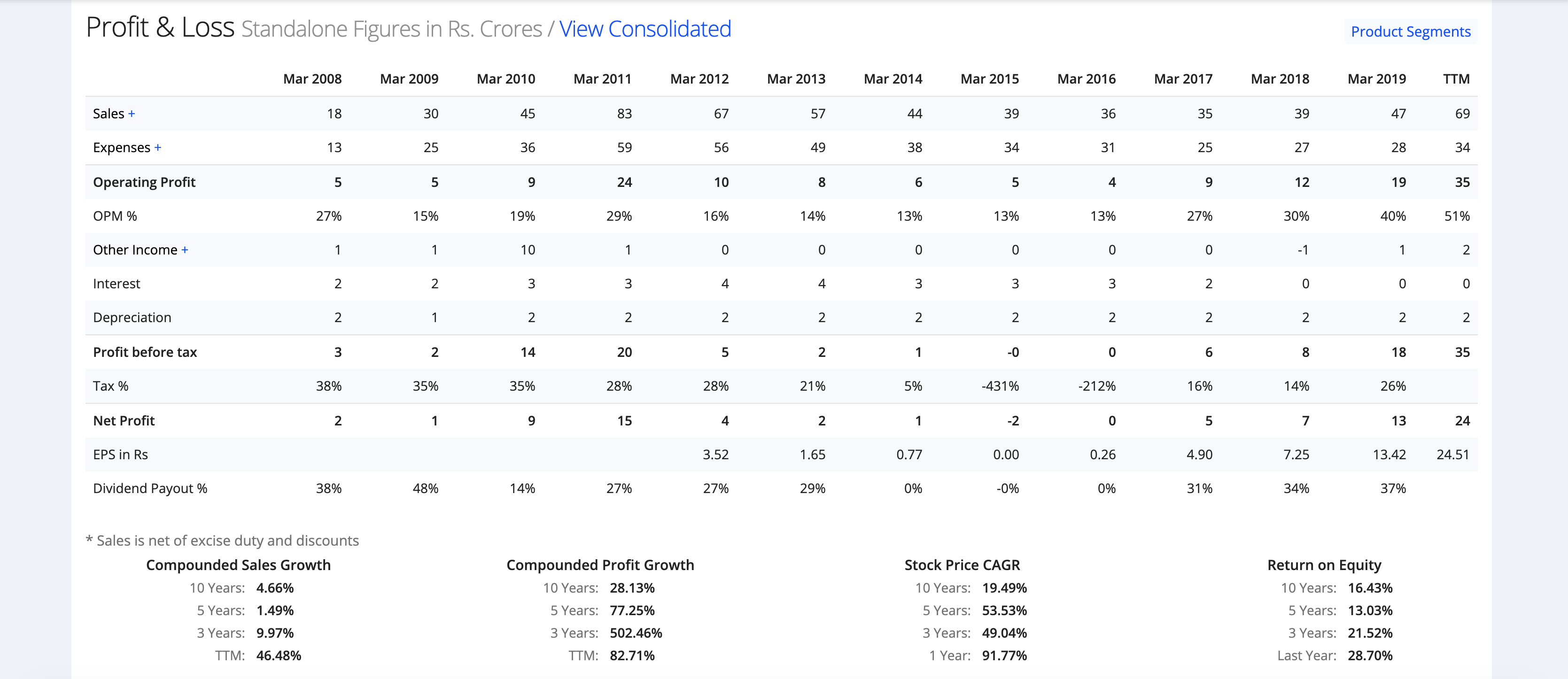

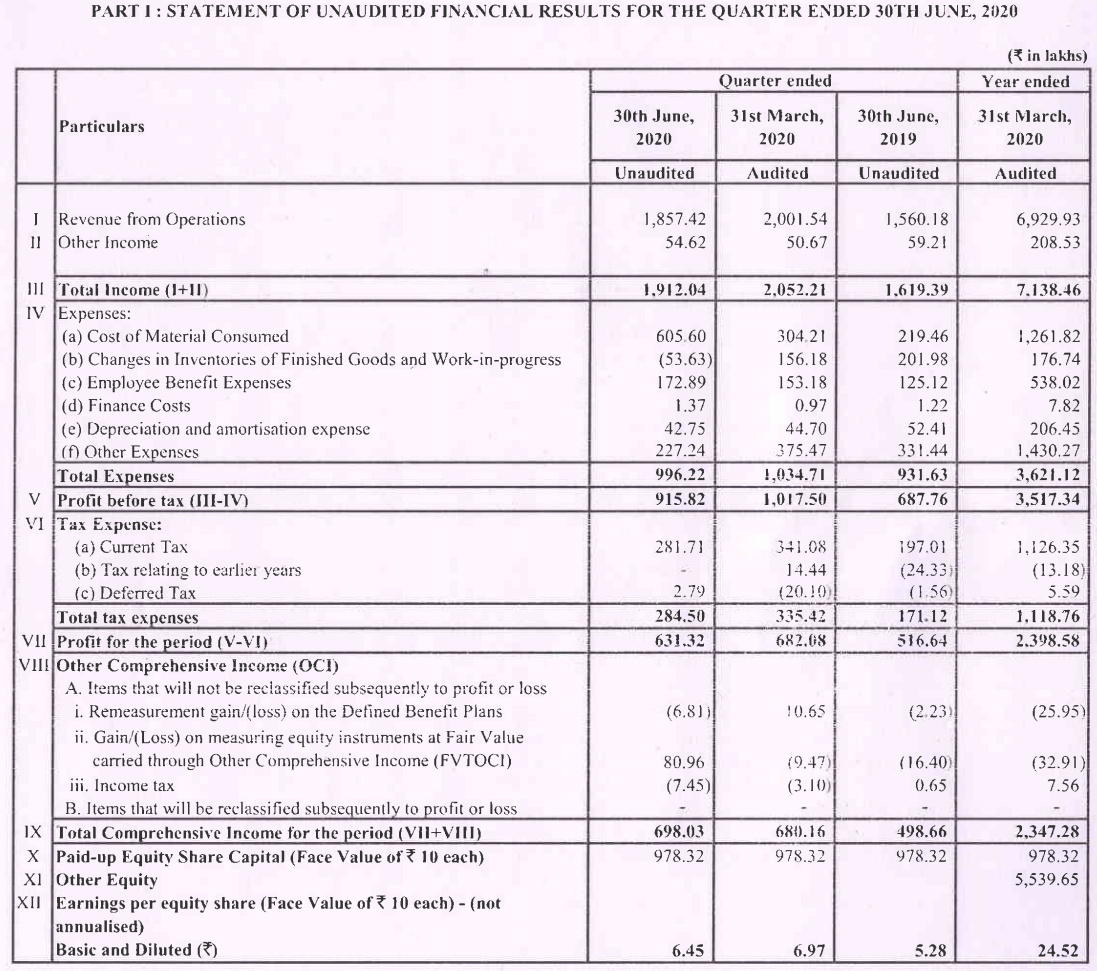

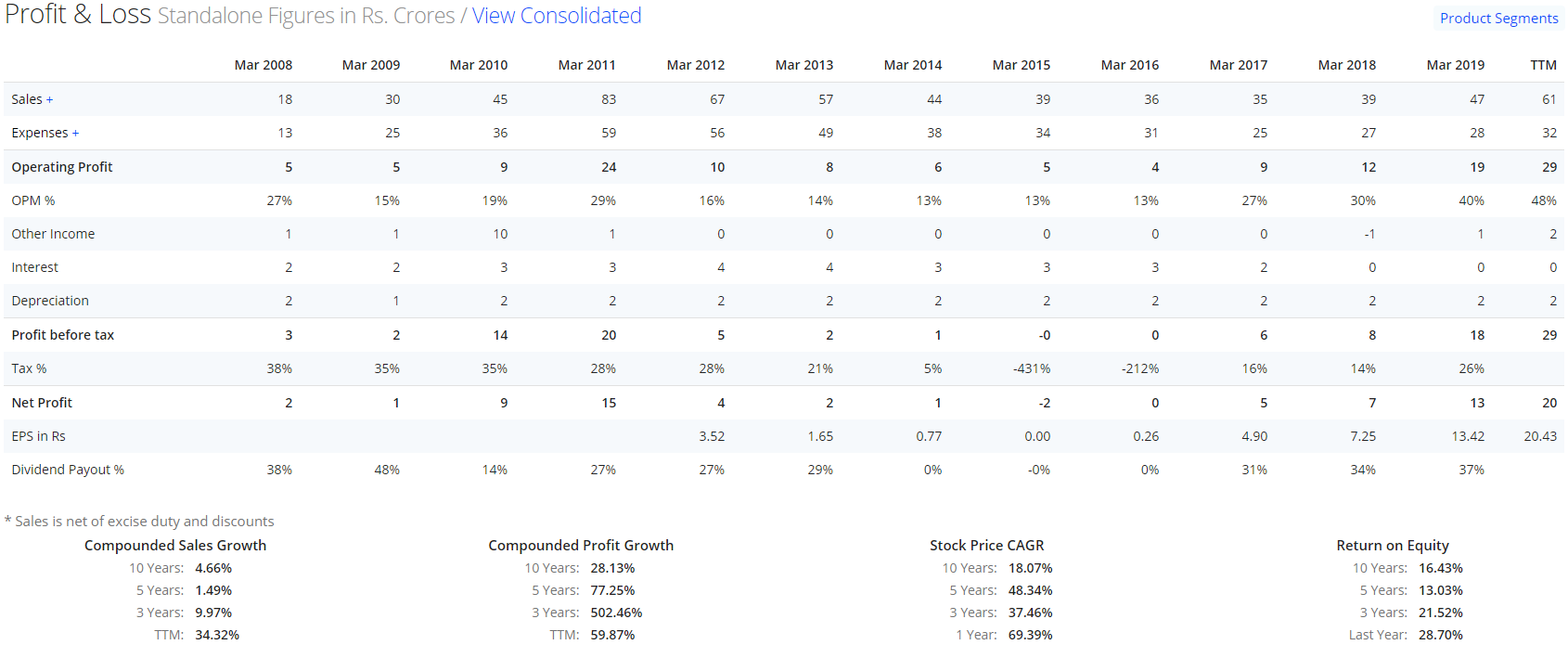

Financials overview:

DACL has zero borrowings.

The only analyst report on DACL: (dated 2011)

https://www.dacl.co.in/investors/crisil_report.htm

AR 2019:

Disc: Invested since 4 months, about 6% of PF.