DHP India - Annual Report FY20 Review

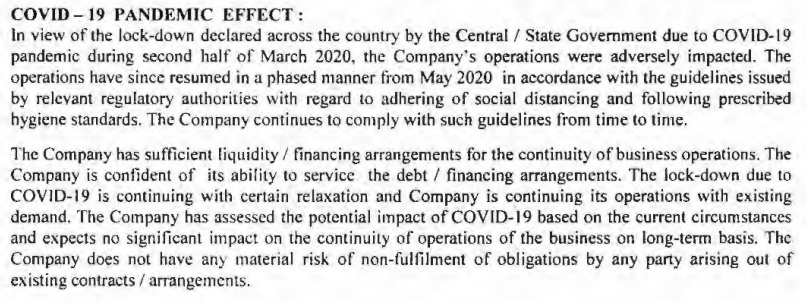

COVID Impact

Company expects no material impact over the long term.

Pain over the short term is expected in any case.

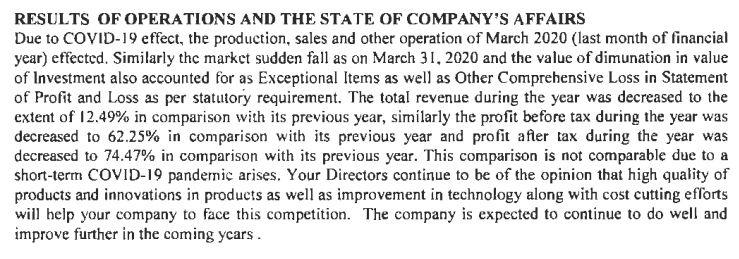

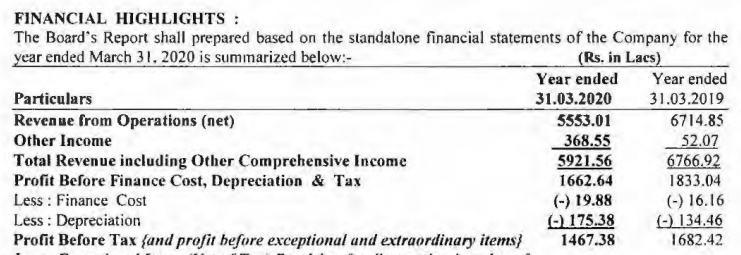

Results - At a Glance

A flat year at best. I ignore anything after this because the loss from Mutual Funds are included, which is not operational in nature.

Key Shareholders

Dr. Vijay Malik increased stake during this year too.

Secretarial Compliance: No deviation

Audit Compliance: No deviation.

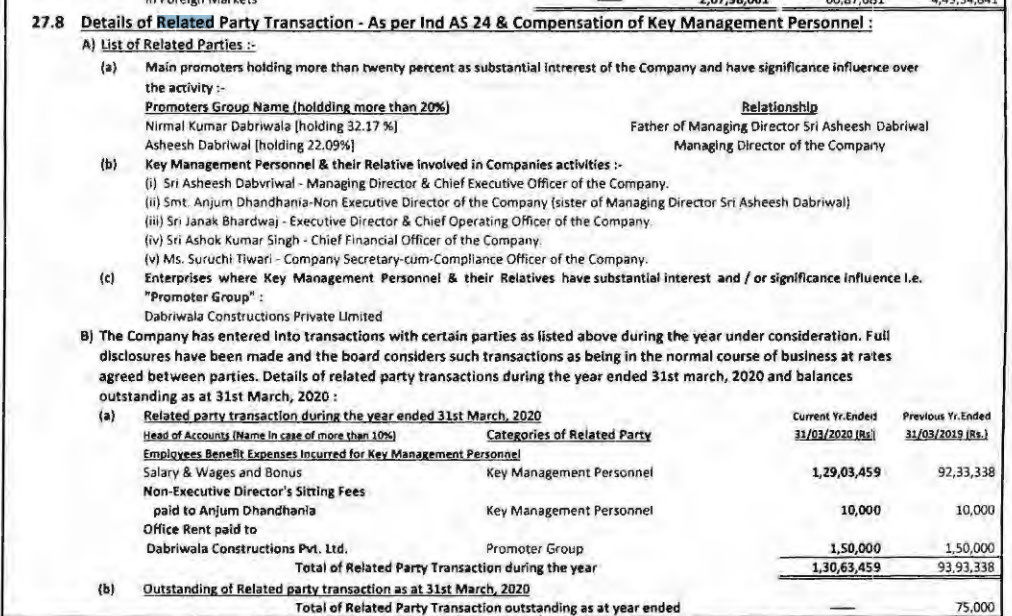

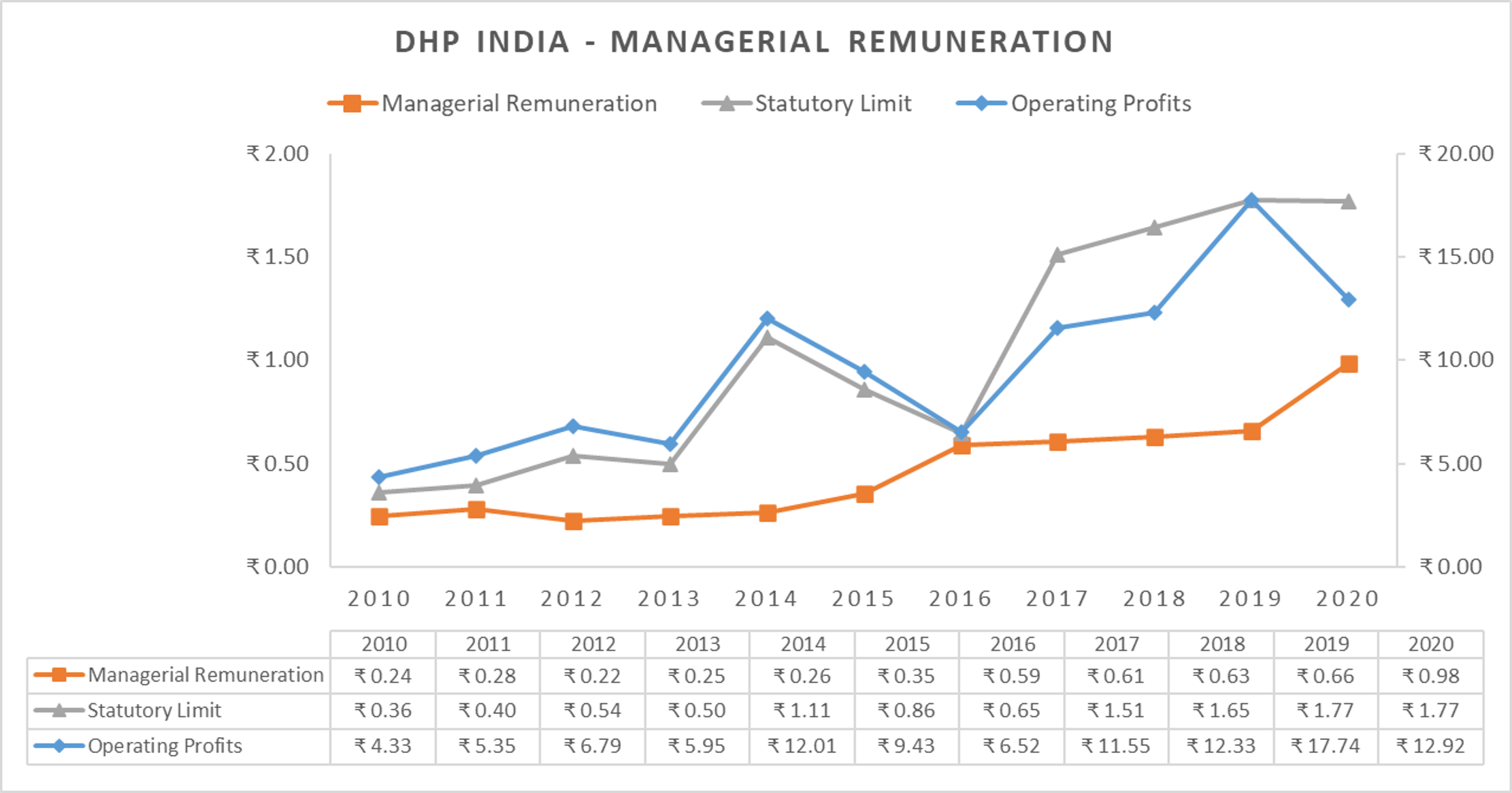

Managerial Remuneration

Managerial Remuneration has been well within the Statutory Limits since 2010 (Annual Reports not available in BSE before this).

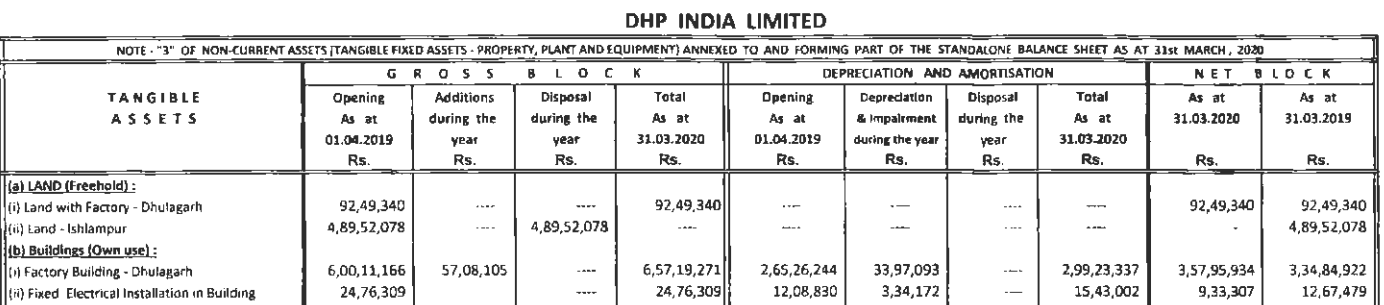

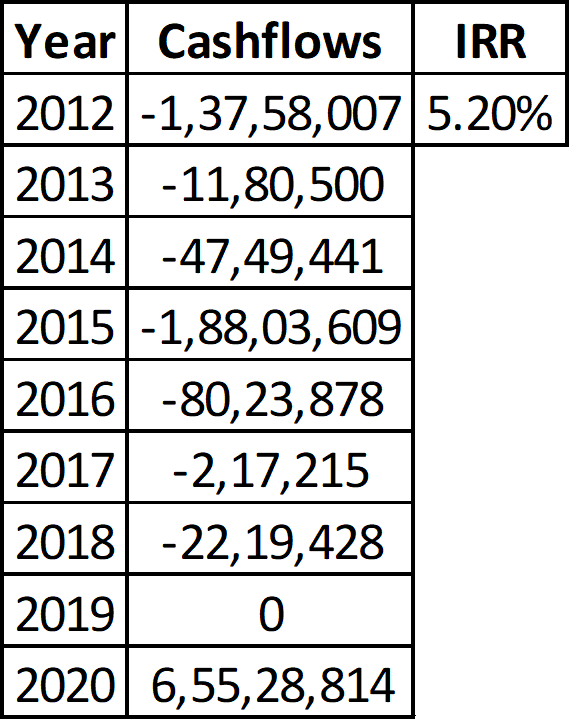

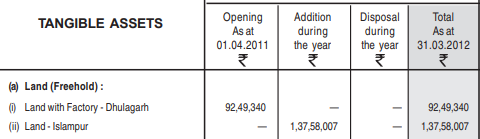

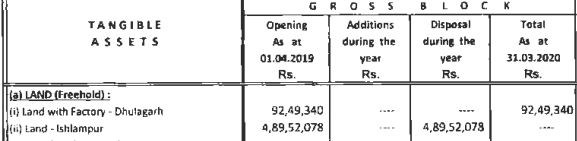

Ishlampur Land

This land parcel was acquired during FY12 at a cost of Rs. 1.37 Crores.

It was sold in the last quarter.

However, over the years there have been multiple investments in this land in between as well.

The IRR from this land seems to be a meagre 5%. I still do not know why the land was sold and what the company plans to do with the proceeds. Currently, the proceeds seem to have gone into the bank and not into Mutual Funds, which is a promising sign, I guess?

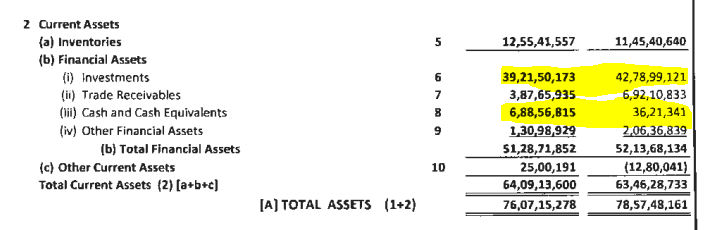

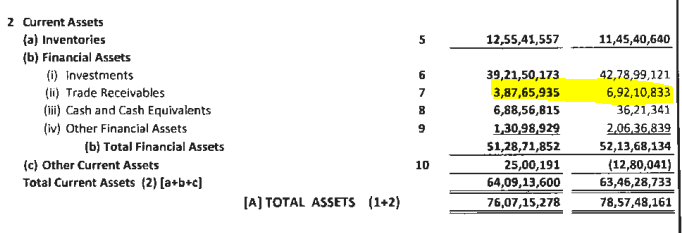

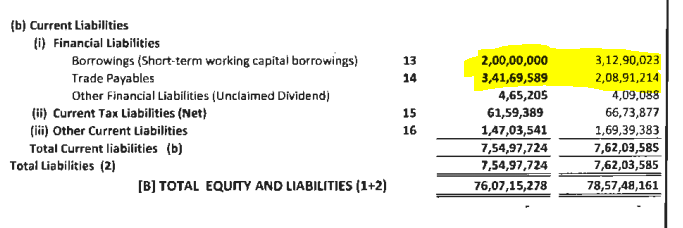

Balance Sheet

- MF investments have reduced from 42 Crs to 39 Crs - in case you are tracking this at all.

- Ishlampur land proceeds has been put in Bank account (For now).

- Receivables decreased and Payables increased - poor Working Capital management for this year. Last year was way better.

- Debt decreased, which is good given the situation we are in.

- The company has no Long Term Liabilities at all. Talk about B/S strength!

Cashflow Statement

CFO was flat, but Net CFO is better thanks to the tax break.

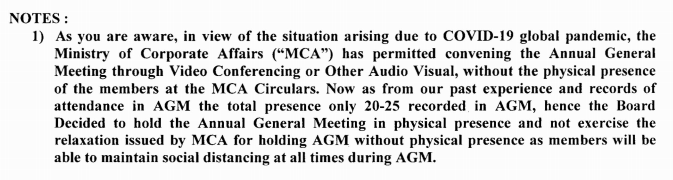

Annual General Meeting

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0d2ecf9d-7010-4524-a937-a35540ede3b6.pdf

AGM, unfortunately, is still going to be conducted in physical format. If anyone is attending, please ask the question on why the land was sold and how the proceeds are supposed to be utilized. Also, the question on why the company is not liquidating Mutual Fund investments and distributing it as dividends can also be asked. But from my experience, B2B companies are often stringent with cash. We can’t blame them. In a crisis, B2B businesses with little to no safety net are the first to go bankrupt.

Overall, I would say a decent year. I look forward to at least one more quarters’ results before deciding whether or not to increase my stake. I mostly want to understand whether the crisis will damage the B/S or not. Everything else seems to be in order.