@Tanishk_Ojha Some Scrips might not be updated till latest concall, Still it is better to keep eye on Max Ventures as these development might play out somewhere in future.

Thanks for updating on it.

Yes i completely missed this one even though i studied this situation. Thanks for pointing it out.

Note: Many company might go IPO way rather then Demerger way because of this current lucrative IPO market.

Recently in Strides-Stelis management is looking for other options apart from demerger for Stelis Bio, I will not be surprised if more companies do it.

After the demerger, SP group is planning to sell its stake in Eureka Forbes inorder to pay its debt. They are expecting a valuation of around 6000-7000 crores.

The final notice for demerger by NCLT and stake sell news should be coming soon,most probably within a month.

Excellent info @Shawn_Lopes : Being interested in arbitrage positions & playing few of those myself, I’m on the look out for evaluating these. And I must confess, the returns have been fairly good in light of lack of undervalued\fairly valued equities.

I added smthng similar on the other thread. Sharing that link below : -

However, I mentioned the opportunities that I was invested in ( hence the smaller list )

Would like to also knw ur views valuation wise on investments, if any, u’ve made in these.

My views can be seen on this other thread. Also thr are 3-4 different threads that are running for these special situations investing. Ur post can be a good starting point to integrate these.

Actually special situations are very profitable if you get it right but key part is to value that business as there is lack of data available for it and even management does not know how NCLT or other situations might plan out.

For Example recently i studied Meghami Orgainics it has been delisted for almost 90 Days and still there is lack of proper clarity on its listing also not to add opportunity cost of capital.

Arvind Fashions is example of failed demerger which destroyed significant capital to its shareholder while Borosil Renewable has really unlocked value for shareholders.

This video can help you understand this special situations better.

Currently I am in exploring stage of these Investment but to give my two penny of thoughts i Usually eliminate Industries I think which are not in good or show characteristics’ of cyclicality for example Textile, Auto , Metals i usually avoid their demerger entity study.

Then we are left with Pharma, IT, Chemicals Industry I go in depth of them to find reasons for demerger and is there actual value in it.

At start all bad companies also will show significant gain because of Scarcity of shares available as they are stuck in upper circuits but eventually quality matters (Study Inox Wind Energy Volume)

Few Scrip i am really interested is Stelis Bio but their management was unclear on demerger of Stelis or IPO of it. Meghamani is more like a valuation play and high capex utilization in near term play for me. Aarti API pharma is very high roce business but i am uncomfortable with how much selling that happens in Aarti group companies by promoter just when they announce Bonus news. Tips seems interesting but haven’t studied it yet.(Really like Saregama as business).Piramal group if ever they demerge their pharma division massive unlocking can happen same thing goes to Sun pharma if they ever decide to demerge domestic pharma business(Not Likely)

Yes initially i was planning to create specific thread for it and explain rationale behind several companies in detail in subsequent post in it. You can share this post to link those threads and bring people in one place to discuss about special situations scrips.

It will be really great if other investors share rationale about other companies like NMDC, Kamdhenu, etc. It will really save time as it is difficult and time consuming to study companies one by one. Even links to other thread or articles/Video from web will be really helpful for such scrips.

Disc: Above scrips are not meant as investment advice please do your own due diligence. I may or may no own few scrips mentioned above.

Thank so much @Shawn_Lopes for collaborating the details.it helps very much.

I am novice investor.i maybe completely wrong.my two cents.

Migration from sme( both in nse emerge/bse sme) to nse/bse mainboard.

Sme Stocks with 25 cr market cap are eligible for migration.

Stocks rise typically 30-100 percent once they plan to move to mainboard.the process goes like this

intimate about the migration in a board meeting

send evoting/postal ballot to shareholders

send the results of voting to exchange ( 1 month interval for voting)

migrate to mainboard ( 1-2 months after submitting the voting results)

The ideas is the buy the reasonable valued , fundamental strong sme stocks once the Announce the migration to mainboard. The lag is about 3-6 months from announcement to migration.

Sometimes the shares quickly go up after announcement ( eg chemcrux went 300 to 450) or wait and move suddenly once the listing days are near ( rajshree migration was announced at Feb and stayed still for a month). You can also check this by mapping the date of announcement with stocks movements of already migrated stocks.

We sell can them after they rise after migration.

Shares about to Migrate

1.chemcrux

2.air olam- evoting complete

3.rajshree- evoting complete

4.bb triplewall

And will add more after searching.

But these are already moved significantly. the idea is buy them when the news is not fully factored i.e they have moved only 10-20 percent.will add more about it later

@Karthikbaskaran Thank you sharing i never thought about this strategy in detail, It makes complete sense why prices appreciates since these SME stocks trade in lots of 500 to 1000 which makes it difficult for retail participation especially when that scrip has rallied 3-4 times.

Can you share link where to track upcoming companies where this event has started and is waiting E-voting Approval.

I have studied Chemcrux 15 Months back and Rajshree Polypack some 2-3 Months back, For Chemcrux their promoter remuneration and Environmental clearance issues where pretty concerning to me while for Rajshree Polypack i was concerned more with pricing power they had and too many peers in that space (If they made products with complexity of Kinder Joy packing I would have been more interested). Will look at them in more detail . If possible can you share list of companies in last 3 Years which went SME to Mainboard IPO is it trackable on NSE website.

@Shawn_Lopes Thank you for your post. It is gold. It is hard to keep track of all special situations. I think if we have a public google sheet and all members can update it as and when they come to know of a new special situation, it will be really useful to the community.

Template can be - Name of company, NSE code / BSE code, Special situation type, Expected timeline, Description

Is this against valuepickr rules? I can create a google sheet if it is not… @Donald and other seniors, Please let us know if it is fine.

Agree with ur points & as u pointed correctly certain uncertainties related to approvals in special situations do add to the risk factor - However, I blv the process will become definite enough, if not smooth as more and more of these corp actions take place and we have supportive regulatory environments in place. To put in other words, the corp restructurings are still in a very nascent stage in India vis-a-vis other prominent capital markets. Till then, the only feasible solution for retail investors is to adjust thr probability and IRR calculations accordingly. E.g - IDFC reverse merger case - The difference in price vs value was so wide at one point of time that the uncertainty hang of over 2-3 yrs was acceptable.

The video u shared was part of my learning arsenal as well along with Greenblatt’s book , I must say its an excellent source.

The other imp aspect aspect of business and industry as u mentioned can be dealt by working out over when\which security to buy. Eg - in Jubilant demerger - I bought Ingrevia post listing when it hit LC at 250+ odd price.

For GHCL - I also agree that textiles business isn’t that strong & might sell it off post demerger. I hv shared my views on its valuations on GHCL thread.

To take ur Inox Wind example, yes the return was made in buying GFL shares before record date & selling out IWEL shares as soon as they reached 60% of thr value. ( Anyone who bought that spin-off might share thr views and we might become intereseted :-P)

Going thru ur list - I have picked up Meghmani idea and have started analysing that.

Another one that can be added to the comprehensive list is HEMISPHERE properties. This also fits in my (1) explanation where the timing of value unlocking is nt clear bt the MOS is very wide.

Consolidating the threads :- Yes, let me go thru all the major threads once( vl probly get more ideas :-P) and see how everythng can be best accomodated.

Disclosure :- Cos. mentioned for knowledge purpose only. I may hold some of the positions above and might exit as well when odds change.

Is there any website,which lists the upcoming spinoffs(demerger).Also the stocks which are removed from nifty and related indices like banknifty etc.

I read in gleenblatt’s book that when a big company spun off a part of it’s business,the institutional investors generally are forced to sell the stock as they are not allowed to own anything below a certain market cap and liquidity.

Meghmani organics ; Meghmani Organics Limited and Meghmani Finechem Limited will be listed on 18 th of August 2021 in T2T Segment

No intraday activity

5% circuit Limit

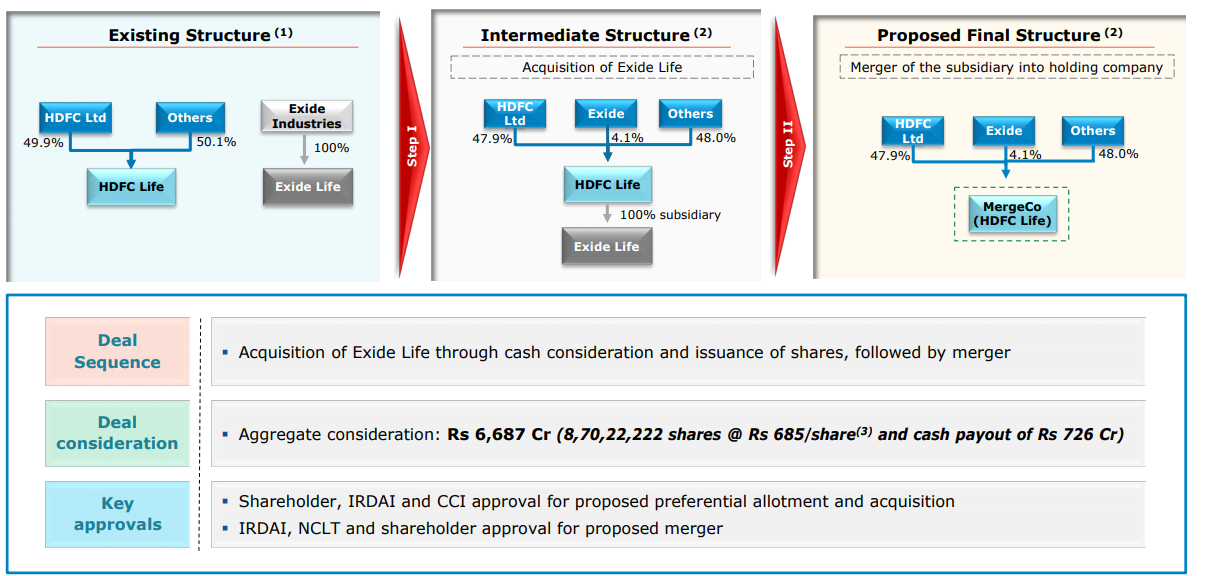

Hdfc Life has given value to Exide Life business is 6687 Cr with cash payout 726 Cr inclusive in it.

Exide will now have a valuable stake in HDFC Life as promoter which will definitely be a long term value to Exide Industries, I believe more such mergers will come in Insurance business as consolidation happens and it was becoming increasingly difficult to compete in Insurance business

Exide can focus more on their storage battery business after merger with Hdfc Life as a group

Now Exide has 1000 Cr PBT and 700 Cr PAT Business with it which trades at 15000 CR - 6687 Cr= 8313 Cr which gives it a multiple of 12 PE to their Battery business while its close competitor Amara Raja trades at multiple of 17

(Note: Amara Raja is growing its topline while Exide is not able to grow its topline i know many people who have shifted from Exide to Amara Raja also it seems that many mechanics push Amara Raja compared to Exide as per my observation but question is at what valuation of Exide is available which compensated all this risk these question can only be answered by investor themselves) Conclusion:

Exide will have 4.1% stake in HDFC Life which most likely will really valuable in future when Insurance Industry go in more mature phase of their cycle.

Battery Storage Division which is available at 12 PE which is 25% ROCE Business (Competitor having 17 PE) but with low growth in topline these sector might get a rerating if tailwinds comes in these sector because of EV (Still in Nascent stage as per me) Please note following thesis won’t be applicable if merger is not allowed by regulators.

Check following post to track upcoming special situations.

Disclosure:Tracking & No position in Exide and Invested in Hdfc Life. This is not a Buy/Sell recommendation please do your own due diligence not a SEBI register advisor.

Call it a coincidence or wat, I’ve been writing abt this frm Exide perspective on Exide thread : -

I was studying the battery players whn this event happened. IMO, it is a fair decision on part of Exide to sell the insurance business at 2.5x EV. not sure abt HDFC Life bt yes Exide seems undervalued now frm purely valuation perspective.

How do you value exide?What would be the valuations of a market leader in battery segment,if the growth runway is still very long.

If we assume 10 years from now,profits go up three times and valuation multiple goes from 17.4 to 25,then the stock goes up 4.5 times,that too in ten years for about 20 percent annual return.

I feel the appropriate place for this will be the Exide thread & probly the Amara Raja thread. Anyways, I was also looking for some valuation perspectives & approached @harsh.beria93 for the Same in case of Amara Raja as below :-

On similar lines, my 2 cents on Exide valuation : -

Earlier case with Exide Life

I valued batteries standalone business on earnings multiple basis separately & insurance part as a multiple of embedded value : -

Pretax operating earnings of last 2 yrs. = 974 crs. discounted to 10% CoC minus 2% perpetual growth rate gives 974*12.5 = 12175 crs.

Insurance business at 2 times embedded value i.e - 2711*2 = 5422

Investments conservatively valued minus Insurance business = 1000 crs.

Total = 18597 crs.

Post Exide Life case : -

HDFC paid 2.5x EV; so net that out & rest remains the rough valuation.

My main concern regarding both the battery manufacturers is regrdng thr mgmt & that’s stopping me frm taking the position apart frm the business aspects.

Disclosure :- no investments as of now in Exide or Amara

along with Greenblatt’s book , I must say its an excellent source.

along with Greenblatt’s book , I must say its an excellent source.