Good coverage on basics of industry, DN as a case study 45:00 onwards

One interesting call out in Q &A by Mr Anish is that DN is very good at getting ADD implemented in every area/product they enter and gives example as well - on lighter note, don’t know if this qualifies for exceptional capabilities or exceptional connects

Yes for that matter BASF, BAYER, DOW Chemicals are all chemical businesses. As a investor we should see business trajectories and management intent to give fair treatment to minority shareholders. If we base analysis ONLY as per the past events we won’t be able to make fair judgement about future, Afterall investing is unfolding movie and not a static picture. That said past can’t be ignored completely for serious management lapses , frauds etc. Also having very clean past record doesn’t guarantee on future returns. Stock market investing is all about taking calculated RISKs, allocation and diversification

A question on Deepak Nitrite and other Specialty Chemicals cos

How does higher crude prices impact these cos specifically DN as most of its RMs are crude linled? Do they actually benefit as higher prices mean higher absolute profits when they eventually pass on RM costs

Downside could be higher freight/power costs - In a concall DN mentioned its more a Phenol transport company which also incidentally manufacturers Phenol

Higher crude oil prices will impact margins directly.

How much it impacts, depends on the company’s pricing power to pass the inflation costs down. Very few chemical companies can pass it directly, most will pass with delays. Even fewer can absorb those costs and not have it affect their margins by increasing operational efficiency in their cycle.

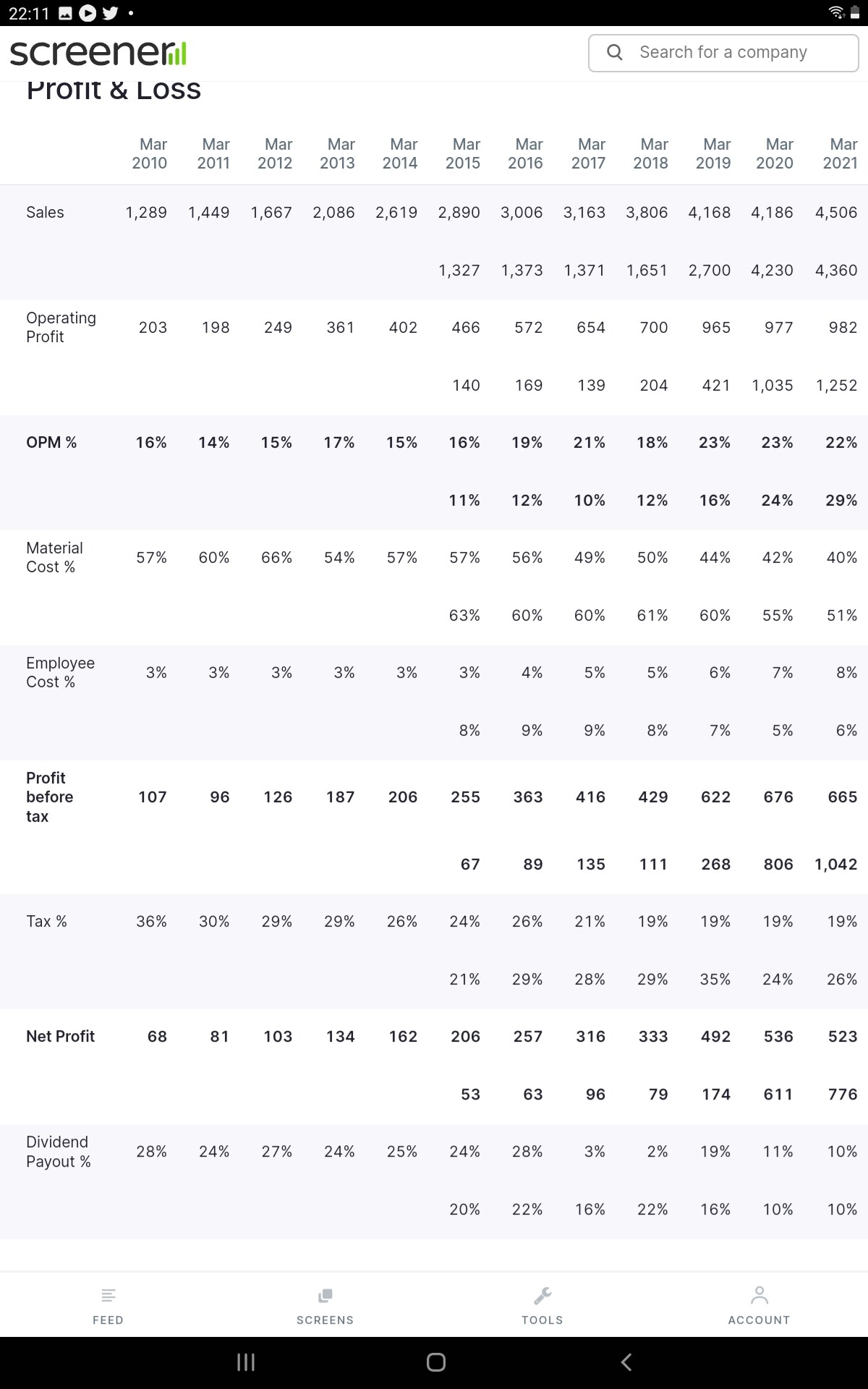

Phenol spreads were expected to cool down. Performance products saved the bottom line. Wonder what happened there. For some reason, fine and specialty chemicals has degrown again this quarter. Looking fwd to the call.

Prime reason as stated for degrowth in F&S is the rise in prices of Basic intermediates division, which serve as RM for F&S. As transfer pricing takes place,

F&S Margins have fallen to 25% (ebitda). Which is disappointing but on the other over the coming quarters they expect to pass on the RM Cost inflation in F&S division.

Not a linear story, more or less will be a lumpy compounder. As real triggers will come from F24 & FY25. As large capex’s start getting commercialized.

These results also show the true nature of the business. A diversified and integrated chemical company, diversification saving it from a disastrous performance. As PP segment picked up. Next quarter to be likely good if current pricing trends persist, as Phenol spreads are back to 120 Rs per KG and Dasda prices have further increased by 14% MoM.

Things yet to play out:-

1100 crore capex announced.

2000 crore QIP probably for additional capex.

Will we see a different DNL by FY25-FY26? Only time will tell.

Amidst this backdrop, the Company has effectively and efficiently executed its operating schedule and fulfilled its supply commitments to ensure reliable and stable supplies to customers.

Import Substitution* : This is very important to retain / gain local customers

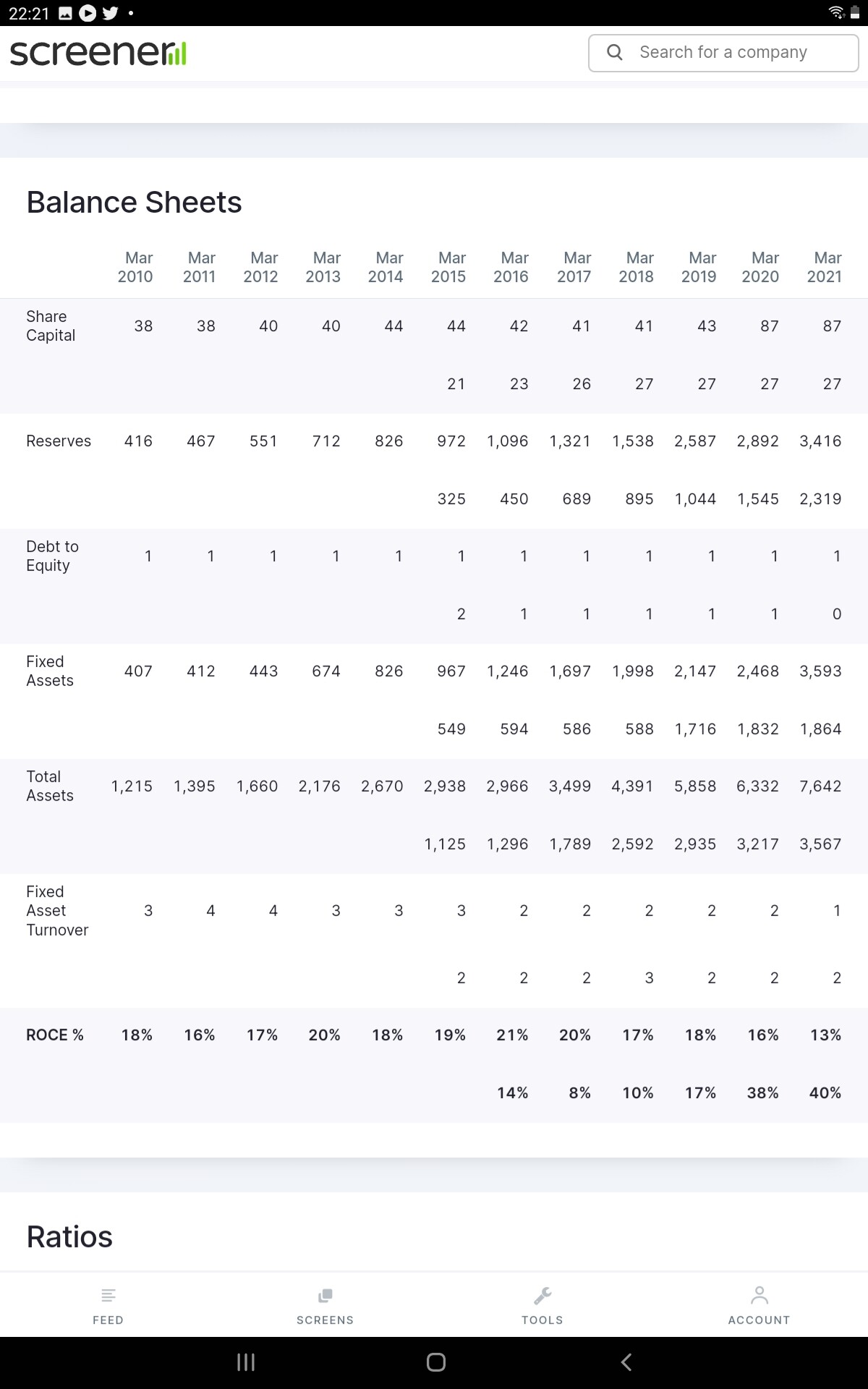

Finance costs were low on account of sizeable prepayments of term loan made during the period || The Company has prepaid Rs. 100 crore of project loan during the quarter without any prepayment penalty

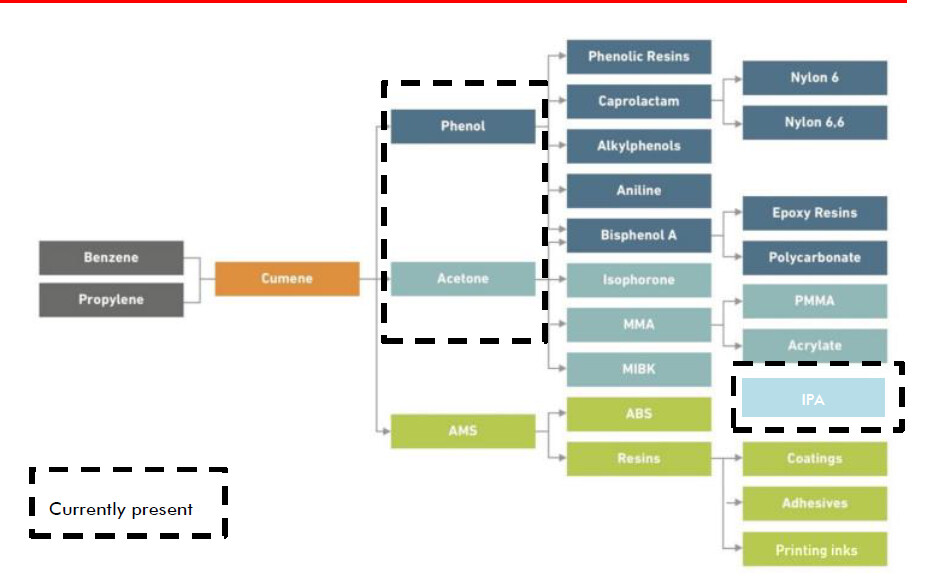

Brownfield expansion of IPA was commissioned on 19th December 2021. This has doubled the IPA capacity to 60,000 MTPA ( This will definitely help topline in Q4FY22)

IPA is the first of a basket of downstream derivatives of phenol and acetone that will drive forward integration in the product portfolio of DPL. This will result in increased captive consumption of these commodity products and enable us to deliver value added products to our customers.

There is one key observation between Deepak and DMCC (later are also completed the 350 TPD sulphuric acid plant so that they can focus more on downstream high margin products ), focusing more on backward integration to produce the basic raw material for captive consumption

If we observe Q2FY22 commentary most of the pharma companies complained about prices of solvents , in some solvents they have gone up by more than 100%

EcoVadis, world’s largest and most trusted provider of business sustainability ratings, has bestowed Silver rating on Deepak Nitrite with sustainability ranking of 83 percentile ranking. This has increased from a 39th percentile score earlier, reaffirming the group’s progress towards greater sustainability

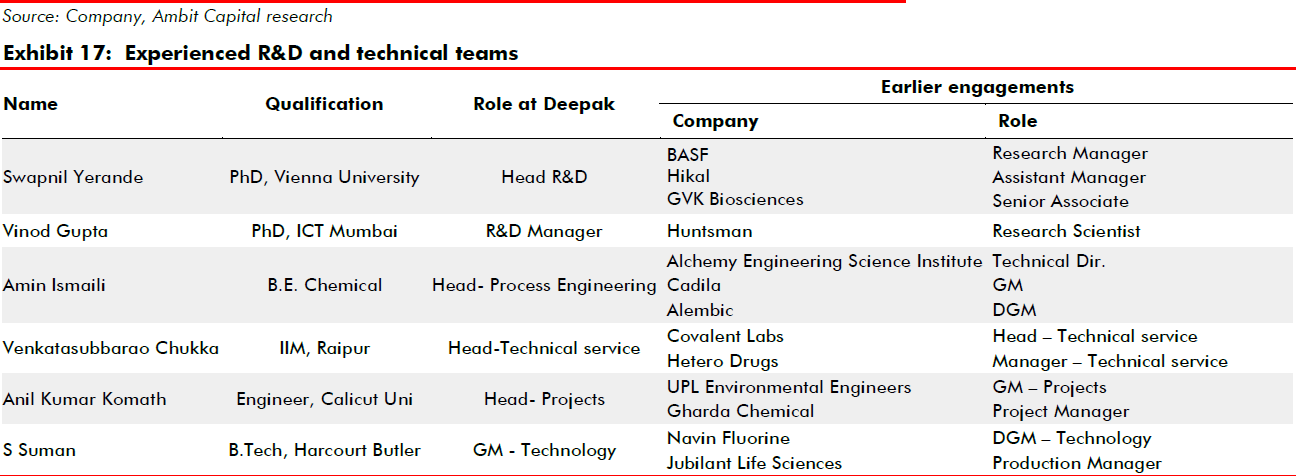

Very very important in chemical companies. One has to have this as one important parameter in their investment thesis . (Lessons have to be learned from Hikal and Gujrat Flourochem , former is sheer negligence )

Management

Young lad Mr. Mehta 37 years old at the helm supported top notch R&D team

As a process, our business segments are interwoven. This means that if prices of BI increases, you may see a simultaneous dip in FSC segment, as internal product transfers take place at market prices. And accordingly, higher margin in one segment may result in lower margin for other. This year has been very strong for BI segment. In FSC segment, as most are long term contracts, there is some lag in

passing the input costs

If they are backward integrated and price rise in Basic Intermediates (they are producing them in house ?) this should help them to maintain good margin in downstream products ? Could someone please explain ?

Believe answer lies in your notes itself, the highlighted part.

In prevailing global supply chain disruptions - Interdependence of one segment with another will ensure that not all three can fire at once, and one benefits at cost of other’s margins, atleast the pattern so far.

Backward integration in normal supply chain scenarios will work with better rhythm.i.e. BI stays at lower margin range it is supposed to be thus lower input prices, RM cost in control ensures end products at better margins which they should deliver.

Given lag( or ability ) in passing the RM inflation ( BI ) price increase to end FSC

causes downstream product margins pressure.

With so many similarities- market values A at 50+ PE and B at 25+ PE

A is Aarti industries and B is Deepak nitrite

Both are aggressive in Capex, dominance in their chemistry, smart mgmt.

Point of post is that beyond numbers, there is lot that market may be seeing - margin volatility( though at annual consol both seems similar - FY 22 is excluded), promoter perception, capital allocation history, commodity vs spec chem perception ( though Deepak guides 20%+ margins for commodity phenolics).

Lot can happen for Deepak in journey ahead, some re-rating, sizable growth, higher margin downstream products incl solvents, New chemistry platforms and so on. Not a QoQ journey, years to go.

Invested in both and excited about possibilities for DN and chemical industry as whole

Heard the concall. Love the way management (Maulik Mehta) answers questions with absolute clarity.Headline commentary

This quarter was impacted due to unavailability of raw material esp for the F&SC segment. Higher freight and power/steam costs which was difficult to pass on

All cost increased in RM materials are passed on - sometimes with a lag

Sustainable EBIT margins in Phenol to be 20-23% and in FSC to be 35-37%.

Volume demand across segments are strong. Have maintained/ increased market share across products/segments

New Phenol capacities to come up in CY2022/CY2023 in China, management explained most will be used for domestic consumption or downstream derivatives. Dont see it as a big cause of concern.

Some margin fluctuation QoQ is always witnessed but key thing is demand is strong.

Power costs may moderate (power plant has been commissioned), freight costs may remain high

PP may see a great qtr continuing in to next qtr

Phenol Downstream projects will be commissioned in Q3/Q4 FY23

F&SC will see better margins as they keep passing on costs and volumes keep improving.

Lot of talk on how Deepak is integrated and how there will always be some segment will be lumpy and some may see few headwinds.

Captive Phenol usage to increase with upcoming capex and will lead to better margins.

No word on Capex/progress on QIP. Strange there were not a lot of questions on capex and ZERO questions on QIP…My view - Management’s focus in on maintaining wallet share/volumes and executing on capex. They explained their strategy quite well - Happy to get back on this stock, had booked out at 2650

Corporate Chat / Twitter Important statement on inorganic growth and valuations. What seems as high valuation / overvalued today 50/100/150 PE can be looked at with a different thought process. One must look at what the buying company WILL DO with the acquisition, the big view/ ambition they have with it. With an acquisition whose earnings can be leveraged right away and the asset can be doubled in six months, can be looked at.

My previously asked question might be relevant in current crude oil pricing scenarios.

Margins will be impacted in short term and medium term(in case they are not able to pass on prices completely). Whoever they source benzene from (most probably Aarti ? as per views I received), will pass on the prices to DN and then they will have to pass on too causing some short term impact depending upon they take 1-3 quarters.

Vinati maybe heavily impacted though and their margins may decline for medium term at least.

Crude Oil prices impact is not felt in India due to elections,so the company pays what other retailers are paying isn’t it, I know they might not consume petrol and diesel more of Crude “Crude Oil” but want to get some light on this, sorry i might be sounding like a noob here.