I think we have to understand this from crude derivatives perspective not the oil (petrol / diesel ) that we use. We add too many taxes on the later which is the saviour during covid lockdown.

Petrol / Diesel prices are already at the elevated levels for many months, they may not go up that fast , if at all they go up then the direct impact is on the freight costs .

The problem for chemicals companies (especially bulk chemical producers ) , feedstock that is dependent on crude and then logistics cost (import / export) . It is not easy to pass on such costs immediately. Very tough times ahead.

Yes Rafi u r right, but during one of the interviews Deepak did mention that they will not be able to bear the high RM or freight costs over a prolonged period and they have to eventually pass it on, last qrtr and the one beofre that the company obsorbed the cost as they didn’t want to keep bothering their clients abt small changes in RM as they belive in building and maintaining relationship over long term and not fuss abt small margins

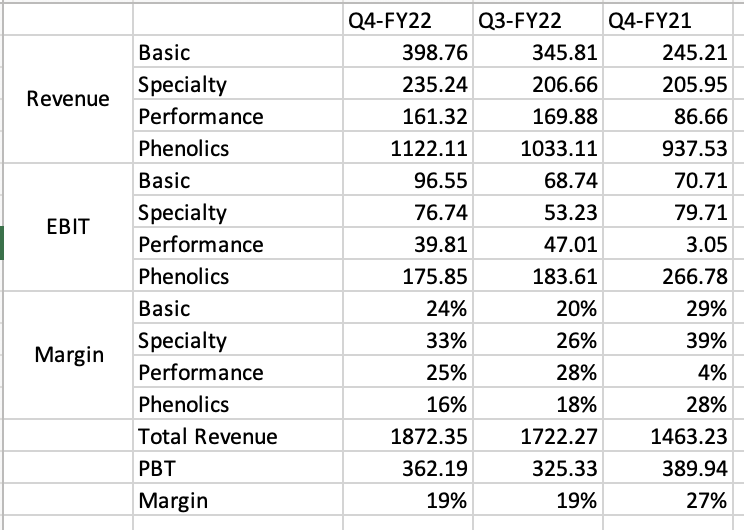

Along with crude oil prices, utilities cost will impact Deepak as well. Maulik Mehta mentioned that even though phenol spreads were going up but since lot of energy is used in phenol part of the business, its rising cost impacted phenol division margins. And after this Russia issue energy costs are sky high

Overall strong results in an inflationary environment. Phenolics is expected to face margin pressure until they go into downstream products with the new capex. Basic and F&S segments have shown improved margin so it looks like they have been able to pass on the higher costs to an extent. Mgmt commentary would tell us if the results should be viewed as strong defensive in inflationary scenario or average margins down from peak of FY21.

1. We’re missing the forest for the trees when we fail to look beyond the margins for the quarter.

Context of RM cost increases. Ammonia has historically been Rs. 26/unit. 6 months ago, procurement team were dismayed that Ammonia costs jumped to Rs. 32/unit. In Q4, Ammonia costs were in excess of Rs. 100.

In this environment, customers continued to buy the same volume of Deepak products, paying nearly 2x for the same quantity of products a quarter ago. This is success to them: maintaining and growing wallet share per client despite a tough environment.

RM prices will be difficult to predict going forward, irresponsible of them to give guidance. What they focus on is client relationships. They sit down with clients and talk openly about RM costs, and this transparency has helped them pass on costs.

2. Management is incredibly detail oriented at every step of the value chain

On capex, keeping track of monsoon data to finish long lead time procurements early.

Needed to buy Nickel, but prices ran up to $50,000 per ton one day. By waiting a few days, they were able to get it for half the price.

Track cement/steel closely, and only make purchases when prices are favourable to them. Rented a port facility to store, allowing materials to be bought on their terms.

Talking to shipping lines for annualised contracts with minimum container offtake.

Continually audit all plants for energy saving, water usage, leakages, etc. Will help the environment and help with cost efficiencies. (PS: I think it’s important for chemical companies to discuss these initiatives in a time where compliance won’t make headlines.)

Opened a captive power plant that allows them to plan plant schedules better, and time shutdowns on their own terms.

3. On how price reviews happen in contracts

Clients look at contracts based on calendar year. These have quarterly price reviews. Last one was in March, next review will be in June.

Focusing on new multi-year contracts that have price increases built in as a clause: ex: if RM costs go up by 5-10%, automatically triggers a review.

Easier to pass on costs for molecules where they already have clients and a foothold. New products will be tougher.

4. General business notes:

High energy costs in EU are hurting clients. Energy costs never took up bandwith, but are now among top 3 costs for clients. Due to this, are not consuming as much. Performance products division will suffer until this abates.

Balance sheet is clean, still proceeding with a QIP because one wants to be in a position of strength, and not look to the market when one needs cash. (anti-fragile) Evaluating multiple whitespaces to target.

All new ventures have an internal Lakshman Rekha: they ask what Deepak’s right to win is, what are the expected asset turns, IRR, etc. They also ask what the probability is of selling products to customers. Easiest when it’s in house consumption.

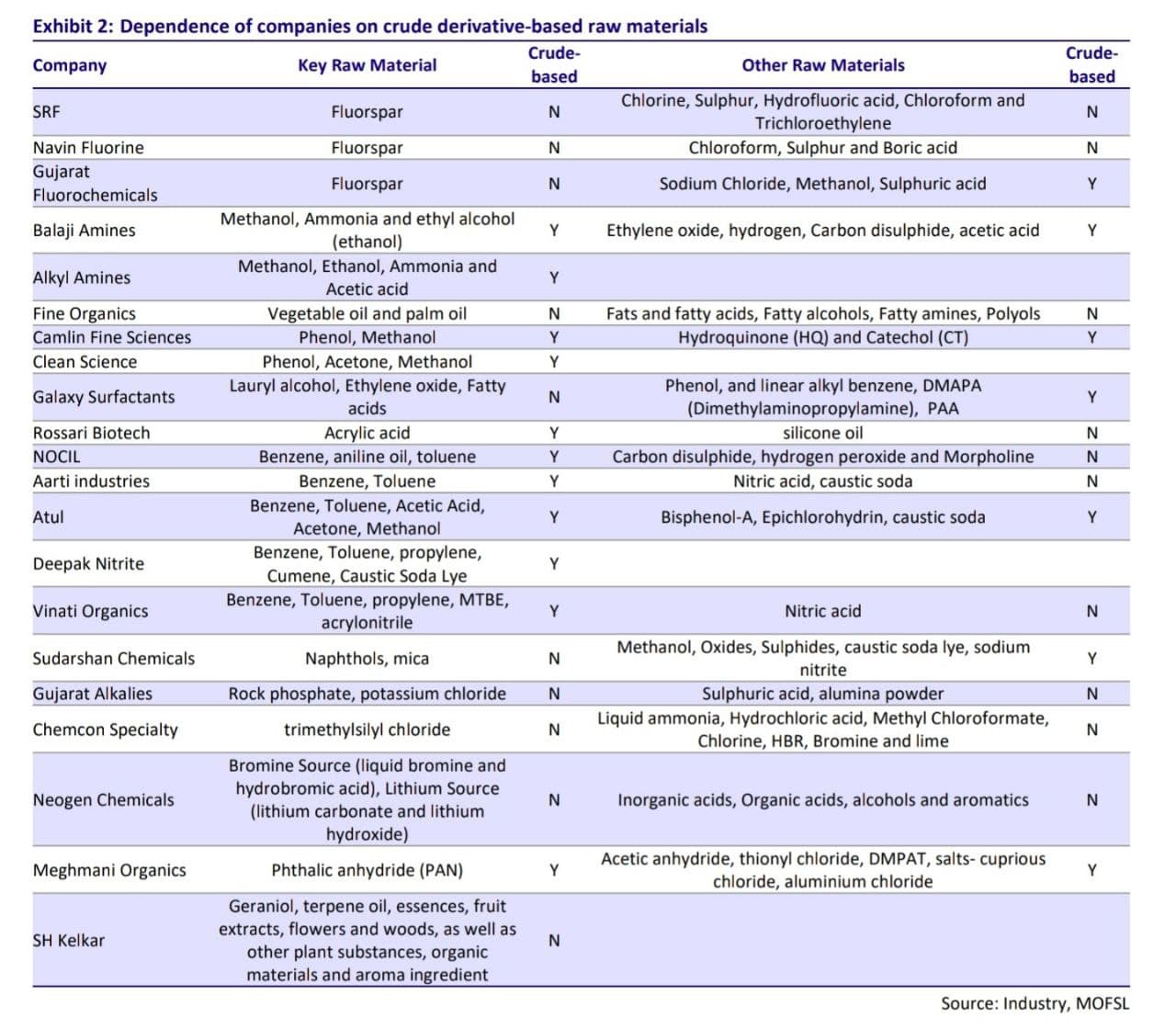

On flurochemicals - someone asked how they can compete with Navin. Management believes they can compare well. First, they’ll target molecules where they have competence in products beyond fluorine. Other answers were about how they have the right people and sources of chemicals.

Edit: I went back and listened to the recording. Question was asked in the dying moments of the concall and management gave a rushed answer. Would like to see this fleshed out in more detail. Writing to the management, will update here if I get a response.

Q1FY23 will see the first phase of new capex come onstream. Greenfield capex will be done in 18-24 months. This is a part of the 1500 Cr. capex, and will be downstream for core biz and Deepak Phenolics.

Opening remarks were a rehash of points from the investor presentation.

D: invested, biased.

I may have missed/misheard key details. Please check all figures with transcripts. Inviting others on the call to also post their views.

I think the results were good considering the macro economic situation that we have. If there are price, margin pressures then it is not company specific issue and is prevalent across industries, across countries.

The share price is down -10% now. Am I missing something? Any product related issue? Future prospects?

I am invested and want to buy the dip but wanted to make sure I am not missing the whole picture. Thanks!

Q4 concall notes - with good coverage on notes above , calling out directional trends inferences

Disconnect between mgmt way of looking at performance ( absolute nos growing, supply chain efficiency, client relationships, already high ROCE and demand visibility barring EU exports) and Analyst questions ( margins trending down and Capex clarity to gauge future potential)

Good parts

Deepak revenue has 80:20 ratio in domestic vs exports, domestic demand visibility strong but part of exports ( spec chem where end customers have B2C products) demand forecast is a challenge for near term

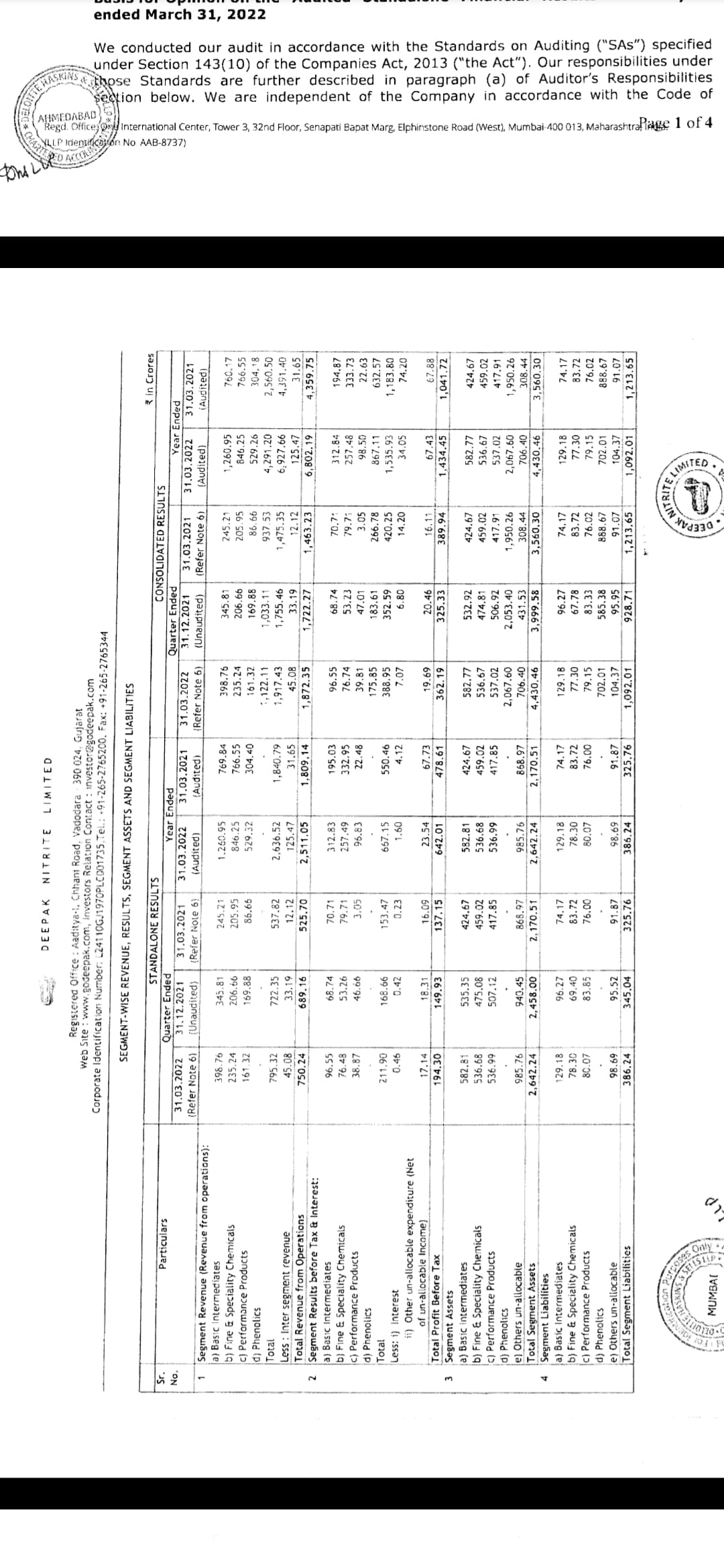

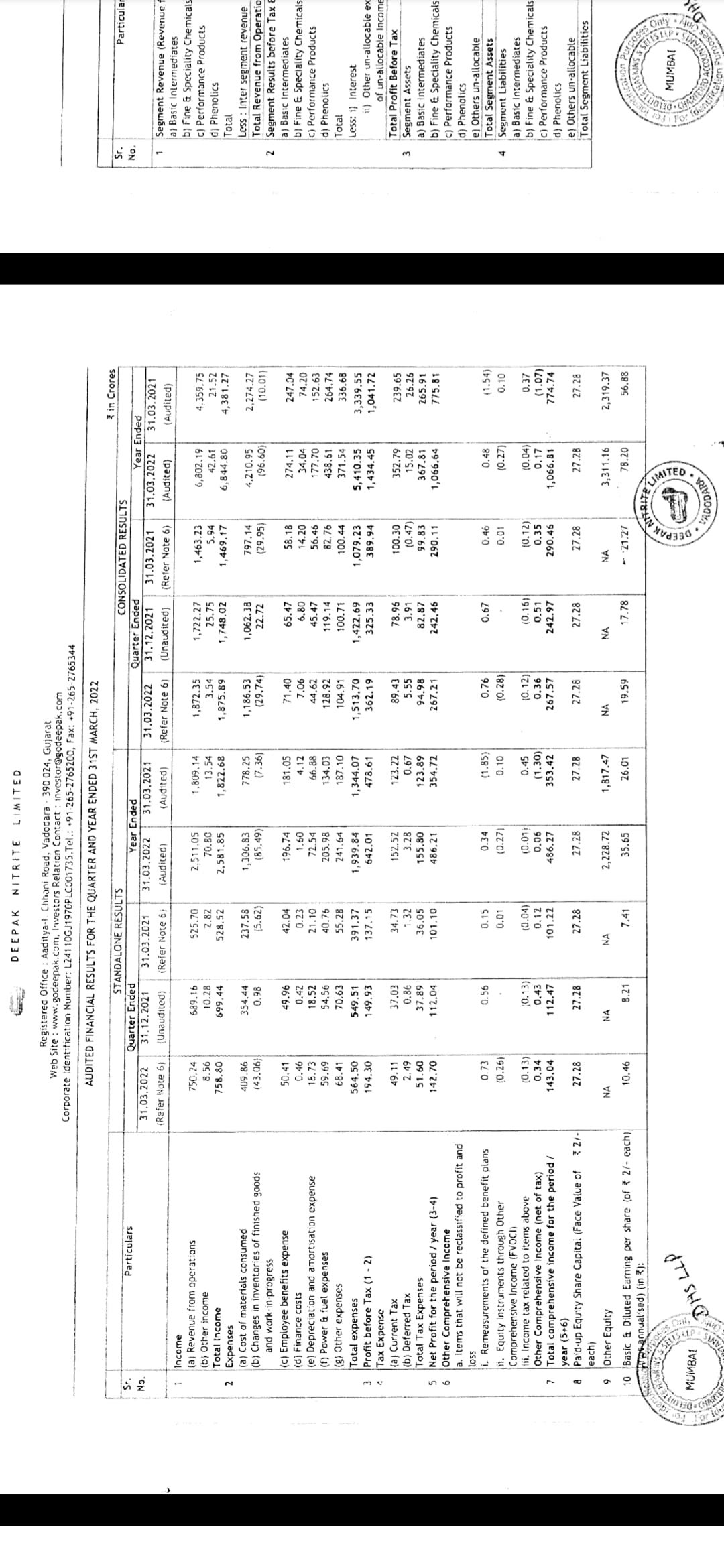

Already a healthy RoCE biz and can’t expect more, high utilization in Phenol( 118%)

About 1500 Capex WIP with multiple go lives - near term Q1 ( Agro intermediate), med term Q3( Spec chem), 1.5 yr+( Upsteram ) - expect 1.75 to 2 Asset turns and 20%+ RoCE

QIP for future capex - intent strong - will need conducive timings - Organic + in organic- not much details but visible aggression supported by healthy balance sheet

Absolute nos growth in all biz verticals and mgmt feels good about it

GM down to 30% in last 3 qtrs, still holding EBDITA 20%+ , if this is not efficiency, don’t know what is. GM in normal times are 40%+, one can imagine what happens when they start to inch up.

Capabilities driven Flurochem entry - mgmt disagree that supplier concentration can be a challenge,

Not so good/unclear bits

Consol and Phenol margins on downward trajectory for last 3 qtrs - market cuts it both ways and likely pessimism over ability to grow Margins unless numbers come - opportunity cost for sizable investors community

Mix dynamics - Though standalone margins improved from Q3 to Q4, Phenol division margins still on downward direction. Unlikely that both segments will do better at same time given interdependence, thus some uncertainty on steady margins. Phenol margins need to stabilize though given volatility mgmt can’t guide.

Valuations and margins

Here is PE ratio over 3+ years

As we could see Dec 19 to Mar 21 was a period for Margins growth trajectory, so was PE ratio, from there on margins have come off a bit and so has valuations multiple, but still higher than median.

What is given is Deepak ability to deliver on absolute nos, directional trend on upsteram products and cost optimization should lead to some margins stability, as product mix improves over next 18 months with 1500 cr Capex coming live.

Deepak credentials and aggression is well known, Deepak current mkt cap is 27000 cr, question we investors need to ask is , can it go past 50000 cr mkt cap in 3 years( for 24% CAGR returns) - which in turn will need

At 22 median PE - about 2200 cr+ profits- a tall ask from current 1000 cr+ profits but Deepak has done it in last 2 years with Phenol Capex, however base is already big

At 30 PE - about 1700 cr profits- to get these valuations- margins need to improve to higher range and less volatility, ofcourse Capex as well

DNL has a great proven management. They did really well when the tailwinds were there.

Inflation has been a pain for everybody, Central banks stepping up and moving ahead of the curve is a good sign for longer term. That basically means that inflation will come under control for sure.

In the concall, Mr. Maulik Mehta was asked about key learnings from this FY. He aptly mentioned about the ignorance by most of the chemical companies, including DNL towards freight, packaging, logistics, transportation costs. Now, when these costs have become a major cost centre, the company has taken steps to minimise its impact on the bottomline. Further, the management also accepted its mistake of relying too much only on a single supplier and it has costed a lot in the past. All these factors led DNL entering into alternative arrangements with suppliers, shipping companies, because there were instances of sudden rise in freight costs, cancellation of ships, etc.

Yes. I think , he even said that, now RM procuring is not only inside, some part they are importing too…Thus dividing RM procurement equally between domestic and import.

Here’s a simple article about the various uses of Phenol in Pharma.

Downstream products of Phenol and Acetone will cater to a significant demand from Pharma industry. DNL has already introduced capes of Rs. 700 crore for solvents in the derivatives space of Phenol and Acetone.

Another thing to note here is that the management of DNL frequently explains about how it’s chemistries are interwoven in each other - meaning - some products from BI or FSC segment will find their application in Phenolics or vice versa. In this case too, Phenol’s derivatives might be used in FSC segment particularly since many derivatives of Phenol are used in paints, coatings, adhesives, etc. (Bisphenol-A and Epoxy Resins in particular)