Inefficiency - Most of the PSUs are managed by IAS officers on rotation basis with 3-5 years time frame. Based on my conversations with few managers at PSUs, every MD/CMD wants to make their own mark and doesn’t continue the previous management’s initiatives. This kills the progress and repeats the cycle. IAS officers are not proficient in the area of business. One manager at JSW told me that they won’t even think of purchasing Vizag Steel Plant because it is so inefficient - massively overstaffed.

For a promoter run business, their entire wealth is tied to the company & they have incentive to create shareholder value. Their family is with the business for couple of decades. They know in & out of efficiencies etc,.

Govt forces them to do their bidding. Say invest in x MW Solar etc,. to reach their targets. Most of the times, these moves are share holder unfriendly.

Example - A company like neyveli lignite which gets ore at super cheap rates failed to create share holder value in last 10 years. See how SBI & other PSU banks end up holding lot of bad loans. (goes with 1)

Exception - HPCL buyback is one of the few rare value creation decisions undertaken by a PSU

In their decision stack, I wonder if PSU management even think of creating shareholder value in their list of priorities.

The Ken had covered Delhivery in its story last week:

It’s behind a paywall. But here is the gist:

In 2018, D2C brands were just 5% of the overall e-commerce volumes. Today, the number has reached 20% and is likely to touch 43% by 2026. And Delhivery and its rivals are racing to capture this growing cohort by luring them with the promise of same- and next-day delivery.

But this is not the first time that India’s largest third-party logistics player has tried this. Costs came in the way of Delhivery’s previous attempts as most D2C brands do not have deep pockets, and Indian customers used to free deliveries don’t want to pay either.

Given the high potential of D2C commerce, enabling same- and next-day delivery for hundreds of cost-conscious D2C brands while also fending off intensely competitive rivals at the same time won’t be an easy feat for Delhivery.

Delhivery majorly depends on few ecom players for its express parcel business. I already mentioned in my previous post, how the other two ecom players are entering this space, which would dampen’s delhivery’s growth.

Below is a classic example, of how another ecom player with 100% of logistics outsourced is seeing the future: Link

This will result in a price war atleast in the mid mile. Delhivery may still be competitive in the first and last mile, but in the mid mile space expect a lot of players with spare capacity.

Looks like Express parcel business should grow a healthy 30%+ this quarter. The asset light business should aid in servicing the growth. No visibility yet on the PTL , FTL and supply chain business. Also, the prices in express parcel havent been hiked and should be in 69 rs range. Considering this is 60% of revenue, should see the Quarterly nos grow a healthy 20%+.

Indian ecom is still growing on a smaller base. World wide ecom volumes are dropping, so that should be factored in while looking at this business.

Yes correct, betting on Delhivery has a lot to do with Indian E-commerce space

But I don’t understand one thing. Why E-commerces companies want to outsource only some part of their logistics and want to keep captive logistics operations?

It is mainly got to do with user experience. You can control the quality by having captive logistics, however it comes at a cost. Its a different strategy adopted by FK, AZ who have their own logistics and others like Meesho , Nykaa have completely outsourced. FK, AZ outsource mostly during sale events when their in house capabilites cant serve peak load.

Got it, can you also give a light on why blue dart being in express delivery segment making good OPM and Delhivery is not? - I guess it is due to blue dart is doing this on its own, asset-heavy business, own vehicles, employees, and everything they own, that is the reason right? - On the other hand Delhivery is outsourcing everything to network partners and they might have to pay higher to them, that is the reason they have low margins?

If you look at Blue dart customers, majorly are banks, fin institutions and other categories which deal with precious cargo. The order value is higher in most cases and customers deal with either confidential information or items like jewellery and so on. You can think of receiving your credit card, pin and so on.

Delhivery is over indexed in smaller value, price sensitive categories like Ecommerce and Delhivery relies on fewer clients for a lot of orders, hence the pricing power is low.

Blue dart also has a separate vertical of air cargo which gives them a higher premium. But that said, having a asset heavy buss is beneficial when the utilization levels are high.

Q3’23 results were pretty subdued and growth was missing (flattish growth QoQ and -9% dip Yoy).

There are finer prints in the con’call.

On the express parcel, festive season was a qtr earlier, hence the growth here was flatter.

On the PTL front, basis the Jan’23 runrate, PTL is now doing 100k ton/month.

The express parcel guidance is now at 15-20%, expect them to hit 1bn parcels by FY’26.

Some good insights on the PTL front where they aim to be the lowest cost player doing a EBITDA margin of 15-20% in a stable state. ( In PTL i believe VRL is the only one to clock 15%+ EBITDA margins). They want to focus more on B2B customer where the yields are lower( right now it is ~11rs/kg) but the loads are more predictable.

Claim nos were still higher, but its a lagging no. In express buss, reverse logistics can at times go beyond a month

The growth is not at par with the other listed new age start ups. But like other listed start ups, there is a move towards profitability may be at the cost of growth.

----------------------------------------------------------------------------|-----------------------------------------------------------

-------- Notes (rephrased per my understanding) from FY23 AR -------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Guiding principles:

Improve supply chain operations efficiency and pass a meaningful proportion to customers

Invest in creating a large-scale infrastructure and network that meets a wide variety of customer requirements

Continue upfront technology investments for higher network reliability and speed.

Continue ESOPs to attract and retain high quality talent

Continue to communicate regularly and transparently with shareholders

FY23 performance update:

Overall network speed improved to ~3.6 days with 91%+ service reliability across entire network

Incremental margin [the margin on every incremental rupee of the revenue] >50% in the transportation business

Invested further in building strategic infrastructure and deploying cutting-edge software, data products, industrial automation, and robotics systems across our network.

New automated terminals at Bhiwandi and Bengaluru

Automated parcel sortation capacity increased to 5.4 million packages/day [+35% YoY]

Trials with Automated Guided Vehicles (AGVs) to reduce manual handling and effort

Inducted 387 new tractors into our fleet, taking the total count to 562. Expect to see deployment of tractor trains on select routes in late FY24.

Launched Delhivery One, which is well suited for SME and D2C customers. It enables customers to directly access all the logistics services and data solutions through a single interface.

Orion (Truckload exchange) is now the single source of capacity for Delhivery’s intercity trucking demand (internal contracted and on-demand) beside servicing external customers and our Supply Chain services division.

Continued to acquire new customers and integrate operations more effectively across our newer lines of business: Supply Chain, Truckload and Cross-Border services.

Investments in Vinculum and Algorhythm have expanded value proposition to e-commerce and enterprise customers. For instance, we maintained leadership in the key growth segment of D2C e-commerce (>75% growth in FY23) through a combination of acquired order management solutions, warehousing and transportation capabilities.

Continue to work with financial institutions to identify ways to lower financing cost for our clients and partners, thereby reducing the indirect supply chain costs.

We believe we have immense value creation opportunities through our data solutions and through the OS1 platform and will continue to invest in these in FY24 and beyond.

Key differentiators:

Integrated full range of logistics services

In-House developed logistics platform with 80 applications that orchestrates all the services

Data based decisions for geo-location, network design, route optimization, load aggregation, ETA prediction, product identification and fraud detection

Automated sortation centers, and material handling systems, system directed floor operations, path expectation algorithms and machine-vision guided truck loading systems

Interoperable network that allows to share infrastructure and operational capacity across business lines and set new service standards, such as providing e-commerce-like turnaround times to traditional part-truckload shippers on several lanes.

Invest only in critical service elements and IP-sensitive areas of the network, while delivering services through many network partners who own warehousing, freight (truckload or air) or first/last-mile capacity. The systems of your Company match partner capacity with Delhivery’s internal and third-party client demand based on partners’ service quality ratings and pricing. This approach minimizes fixed costs and enables the Company to scale as per market demand.

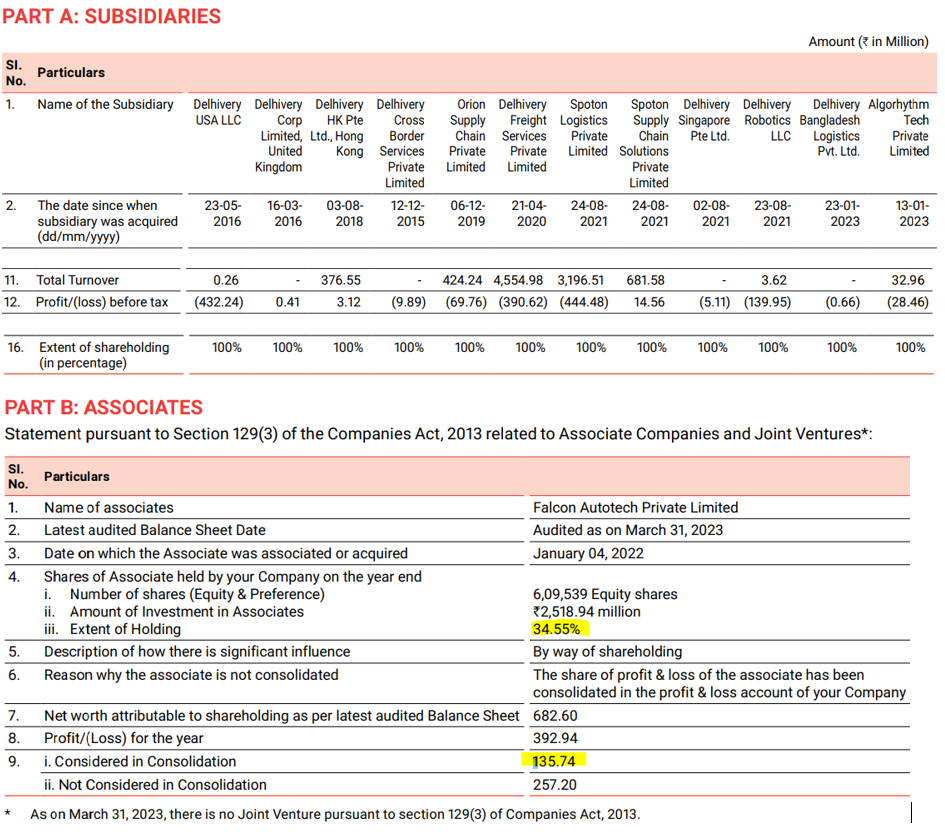

Algorhythm Tech:

A software company that offers comprehensive, end-to-end supply chain planning & execution solutions. The platform consists of a dozen products designed to deal with various problems in manufacturing, supply chain, and sales & distribution processes.

----------------------------------------------------------------------------|-----------------------------------------------------------

-------- Notes (rephrased per my understanding) from conference calls conducted till date --------------------------------------------------------------------------------------------------------------------------------------------------

Overall:

Provides logistics service using infrastructure and technology that enables buyers and sellers to transact [B2B (business to business), C2C (Customer to business), or B2C | at Domestic or International level] with each other

Business Segments – Logistics Services: Express Parcel, PTL/LTL (Part Truck Load), FTL (Full Truck Load), and SCM (Supply Chain Management).

Q1 volumes typically lower than Q2 (end of season sale and Prime Day, Flipkart Founder’s Day), Q3(Diwali, peak season) and Q4(Republic Day, year-end sales).

India’s addressable logistics market is $200 billion and fragmented. However, India is yet to produce a large integrated domestic logistics company. Expand capacity and be a large player using Delhivery’s technology platform and well capitalized balance sheet by plugging in partners for infrastructure – Land, Building Warehouse, and Trucks - across the country. Technology and data intelligence capabilities differentiate us from the competitors. As the logistics space becomes more organized and consolidates, Delhivery is the natural consolidator of the industry as evidenced by past track record of complimentary acquisitions to acquire either geographic or a customer capability synergy value.

Asset-light operations: Invest in critical service elements and IP-sensitive areas of the network, while delivering services through many network partners. Network partners with warehousing, freight (truckload or air) or first/last-mile capacity can sign up and find customers via applications. Our systems function as managed marketplaces that match partner capacity with Delhivery’s internal and third-party client demand based on partners’ service quality ratings and pricing. This approach enables us to quickly expand to geographically dispersed locations, optimize loads, improve our cost structure, and maintain flexibility in handling seasonal variations and changes in client requirements while incurring minimal fixed costs and capital expenditures. Platform orchestrates infrastructure and participants across our network.

Building automated trucking terminals, the technology systems, and acquiring complementary assets to scale the network. Provide mechanism for partners to exposes their truck capacity, orchestrate the demand efficiently into their trucks so that they can drive 18,000+ kilometers a month Note: operate over 12,000 trucks daily. Our own fleet is only about 562 trucks. The tractor trailers were bought to design so that parcel and freight can move together

Network is a unique mesh, which is fundamentally different from classical hub and spoke models run by other logistics companies across India and the world

Network is powered by over 80 technology applications, which have been built on a proprietary logistics operating system and platform, and vast amounts of data.

Seattle office to open out Delhivery’s technology to third party developers and other logistics companies.

The regulatory environment has improved in the last decade. Logistics has been accorded infrastructure status and there is continued improvement of road, air, and rail infrastructure. Government reforms like Make in India, and PLI schemes are ultimately driving non-discretionary demand for logistics services. Rapid adoption of digitization through GST, e-way bills, EPOD, and E-invoicing, is helping reduce overall inefficiency costs for logistics companies.

New axle load norms have improved utilization of trucks. And new initiatives by the government such as ONDC and the data privacy law will ultimately drive merchants to have more direct relationships with logistics partners.

Orchestrate the network using technology and data driven systems.

2 Key Performance Indicators: service quality and cost per shipment. If we deliver high-quality service and continue to improve efficiencies internally, market share is a direct consequence.

Cash Utilization: Massive growth opportunity ahead of us and we shall play the consolidators role. Acquire complimentary networks either from a geographic standpoint or with service specific verticals. Scale the revenue to $5~$10 billion. Hence, continue to make capacity investments to deliver growth and profitability going fwd.

On a normalized basis, our expectation is that loss and damage should be sub 1% of revenue.

In every year, margins begin to improve in Q2 till Q4 since Q3 and Q4 are seasonally high quarters. Wage increment and ~70% of Capex happen in Q1.

Higher unbilled receivables: Delhivery’s system was not fully automated, but it is now close to the final stage. So because of merger with spoton and ongoing automation, billing cycle got extended. In the next two quarters, expect to see a significant improvement.

Target ROCE of 30% for every business.

Expect to break-even in quarters of FY24 and generate net profits by early FY26.

Big macro risks weather and geopolitics.

Management:

Sahil Barua - MD & CEO [Age: 39 | BE(Mech) NIT Surathkal + PG from IIMB | Director since December 19, 2011]

Sandeep Barasia - CBO [ Age: 52 Yrs. | — | Director since July 1, 2015]

Kapil Bharati-CTO [Age: 46 Yrs.| BE(Mech) IITD | Director since August 19, 2021]

Amit Agarwal, CFO

Strategy:

Our focus is mid-mile optimization since it is complex to move a large quantity of products across India with speed and reliability in a cost-effective manner. To improve mid-mile efficiency, we have integrated the express and parcel segment by increasing use of 46-foot Volvo tractor trailers, which are 15 ~ 30% more efficient, expanded the automated sortation capacity, and invested in new automation, including autonomously guided vehicles, automated storage and retrieval systems and system direction. At PTL revenue of 4K+ crore, network would provide a near express service at the cost of time-indefinite service and that will be a big inflection point. First and last mile is least differentiated and has flexible capacity.

Integrated mid-mile’s utilization will not be completely sensitive to express volumes if PTL volumes grow. In that sense, the express unit economics are impervious to changes in express volumes.

Logistics is cost input to highly cost-sensitive customers. Our approach is to build high-quality, large-scale, & integrated mid-mile operation. Engineer it to be highly productive, reliable, and low-cost. Pass benefits to customers to gain volume and avoid competition.

Express market:

Highly competitive | Expected Mkt. Growth Rate: 15~20% | Will at least grow at the mkt. rate | Composed of individual parcels that weigh <40 kg and Turnaround time (TAT) of <3 days.

Beside price, other differentiators are reach of the network, and speed with quality of delivery.

High incremental gross margin which acts as a tool to fight competition.

The new D2C brand owners such as Reliance, Unilever, Dabur are not affected by funding winter.

Aviation is not a preferred mode of transport for packages that cost ~500 rupees.

Pass on efficiency gains to customers. Makes new categories viable and grows wallet share.

Top five customers less than 40% of revenue. No customer forms > 14% of revenue.

Increase in PTL volumes will expand mid-mile utilizations. Hence, improving the unit economics.

Self-serve portal (Delhivery One) allows small brands to access our services seamlessly, and franchise network plus C2C app allows the extreme long tail to start shipping immediately.

eCom very small fraction of total consumption. e-Com opportunity supported by increase in online purchase frequency, tier 3/ 4 cities penetration, and new categories.

ONDC platform: Seek to grow volumes in FY24.

In-house logistics arm cannot build flexible capacities like third party logistics partners.

Lowest cost Operator in logistics space - bundled or unbundled at each individual leg.

Target gross and EBITDA margins for every account.

Capex:

Do not incur any capital expenditure towards ownership of real estate. Our capital expenditure is focused towards investing in fit-out infrastructure, state-of-the-art (a major share of it is in our integrated mid-mile) automation, IT assets and tractor-trailers (to do design fit outs). Automation includes parcel sorter systems, bag sortation systems, conveyance systems and future-ready technologies such as automatic guided vehicles, automatic storage and retrieval systems and unmanned aerial vehicles.

Over time we expect capex to stabilize at between about 3 and 3.5% of revenue, which will include both new and maintenance capex for sortation centers and gateways.

Most capacities built in 1st half of FY. So, 2nd half is a higher depreciation period.

Expect 2 mega-gateway to go live: Bhiwandi by November 2023 and Bangalore by March 2024.

Expand hub when see sustained ~ 100% utilization of the hub’s theoretical capacity.

Margin Improvement Levers:

50% incremental gross margins on transport business.

Normalized gross margins in transportation business is 26~30% at 80% capacity utilization.

Incremental service EBITDA margins in 18~22% range.

Engineering continues to discover new ways of improving productivity in the mid-mile.

Increase fleet sourcing from Orion platform.

Cull or renegotiate with low margin customers.

Introduce 46-foot trailer in more hubs, conjoined trailers, and EVs in mid-mile operations.

Prevent revenue leakage, fill trucks to axle payload using algorithms, and consolidate facilities.

PTL | Total shipment weight of 40-1,000 kg:

Opportunity size $8 to $10 billion, which grows at 10 ~12%. Highly fragmented and unorganized market. The top 10 organized players form less than 20% of the market. Delhivery revenue 2.5%. Aim to gain share. So, growth with margin improvement is the focus instead of yield protection.

Pricing well established in the market and will be determined by the competitor’s action

Pickup & delivery costs - 15% to 20%; line haul [trucking] costs - 35% to 40%, load handling costs [manpower] - 5% to 7%. Opportunity to do Gross margin: 25~30% and EBITDA margins 14~20%.

Yield comparison across competitors misleads. Change in customer mix, and lane distance affects the yield. Our focus is gross margin and EBITDA.

Entering the economy (time insensitive) space to drive up utilization of mid-mile.

Post GST, PTL preferred over FTL. In PTL, shift towards organized players and express PTL as it brings down inventory across the supply chain.

SCM (Supply Chain Management):

Includes Warehousing space (fulfillment centers to store and transport inventory) and software solutions to optimize inventory placement, and fill rates, and transport selection.

Early days and hence growth trends look a bit volatile.

Misc. Products:

Platform (OS1) with base components to build customized logistics applications: It is aimed at small scale operators to build first-party dispatch application. Targeting both the Middle East and the US as potential customers. In conversation with 10 potential customers. It’ll be monetized similar to a standard SaaS product. Start seeing monetization slightly more significantly in the FY25. For e.g., Dispatch One, which allows last mile operators to use our dispatch service.

IP of transition robotics: one of our models should now be commercially ready by Q3FY24.

Orion platform: It is platform that acts as a freight exchange to discover the price of truckloads and book truckload freight across the country. Began by exposing spot (10~14%) requirements of trucking or fixed (86%) contracts. Now, expanded to intracity movements.

Algorhythm’s product enable supply chain planning activities such as optimize inventory placement and transport selection and complements our warehouse management system.

Vinculum provides order management solutions (OMS) and warehouse management solutions (WMS) to companies in consumer internet space, cutting across multiple categories. Enhances value proposition for D2C brands as it is a direct integration of the OMS with our own WMS.

Primaseller expands our direct-to-consumer (D2C) value proposition.

Road piper allowed us to effectively communicate with fleet owners across the country.

Unified Client Portal and merchant panel allow customers to self-serve.

Launched Delhivery Direct mobile application allows consumers to self-serve.

Delhivery Academy provides training and skill development from grassroot to supervisory levels.

Note:

Adjusted EBITDA margins improved from -11.3% in FY19 to 1% in FY22 when we brought down the yield per express parcel from Rs. 92 to Rs. 72 while fuel costs inflated from Rs. 66 to Rs. 93 per liter.

Technology is not a moat as two legacy players i track also invest aggressively. It is a complex fragmented industry and very difficult to consolidate. I think profit, cash flow are more important here.

Thanks for summarising this.

I’m particularly quite excited about the platform OS1 which can be the real game changer. This will make Delhivery a logistics Saas company whose growth as well as profit potential will be much higher. They have been working on this for last 3+ years and seems like the full stack launch is still 3-4 quarters away.

If they are able to execute it well, this can be like what AWS is for Amazon.

Currently, it’s mentioned in the corners of the annual report. Hoping to see this occupy the main spaces in their reports in another year or so.

I am working in the ecommerce logistics space, and know that address accuracy is a big problem. I have tried various services to get the coordinates of an address as inputted by a customer, and many a time, it is not accurate. Even Google API is not accurate. We have scenarios when a local area can be spelled in different ways by different customers eg. Bazaar can be bazar, bajar etc. This causes a lot of issues when we run Google API to fetch the coordinates of a certain address. I have been trying various solves for years now, and am yet to find anything 100% accurate. So a solution which gives a breakthrough in this will certainly be game changing.

GPS tracking and telematics of vehicles is a pretty standard solution available in the industry. There are dozens of softwares available, and the quality of product is pretty standard. Location intelligence is the area where no solution is 100% correct in India. I have used Google API, MapMyIndia etc. And none produce accurate results 100% of the time.