Delhivery is the largest and fastest-growing fully-integrated logistics services player in India by revenue as of Fiscal 2021

Delhivery operates a pan-India network and provides its services in 17,488 PIN codes, as of December 31, 2021

Delhivery acquired Spoton in August 2021 to further scale its PTL freight services business. Spoton delivered 758,730 tonnes of freight in Fiscal 2021 and had a network presence across 13,087 PIN codes with 2.85 msf of infrastructure as of December 31, 2021.

INDUSTRY OVERVIEW

Indian logistics had a direct spend of $216 billion in the fiscal year 2020

Expected to reach $365 billion in the year 2026

Growth cagr expected at 9%

Factors that drive growth in this industry:

E-Commerce, B2C culture

Favourable legal support

Increased spending on logistic services

Underlying growth of the Indian economy which in turn rise demand for goods which requires logistics

Organised players accounted for only ~3.5% of the logistics market for fiscal year 2020

The Indian logistics industry is characterised by high indirect spends on account of high inventory carrying costs, pilferage, damage and wastage. Indirect spends were estimated at US$174 billion in Fiscal 2020 and are expected to marginally decline to US$166 billion by Fiscal 2026.

SEGMENTS OF THE INDUSTRY

Road segment is the largest mode of logistics in India.

The total road transportation market was estimated at US$124 billion in Fiscal 2020 and is expected to grow at a CAGR of ~8% to reach US$200 billion in Fiscal 2026.

Express Parcel: Fastest growing segment of Road Transportation

Key trends: E-Commerce, Category expansion, New payment methods, New business methods, Value added services.

Part Truckload (PTL) Freight: Rapidly shifting towards Organised Players

Truckload Freight: Largest segment of Road Transportation

The TL market has been historically fragmented

High Intermediary costs

Inefficient matching of supply and demand

Possible Changes that could bring opportunities:

Digitalisation of supply chain operations

Real time visibility and control

Data led efficiency

The domestic rail transportation market stood at a size of ~US$21 billion in Fiscal 2020, which is expected to reach US$47 billion by Fiscal 2026 at a CAGR of 17%.

Rail’s share in freight has been continuously declining,CAGR standing at 18% in 2020 (versus 71% for road transportation).

DOMESTIC AIR EXPRESS TRANSPORTATION: NICHE SEGMENT WITH LIMITED GROWTH

Waterways isn’t opted by the company

Warehousing:

India had a per capita warehousing stock of 0.02 sq. m. as of 2020.

While warehousing space taken up fell 11% YoY in Fiscal 2020, overall warehousing market growth has been robust, at 44% CAGR during Fiscal 2017- 2020.

Demand for warehousing is being driven by rapid growth in e-commerce, organised retail, manufacturing and international trade.

Business undertaken by the company

Value objective: “To enable customers to operate flexible, reliable and resilient supply chains at the lowest costs.”

Active customer base of the company can be found across a diverse spectrum of :

FMCG

Consumer durables

Consumer electronics

Lifestyle

Retail

Automotive and manufacturing

Key differentiators of the company from the rest in the industry:

Integrated solutions: Provides a full range of logistics services

including express parcel delivery, heavy goods delivery, PTL freight, TL freight, warehousing, supply chain solutions, cross-border express and freight services and supply chain software, along with value added services such as ecommerce return services, payment collection and processing, installation and assembly services and fraud detection.

Proprietary logistics operating system: The in-house logistics technology stack is built to meet the dynamic needs of modern supply chains.

Has over 80 Applications

Asset-light operations: We follow an asset-light model. As of December 31, 2021, all of our logistics facilities were leased from third parties.

Risks faced by the company:

A history of losses and negative cash flows from operating, investing and financing activities and we may continue to experience losses and negative cash flows in the future as we anticipate increased expenses in the future.

incurred restated losses for the year/period of ₹17,833.04 million, ₹2,689.26 million, ₹4,157.43 million, ₹2,974.92 million and ₹8,911.39 million in Fiscal 2019, Fiscal 2020 and Fiscal 2021 and the nine month periods ended December 31, 2020 and December 31, 2021, respectively.

Negative cash flows from operating, investing and financing activities

Relies on technology a lot for its operations and won’t be able to survive without constant upgradation

Issue for sale is not appraised by any financial institutions or banks. Only the fresh issue is to bring in funds. Shows that the funding and deployment of said funds is not viable according to the banks

High employee costs

Dependency on third parties and travel partners

Competitive pricing makes profitable numbers impossible on the market, meaning very few chances to carry out a profitable trade.

Contingent liabilities that can destabilise the company on maturing

Operate in a highly fragmented industry and face intense competition, which could adversely affect our results of operations and market share.

Major part of the business is with limited huge consumers , whose actions would affect the company

Defaults of payment by consumer would seriously affect cash flow in the business

Equipments used in business including vehicles are leased failure to renew which would materially affect the business

Insurance may be insufficient to cover all losses associated with our business operation

The PTL segment of Delhivery is new segment comparing all other segment but the problem lies in their operations they pay more to their vendors and they (Delhivery) recieve less from their client’s may be they are doing these to maintain their vendors. But how Long they can do this if they want to break even in PTL segment or want to turned themselves into profit they needs to on-board their own truck rather than outsourcing to vendor’s it will bring down their cost but one time investment will be large in purchasing their own trucks.

Source: My friend work in Delhivery for almost 2 year’s in PTL segment and he told me about this.

They have a large share of express parcels mainly caterting to Ecommerce. Majority of the chunk comes from Ecommerce marketplaces.

The questions to ask are:

Are they price takers or givers in this segment?

What is the moat here when compared to the likes of Shadow fax, ecom express, Express bees. All operating in the same Ecommerce segment

Can they engage with D2C brands to reduce the dependencies on big marketplaces?

I come from an ecommerce background and here are my 2 cents:

They work on very tight numbers in the Ecommerce segment since 40%+ of the numbers are driven through the marketplaces. They have an opportunity to cater to small SME’s who want to transition to an online model and want to outsource their ops to the likes of delhivery. If they can execute their margins will go north, else they will continue to be at the mercy of the likes of 4 big ecommerce players of India

I read one interview for IPO where on being asked about situation of new age companies, they said that they are not new age tech companies but are very much brick & motar company…I am guessing what would they be saying if their IPO came before the new age tech meltdown?

I was a former employee at Delhivery. Sharing a few points which might be of help:

Delhivery has great capabilities to execute at scale. This company has got that operational DNA required to manage huge shipment volumes and therefore they are well placed to gain with increasing shipment volumes in future

Since fixed costs are huge in logistics, their economics improve significantly with scale. This is a big differentiator from other ecomm companies which are burning money for growth and therefore their losses also increase

Delhivery has relatively much better technology than their listed peers. There are a lot of softwares which are required to manage manpower, fleet, shipments, etc. and all these are developed in-house and constantly improved through ground feedback at a faster pace as compared to outsourced tech

The leadership team is always close to ground. You can easily find the CXOs on the floor of warehouses observing and solving stuff first hand

In terms of work culture, not a great company and this reflects in their attrition numbers, specially in technology teams which is currently a factor hindering them from moving faster. If they are able to solve this, then they can grow even faster and become a major global player

Disclaimer: The idea to share this is to provide more info for better decision making but in way a recommendation to buy.

Is this not the narrative for every company that with scale the economics would increase significantly? Same is for other tech/non tech companies as well…infact, it may hold true for every listed as well as unlisted company…

If you just look at growth aspect the ecommerce logistics can grow upwards of 30% so this is some companies that can’t be ignored.

But in these uncertain times with all stocks looking for there correct price and a buisness that is actually is in very early stages getting an ipo is good but not for most.

The market will correct and value it itself so one of the stock to watch in these new age tech listing I personally have added in watchlist with nykaa and zomato.

All three have some problem may it be no proper buisness moat in case of delivery specially can they actually be unrivalled or not, nykaa crazy valuation and Zomato path to profitability.

Looking at there buisness other then scale and reach can they actually have any pricing power as most of there buisness is asset lite but working capital heavy that could be very painful specially if anything like capital stuck is there and depend on some clients that may be the biggest ecommerce is a good thing and also a bad thing.

Buisness is good but valuation multiple for such business according to me is unknown specially looking even they don’t know what will be there long term margins and how logistics work in India its very hard to even compare with foreign peers as logistic cost is India is actually one of the few countries where it is decreasing even in these low worker and high fuel scenarios.

Without any clear margins after the sector matures it’s very hard to even predict what will be the valuation that it can be cheap or very expensive also.

Agree with the narrative point but in most of the ecomm companies the variable costs are more dominant than fixed costs (like discounting, etc.) whereas in logistics, fixed costs are more dominant (warehousing space, leased trucks, manpower, etc.) that is why the chances of them improving profitability with scale are much higher. Have experienced this first hand in Delhivery. Margins improve significantly during the ecommerce sales as most of the facilities/ trucks/ manpower run on near 100% utilisation and there’s a baseline shift every year with increasing volumes.

Had a cursoy look at RHP and found that its competitor blue dart is asset heavy and still makes a profit… while they claim to be asset light and still have a negetive ebitda

also huge employee costs of 20% ?

They claimed to have about 2000 Cr cash in the books. But I am wondering from where did it come?? They are cash negative in ops so it cannot be earned cash, If its cah from liabilities , why they are adding the liabilities by cash from IPO? They could have been more transparent.

This is a asset heavy business and I am yet to come across any success story which is asset light in the segment.

Delhivery granted a patent for its proprietary technology product, Addfix. This is an in-house developed location intelligence technology built over mountains of data collected by Delhivery in last 11 years. You know how the addresses in India are not very simple and a lot of people end up putting incomplete, wrong information in their addresses. This leads to wastage of resources in finding those addresses. Addfix helps the last mile courier agent in reaching the exact location even if the address in not accurate or incomplete. Selling this software licenses itself has a huge potential for revenue.

We are importers of tennis and Badminton equipment in India. For domestic logistics we used FedEx from 2012 till 2021. For pin codes that FedEx didn’t cover, we used Professional Courier.

Then suddenly FedEx decided to stop it’s domestic operations in India and Delhivery took over their business. Dealing with Delhivery has been fantastic so far. Much superior to FedEx. They cover almost entire pin codes and we now don’t use Professional. So our entire business is with them.

Unlike FedEx where reaching out to “Point of Contact” was a terrifying process, in Delhivery we get instant response.

So with respect to B2C and B2B operations with them, we are extremely happy.

Just wanted to highlight a consumer’s point of view with Delhivery.

Apart from non-Amazon, non-Flipkart volume(roughly 20% for delhivery) it depends a lot on other ecommerce players along with other D2C players. This volume is bound to drop as customer acquisitions slow down and also discounting at order level. Attaching public information available that will correlate with what I am saying. This is substantial volume that will be hit and growth will slowdown. Also, there have been 2 reports today both projecting growth nos on the assumption that e-commerce will grow at 35% pa.

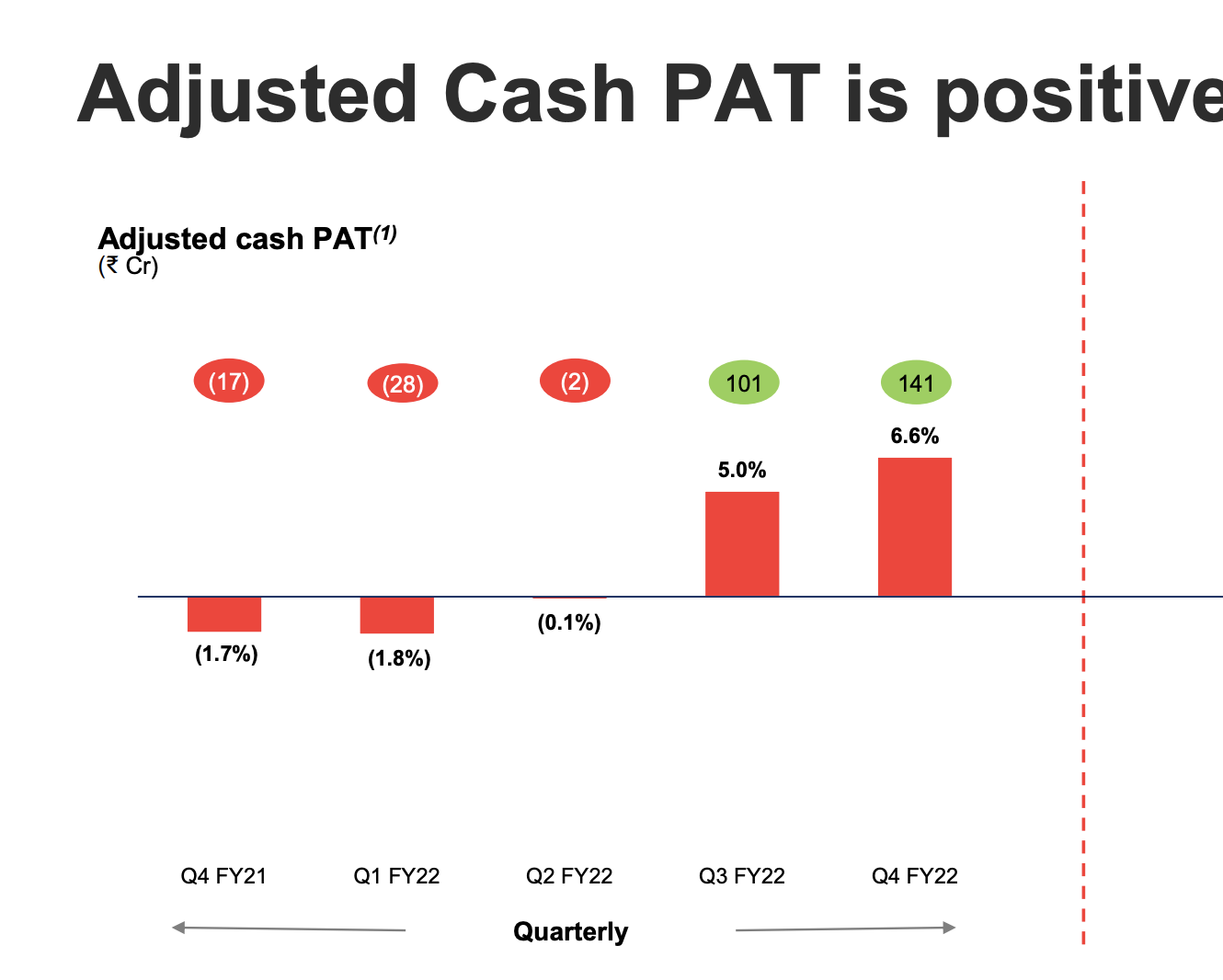

Operating leverage - incremental EBITDA generated over the incremental revenue between Q1 and Q4 has come in at close to about 24.6% (from transcript)

Low cost - In the short term, Delhivery is aspiring to reduce overall logistics cost and pass on the benefits to the customers. This will create significant moat.

From transcript - the more money we save our customers, the more they have to invest in their businesses. … as Delhivery brings down the cost of logistics, several categories which were previously unviable in eCommerce suddenly start becoming viable. And so it is important that we continue to pass some of our efficiency gains back to customers. Now, the extent to which we will continue to pass these efficiency gains back to customers is a pricing decision that we take at an individual client and sometimes at an individual category or individual lane level, so it’s a little hard to predict.

Efficiency - yield per parcel is brought down from 92 ('19) to 72 ('22) in a time frame where fuel costs increased from 66 to 93

Inorganic - Delhivery has 6358 Cr cash available for inorganic opportunities. SpotOn is purchased at 1900 Cr. Company is eagerly looking for build vs buy options.

Capex - CapEx for financial '22 was at about Rs. 466 Crores. Our CapEx as a percentage of revenue has come down from 9% in financial '19 to 6.8% in financial '22, and our expectation in the medium term is that this will settle at about 5% and in the long term, at close to about three and a half to 4% of revenue.

The cash generating capability of the company should be in-line with their Capex forecast. Inorganic opportunities should take company to next level with respect to revenue and cash generated.

It’s a loss making company that has consistently lowered it losses across the last 4 years and has broken even in FY22 with Operating leverage waiting to kick in in coming years.

The first part though optically correct is probably not a complete summation of the company today. Q4 results posted above has the data.

If good companies with competitive advantage are available in good valuation …Then why someone should think about loss making companies…If it has some competitive advantage …Then it will continue to make profit consistently…Therefore nothing wrong if u miss initial years of that company…

My investing criteria is very simple…

High entry barrier,

Competitive advantage,

No loss making,

Profit making,

No capital intensive business,

No PSU,

No debt,

High ability to give back cash to the shareholders,

Should be available in good valuation,

Products and services offered by the company are so good that any idiot can run the company…

I can talk whole day regarding not to invest in PSUs. But lets talk in brief.You have to consider the basic purpose for which PSUs are created.Post independence,there was capital crunch in country and FDIs are not possible.So govt has to set up Steel Plants,Airline,Coal Mining Companies etc. in tax payers money.That is perfectly fine.But you should ask questions that when after so many years…if money is available in the country to build these things ,then why govt is holding these things in the name of PSUs. Consider an example -Lets say after Independence ,govt put 500 crores and set up 5 steel plants through Steel Authority of India (SAIL).Lets say after 20 years investment came to India and Jindal,Bhusan all set up steel plants.Then what would you think the value of the govt steel plants would be if any body else setup steel plants in the country.Definitely the value of the govt steel plants will go down.Then what was the perfect time to monetize these PSU steel plants.Govt would have get best price for the plants when the Jindal,Bhusan etc. were thinking of setting of their plants.Govt could have gone to them and said that …don’t setup the plant and buy my plant.If they already set up their plants, then the selling price of the PSU plants will decrease.Then why govt did not do it.Simply because vote bank politics.This is all about the asset management in PSU.

Now consider the efficiency part in PSUs.The PSU’s always recruit good talents with written exams like reasoning,aptitude,engineering,General knowledge etc…etc…but why they produce mediocre results on profit/loss.Because its the process which delivers result not individuals .HDFC bank can deliver good result with average people because of its good processes where as SBI and PSU banks will deliver mediocre results as they do not have efficient processes.

Salary of an employee in Private bank is a function of demand and supply of talents,skills,profit of the bank etc. where as a PSU Bank employee’s salary is a function of inflation,Fixed annual increment etc.

If there are vacancies in HDFC bank and PSU bank …then which would you select first …think … HDFC bank is more profitable than almost all PSU banks…So by logic every one should be applying HDFC bank …Now ask your near and dears… about their view regarding this vacancy…you will be surprised by the answer.

Again if job security is the parameter for creating excellent result for the company…then do you really think that "Lockheed martin’s " job is more secure than “Hindustan aeronautics limited”.Then why is this huge difference between their results in terms of innovation.

Apart from this what u think… to whom LIC would listen …its retail shareholders or Govt.LIC will serve govt’s interest or its retail shareholder’s.During LIC IPO no body asked tough questions to LIC management about the value behind the buying of IDBI bank.

Govt do not sell PSU when its demand is very high…it sells PSU when it need money…means distress selling…no pricing power …by the time govt sell PSUs…the PSU’s already lost their competitive advantage.What you think …would any body buy …BPCL,HPCL 's petrol pump network once Relience setup 50000 new petrol pumps. At present BPCL,HPCL etc. are taking losses …say Rs.10-15 per ltr at present…What do u think, who will bear these losses…its the shareholders who will take the losses…so read a lot from books on investment…and stay away from business channels…They will tell you to buy LIC…sorry for any grammatical mistake