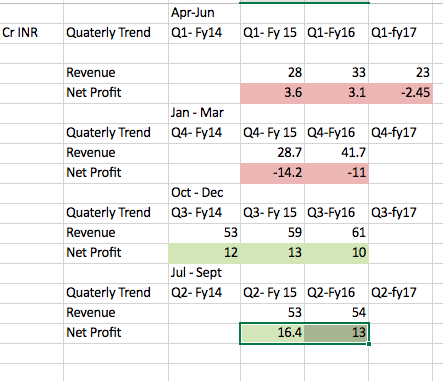

This stock caught my eye when i saw its trading at Rs 197 Cr and it did the profit of RS 27 Cr in FY17. It’s been making profits around RS 25 - 28 Cr from last three years , PE = 7 with dividend yield of 2.98 %.

If you see whole sector seems to be trading at fairly high valuation, most of its peer are near 52 week high. So, at least fair to assume sector is not facing any headwinds.

Stock seems cheap to me its trading at 0.25 times its book value.

Detailed Financial Analysis : Microsoft OneDrive - Access files anywhere. Create docs with free Office Online.

Company has the total long term Debt around Rs 68 Cr /- , Considering company do the net revenue of Rs 300 Cr /- It think its on the higher side.

Ideally i like debt to be around 10% of the revenue 30Cr to be bit comfortable.

Again , As they have marked up the land prices the Debt/Equity went drastically down in FY17.

If you see the total short term debt is around Rs 118 Cr (revenue of Rs 300 Cr) , This shows the very high working capital requirement of the business. This they have mentioned repeatedly in annual report. Tea business require lots of working capital and manpower may be because you can’t run sophisticated agricultures machines (like Tractor etc) to do the job on the hills and that’s the reason availability of low cost labor becomes key differentiator (we will touch upon this later).

Liquidity Ratios doesn’t give me much comfort too, Ideally i would like all of them to be > 1.

This shows company is barely able to manage its liquidity.

The days account receivables seems to be going up (48 to 63 days) , May be demonetization played its role in Fy17.

The important thing to watch out is days payable are way too high, which makes the net trade cycle negative. One possibility could be the retailers who sell company tea are giving them advance payment as a contract to receive fix amount of tea bags every year, If that is the case then its great.

Company has been CFO and FCF positive, makes around Rs 25-27 Cr of profits on around 300 Cr of revenue. (for details please refer the spreadsheet)

Overall i see it as a assets for Rs 193 Cr /- , which generates 27 Cr of profits. Although i like debt to be on the lower side and return ratios to be on the higher side but again as this is available with high margin of safety which subdudes my concerns very much.

What could be the key trigger ?

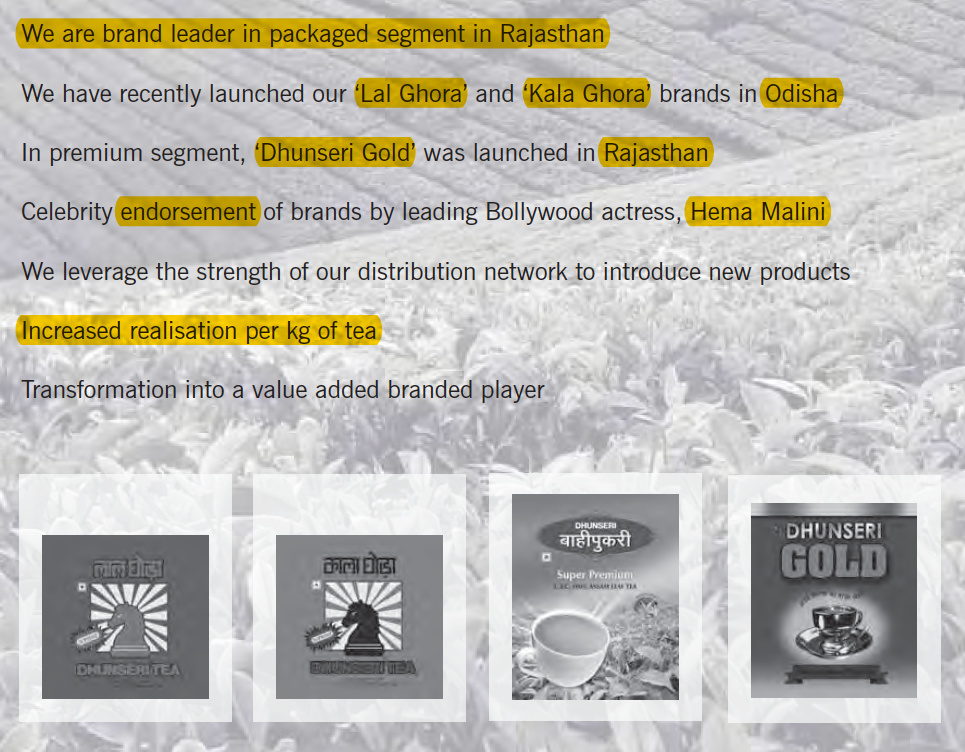

They are pretty much in Rajasthan, There their products are known to the people and are well accepted.

The recent launch in the Orisa is interesting, If this works out they may start expanding into other states as well. Which could potentially drive the growth for the company and help them sell 100% of the Tea production as a value added product (right now it is 35%).

Recent launch in Orisa April 2017

Management Analysis :

Salary 52.7 Lacs seems to be adequate compared to 27Cr of profits company make.

// promoter’s stake has increased recently

They increased around 5% stake in the company in Fy17.

To me overall it seems to be low risk, Average reward type stock, I am hopeful it could give 14-15% return from current price as monsoon were good. Moreover their Orissa expansion could surprise on the upside and their focus / expansion into Africa seems like the logical thing to do.

Disc : Invested.