Did anyone attend AGM today? Plz share the notes

2 Likes

I recently went through the past AR’s of the company. Just sharing some things that stood out:

1.) Company is moving into higher quality products

*Average selling price and production numbers have been estimated using electricity consumption data given. Figures won’t be exactly accurate but they’ll be roughly in the right range.

| FY07 | FY08 | FY09 | FY10 | FY11 | FY12 | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ASP | 68 | 86 | 86 | 95.5 | 85 | 91.5 | 119 | 121 | 155 | 152 | 178 | 200 | 175 | 233 |

| Production (no of pcs in lakhs) | 14.6 | 13.6 | 14.6 | 19.2 | 27.6 | 27.2 | 21.2 | 32.6 | 23.5 | 19.8 | 22.5 | 22.5 | 32.3 | 21.7 |

From the above data, we can see that production volumes have largely been stagnant over the last few years, but selling price has gone up considerably since FY14.

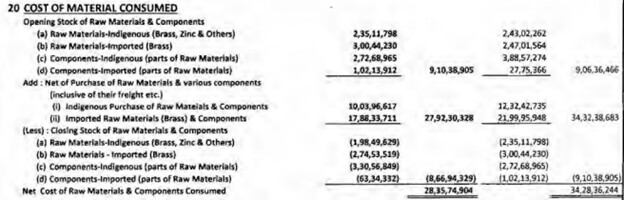

Another data point confirming this is the fact from FY14 onwards, company has started importing 50% of its raw materials (brass, components etc), whereas earlier they were exclusively using Indigenous materials. This is also the year when they started selling “Brass accessories” which led to a jump in Sales.

2.) Sale of land in Islampur - I must admit I was quite surprised to see this. Even though growth has been stagnant over the past couple of years it was sort of reassuring to see that they have land which could potentially be used for expansion.

One explanation for this could be that at their existing factory they have an installed capacity of 45L units per annum (as mentioned in the FY11 AR) which means that they only use about 50% of that on a regular basis.

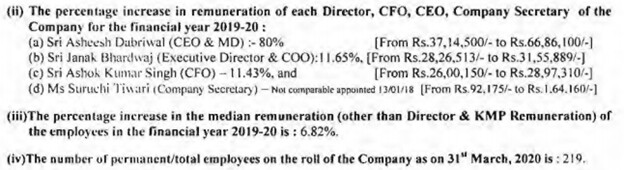

3.) Management remuneration - couple of years that stood out for me were FY12-14. Company was in need of funds because of increasing working capital and capex requirements. Company stopped the dividends and MD’s salary reduced by 50% to 6L p.a. for these 3 years. No cut was made to the COO and CFO salaries.

This to me highlights the integrity of the promoters and the fact that they think highly of their employees. Also shows that they don’t consider the company to be a cash cow for themselves, but think of it as a long term asset.

They promptly resumed the dividends in FY13 once the crunch was over.

FY20 has seen a spike in MD’s salary however. It would be good to see an increase in dividends going forward.

16 Likes

If anyone wants a list of potential competitors, here’s a compilation:

Indian Competitors

List of approved Regulators producers in India (http://peso.gov.in/PDF/List%20of%20Approved%20LPG%20Pressure%20Regulator%20Manufacturers.pdf)

Foreign Competitiors

World LP Gas Forum Brochure (https://www.yumpu.com/en/document/view/43794279/24th-world-lp-gas-forum-wlpgas-2011)

European LPG Congress 2021 - List of Exhibitors / Floorplan (https://www.europeanlpgcongress2020.com/exhibition/exhibition-floorplan/19) - DHP India is taking a stall here.

I intend to study all of them, at least on an overall level, when I get the time.

11 Likes

1 Like

Looking at the Operating Cashflows will give us the more unbiased picture. The situation is still anemic due to the virus, I presume.

Interesting to see that all cost items are more or less the same, when most companies are trying to cut costs and improve Margins.

But the silver lining is that they’ve paid off whatever little loan was present (I think they might have used a part of the proceeds from land sale). Now only a few lakhs remain.

4 Likes

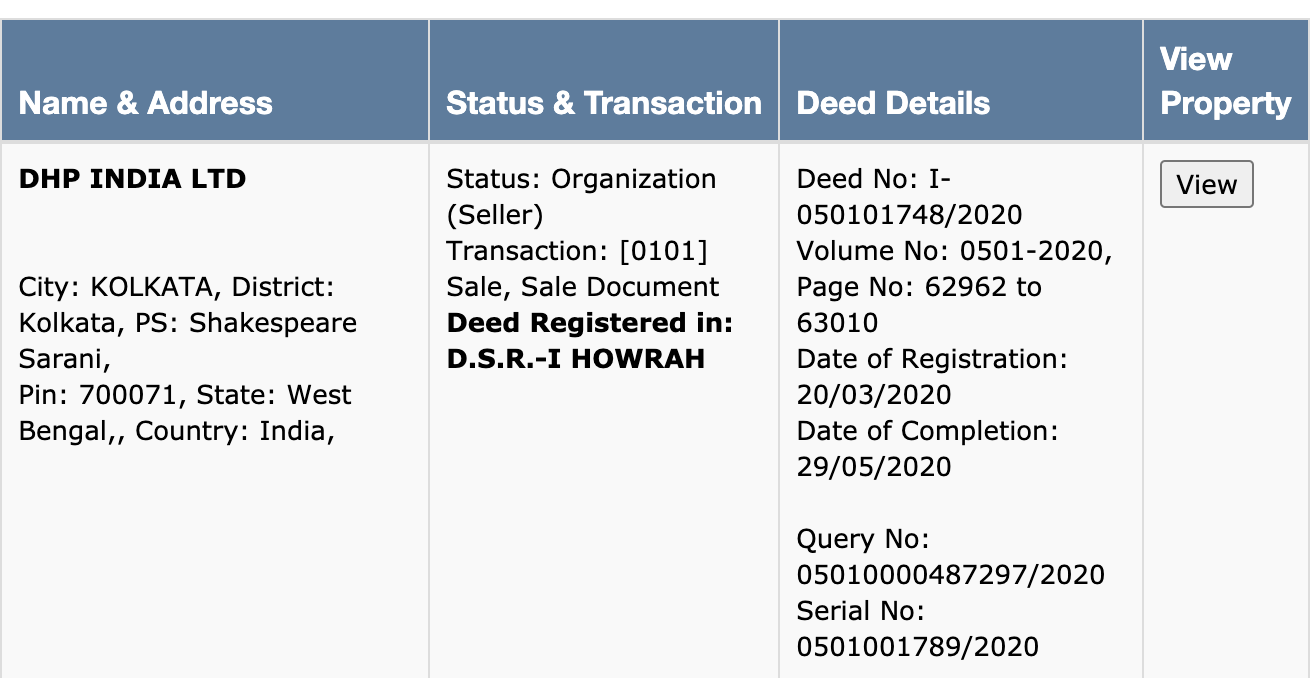

Land sale has happened on March 20th according to WB land registration site. The buyer is Gypmart Pvt Ltd.

My assumption is management might have panicked about prevailing situation and wanted to have ample liquidity coupled with thinking that markets might not bounce back quickly.

Thanks,

Rohil

6 Likes

why they are not going to expand and why they keep money in Mutual fund. in this case we can directly invest in mutual funds better than invest in this comapny

any listed peers in manfacturing pressure gauges

None as far as I know (At least with the Core Business of manufacturing Gas Pressure Regulators and parts).

For general list of local and global competitors, see a few posts above where I’ve given references.

3 Likes

Hi all, new to this thread but I don’t see enough discussion on the company’s opportunities and expansion plans. What is DHP going to do to grow? At present, it looks like an annuity business with investments

Yes growth is one concern plus a have a few more…

Both Domestic aswell as export revenue sees a fall in FY20 as compared to FY19

Overall revenue fall = 6714L-5553L = 11.61 Cr; while export revenue fall contributed 5646-4785=8.61Cr

So balance, roughly 3 Cr revenue fall was from domestic market; Is the domestic market itself shrinking due to Piped gas? But this is roughly 30% fall from last year;

They might be losing market share in India due to price sensitivity of Indian Consumers? However this is B2B and that too in an area where switching to low cost inferior product can be dangerous; I wonder why they are losing market and have decided to shift focus to export instead!

-

While MD salary jumps 80% in the year revenues have fallen around 20%

-

Wonder why do they say, they have no commodity hedging; should’nt Brass constitute major portion of their cost?

- Also is it a good accounting practice to adjust the P&L as per the current value of MF holdings; it seems conservative and hence good; but today’s DTA will become next years Deferred Tax liability

4 Likes

I suggest you read up on the Annual Reports of DHP India. There is no ‘domestic business’. The only Revenues from India are from selling the Scrap parts remaining after the Production is done for exports.

It constitutes 10-15% of Revenues, but it would be a stretch to call it an entire market or business unit by itself.

On many of the previous years, the MD’s Salary wasn’t close to the Statutory Limit. The current increase still puts it within the limit. As long as that’s the case, we should have no problem as Shareholders.

Would you have liked it better if the Salary was higher initially and the current year’s increase was only a small percentage?

I don’t think smaller companies do a lot of hedging activities. But it’s a valid point for when they do scale up.

The laws changed last year and many companies are forced include MTM values in their P&L too. Even Warren Buffett has been doing it and he expressed his unhappiness in one of the earlier Shareholder letters (Not that I’m making any direct comparisons - just pointing out that Accounting Rules may not always make sense).

4 Likes

- MD remuneration increase after 5 yrs, coincidentally when sales down.

- They do export mainly to get higher margin.

Sir, do u have addressable mkt size data type information

I feel al of these salary etc points are moot in the absense of growth. That is the key point of discussion, can DHP grow?

If you see the section g) Operational performance in my previous post taken from this years Annual Report, it states, they have consciously shifted focus away from local market to Exports… This is what i am talking about, as to why are they not competing here. India is a big market and Piped gas is still a long time away for majority India.

Do we have information on their client concentration? Apart from About Us | Rotarex SRG do we know of any other clients of DHP?

The market is sensing the growth concern.

Plus mutual fund investments have already been highlighted as a risk!

On the positives with growing commodity prices and large inventory at DHP, next year could be much better even with no growth in unit sales plus the mutual fund investments will also turn from loss to profit!

Disclosure: Invested a small portion of PF; just studying the various risks and growth opportunities

1 Like

The Global Industrial Gas Regulators industry is around $10 Billion or Rs. 73,000 Crores in size. Of course, DHP India supplies mostly to US and Europe. We also know for a fact that there is a lot of competition.

The Global Gas Cylinders Market Size is also about $10 Billion in itself. But DHP India only supplies Parts and Accessories to this market, so their actual Addressable Market may be close to ~5% ($500 Million or about ~3,500 Crores). Once again, we don’t know the competitive scenario here.

Rest assured, the market size is considerably high compared to DHP India’s current Sales levels. We just don’t know the exact figure.

As Warren Buffett would put it: “You don’t need to know a man’s weight to know that he’s fat.”

There’s also a ton of Competition in India and hence, Margins would be low. It’s not a Risk worth taking in my opinion. But who knows? Maybe you’ll turn out to be right. I am happy with what DHP India is doing right now.

Search this thread for that information. I had posted a list of 4 customers from different regions. Also generally, request you to read the entire thread before responding. It avoids repetition and saves a lot of time and effort for everyone.

8 Likes

DHP is a highly illiquid stock. When someone wants to buy a large quantity, the stock shoots up like it did today. They have a huge investment in equity mutual funds that were written down during the meltdown. Now, happy days are back and we are seeing the investment income soar for DHP

2 Likes

I just read one up on wall street and one point is about the net cash per share.

Which is ( current cash + investments ) - long term liabilities and divide by the number of shares outstanding

Dhp has about 46cr cash and investment and around 768000 shares outstanding which gives it around 598rs per share as cash.

Can anyone point out if this is correct ?

Yes it’s correct , but total outstanding shares are about 3 crores I believe.