The company submitted a new plan and previous plan of 2019 has been cancelled. Hence it is not cancelled but re-arranged

2 Likes

Special Situation (Acquisition )

Few weeks back I cam across scrip called HG Industries (42 Cr Mcap)

It is very illiquid scrip with barley any trading but about month back it got stuck in upper circuits from 40 odd level up to 100+ level just recently it came out of circuits & recently hit a lower circuit.

Now reason why this is happening is because of Greenlam industries where they acquired HG indutries promoter stake of 74% and rolled an open offer of 41 rupees per share to retail investors.

Objective of these acquisition as per Greenlam Industries is

- Set up manufacturing facilities on the properties of HGIL and expansion of business of the Company

- Company may also consider disposing of the office space of HGIL.

- They may also consider the Merger of HGIL with Acquirer post the completion of the Open Offer and consummation of the Proposed Acquisition in terms of the SPA.

Please refer following article for more details on it:

Disclosure: Not Invested only tracking developments in it also had tried entering scrip as tracking position when price was less then fair value of company as per me but could enter as it was in circuits. Please be averse of risk in such illiquid scrip before any investment decision. please do you own due diligence & not SEBI registered advisor.

4 Likes

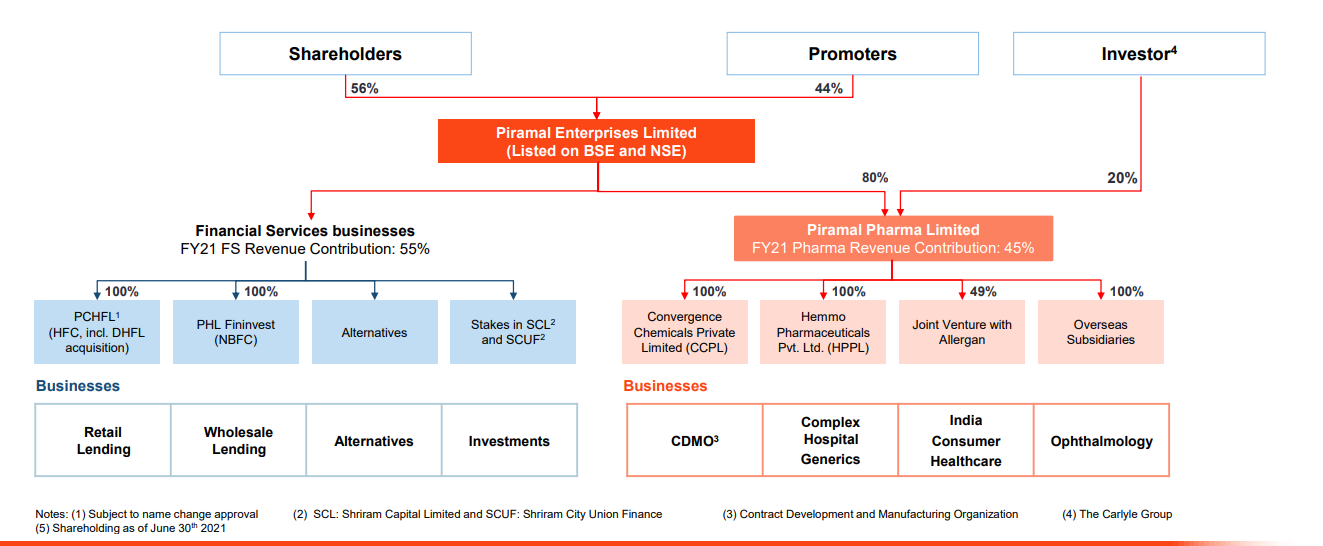

Piramal Proposed Scheme of Arrangement

Structure: Four equity shares of face and paid-up value of ₹10 in PPL for every one share held in PEL

Timeline: Timeline as per Piramal thread is 9-10 months from current date as per concall.

For More Details:

Disc: Invested in Piramal in last 30 days.

8 Likes

- Oct 14, 2016")

Mohnish Pabrai explaining some good special situations he came across

5 Likes

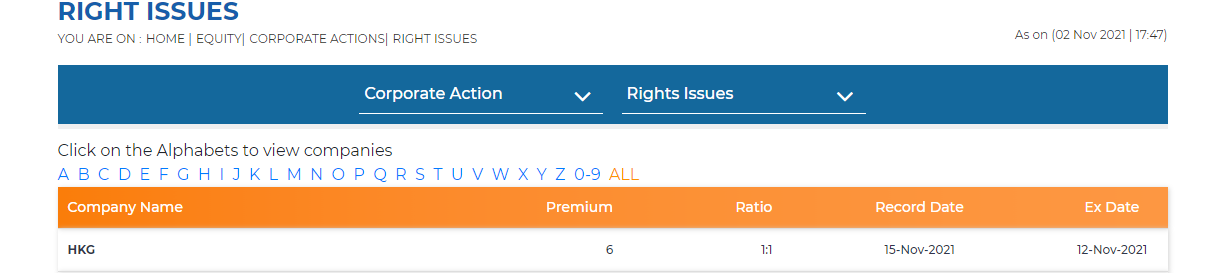

Texmaco Rail & Engg rights issue is coming up

Trying to calculate if thr’s a rights arbitrage here. Based on today’s price of 35.35, the bet seems to be more risky than rewarding. The proportionate price is expected to fall to arnd 27.

Can expert fellow Pickrs who have done rights arbs previously please advice here?

Disclosure :- no investment.

1 Like

Good analysis on GMR Infrastructure.

Upcoming Triggers, Business segment structure of Airport Business and Valuation of Airport Business.

1 Like

This is yet to happen, right? I’m not seeing any dates in the pdf document as to when it will happen.

Sharing a link to track corporate announcemnts for special situations tracking :-

I found this source to have one of the cleanest & precise interface. Feedback\Other sources links invited.

13 Likes

This link is also useful

https://www.questgroup.in/CorporateActions/Merger-and-Demerger/

5 Likes

any thots on the rights issue? am only considering applying to avg, but is even that a risk?

(1) From arb perspective, thr wasn’t enough gap to play for decent IRR as I mentioned above.

(2) From holding perspective, Generally, a person holds an investment bcoz of faith in future performnce & value enhancement accordingly. - So, if cm from that perspective, plz apply to rights issue - otherwise ur holdings will be diluted to the extent of additional issued shares.

(3) If u realized it as an investmnt mistake, thn sell the current holdings & Rights Entitelment that’s currently listed, take the loss & move on.

Since I considered only arb part, u’ll be a better judge for taking steps (2) or (3).

Dat’s my 2 cents.

Disclosure :- not invested.

2 Likes

Some updates on the demergers and mergers I am tracking:

- Tips industries - Shareholder meeting on 2nd December for approving the demerger of movie business. Demerger should be completed in the next quarter.

- Forbes and company - Shareholders and creditors meeting on 22nd November for approving the demerger of Eureka Forbes. Demerger should be completed in the next quarter.

- IB real estate has filed the application with NCLT for merger with Embassy group. They should get the NCLT approval in this quarter. Merger should happen in the next quarter.

- GMR infra is waiting for the final approval from the NCLT for demerger of its airport business. Demerger should happen by end of December.

12 Likes

Another Rights issue arbitrage : -

The discount seems good but the co. & biz seem dubious. Any investor in it can prbly throw sm light plz.

1 Like

Here is a free crowdsourced tool that can help to get a constant and clear stream of new special situation opportunities and keep a track of everything.

Very nascent stage right now but will eventually improve in later versions.

Tool can be accessed at below link :

http://specialsituations.investkaroindia.in/

Credits to our fellow VP member @Tar for making this …

24 Likes

thanks for developing the much desired tool @Tar.

Entire VP family will remain indebted to you.

2 Likes

Special Situation(Amalgamation and Demerger)

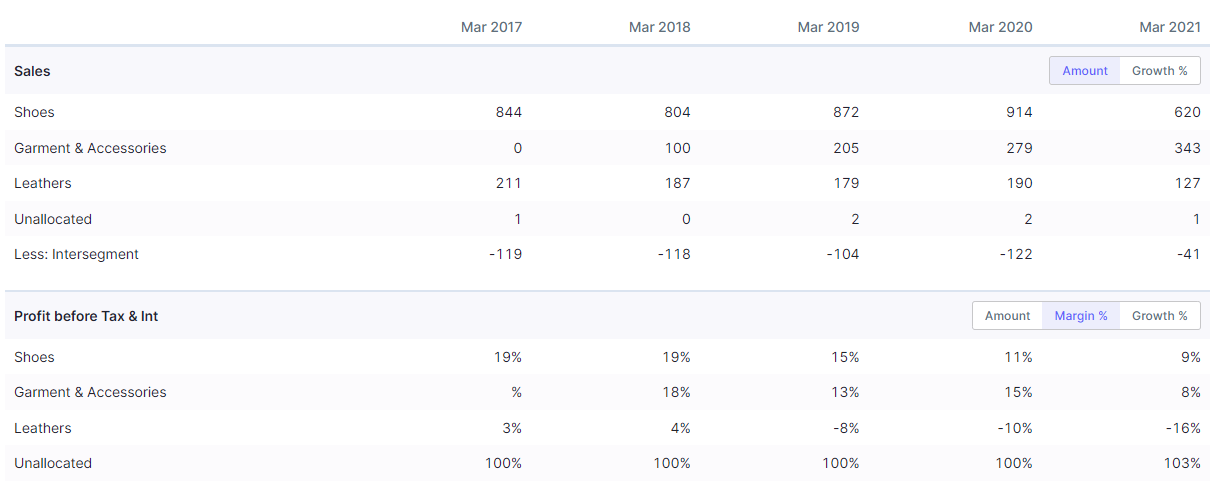

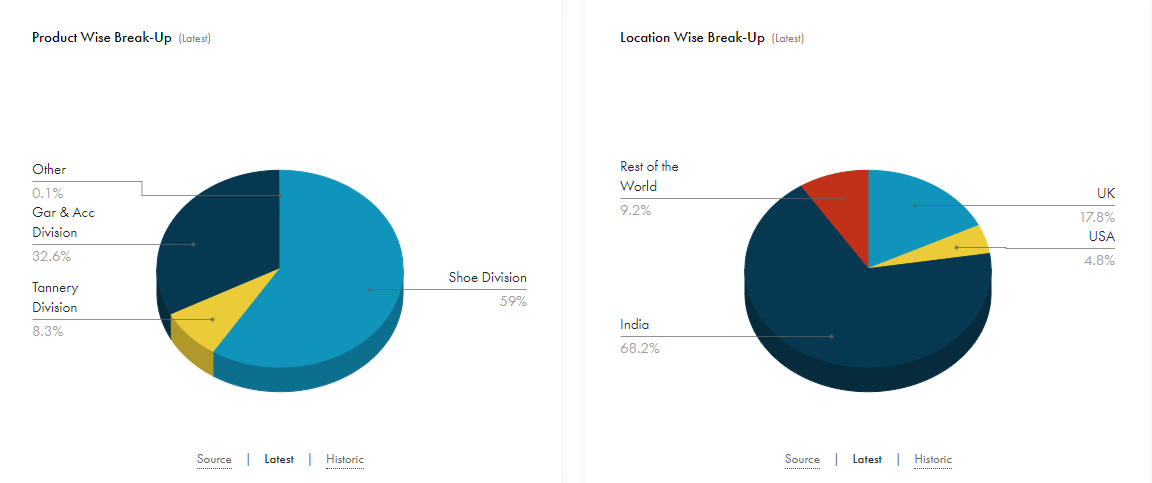

Mirza International

1)Amalgamation of RTS Fashions Private Limited, the ultimate holding company of Mirza U.K. Limited, with Mirza International Limited

2)Demerger of Domestic Business of Mirza International Limited into a Resulting Company, on mirror shareholding basis

Segmental reported P&L of Mirza International

Product/Geographic segment of sales

Disclosure: Tracking as special situation arbitrage opportunity and no active position currently.

Note: Company is yet to get approval from all creditors and yet to apply for NCLT for further process for demerger please be vary of all potential risk in such special situations.

6 Likes

Note: These is not a special situation its a opportunity on heavy discount to Book Value(Holding companies at very cheap valuation)

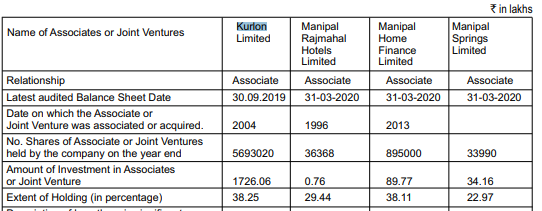

Kurlon Ltd(KL) and Kurlon Enterprises(KEL) these are 2 companies.

Kurlon Enterprises deals with Mattress and other segments here its competitor in listed space is Sheela Foam

Holding Pattern: KL hold 85% stake in KEL and rest 15% is with Motilal Oswal PE firm.

Bio about company KL : KL was incorporated in February 1962 as Karnataka Consumer Products Limited by Mr. T Ramesh U Pai. The name of the company was changed to Kurlon Ltd. in 1995. The company manufactures rubberised coir, foam and spring mattresses foam products and home furnishings through its subsidiary, KEL. The mattress and foam products business of KL was transferred to KEL through a business transfer agreement, effective from April 01, 2014. The Group has manufacturing facilities for rubberised coir in Yeswanthpur (Bangalore), Bhubaneswar and Gwalior, polyurethane foam-manufacturing facility at Dabaspet (Karnataka), Roorkee (Uttarakhand) and Jhagadia (Gujarat), and spring manufacturing facility at Peenya (Bangalore), Jhagadia (Gujarat) and Bhubaneshwar. KL currently holds 85.06% shareholding in KEL.

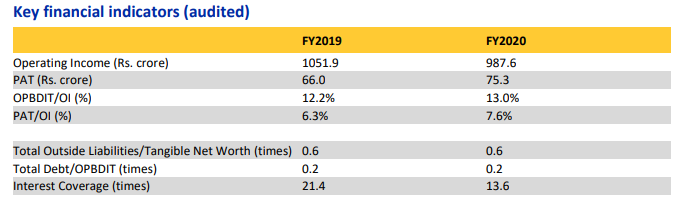

Kurlon Ltd earns some 8-9 Cr of PAT.

KEL(Financials):

It earns some 75 crores of PAT in FY2020

Valuations: Sheela foam trades at 45PE currently lets take a modest PE of 35 for Kurlon since its not market leader we get valuation of 2600 Crores

Now for Kurlon Ltd company which we are tracking is Maha Rashtra Apex(Listed) it holds 38% in KL

which gives it holding value of 1060Cr we can further give 25-40% holding discount to Maha Rashtra Apex.

Trigger: Motilal Oswal PE firm would need exit someday and Kurlon shares are pretty common in grey market as many are expecting its IPO

About Maharashtra Apex:

Maha Rashtra Apex trades at 120 Cr roughly. It is Manipal Group company with some other subsidiaries in it. It is pretty old NBFC which eventually became a holding company

.

Risk:

1)It can delist itself

2) It can take OFS proceedings in event of IPO and give to group companies leaving minority shareholders empty handed

3)Management has never given dividends to shareholders

Disclosure : Tracking position of 1%in Maha Rashtra Apex at portfolio level from lower levels in last down cycle.

Note: Intention of these post is for study purpose only and not investment advice please be very careful of holding companies risk before entering in such scrips.

Reference article by 2point2capital to understand risk of such companies attaching for reference of interested individuals: Investing In Holding Companies

14 Likes

Sm recent developments in arb categories : -

- GHCL - Demerger scheme changed. Home textiles division sold to Indo Count. Only spinning part to be demerged now. Filings/details are latest posts on the relevant thread : -

- SCI - This seemed to slip under the radar ( atleast for me). The land\residential assets are demerged into separat co. & govt. also looking to divest the co. to private players. The value of non-core assets itself is slated at 200-230\share. Apart frm this the shipping biz itself is valuable & has seen interest from likes of Vedanta & Fairfax. The last update here is that all demerger approvals were received by mid-Nov & everythng is expected to wrap up by Mar’22.

Requesting @Tar , @shivammitra others to share inputs, or misses here, if any.

Disclosure : - Invested in scrips mentioned purely as arb play.

1 Like

You really shouldn’t depend on the non core assets. Just have a look at Hemisphere Properties which has the demerged real estate assets of VSNL. The value of the assets are nearly 7 times its current market cap. It has been over 16 years since the demerger of these assets but nothing has happened till now.

1 Like

Here is the complied list of corporate action - Bonus, split, buy back, dividends, right issue or IPO status, are curated in one unified view for the benefit of larger communities, Do check it out Link- Corporate actions - Google Drive

4 Likes