4 Likes

Is DMCC not going to have an earnings call this quarter ?

They usually do it Half yearly. At the end of Q2 & Q4

6 Likes

Is there any other company which has done the same as DMCC ? I mean setting sulphur ( any commodity) as a bedrock and going into downstream products. I’m asking this bcoz DMCC is a small company and if they are able to play this part then the story looks very interesting. Any company which was small as DMCC and was able to do this in the past ?

Yes Deepak Nitrite did it in a similar way.

See the twitter thread https://twitter.com/soicfinance/status/1483795317627965441?s=20

1 Like

DMCC had embarked on a capex plan of Rs110 crore of which Rs70 crore capex has already been completed. This includes Rs10 crore incurred for de-bottlenecking at Roha, another Rs10 crore for setting multi-purpose plants at Dahej and Rs50 crore has been invested in new bulk chemicals facility at Dahej.

Bulk chemicals- Dahej- 50 crores capex done @1x asset turn - revenues will be 50 crores by end FY’23.

Speciality chemicals- Dahej - 20 crore capex done expected to commence production by Q4 FY’22 @ 2x asset turns - revenues will be 40 crores by end FY’23.

Intermediates plant -dahej - 20 crore capex to be commercialised by Q1 FY’23.

@1.5x asset turns , revenues will be 30 crores by end fy’23, but utilisation will be for 3 quarters, hence 23 crores.

Total incremental revenue from capex: 50 +40 +23 = 113 crores.

This incremental revenue will be over base of 72 crores in Q2 FY22, which when annualised gives revenues of 290 crores.

Hence FY’23 revenues to be in range of 400 crores.

EBITDA margin :18%

EBITDA: 72 crores

Interest: 6 crores

Depreciation: 10 crores

PBT: 56 crores

Tax:25%

PAT: 42 crores

At current map of 950 crores, it is trading at 22 times one year forward earnings, which is not too pricey.

Ultimately, it depends on how well the company is able to sweat the incremental assets which will come online between this and next quarter.

If company can walk the talk on this "Focusing only on Chemicals where the company

envisages an operating margin of 30 % + and a payback period of no more than 3 years.", I think upside could be significant.

Disclosure: Studying, no investment yet.

21 Likes

1 Like

Concall notes:

- Next quarter to show true potential of newly invested capex. With new capex we’ll have twice the capacity of what we used to have

- Growth possible for old strategy of operating in niche areas where little or no competition?: Haven’t come close to exhaustion of this model.So no plan to change.

- Further expansion plan: We’ll tell later at appropriate time. Lets digest the current investment first.

- With new Operating cash flow coming : debt reduction + new investment like energy recovery.

- Boron Business: Positive comment. Improvement in supply. Expect to have better boron business in coming months. debottlenecking ahead.

- New products launched: These are introductory products, Speciality chem in nature. 50-100 cr market potential.

- Margin: Able to manage it. By passing on price. Rolling contract for spec chem quarterly or 6 month. Absolute number is okay(it’s like raw material cost was 100 and product cost was 120, now both increased by 20, it will causes the margin to shrink but the actual profit will be same).

- 98 cr outflow due to capex in cash flow statement of fy22+CWIP of 65 cr in balance sheet of fy22: Cost over run due to giving old value in presentations + some other projects like (fire hydrant system+zero liquid discharge facility+safety+environmental)

- Working Capital( Negative this year): Taking credit from suppliers. Good demand for products so debtors day also under control.

- peak debt (working capital+long term): It will grow. 100 cr long term debt. WC difficult to say depends on raw material price.

- Jewan Patwa: 200 cr capex(98cr in fy22 cash flow statement+47 cr fy21 cash flow statement+65 cwip in fy22 balance sheet): same reason as stated earlier.

- Long term contracts are for how long: perpetual contract as long as customers are satisfied we renew it. no intension to make it monthly. it will increase complexity. raw material fluctuations will dampen out.

- Our customers surely have other supplier also. But we are the significant supplier.

- Sulphur price increased hugely: Passed on some price for H2SO4. But can’t control price pass on. since not in our control. However we get some premium for our reliability.

- Backward integrated for spec chem.how much cost benefit: It depends on product and time to time. Safety + supply chain advantage.

- Bulk chem capacity: is it enough for downstream spec chem?: for next several year will have enough.

- Intermediate Plant at Dahej: It has single product. one customer gets 50% of the production and rest to multiple customers. long term contract with customer getting 50% of production.

- spec chem volume growth in fy22: 10% growth. could have been better if logistics was there for foreign customers. came from top 3 products.

- new capex coming live in q1: Market visibility is there. Some good impact in Q2. ramp up later.

- new H2So4 plant at dahej is not running in full utilisation. q2 it will be running at better utilisation. as we commission the downstream products.

- Scenario with New products sulfone, thiol, amide: sulfone’s growth is good. thiol not happy however it’s growing. amide has become like mature product.

- Can we expect all the new capex to be fully utilised at fy23 end: like to do so. but depends on things like logistics. some products were going to foreign. market visibility is there for those products.

- Sulfone revenue and vol growth in fy22: it had good growt and still growing. doing debottlenecking.

- Growth in fy23 will come from boron+new plants. boron peak sales happened in 3 yrs back. now it’s down 20-25%. Boron raw material availability is improved.

- Other expenses has increased hugely this quarter: Due to logistics cost due to Container cost. Container rates increased more than 4 times. Situation has not improved. Logistics supply chain is across all the Imdustries.Most ships are stuck at china and us.

- 5 years later where do we see ourselves in terms of spec chem and bulk chemistry: Our usual revenue split used to be 1/3rd bulk rest spec chem. It will happen once we increase our spec chem capacity. normal spec chem is 2/3rd. now it’s 50:50. Difficult to say what will be 5yrs later.

- One dahej plant is mainly for export market.

- At Roha h2sp4 plant 90% capacity utilisation. dahej h2so4 plant it’s lower.

- if prices of raw material goes down it will look like fantastic margin. but that will not be sustainable just like today’s low margin.

- top 3 products contributed 2/3rd of revenue.

a. Temporary headwinds: RM cost impacting gross margins, logistics issue impacting foreign revenue, fuel cost

b. margins will improve with rm cost going down, logistics issue improving, fuel cost going down and most importantly increasing speciality chemicals. Revenue will increase as all the new plants fully ramp up. So with margin expansion + revenue increases profits can increase even faster with respect to present situation with multiple headwinds.

c. Management is not giving any forward looking statements regarding revenue of fy23. It will not be surprising if they deliver good growth without promising anything.

Disclosure: Invested

27 Likes

5 Likes

FY 22 AGM Notes - Link to Audio

- We should have started the capex bit earlier (little more conservative , due to this we were unable to supply)

- Current Capex will take us to 500cr Revenue (need to make capex for the growth beyond this )

- Sulphones - One of the Sulphones doing pretty well and completely sold out (large room for growth, not yet made any investments on that )

- Electronic Chemicals - There is not enough demand in India || In India air quality and water quality is not conducive to make electronic chemicals

- Future capex is on Specialty chemicals

- 2/3 capex is borrowing

- 5 Phds working in R&D and QC

- Two New products commercially launched last year - did reasonably well, expect to grow in coming years

- Export - Specialty chemicals did well

- EU-Ukraine Crisis - This a area for concern , no direct problem to DMCC but for all the global companies

- RM Prices - Gone up substantially in last 12 months (Pass increases are passed on but unable to do on Bulk Chemicals)

- Roha - Carbon negative (will achieve this in Dahej as well)

- Boron - Capacity is not fully utilized due to raw material shortage

- 400 people working on Roha and Dahej

- Setting up new R&D lab in Roha and Dahej

- We are strong in Sulphur and Boron chemistry , don’t see we are going into other chemistries

- 1-1.5x asset turnover on bulk chemicals, specialty 2-2.5x asset turnover

- We don’t rely on Ukraine or Russia for RM

- Borrowings are USD, EUR and INR terms

- Bulk plant running at 90% capacity

- Immediately two capex plans

- We don’t burn too much of power, we rely on heat recovery , dahej grid independent will achieve this at roha as well

- Sulphuric acid plant - 350 Ton at Roha - 350 Ton at Dahej (no need to make any investment in this for next 5-10 years)

- In three products we are top in the world

33 Likes

Azelis is very strong in Sulphur and Boron Derivatives , they have base in India as well.

Some more insights about DMCC from their EC Report (Page 63 Onwards)

DownloadPfdFile.pdf (7.3 MB)

@phreakv6 @Worldlywiseinvestors or any chemical experts can you please dig deep and educate the VP tribe which are these downstream products that going to be

- Import Substitutes

- High Margin

Thanks

4 Likes

Company has changed their name to "DMCC Speciality Chemicals Limited” w.e.f. October 12, 2022.

May be they are trying to make themselves known as a spec chem player & showcase that they are no longer a commodity only player. Anyway no change in fundamentals.

D: Invested, no transaction in last 6 months.

7 Likes

I think a good development as Morarji name was a overhang from old times and lets hope market gives better valuation with new name . In fact new name is a better reflection of their current status

Out of curiosity, what’s the relation between name and valuation? Are there any known cases where purely a name change led to higher valuation?

1 Like

Very simple . Lots of people buy stocks based on hype or for being from a hot sector . So if the company makes Biryani and has a name like a pice hotel, people may not know it sells Biryani . So DMCC is just letting fools know that they make specialty chemical and not only sulphuric acid.

Considering even moneycontrol itself is fooled by presence of metal in name to categorize Shivalik Bimetal Controls as a steel stock ,one should not be too critical of the DMCC management.I myself have observed Sell calls on MC on Shivaliks forum on days when metal stocks go down and coincidence or not stock price go down as well.

19 Likes

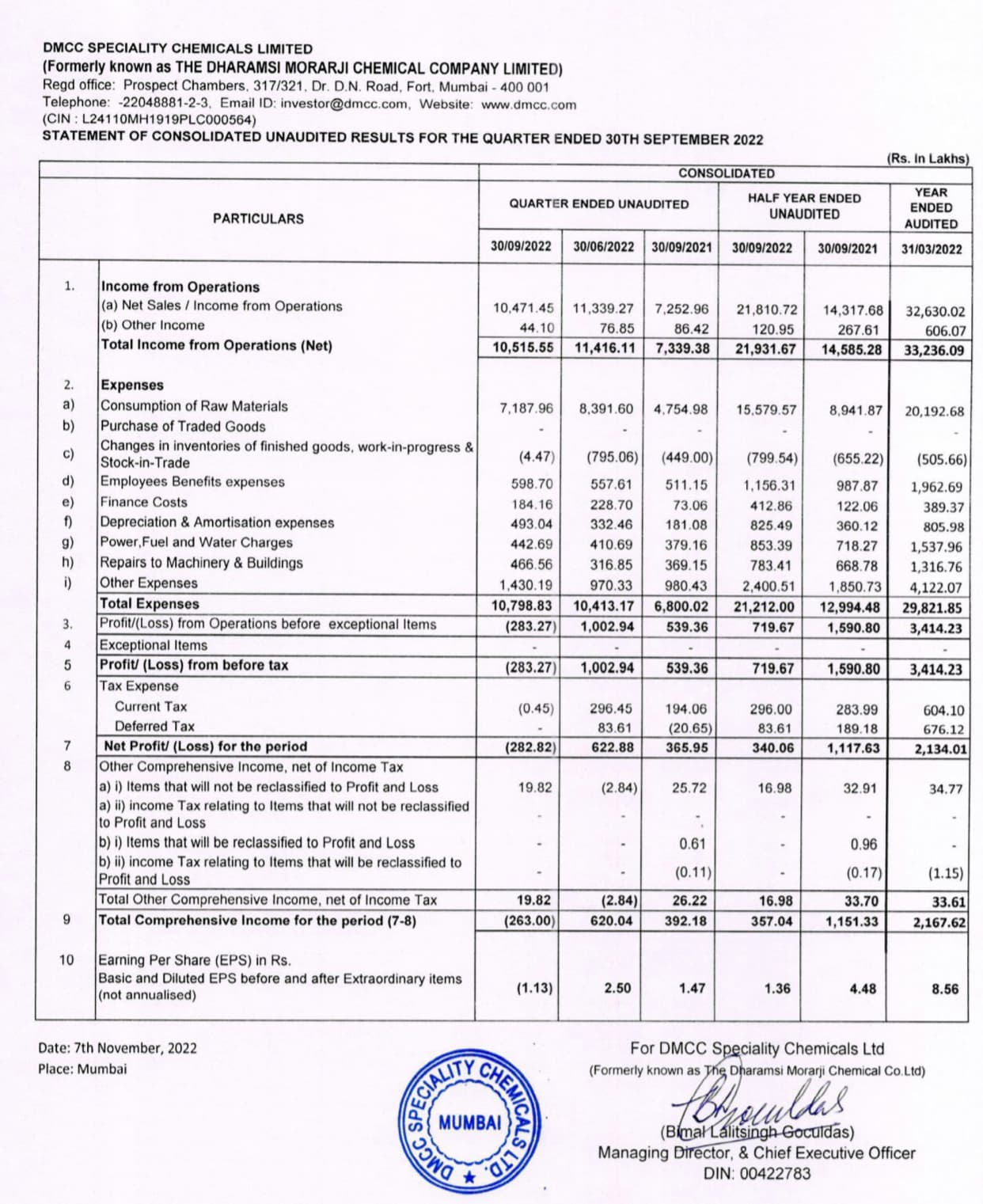

result looks very weak.