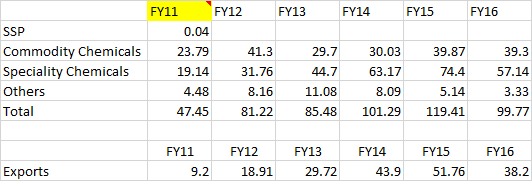

Dharamsi Morarji Chemicals is an old Indian company. It was formed in 1919. It was India’s first sulphuric acid manufacturer. It later diversified into fertilizers and for a large part of its existence it used to manufacture fertilizer. However, given the unattractive nature of the business and government intervention, the company kept on losing money in this business. It exited the fertilizer business few years back and since then has been focusing on the speciality chemicals space. If we look at the numbers from the speciality chemicals it has grown at a good clip (last year realizations were down, but volumes were up)

I have been tracking this co for more than a year. I don’t understand the products it makes as I don’t have the background and there is very limited info available. But I have attended the last 2 AGM’s and these notes are from there. My thesis at the time of investment was

The company has seen a revival through exports and its focus on speciality chemicals. Numbers in terms of margins & working capital are improving. Company’s balance sheet has improved significantly with debt/equity below 1. Speciality chemicals is a sticky sort of business, so they should be able to grow with existing clients. The company is available at TTM P/E of 7

About the Business

The company focuses on 2 lines of chemistry -sulphur based and ethanol based. In its 2015 AGM the co mentioned that it is in global top 3 of all the spec chemical products it manufacturers. The interesting part is that these products are not high volume products but are niche products and are high on margins but could be low on volumes.

For ex - Benzene Sulphonyl Chloride - which is its leading product, it is the largest manufacturer in the world controlling ~ 50% market share. In FY15 it did ~ 35 Crores of sales from this product. Thus globally it is just a 70 Crores market.

It has 35 such products and has recently entered sulphones which as per management is a big market.

The company has the following criteria for choosing a new product

Should have some edge either in terms of cost – backward integration or in terms of better process

In terms of quantitative benchmarks the product should deliver 30% minimum profit margins.

(These margins are at a PAT level as per mgt, even if they are at EBITDA level it will be great )

In terms of expansion the company has recently got approval for its new multi-functional plant - this has the potential to do ~ 20 Crores of revenue and 6 Crores of EBIT. Capex was around 5-6 Crores.

Nature of contracts with customers and suppliers

Long term contracts of more than 1 year - 70% of the contracts are for more than 1 year, company is trying to move away from spot contracts to 100% >1yr contracts

With customers – quarterly adjustments with regard to change in raw material prices, maintains fixed EBITDA per ton. Also doesn’t take forex fluctuation risk with key customers. That is also baked in to the quarterly pricing revision

Major RMs are Ethanol, Benzene, Sulphur. Suppliers are Indian Oil etc and thus no bargaining power and there are monthly pricing adjustments

Other Interesting points

Co has been hiring strongly in its engineering and R&D team. The CEO mentioned that the headcount addition has been of the highest in the last many years for the company.

Q1 was strong with 25% EBITDA margins. If this is sustainable it will lead to strong bottom line growth

A 30 Crore top-line can be considered as a good quarter for the company. As per the numbers disclosed during the AGM the company seems to be on a run rate of ~ 40 Crore run-rate in top line in Q2. This is significantly better than many of its previous quarters.

The negatives

DTA- Company is carrying 26 Crores of Def tax assets in its P&L which it has to w/o. This has begun already and will be passed through P&L over the next few years. this will have a limiting impact on profit and profit growth

Given it only looks for niche chemicals - scalability is an unknown here. Company has to introduce a lot products to become big.

Disc: Forms ~15% of my PF. Bought in the range of 45-55.

High Raw Material costs: Raw Material costs are ~60 % of revenues. In quarters when RM prices increase (linked to increase in crude price - a seemingly likely scenario), the company might not be able to pass on the higher prices instantly (there will be a lag of at least 1 quarter)

Exiting Fertilizer business: Company exited SSP (fertilizer business) because of less profitability. SSP is made from sulphuric acid and rock phosphate. There are many companies in India that produce sulphuric acid as a by-product and use it to make SSP at zero or even negative cost.

Cyclicality and low profitability of sulphuric acid: ~25% of company’s revenues come from sulphuric acid. As already highlighted in the HDFC report, this is a cyclical business and margins on average are very low. This business has been at its peak in the past two quarters and the forecast is that prices will go down after Diwali.

Old manufacturing plants: Also, the company’s plants seem to be very old (going by the fact that there was expansion activity in 1988). Typically, a sulphuric acid plant needs ~ 15 day shutdown every two years. Last year the company lost a month during shutdown which indicates problems manifested that the company had not foreseen. Also, products from sulphuric acid plant - including sulphur trioxide, oleum and sulphuric acid are used as raw materials for its other “specialty” chemicals. If sulphuric acid plant is shut, company will have to procure there raw materials from outside at a rate that might lead to severe margin pressures. Old plants generally require higher maintenance and the company might see more frequent unplanned breakdowns/ plant shutdowns.

Low barriers to entry: Looking at the chemistries (primarily sulphonic acid and sulphur based derivatives of benzene and ethanol) that the company works on, I’d say that it’s not very difficult to replicate by any other chemical company. In this scenario, when the company’s market share in it’s products is already very high, it will mostly lose it’s market share to a newcomers lured by good margins in this business.

Multipurpose plant a hope: Company’s multipurpose plant seems to be of a very low capacity basis their CAPEX spend. However, in the entire manufacturing portfolio, this seems to be the best hope. If they’re able to exploit this very well, then there’s credence to the future growth story.

Merger w/o business synergies: Possible merger with Borax Morarji will offer no synergies in terms of marketing as the product lines are very different. Only positive could be any reduction in indirect costs, which will not be a huge amount.

(Work in the chemical industry, graduated in chemical engineering.)

I am not from chemical background. I am trying to understand the usage and what might be the runway ahead. The leading product Benzenesulfonyl chloride - what is this used for? Is there any scope for increased demand?

Also - to understand the complete picture, would you mind your investment rationale? Do you think it is long term story or may be a mispriced one? Do you foresee a re-rating?

Thanks @mythace for bringing some good points into the discussion. I wanted to discuss your point on entry barriers - What are the barriers to entry in the chemicals business in general- I would like to understand if from you, since you are from the industry? As per my understanding, most of the chemicals have a life-cycle and the margins shrink in 3-4 years and in that sense it’s a treadmill business, you need to keep finding new products to protect yourself from the inevitable.

Specific to DMCC - I think the management is cognizant of that it is trying to get into more such niches. But I don’t have a clear answer on its scalabilit- though sulphones seem to be a big push for the co given its size and scale.

While this is true - What the management mentioned is that the shutdown will be 18 month exercise. FY17 will not see any planned shutdown. However FY18 will see one.[quote=“mythace, post:4, topic:7796”]

Multipurpose plant a hope: Company’s multipurpose plant seems to be of a very low capacity basis their CAPEX spend. However, in the entire manufacturing portfolio, this seems to be the best hope. If they’re able to exploit this very well, then there’s credence to the future growth story.

[/quote]

Fixed asset turn of 3X is bad? I thought its pretty decent. I don’t think others in the industry have such metrics (more in the 1-2X range). Please help me understand this part.[quote=“mythace, post:4, topic:7796”]

Merger w/o business synergies: Possible merger with Borax Morarji will offer no synergies in terms of marketing as the product lines are very different. Only positive could be any reduction in indirect costs, which will not be a huge amount.

[/quote]

Too early to take a call on this in my view. Management has not indicated anything on this so far.

DMCC after a torrid time, finally seems to have got some mojo. I don’t think the promoters will like to kill it by getting another bleeding co into its fold w/o any benefit.

On commodity business:

What led to the recent run up and why do you think it will fall post Diwali- any thoughts would be greatly appreciated and will be helpful.

Do you have details of products/byproducts along with production capacity details of said plant…in case you have Eia or tor report of the plant then it will be of great help as an asset turn of more than 3x even for a high value low volume specialty chemical plant is quite interesting and if you have precise data then would like to run a product realisation exercise at CMP…however, in any case, my knowledge makes me believe that highest asset turn can be achieved only after few years and not immediately.

Dear Rohit Sir,

As seen from your initial write up it seems that you are invested in DMCC from the level of 47-48 and now the stock trades at some Rs. 100/- odd. What change so suddenly that you have not posted the idea for discussion when you have just invested and now when the stock has climbed nearly 100% an idea is floated for discussion.

Isn’t it would be good that the idea will be posted as soon as one invested so that everyone can research and ripe the fruit.

Ideally, that’s the best way. And I do agree that its best to post when you have invested.

In this case I did not have a lot of information to start a thread but I felt the valuation comfort was there and hence invested. For the forum, I felt it may not be right on my part to just randomly start a thread.

The purpose of posting it now was not driven by price. After attending the AGM I decided to start a thread but somehow I couldn’t get the time to post it immediately. In the ensuing days the stock went up.The story however still remains interesting to me.

Whereas it is better for an initiator to post the idea on a public forum like VP as soon as he invests in it but one needs to respect the fact that there are varied preoccupations and constraints involved on the part of the initiator because of which he might not be able to do so…also, researching a company from varied angles and collecting all the information regarding a company from varied sources is a long process (most of the times it takes many months) and although the initiator can afford to invest as soon as rough homework is over but when he posts on a public forum he has to be double sure of the basis and correctness of the information as posting a research work on a public forum involves a responsibility.

Hence, instead of pointing fingers on an initiator like @rohitbalakrish_, we need to be grateful to him for sharing his work with all of us and we need to have utmost respect for him…we need to remember that no one is prompting you to buy the story at face value…he is only sharing his work and inviting varied inputs on that work which could be both, positive and negative…we need to do our value addition and put in our own efforts and then if the story looks interesting at appreciated valuations we need to take our own decision.

I deliberately played the role of a devil’s advocate. So, you can take some of my views with a pinch of salt.

Typical entry barriers for a chemical company will be:

Technology and know-how

Scale of the incumbent (if incumbent already has higher capacity, it can outprice new entrants - overcapcity isn’t a favorable situation)

CAPEX (the upwards you are in the value chain, the more scale you require to being down other operating costs)

Integration of value chain (from starting raw material to finished product)

Company’s brand image & reliability (for exports)

The kind of chemicals DMCC is making typically don’t have a life-cycle as they are intermediates for other finished/ active molecules. As soon as another Indian manufacturer will start producing these chemicals, the margins will reduce.

If DMCC could get tech and know-how, there are other companies in India who will be able to acquire it. Won’t get into how. CAPEX, as you see, isn’t huge for this line of chemicals. Any company that has a sulphuric acid plant can theoretically get into sulphones line of business. On brand image, DMCC will not have a huge advantage over other companies and at times, might be at a disadvantage.

FY 17 will definitely not have a “planned shutdown”. However, the number of unplanned breakdowns will increase with the age of the plant. So, total availability will reduce - or generally does so after plants are of a certain age.

This assumes the capacity utilization will be 100%, which I’ve never seen in the first year of operation. Realistic number will be more like 50% because of startup issues, lag for market development etc. In my experience, the 3X turn is typically achieved in 4-5 years. Also, a multipurpose plant will have higher operating costs (because of a changeover etc.) than a dedicated plant.

I agree. Only mentioned this as a response to the commentary in the HDFC report

It was a simple case of short term demand exceeding supply with factors at both the ends. I’m sorry I cannot answer this question in detail. I work with a company that has these products as a part of it’s portfolio.

Just on the point of others entering the space.Is it fair to say that given the market size of these chemicals is not very large - not many people will be interested?

If DMCC earns better than normal margins, other players will jump in. The sulphone mfg technology isn’t too sophisticated. So, most companies will make a choice to move downstream, towards value added products.

There was very limited information available till now on this company and you have done excellent work in filling the white space. To me there were a few triggers that have played out providing enough margin of safety to invest even though with limited information.

Chiefly the next generation of promoter (Bimal Goculdas) had taken over as CEO in 2011. The changed fortunes started reflecting in financials from FY14. He has a patent to his name http://patents.justia.com/inventor/bimal-goculdas (thanks to a fellow investor to pointing me to this. Bimal could be the case of intelligent iconoclast driving value in a small company. @rohitbalakrish_any views you could gather on Bimal/promoters from AGM?

They had already discontinued fertilizer activity which curtailed losses

Commentary on R&D focus and new products had started

It was an opportunistic bet and it has played out well. It is good to see more commentary coming out from management and expansion plan.

The Borax Morarji link continues to be a watch item considering the common promoters and Bimal being the common CEO.

Co is announcing the results on 27th October. usually the co announces the results at the fag end of the season. Also promoters doing a pref allotment…

Thanks for bringing up this company . What seems to be the reasons for change in the fortunes of the company has been rightly pointed out by Bigvig as the next generation of promoter having taken over the management . This is a major factor and no matter that the plant is old or require regular maintenance or product market is small is not relevant as the new management has proven their capabilities,

Yes, agree to your point. Bimal Goculdas at the helm has been a major factor for the turnaround in the co.

Q2 results were very good. However marred a bit by the tax bit. However EBITDA margins were very respectable. If these margins are sustainable then it will be very interesting.

Promoter is infusing some capital at around 95-100 Rs this will strengthen the Balance sheet further.

)

)