Glad u brought this up. I had the same concern & hence had done sm further analysis before posting. Below is my understanding to your concern :-

The TATA comm- Hemisphere demerger broadly happened within a yr’s time-frame after announcement. Prior to that it was a speculation anyways. The arbitrageur jumps into play only after official announcements & filings take place.

Even in case of Hemisphere properties, the initial out of selling was followed y discount narrowing gradually. I myself rode it from 65-odd to 130 in 6 months time. So, from arbitrageur angle, a play can be to Buy the demerged entity if it gets super discounted. You dont need full realization, only a move from 80% discount to 60% discount will double your investment.

In this case too, if u discount the assets worth 200+ to 100/share only. You are paying 40-55/share for a residual shipping iz that the govt is looking to sell-off or an industry that is in an up cycle. So thr’s MOS on that side as well.

The Land & apartment assets here have another kicker. The Shipping ministry entities will have first preference over these. So you have a first ready buyer in place for the assets

The main question arb investor has to focus on is which asset to buy & when. My understanding is it makes sense to buy SCI now and the demerged entity to if it gets whacked to 75-80% discount.

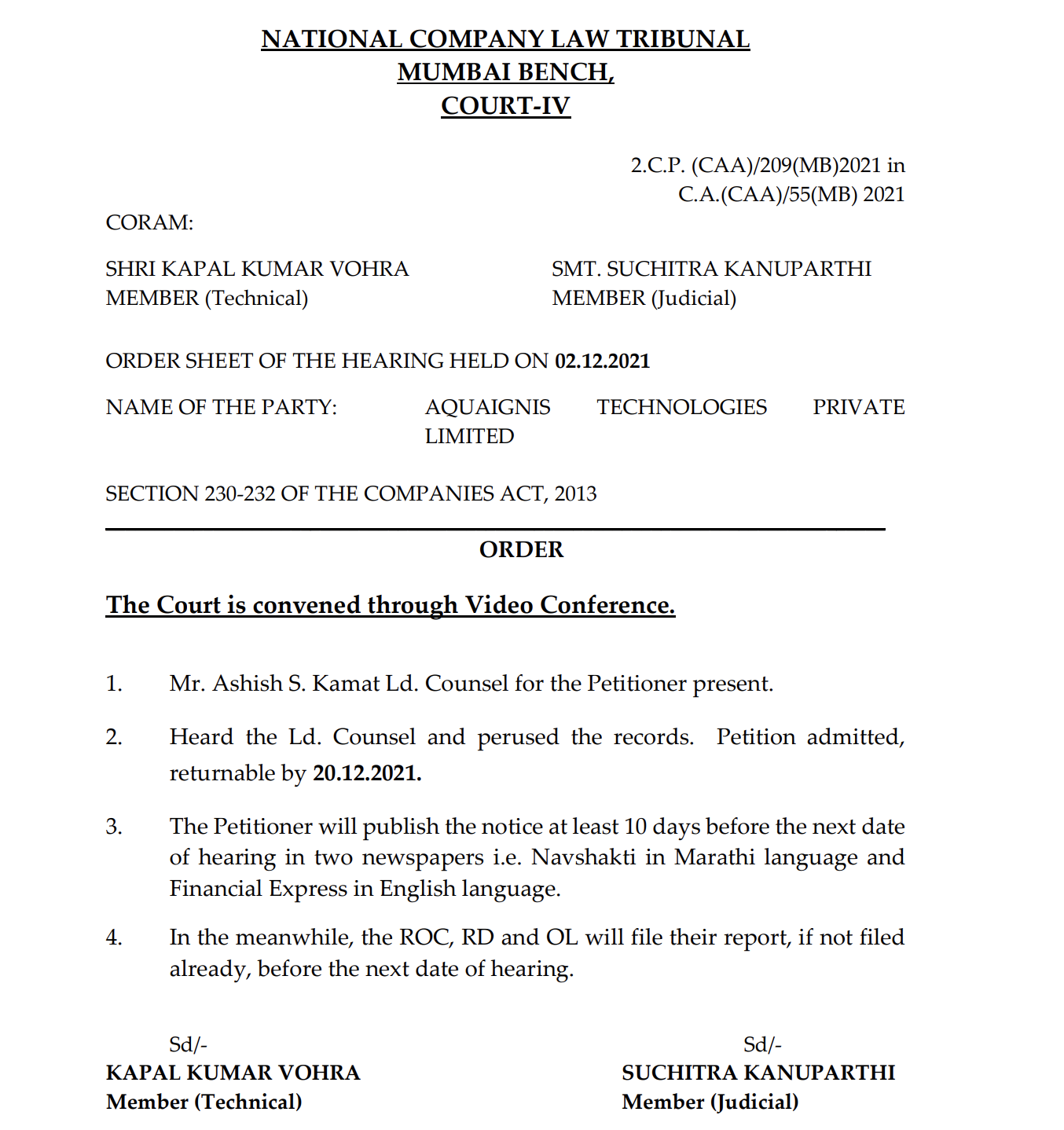

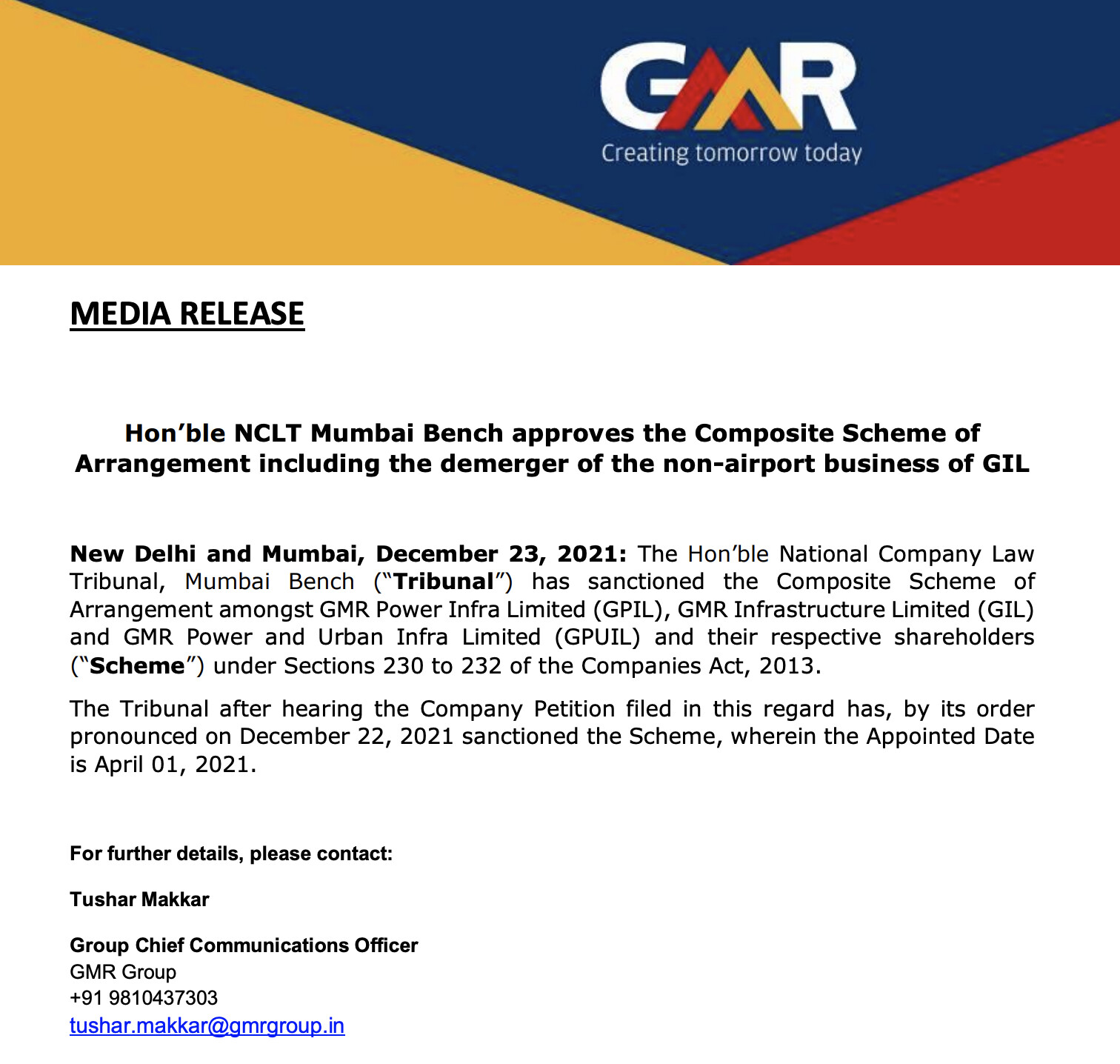

Based on previous cases, GMR listing shd take a month or 2 max now. Also attaching screenshot from Neil Bahal’s log to round up demerger listings in FY22 :-

Its of importance bcoz arb players can keep track of these & sometimes the value lies in buying the demerged stubs post listing.

Sharing another idea from a blog written by Ameya bhai : -

He wrote this more from investing point of view, but on purely mathematical arbitrage basis I find this situation on par with IDFC reverse merger. In fact, I will prioritize this over IDFC purely bcoz of mgmt lethargy there.

Disclosure :- Positions in GMR, Piramal, IDFC & Ujjivan as part of special situations Basket.

Hi everyone,

Can you please help in telling what happens to shares when a demerger is approved like the case in gmr? It will help me gain more knowledge.

Just a newbie trying to learn more.

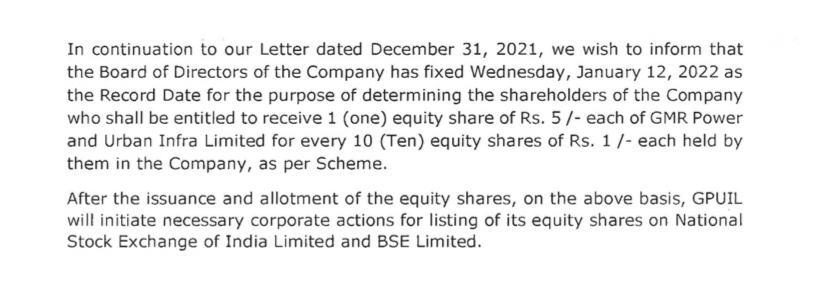

After demerger is approved, a record date will be fixed. Investors who hold the GMR Infra shares on the record date will only get the demerged shares. There is also a fix swap ratio for allotment of demerged shares. In case of GMR Infra, you will get 1 share of GPUIL(non-airport business) for every 10 shares of GMR Infra. The stock price of GMR infra will adjust on the record date. It takes around 1-2 months after the record date to list the demerged entity shares on the stock exchanges.

I am a newbie to special situation investing…i wanted to ask folks…if they could suggest any special situation opportunity currently worth digging…though i am aware of forbes and mirza but i think forbes now does not provide much arbitrage and mirza has run much.

Invested in gmr infra and idfcltd recently

Plz guide if possible

I still see a lot of value in Eureka Forbes demerger as it currently trades at around 3x sales. Once the promoter changes, one will see good growth and increase in margins. Kent EBIDTA margins is around 25%. I believe that Eureka Forbes will also be able to do so in the future. With 3k sales and 20% margins, Eureka Forbes could do around 500 crores PAT. It may take around 1-2 years for full turnaround once the management change happens. Advent(which will be new promoter of Eureka Forbes) bought Crompton consumer electricals from the Thapar group and turned it around.

Indiabulls real estate and GMR airports are my other two favorites. Both of these companies has huge assets and are hungry for growth. IB real estate will have backing of Blackstone and Embassy whereas GMR airports has the backing of Groupe ADP which is an international airport operator.

My suggestion is start with reading thoroughly the book - " You can be a Stock Market Genius".

In my ltd learnings in special situation cases, thr are 2 things to consider here : -

Which security to buy - eg. in spin-off cases - the demerged co. or in merger cases the acquirer or acquiree

The IRR - since these cases are time bound events, thr should be a calculation of expected return with sufficient Margin-Of-Safety to factor for unforeseen delays.

e.g- U mentioned IDFC - Assuming u r playing only arbitrage, the net discount here will be 30-35% - If the unwinding happens in 1 yr - ur IRR is 30-35%; if it takes 2 yrs - it will come down to 17% - Is this a good enough return - dat’s for u to decide.

1 final suggestion is to improve ur decisions - read the failure cases too along with the successfull ones - That will give u pointers to where and how things go wrong.

Urw… ; the more u learn & bring back ideas here, the better for community.

U have completed 80% theory & basics with that book. Now dont fall into the guy-asked-Mozart how to practice trap ( assuming u know this story ).

I have mentioned 1 other resource above - failed delisting & merger cases. U vl get other links in this thread & over VP community itself. So explore & learn. @shivammitra , @Shawn_Lopes , @Tar & others are thr to reach out & ask for help.

Another source is Mr. Neil Bahl’s newsletter : -

Refer it for few of the special situations he has discussed. But avoid blind copy+paste & taking his analysis on face value ( In fact, take nothing in investing on Face value)

Happy Learning!!! Looking to hear out ur thesis\ideas on special sits soon

; the more u learn & bring back ideas here, the better for community.

; the more u learn & bring back ideas here, the better for community. ).

).