you get the right to offer the shares to the promoters at the final delisting price within 1 year of delisting.

1 Like

Thanks a lot @Naresh

There is another delisting in early stages, Shreyas Shipping!

Don’t find it compelling enough to bet on.

1 Like

I got a reply from the exchanges(NSE) that the application has been sent to the company for resubmission. So, this might get delayed for a month in my opinion. Yet to receive a reply from the company on the expected date of the resubmission of the application to the exchanges.

2 Likes

TTK HEALTHCARE

Revised floor price from 1051 to 1201

2 Likes

The downside is more protected now. The observation and consequent delay in in principle approval for this reason only.

1 Like

This is the additional checks in delisting. Look at the pattern in hexaware and TTK. There have not been any delay whatsoever at any stage at least at the company end. Now look at other companies from Alcargo., Vedl, adani power and judge if what’s the additional check to judge the success of delisting and promoters intentions.

1 Like

Wanted to share one more thing that many might have in their mind. Given the momentum in the market, the small caps and midcap have given better return than playing delisting. Yes, true. But this is a hiding place, where returns will only come to those who have patience and appropriate allocation. In my opinion, the market is overheated (by valuation) and you can confirm that through the fact that fund manager (who are long only) are more frequently on the media to justify the India premium valuation. So, if somebody is afraid of the valuations at broader level, properly analysed delisting cases are places to hide and earn an above average return( > 12%). Problem with special situation these days is it has become mainstream. Seth klarman in his book “margin of safety” has clearly stated that as more people chases the special situations, the potential return gets lower. Therefore, it is necessary to be selective even with the special situations. Remember, on the other side of the trade ( Company) there are smarter merchant bakers who will try to control the prices in their favor.

2 Likes

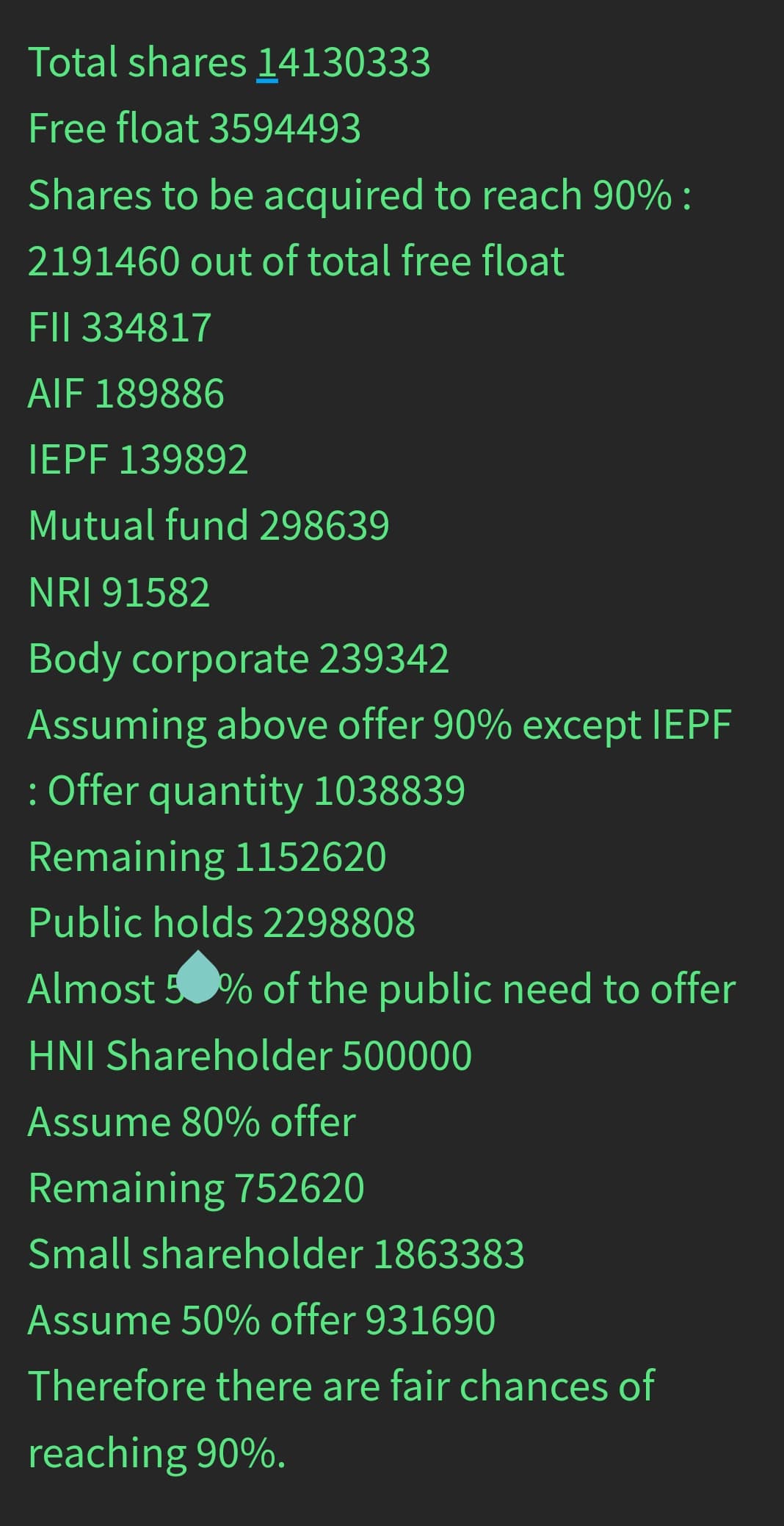

Regarding TTK healthcare delisting,

What is probability of delisting going successful ? Out of minimum of 90% total shareholding requirement, as per current shareholding

~75% is by promotor,

16.5% is holding by Retail shareholder (13% small less than 2L capital)

5.5% with MF & FII,

1% in IEPF

~2% Corporate and NRI

To me it appears that without any large fund holding/tendering and retail holding key to delisting, reaching 90% itself is difficult when cmp and floor price is not huge diff. Since promoter hold quite a large stack, remaining 15% asking for higher price may not make dent on delisting price derivation.

For fund houses, the average buying price matters. Most of them bought the stocks at the lower level (look at the recent price moment). Assume yourself being a fund manager, where you are being offered an exit price (1200) on a stock that you bought a few years back at less than 25% of the CMP(Rs 900). Assuming the Final Exit price will be Rs 1500, Will you accept that offer? The judgement will be based on the EBIT/EV i.e. RoIC (From the investor’s point of View). The promoters have themselves stated that the opportunities may be large in the business but in the near term outlook is not good. So, as a fund manager will you accept the good return (at this point) and invest funds in other opportunities or will you stick with the business (That may not generate alpha for an uncertain period of time)?

If I were a fund manager, I would have chosen to exit and redeploy the funds in other opportunities.(Remember, a fund manager is answerable to his owners). This is a business where competition is intense and achieving higher RoIC will remain lower. Therefore, in my opinion, there are higher chances that Company will successfully get to the 90% Milestone. On Qualitative judgement, this passes the promoter integrity test. Retail shareholders have little say and will offer as per RBB price and fund managers have an advantage as I listed above. This is my process, one may have their own. Delistings are analysed more from qualitative angles than Quantitative and that’s why it remains a grey area.

2 Likes

Not many mutual funds own shreyas and for ttk it is 6% held by mfs which is good for TTK to delist and it could make them sell at a lower premiums due to their own performance pressures.

That’s why there are lower chances on anything above 1500/-.we’ll have to wait for things to unfold.

1 Like

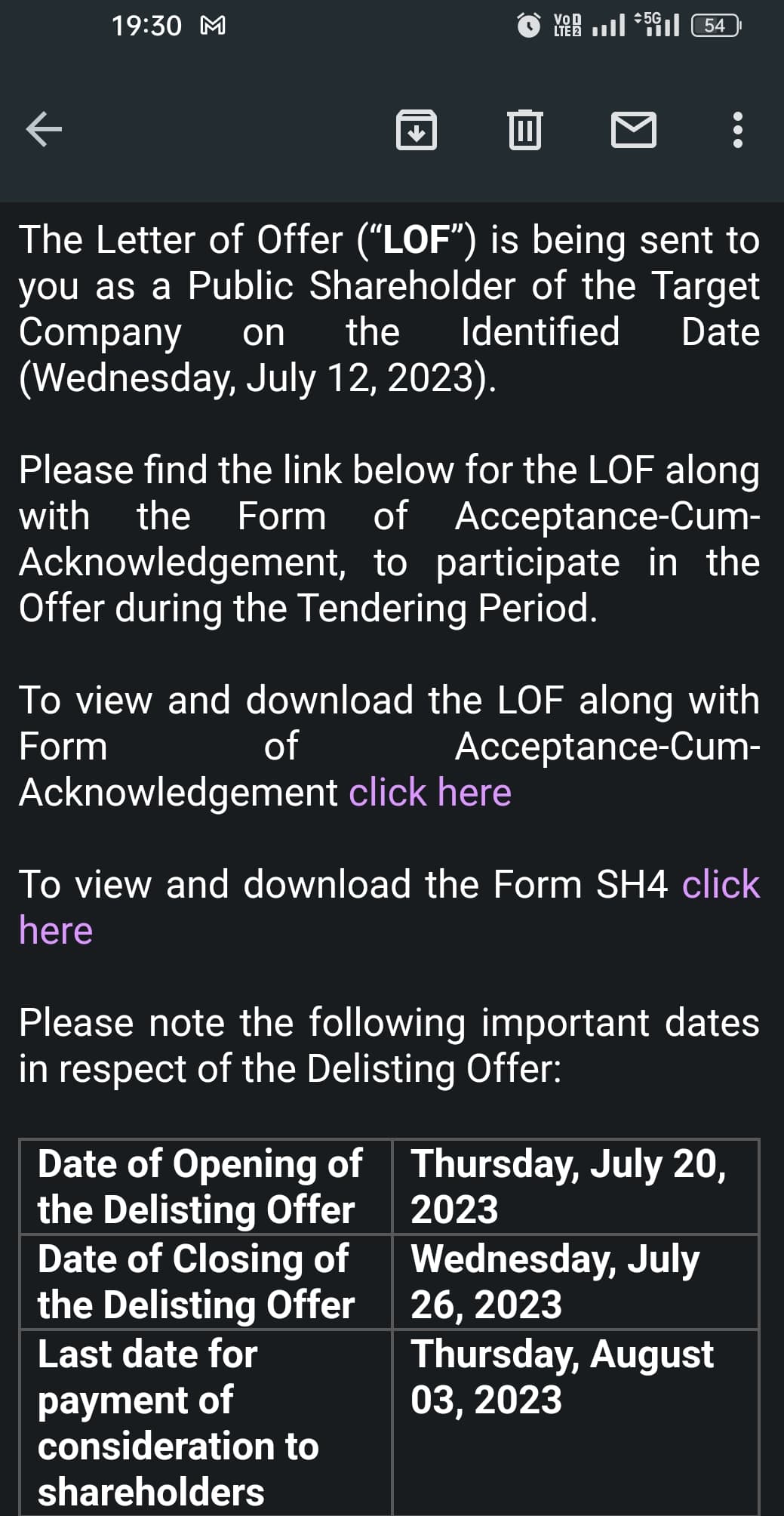

TTK submitted the clarification to NSE on 04.07.2023. As per the mail from the NSE, they will count 15 working days afresh for the grant of approval. The implied date for in-principle approval is now 26.07.2023 (Provided, no more issues with the application.)

1 Like

Lo ji ho gaya approve.

1 Like

Remember, the delisting is deemed to be completed at a price where the 90% quota gets filled. Therefore, we need to track the RBB Proceedings both at NSE and BSE. I’ll update the same and the price of offer here. Stay tuned.

1 Like

1 Like