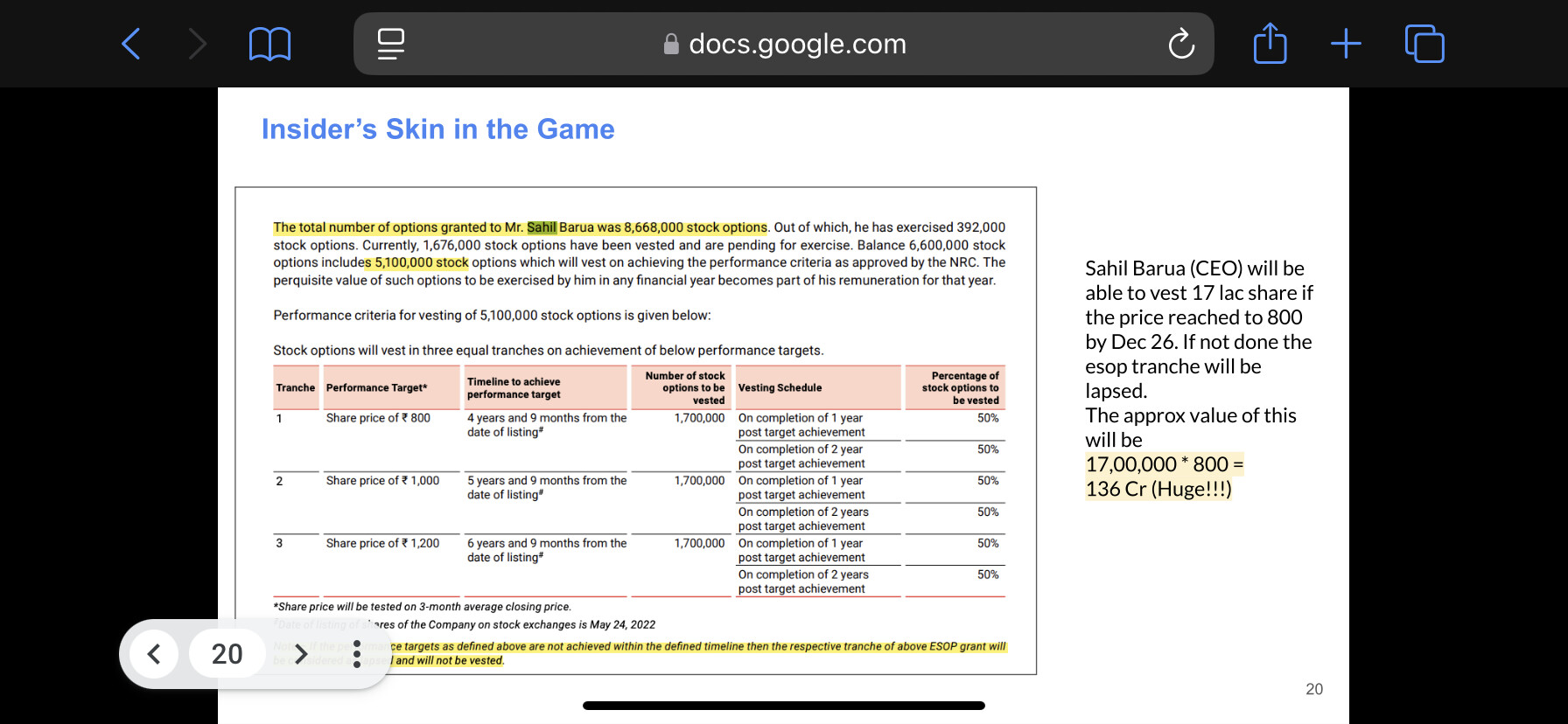

This is very interesting - I wasn’t aware that stock vesting can be based on price performance of the stock. Good that CEO (promoter) will work towards achieving that price however it will result in significant equity dilution.

5 Likes

My personal experience - I ordered via jiomart and it was delivered by Delhivery. Because of a size issue, I placed a return order within 10 mins of delivery. Generally, with Amazon/Flipkart, it is picked the next day/few days in case of Flipkart. With Delhivery, he picked up within the next 5-10 mins. I asked the delivery boy and he said he got an alert - that talks about technology use.

Having said that, Delhivery always had FII investment. With the last month FII selling and the lower reported numbers from consumption/industrial, expect weak set of Sep Qrtr numbers. This should pick up in Q3 for e-commerce/PTL. Supply chain services is also a growing area. Overall, good managements - waiting to hear Q2 company concall.

6 Likes

Writing this from my memory after listening to concall yesterday

Sahil(CEO) sounded very confident in growth.

One particular statement - We will push the pedestal on growth even if consumption remains sluggish.

Delhivery has a unique MOAT - The ability to do PTL + Heavy across all its Pincodes. None of the other 3PL players have this capability. For instance, if someone orders refridgerator in a tier 2 city, other players will mark these pincodes as out of reach and charge a premium but with Delhivery they charge the same (reach for heavy is high). This translates to delhivery having the highest market share for things like furniture, cycles, etc

Few things that could be the next lever for growth

- Shared warehouses for quick commerce players (mentioned in last concall, pilots soon in Bangalore)

- Franchise at the last mile - we will see lot of delhivery stores in locality - Similar to DTDC

Interesting points:

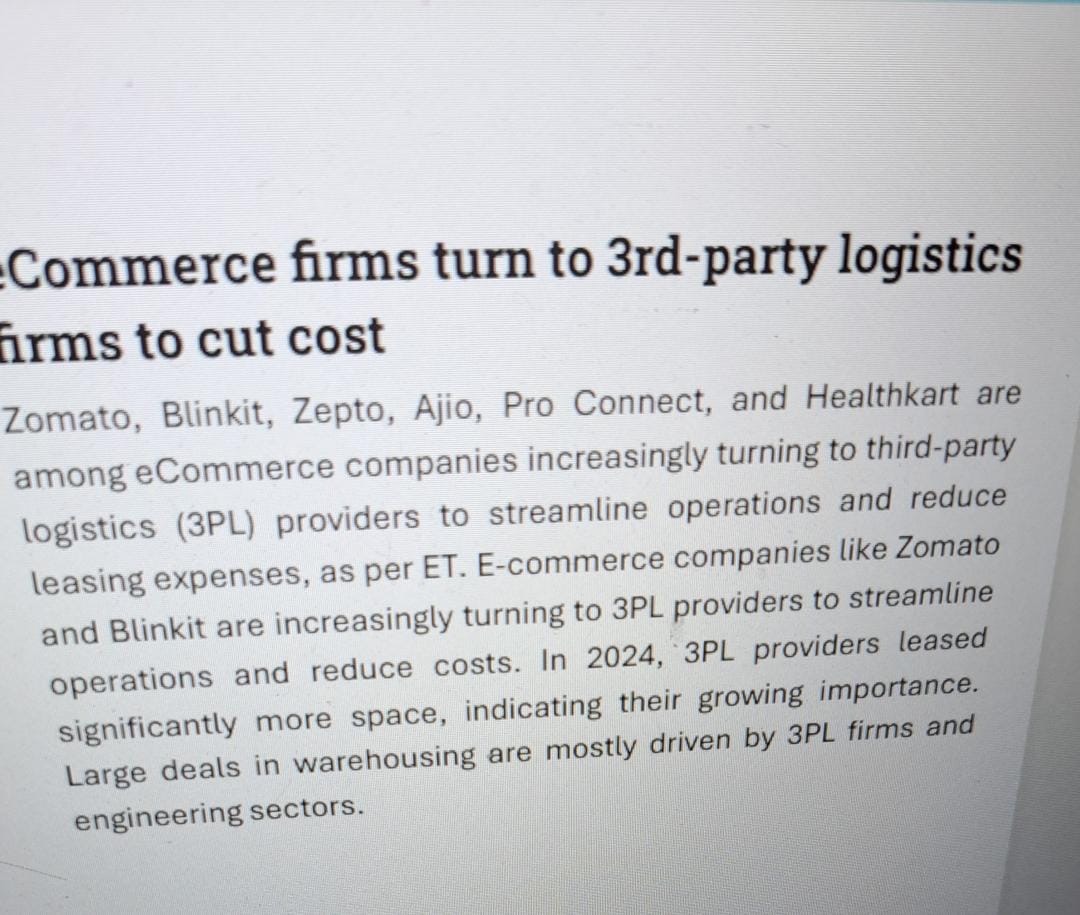

- Amazon/Flipkart does 90:10 split (90% is in-sourced only 10% is out-sourced). CEO believes this is not in the best financial interest. Flipkart’s Ekart logistics losses ballooned 5x in fy24

- Meesho’s valmo strategy is behind them - Most of the effects felt

Not liking the number theatrics:

- Changed depreciation from WDV to SLM last quarter

- Cash that was received in October was already provisioned in September quarter

Nothing wrong with these but has been bothering me

Disc: Invested

3 Likes

Some other points that i observed

Express parcel count shippedin october was 80 mn + indicating a decent festival season bounce. Last quarter averaged 68 mn+ monthly

Will also launch

Air package express service on prime routes( its only on non prime routes so far)

Data products coming out of their delhivery one platform for d2c companies

Their q com service pilot in bangalore was probably for amazon tez / flipkart minutes

None of these growth intiatives are immediate in nature. They will add to revenue over time. The only way to grow meaning fully over next 2-3 quarters is

Grow parcel business ( seasonality favors)

Grow ptl business (high confidence)

Show positive PAT and YOY growth and over q1 fy25 ( reasonable confidence)

Their operating cash flows are healthy but they keep investing every year leading to FCF being low.

At some point someone has to ask what is the investment for and when will operating leverage play out

Good thing is 5k crores cash on the books has stayed that way for last 10-12 months and nothing stupid has been done with it

Sahil barua is a great guy and a good strategy thinker. Maybe its day one for him and he is playing the long game like bezos but he is testing the public market patience

Disc: invested from higher levels

9 Likes

Based on the TTM numbers, look like this financial year the company will turn into net profit for the first time!

- Not invested. Studying.

2 Likes

There annual capex for the last 3 yrs has stayed in the range of 500 cr and can easily be met through Operating cash flow (~220 cr for FY23-24 post lease liability) and return from cash on balance sheet (~6k crore). The main use of cash might be for some M&A, which could also reduce some competition from the competitive express parcel/ LTL vertical.

P.S. — Not invested. Studying.

3 Likes

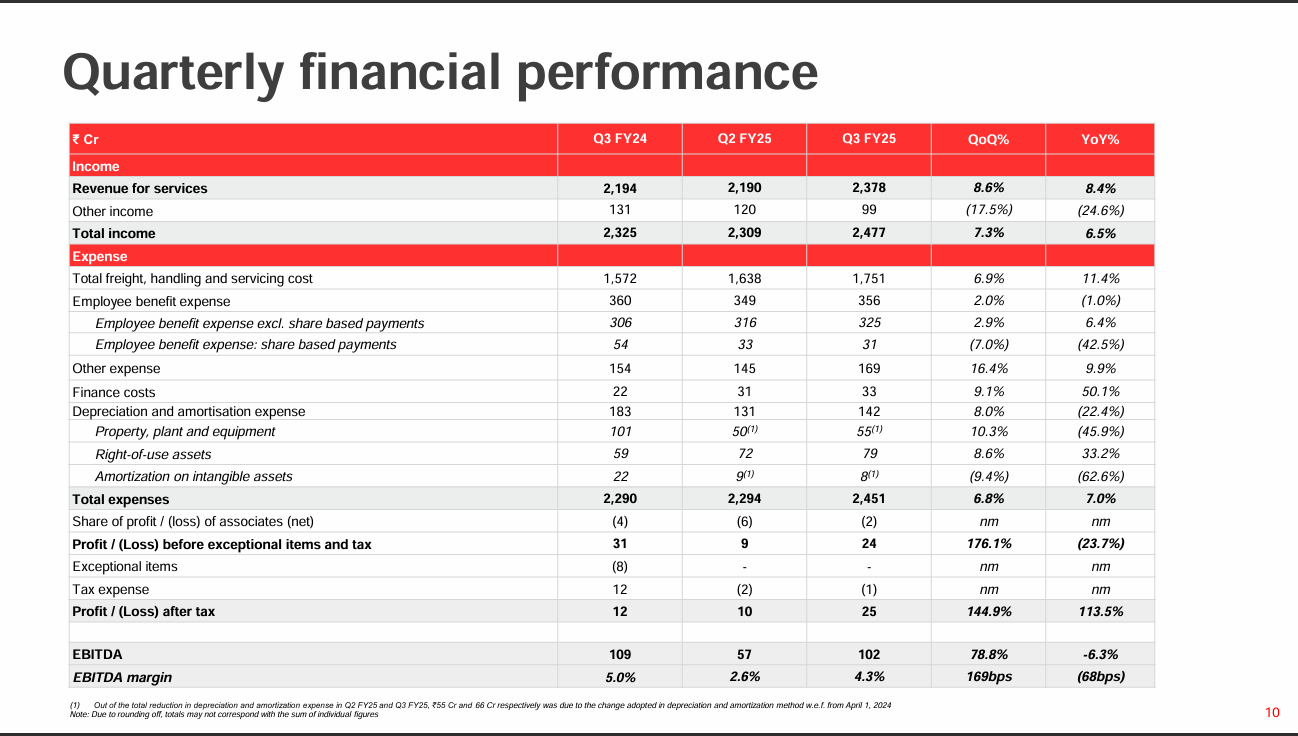

Great results. Company on track to report net profit for FY25.

However, express parcel revenue had a muted growth despite the festive season (peak season for e-commerce). What are your views on this? Are they losing market share?

Express parcel revenue increased from 4191cr in FY22 to 4552cr (8.6% YoY) in FY23 and 5077cr (11.5% YoY) in FY24. However, in FY25, the past three quarters had 1276cr, 1298cr, and 1488cr. Assuming another 1200cr in the last quarter, their FY25 express parcel revenue growth will be less than 5% YoY, although the express parcel segment is reportedly growing at 32-34% (according to RedSeer). Is Delhivery losing market share to other 3PL players or is the 3PL segment losing share to the captive segment?

In Q3FY24 concall, Sahil Barua noted that

Our expectation is that the market (e-commerce / express parcel) grows somewhere between 15% to 20% annually

and guided that this segment will continue to grow at a similar rate.

2 Likes

Sahil Barua repeatedly mentioned about how in-house logistic arms of amazon& meesho are in losses hence burning vc cash(specifically valmo) and eventually they need to increase prices. In such scenario 3pl’s like delhivery may benefit, which has more than 100% share of profits earned by all e com parcel delivery players during recent period.

1 Like

From Q3FY24 to Q3FY25 a lot has changed in terms of market dynamics.

- Overall Indian Economic growth has slowed down,

- Quick commerce has emerged significantly eating up of e-commerce share (Though Sahil Barua is of the view that it has not eaten up much of ecom share).

- Meesho was a large customer till Q3FY24 whose share in total operating income has declined after insourcing from them. Excluding Meesho from previous year I think Delhivery has grown at a satisfied rate.

- Even other companies like Blue dart, have shown muted growth despite not being serving to Meesho in Q3FY24. While in PTL VRL’s tonnage growth was 1% yoy.

So, 15-20% growth is definitely not there in express parcel. Also Delhivery has lost market share with exit of Meesho in Q4FY24, post that the impact is there in yoy performance of express.

Some of the concerns according to me are:

- Delhivery has incurred fixed cost for rapid commerce to variablise the cost of D2C brands but makes the company asset heavy. Also, according to him the market size is limited as only 8% of the movement of goods are intra city. Will depend a lot on increase in daily orders for this segment to become profitable. (As informed, 500 order per day is processed right now, and almost need 800 orders per day for a dark store to be profitable)

- Despite other players increasing their prices why is Delhivery not doing so? Probably they are playing on volume game and hence take advantage from operating leverage.

- High freight cost has dampened the margins. Though Sahil said that they will enter into long term fixed contract to prevent from sudden price hikes.

- Mr. Jyotiraditya Scindia said in a press conference that India post will also be entering into logistics business which again will increase competitive landscape for the industry. India post might benefit from long reach in rural as well as in urban areas.

Disclaimer: Invested at higher levels.

4 Likes

I know Sahil mentioned that there is a recokning waiting to happen in this space.

This came out today.

Meesho insourcing majority of their volumn onto their valmo platform is changing the landscape I would have to guess.

Growth even in single digits is decent in these tough times imo.

Disc: Invested. Did some consulting work for Delhivery back in 2018 where I worked on automated signature detection.

4 Likes

Delhivery commands premium valuations but without much core IP. Their key is ‘fully integrated logistics provider’. This space is very low margin as the service providers are squeezed by biggies and biggies are trying to save by having their own in-house delivery

Without any core IP developed, what is the future for Delhivery? What could be the ‘buy thesis’ on this?

Buying delhivery is more like a bet, you can’t buy these shares on valuations.

There are many examples in the market where valuations don’t make sense but they are bought on future assumptions are story sold (Eg:Zomato few years ago). As of now company is giving profitable quarters & per concalls they are trying to push themselves while sustaining.

Disc: Invested!

I am trying to understand what is the ‘story’ here. Zomato is a tech company and has tech at its core and you are buying the tech story. What is the tech at Delhivery when this is going to be disrupted by robots in the future?

IMO just because the company doesn’t have tech that doesn’t mean that they can’t disrupt the market.

Secondly as per google company has been in market since 2011 that is 14 years in business.

I believe at this point after going through so many cycles & decisions Sahil won’t leave a room for error.

In the end when most of the things are going online delhivery has a chance to capture market in all segmets, you say it they have it.

Note: Could be biased because invested !

This explains the thesis well. Tech is in terms of their superior logistics model, sorting, etc.

2 Likes

This is dated from a year ago. I wonder what is their position now. It will be interesting to find out . Price then was between 350-400. CMP is 260

Their jan 2024 projections at 9k crore revenues were marginal Negative PAT. Delhivery is actually ahead of that as of today (with some help of change in depreciation policy)

If they still hold their position and have bought more then i admire their conviction.

Disc: invested in delhivery at similar levels with similar ideas but didnt have as much detail as they had in their notes.

In my view: the single biggest reason to buy delhivery is that they aim to be the lowest cost operator and share the cost benefits with their customers. If they do that they will continue to gain market share. This is a very amazon like thought process and will do very well in the long run.

The question often is how long can investors wait.

What i dont like is that they continue to invest despite guidance of slowing or reduced investments and the depreciation kills the PAT.

If you look at FCF post capex its practically nothing and you think the entire 5 k cash on books FD return would have given you better profits than running the whole company.

In my view the only way out of this is growing revenues in double digits . Unfortunately e commerce their main revenues stream is growing in single digit only and they cant increase prices because they are the lowest cost player.

It will take time to scale up PTL and other smaller revenue stream so this is a really long hold.

That said at some price this business will become too cheap.

today if you knock off 5k crore from Market cap you get 15-16 k crore valuation.

At 30 x multiple ( same as solidarity) they need 500 crore pat TODAY on TTM basis to justify current price.

I dont see them doing 500 crore PAT in next 2 years also.

Will i buy more of it at 10k crore market cap net of cash? Probably

2 Likes

Yes this is reason for my investment as well. PTL is growth and margins are expanding - war chest of 5K is meant for inorganic opportunities but per latest conf call they don’t see any in the immediate future.

Express parcel delivery will do well when insourcing : outsourcing ratio changes. Conf cakl suggests that current scenario of preference of control will give way to economic sense at some point.

Another reason is CEO share vesting is conditional upon stock performance so am hoping that skin in the game helps in delivery, pun intended.

2 Likes

Disc: Invested and biased.

My thesis:

- The profits generated from Logistics players are concentrated heavily at the top. Bluedart is trying to increase its market share in ground but its margin are contracting. Delhivery on the other hand are consistent even with volume increases. Their networks are designed to handle much larger volume

- Meesho insourcing had a great impact on the industry as a whole. Amazon and Flipkart hardly outsource 10%, meesho was the one responsible for providing volumes to 3PL players. With valmo, they become a threat to 3PL overnight. Delhivery has managed to brush it off

- PTL segment looks promising. Express + PTL run on same integrated network. I’m not sure how the efficiency will playout. This quarter PTL had more expenses because volume surged in Express (Both a bane and boon)

- I like businesses that try to do one thing great, unlike many which run behind shiny, trendy things. In Delhivery, its quite simple, be the most cost efficient player to move a box from Point A to Point B. This is a talk from CEO 8 years ago (https://www.youtube.com/watch?v=tyZuZyxAsZY) and nothing has changed since

- India is a very price sensitive market and hardest to satisfy imo. You can see reviews of Delhivery online. But people still use Delhivery for pricing reasons.

- Tech company of sorts. I had a friend who visited FedEx in middle-east, they still use those windows XP kind of systems.

Valuations might be stretched at the moment. But I think Delhivery can be a wealth creator in the long run

9 Likes

To be a wealth creator, it has to grow revenue at double digit and show increase in margins

Revenue is growing in single digits and under pressure as all e-commerce vendors are in-sourcing. There is no moat in personal deliveries. Everyone is looking to squeeze money out of the supply chain.

If valuations are stretched now, then it was 480 odd at IPO time and it has almost halved now. No growth or appreciation in last few years and better to keep money in FD than in Delhivery

4 Likes