@Naresh on xchanging - how would u arrive at a fair value of 105/110 for delisting ? Also - when does the rbb process start ?any changes u think on delisting strategies post vedanta failure ?

This is new game … investor has to be cautious. Some times it’s best to not tender shares, when we are not sure of honesty of promotors in first offer and let the price get discove. They are bound to accept all shares till one year at agreed price even afte delisting.

Just my views…

The indicative price for delisting of Xchanging solution is 56.50 as per company’s exchange filing which is at a discount of around 40% from the current trading prices and share price is down 16% today.

2 Likes

if xchanging technologies (indirectly owned by csc/hp) falls below 65,

it would be a great buy with enough margin of safety.

will post more details once results r declared

disclaimer : i am invested in xchanging technologies, this is not investment advice. pls do your due diligence before investing.

1 Like

Xchanging seems an interesting turnaround story.

| FY 2018 | FY 2019 | FY 2020 | |

|---|---|---|---|

| Sales | 186 | 184 | 182 |

| OPM % | 14% | 23% | 26% |

| PBT | 41 | 57 | 59 |

| PAT | 32 | 47 | 55 |

| Cash + Investment | 201 | 259 | 327 |

| Receivables | 31 | 29 | 21 |

Business started to have significant turnaround as margin is concerned in FY 2018. Seems to be pretty irregular before that. It seems they have removed certain part of business from this company. Sales dropped from 307 Cr to 186 Cr in FY 2017 to 2018. Company is able to convert most of the PAT into cash in last 3 years. But they don’t pay dividend and all the amount is invested into less than 3 month treasury or is bank balance. Wondering why would one want to do that? No new capex, investments in fixed assets. Company has given approx 50 Cr as loans. Company mostly writes off receivables and does transactions mainly with subsidiaries companies. Wondering why a subsidiary company would start giving another subsidiary company such a nice margin and >20% ROCE (after removing cash, business is generating ~60 Cr profit on 250 Cr assets)? Why do they not pay any dividend at all? With current information on hand, I doubt management would de-list if the share price goes too high (>100). Don’t see any immediate requirement and past management action. Sunil singhania from Abakkus Growth Fund had been holding from June 2019, Is it a turn around play? Having a basic fundamental view on stock would be required for downside protection in case de-listing does not go through.

3 Likes

hii regarding the fantastic margins of xchanging, could it be that since csc and hp enterprise both r involved in dxc technology which is the owner of xchanging

they are not able to use xchanging to get work done at low margins(like hp used to do in the past before blackstone came into the picture with mphasis)

2 Likes

Wintac delisting PA. Details in the link. Experts views invited.

Hi All,

Anybody looked at\considering the demerged entity of Tata Communications - HEMISPHERE PROPERTIES LTD.

The co. listed in Oct 2020 and the erstwhile shareholders of TCL booked profits as the got the demerged entity shares.

Based on co’s recent filings - " the title deeds of land bank are yet to be transferred to the name of the company. The company is required to pay stamp duty of Rs. 651 cr. on such transfer of land in the name of the company."

Assuming stamp-duty to be 5%, the value of land bank comes out to be approx. 13000 crs. Considering a holdco. discount of 50% the price comes out to be 6500 crs.

However, owing the selling pressure created from spin-off and the overhang of a majority-govt. held stake the company is currently valued at 1865 crs. almost 70% discount to calculated value

The objective of co. is to dispose, develop the 740 acres of land bank which is primarily in Delhi, Pune and Kolkata.

This isn’t a classic arbitrage given that timelines are not fixed but the co.'s deep discount to the value of assets it will be holding can itself be a trigger for re-rating.

2 Likes

I have done some basic digging into Hemisphere properties and am mildly interested with a small 1-2% position initiated around 59.

Starting pg 50 in the below document provides a quick (and blurred ) view of the layout of the land holdings and very basic details of the 36 legal cases pending. 23 of the 36 cases are related to the land in Dighi, Pune, 8 with mostly Govt parties for the Greater Kailash land , Delhi and 4 for the Chennai land.

https://www.sebi.gov.in/sebi_data/attachdocs/apr-2018/1523427841352.pdf

Most of the past news articles that Google provides talk about using NBCC as an agency to execute real estate projects on the land - at some point in time.

So, maybe just wait for news flow in the next 2-3 quarters and understand more on how much time it can take to work out. It took 10-15 years for the listing to happen - so maybe we need to have more patience to figure out if this could work out from an investor perspective.

Anybody researched into this. The record date is 11th Dec. Not sure how much of value unlocking is there, but considering that record date is around, it’s worth checking if sufficient IRR is there or not

1 Like

One more company recently announced delisting plan. LKP Finance. Floor price has been set at 75 bucks.

2 Likes

Xchanging Solutions Delisting Bidding starts today

Floor Price 44.64

Indicative price 56.50

CMP 77.5

As per shares distribution mentioned in 2020 AR. It seems that ownership is concentrated on a few people. 91% of the stock is owned by just 26 shareholders out of which there are 3 promoters. I believe if the company has a strong intention to delist. It can convince this small group of shareholders. But stock price movement in recent pastr does not support this narrative. Post announcement of delisting in Oct 2020, the price went up to 90, but it came down to a CMP of 77. Today also down by ~ 2.5%.

Is the stock overvalued so that market believes that prices should not go up. With the change in stock fundamentals over the last few years, it does not seem overvalued at 15 PE.

2 Likes

Xchanging Solutions update:

In 2016, the company did not accept the discovered price of Rs 109. Now, the latest attempt at delisting has failed as the company could not get adequate number of shares offered by the shareholders (about 11.9% of total outstanding shares were offered).

Cn anybody tell me what happens in xchanging solution now after their delisting has failed?? What are the learnings can we draw from such behavior of promoters ?

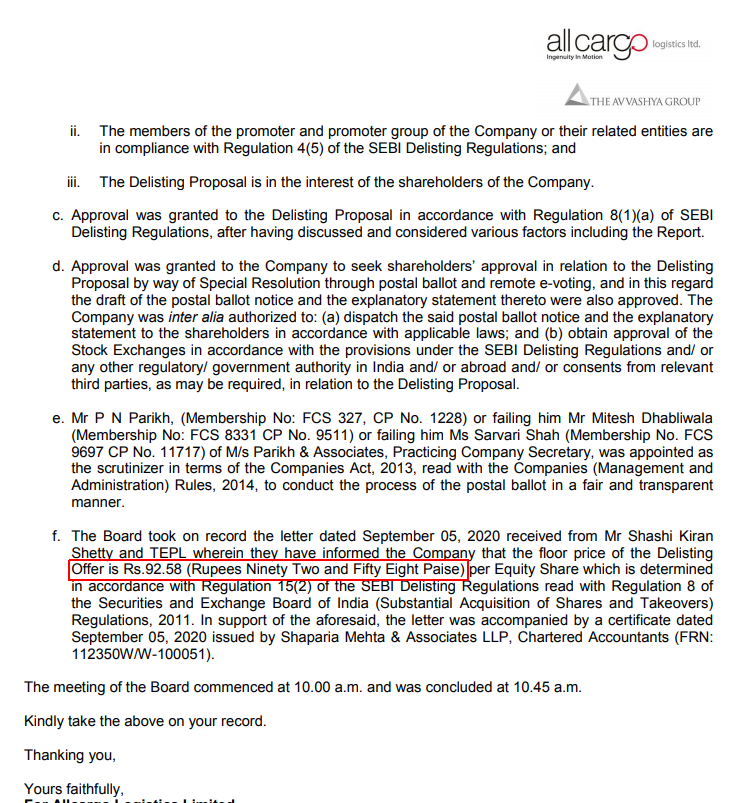

Anyone invested\tracking Allcargo logistics delisting? Seems to be a low-risk bet currently. The price is abt 35% above the floor price bt the fair valuation shd be arnd Rs. 200 considering Gati’s takeover and turnaround.

1 Like

LKP Finance delisting update.

LKP Finance had announced delisting on 01-Dec-20. Promoters hold 63.6% of stake. The floor price was Rs 75.

The discovered price during the book building process was Rs 140. Promoters did not like the price. They have decided not to accept the discovered price and have also decided not to make any counter offer. Delisting offer has failed.

The table below shows how the market price moved during this episode.

| Date | Event | Market price | Change |

|---|---|---|---|

| 01-Dec-20 | Announcement after mkt hrs | 62 | - |

| 02-Dec-20 | 1 day later | 74 | 19% |

| 03-Dec-20 | 2 days later | 89 | 20% |

| 04-Dec-20 | 3 days later | 98 | 10% |

| 17-Dec-20 | Board approval | 112 | 14% |

| 25-Jan-21 | Shareholder approval | 112 | 0% |

| 05-Mar-21 | Bid open | 102 | -9% |

| 12-Mar-21 | Bid close | 128 | 25% |

| 15-Mar-21 | 1 day prior to result | 125 | -2% |

| 16-Mar-21 | Offer result | 100 | -20% |

| 17-Mar-21 | 1 day later | 80 | -20% |

| 18-Mar-21 | 2 days later | 74 | -8% |

4 Likes

Compared to time taken for these delisting processes to close, the Allcargo logistics delisting is taking a lot of time. Thr’s been no news on that since the price announcement.

Anyone has any update on this?

2 Likes