Thanks @shardhr and @Shawn_Lopes for sharing your valuable insights (and also your views on Forbes specifically), especially appreciate your point emphasising judicious allocation of scarce capital. Your point is right on the mark, that as an investor, we should be clear on our approach before one makes an entry in such special situations. Thanks for highlighting that.

Personally, my motive to approach demerger special situation opportunities is never from a price arbitrage perspective. My understating on this style of investing is non-existent, so I’ve never ventured there.

My philosophy is to buy, hold and track. In past, I’ve had decent outcomes on few occasions that I have invested in demerger Special Situations (Meghmani, Jubilant Life and couple more. Have also seen good returns in Suven, though I’ve held that for many years now, and my entry was years before the special situation came up). On each of these occasions, I’ve entered clearly with the buy and hold view, based on the analysis that the demerged businesses (or at least 1 part of it) is likely to deliver better returns going forward. So the motive is to hold longer term.

Hence, I am far more comfortable entering once there is a clarity on the demerger process, even though it may mean paying a slightly higher price at for entering late, compared to the time when the SS first announced itself. As long as there is enough conviction that the demerged business will grow well, its worth paying the premium, especially to eliminate uncertainty of demerger process.

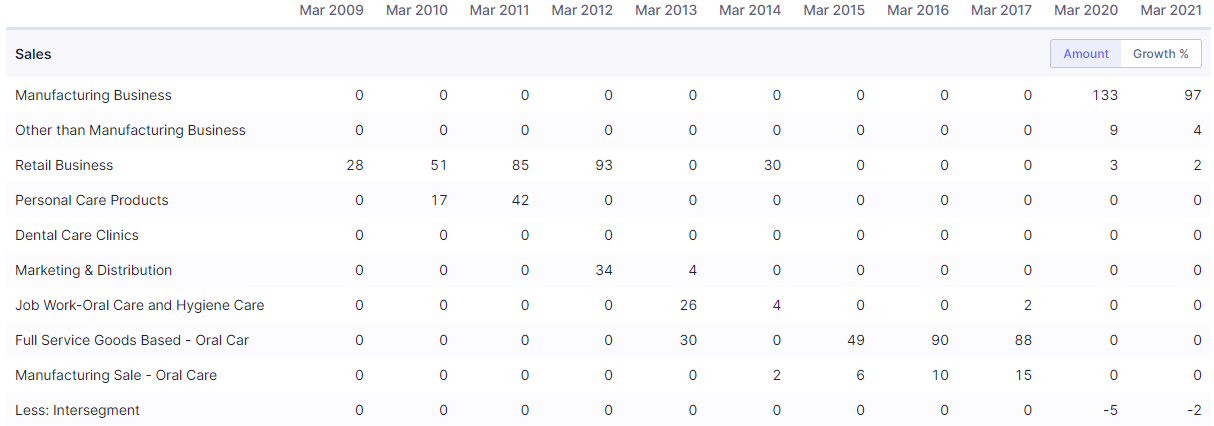

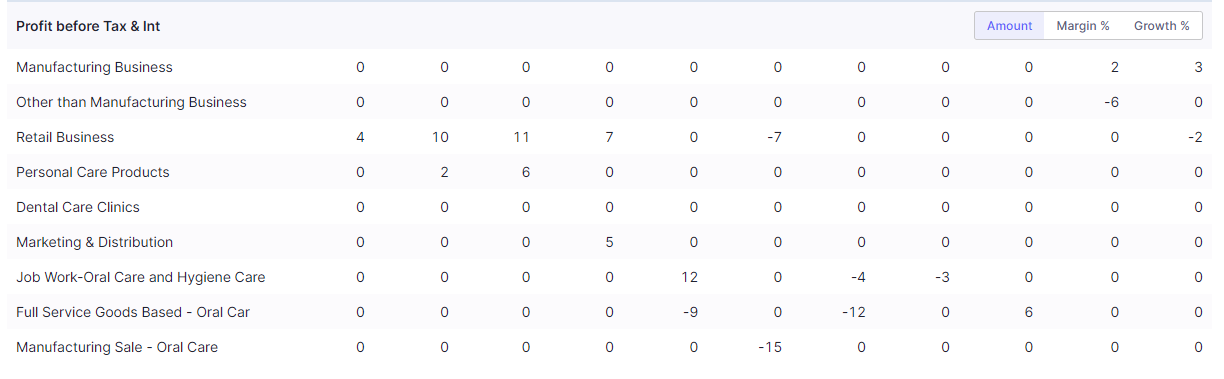

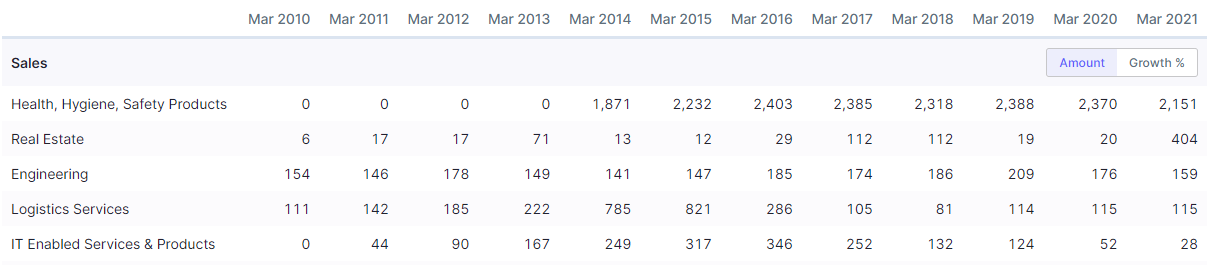

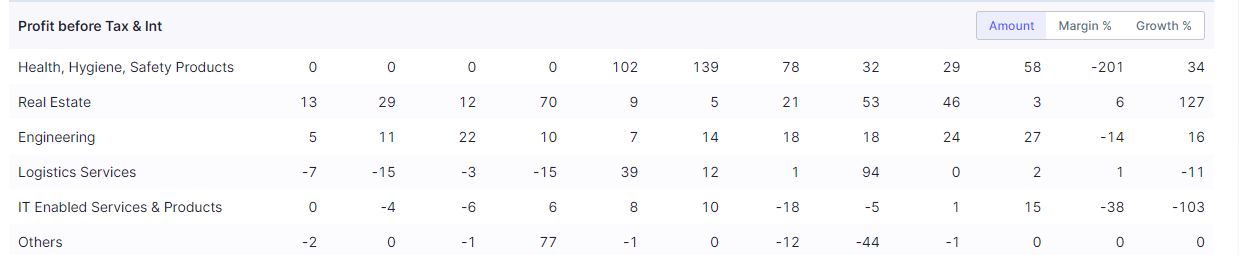

On Eureka Forbes, the business has indeed delivered below par numbers. But I believe that has more to do with the management and inefficiencies within the organisation. The trend is common across all their businesses. If it weren’t for the land they own, even real-estate division may struggle.

Eureka Forbes as a brand has high recall, and despite the mediocre way it has been run, it still enjoys a great market share. So it has potential to grow in an underpenetrated product category, that is beyond doubt. Valuation wise, at roughly 4400 cr, 2x Sales, for a established consumer business, there is definitely potential still left on the table, especially in the hands of a new, professional, capable management.

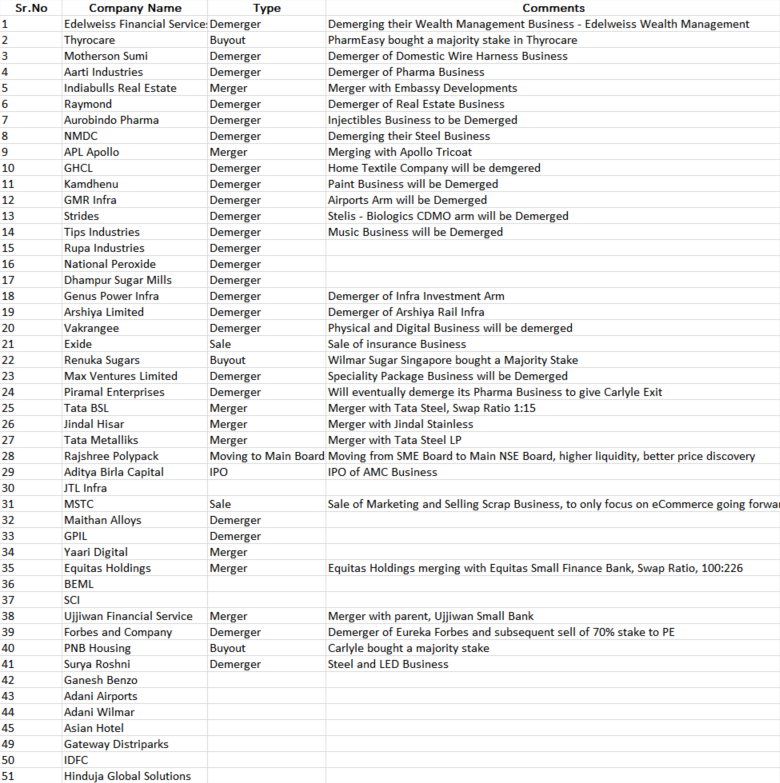

Disclosure: Not invested, but tracking