Largest 3rd party express parcel player: Express parcel logistics is all about optimizing last-mile costs, as they form the largest cost component. Higher drops per trip drive cost efficiency. The larger the market share, the greater the pin-code coverage, the better the in-house route optimization technology, and the higher the efficiency. As the largest player in this industry, Delhivery benefits from these cost efficiencies.

Unorganised to organised shift in PTL business: The PTL (Partial Truckload) business in India is largely unorganized and dominated by local/regional players. However, customers often suffer from mediocre service levels and delivery delays. With the implementation of GST, pan-India players have an advantage over local operators due to better cost efficiencies and superior service levels. Delhivery has demonstrated strong execution post the initial challenges following the Spoton acquisition. Growing at double digits while the industry remains largely flat reinforces Sahil Barua’s point that Delhivery can continue gaining market share regardless of overall industry growth.

Integration of PTL and EP network: If its current plans to integrate the PTL and Express Parcel businesses succeed, the cost benefits due to higher utilization levels will lead to strong operating leverage playing out at scale.

Opportunity: Logistics in India has historically been inefficient, presenting a strong case for a technology-driven, pan-India, cost-efficient player. Delhivery has a good opportunity to be that player.

The company has already demonstrated strong execution in the Express Parcel business, achieving 15%+ Service EBITDA margins

They have learned through their failures post Spoton acquisition and have shown consistent improvement in PTL margins.

Companies like Amazon have tech to get robots into their supply chain. No wonder opex players like Delhivery are getting slaughtered. This plane jane company has no technical moat

I don’t think, robots will be used for logistics(atleast within next 10 years). In Amazon warehouse, yes they can use robots. Delhivery is in Express parcel delivery, Truck load logistics - this segments cannot be replaced so easily with robots/drones.

American workers are much costlier than Indian workers …right ? Have you done any cost analysis whether replacing Indian workers with robots will bring any cost benefits or its just a we must do what amazon has done thingy ?

As anticipated, Delhivery using cash on books for inorganic expansion in Express parcel segment. Its best bet is growing its market share through similar inorganic expansions in the future resulting in economics of scale, lower costs and higher margins. Apart from this, from a product differentiation point of view, not sure how 1 logistics player is different from another.

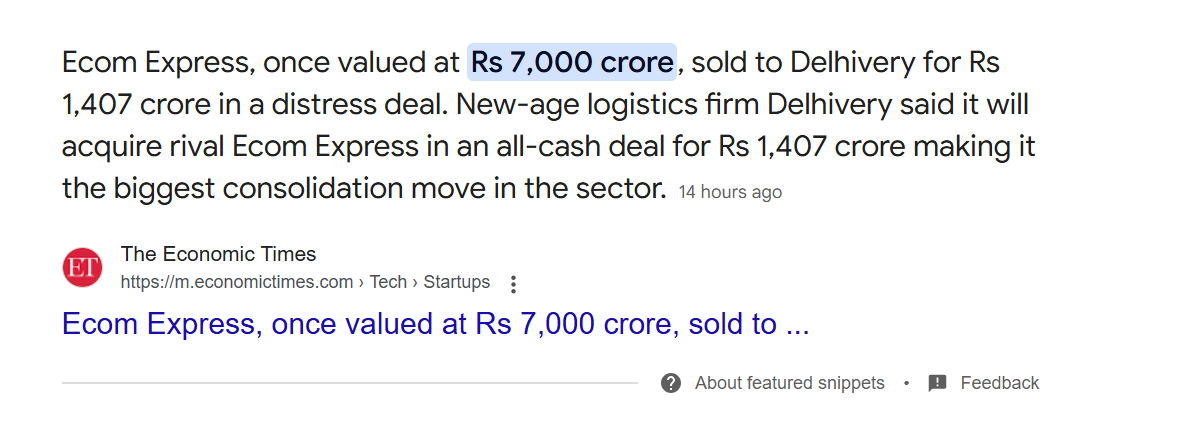

Just 6 months back it was about to bring this to IPO with staggering valuations at 7000 crores now they sold it to 1400 crores. 80% discount. One sould be cautious while applying IPO as most of the IPO are came with very high valuations. As usual retail investors are the jokers always. I am still puzzeled how come anchor investors agreed for such a discount?. what’s cooking inside ?

It’s business as usual. Time was against them. They already raised 320million$ (~2700 crs). IPO was supposed to be the exit.

A lot of things went wrong for Ecomm express.

Meesho insourcing logistics - client concentration - ~50% revenue came from meesho.Considering their revenue was around 2600crores, it must have reduced to 1300crores

unfortunate demise of the ceo back in 2023

failed ipo attempts twice.

Im guessing valuation was at 1x sales (they are still loss making)

For DELHIVERY, this acquisition can enhance tier 2 and tier 3 (meesho is/was primarily tier 2 and tier 3)

Post the recent acquisition, Delhivery released FAQs answering queries on their profitability and how Ecom’s PAT loss will affect Delhivery’s P&L consolidation.

Few things that can be overlooked in Delhivery results:

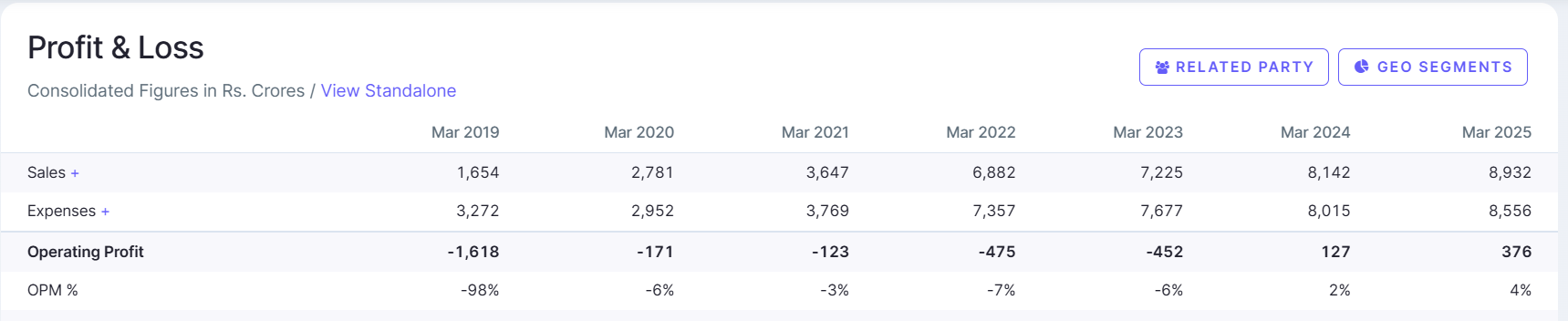

PAT at 162 crores for FY25 ( Almost 230cr change is due to how depreciation was calculated. YOY comparison with FY24 method - PAT will be at (68) FY25 vs (249) FY24

Only expects 30% volume from EcommExpress previous clients (100% overlap in clients).

300 cr integration costs expected.

Ecomm express acquisition will reduce Capex (since EcommExpress has Falcon Autotech machinery/automation - same as what Delhivery is using)

Quick commerce for B2C seems to be operating at 350-400 orders per day. It needs 700+ orders to break even. They seem to pivot towards B2B quick commerce (darkstores for clients who need time critical delivery - spare parts, etc)

Some of your points make sense but what about Op. profit, which is 3X from last year. As volume goes up, operating leverage kicks, in. They are using huge scale in WH automation, Container Trucks (40 ft vs 32 ft) etc…

As I talk to some Industry experts, they r telling there will be 2 big players in mkt , 1. Blue Dart,which always plays on high margin & low volume 2. Delhivery , Low margin & High Volume…+ smaller players. Xpressbees ..( MLL nearly surviving on parent’s support), Consolidation is happening..

Primarily serving E-commerce and D2C clients in India

Vast network covering > 18,800 pincodes

Enables B2C deliveries with industry leading transit times and real-time tracking capabilities

Competitors are: Xpressbees, Ekart, Ecom Express, Shadowfax, etc.

Delhivery’s acquisition of Ecom Express: A boost to the revenue and long term profitability in the express business

In April 2025, Delhivery announced the acquisition of Ecom Express for a cash consideration of Rs 1407 crores

Ecom Express was facing major issues internally as its largest client Meesho started insourcing

Ecom was eyeing to go public at a valution of USD 700 million before it went down the downward spiral

This acquisition reinforces Delhivery’s competitive position in the industry, will reduce pricing pressures and will result in increased volume in the express parcel business

Part Truck-Load Business:

PTL market in India is between USD 20-30 billion, of which only 15% is the share of organized players

Caters to B2B cargo shipments that are too large for parcel delivery but don’t require a full truck

Fastest growing segment, grew at 25% in FY25 YoY

Clients in Apparel, Consumer durables, Auto parts, FMCG, Industrial and B2B e-commerce

Strong shift from unorganized to organized players: trust, speed, real-time tracking and reliability

Some clients are Amazon, HPCL, etc. Other clients data is not publicly disclosed

Delhivery’s Technological Moat

Proprietary Logistics Operating System: Over 80 interconnected applications

Automation at Scale: operates automated mega-gateways and sortation centers

Data Intelligence capabilities: used for demand forecasting, delivery time estimation and capacity planning

They have invested significant capital into building these capabilities and they continue doing so.

Their customer facing apps:

Delhivery One: for Corporate clients

Delhivery Direct: for SMEs and Individuals

Rs 1400 crores will be used for acquisition of Ecom Express

Remaining Rs 3000 crores will be there with Delhivery to pursue future acquisitions, ventures and capital investments

Intra-city logistics

Startup inside a startup

Porter is the market leader in this segment with:

FY24 Revenue: Rs 2733 crores

A few days back, Porter entered the unicorn club by raising USD 200 million round, shows the industry potential of Intra-city logistics

Already launched in Ahmedabad and Delhi. Will launch soon in Mumbai and BLR.

All in all, Growth Drivers are:

Industry consolidation

Growth in e-commerce and D2C- megatrend

Yield per shipment improvement due to productivity growth and economies of scale

Unorganized to Organized shift in Part truck-load and truckload

Proprietary technology and high automation

Asset light operations

Entrepreneurial team

Risk factors are:

Insourcing by major players

Shift to quick commerce is an overhanging risk

Pricing pressures due to competitive intensity by loss-making funded startups

Financial Assumptions:

Business Segments Growth:

Express Parcel segment can grow at 10% CAGR due to industry consolidation and growth in E-commerce

Part Truck-Load business is growing very strongly in last 3 years, Revenue in FY23 at Rs 1157 crores which increased to Rs 1889 crores in FY25, it can be expected to grow at 12% for the next 5 years

Delhivery Direct, an Intra-city logistics business is an optionality, if executed well, this business can itself be worth Rs 8,000 to Rs 16,000 crores

Other businesses of Supply chain services, Full Truck Load and Cross border can be expected to grow at 4% CAGR going ahead

Current EBITDA margins of the consolidated business is at ~2%, which will go up with economies of scale, cost rationalization and industry consolidation

EBITDA margins in Express segment assumed to be at 18%, as competitive intensity will ease going ahead

EBITDA margins in Part Truck load business can be same as those of Express segment mgmt. guides, however we can assume it at a long-term margin of 16%, similar to pureplay Part Truck load competitors

Future PAT margin could be 7% of overall business in FY30

Financials FY30E can be:

Revenue: Rs 16500 crores

Operating Profit: Rs 2233 crores

PAT: Rs 1000 crores

Current Market cap as of May 29, 2025 ~ Rs 26,800 Crs

Conclusion:

Strengths: Technological moat, wide network, great service and reliability helps commands premium, strong financial position with huge cash on the balance sheet

Opportunities: Can emerge as a winner after industry consolidation plays out, Intra-city logistics and unorganized to organized shift

Risks: Insourcing by major e-commerce companies, Shift of share of online commerce to quick commerce from e-commerce and pricing pressures from other well funded startups

Overall: Delhivery is a disruptor and market leader in 3PL and can emerge as an integrated logistics giant, valuation will be sensitive to growing market share and profitability expansion

E-commerce has emerged as a thing only during the last decade. I think Ecomm’s fate will begin a consolidation in this sector, as burning cash wouldn’t be prudent now.

Delhivery has a strong balance sheet, and the management has good experience in the sector. This business might do well and further acquisitions are possible.