It gets added there cos the accounting standard for revenue recognition is very grey. “transfer of control”, “transfer of risks”. Auditors tend to play safe. I’m a big4 chap whos been in audit and taxes so can say with some degree of certainty here

The internal cash accruals of the Company seems to be very strong and is sufficient for them to take care of future CAPEX need. Any shortfall can be easily met out by debt as there debt matrix is very comfortable. i do not see any reason why the Company needs to dilute the equity…

May be Company would like to encash the euphoric share prices…

Disclosure : Not invested as I find the valuations to be high and my views are biased

Good for existing shareholders that company is diluting share at a higher price resulting in less dilution for same amount of capital raised.

I think management knows very well when to do the capex as this is not the first time DNL is raising capital through QIP before a massive capex.

Lets see how this goes…

Also on valuation… The one who see the company as a commodity producer Then it may appear like expensive and for people who see deepak as a speciality chemicals company with value added products then for them it’s fairly valued.

Hey Investors,

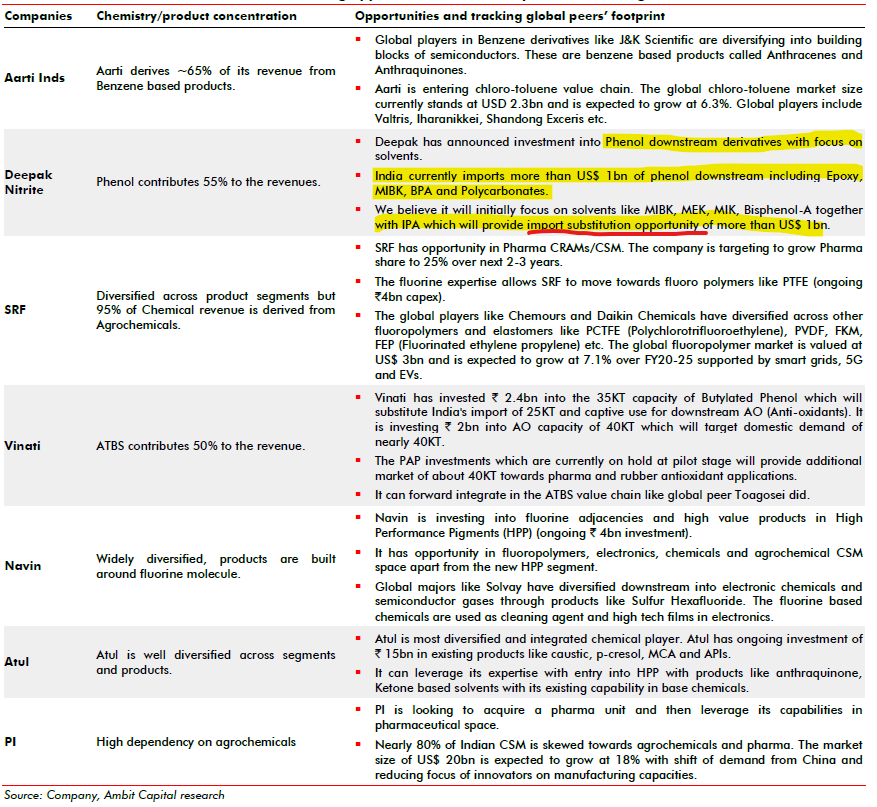

Can somebody let me know from where is Deepak sourcing Cumene, Benzene and Propylene from ?

Are they importing 100% of these materials or is it domestically sourced. Just curious as I don’t expect too much margins in these chemicals but the scale is huge.

Pretty damn sure Benzene and Proplene would be domestically sourced. Latter is a petrochem products and PSU oil refiners / Reliance make it. I doubt DN would be importing these but I may be wrong.

Lot of sourcing possibilities from India (PSUs & RIL ) as well as from the Middle East (Petrochemical companies from UAE, Saudi etc )

cumene can also be taken from petro companies …and locally it is RIL as also mentioned by you.

They manufacture their own cumene, benzene and propylene are locally sourced from all the well-known domestic petchem companies…

Is there any speciality chemical product added by the Company or is there any capacity addition in existing speciality chemical segment of the during last 3 years …

Check this link for new Launches.

This article is a must for everyone invested to read through, esp anti thesis and risk aspects, not a gold standards governance either( not that there are many in Chemicals space ), some risks are inherent to industry some are company specific

Here are some low lights as called out in Mr Malik in his analysis , felt positives are well known and acknowledged in article as well hence not highlighting

Low lights

- History of equity and debt funded growth - multiple rounds of QIPs and Debt usage - at 10 yr cumulative CFO and PAT diff is negative, dividends are also funded by debt( not necessarily a negative IMO but helps understand Promoter way of growth)

- All Capex till date had cost and schedule overruns - a pattern

- Current state of margins are more tilted towards favorable mkt conditions for various reasons, unlikely to sustain( key monitorable)

- 6+ years to get profitability in OBA+ DASDA plant ( after building world’s largest plant) - Contrast to much acclaimed 110% utilization and high profitability in phenolics right after being commissioned ( again supply deficit helped them Here- but still mgmt deserves the credit)

- RPT, Capex write off midway, plant closure in Hyd for pollution and criminal case( promoters removed as party recently) and company sponsored residential property at high rents benefittinb Promoter also called out - small but noticeable for Minority shareholders

Point of above is to keep in mind what has happened in past, we don’t necessarily go that far back in past and focus more on current narratives. As per our risk mgmt criterion add some of above in key monitorable as well.

To be fair- positives IMO - There is no doubt that it’s driven by ambitious and smart management, past issues is not necessarily a future repetition guarantee, transparency and communication is top notch, solid case for Import substitution play, future capex in right direction and right times( solvent etc), China+1 key winner and deserves credit for aggression

Invested

These issues were known pre 2018 also - despite that business has grown tremendously, At the end of the day stock price is slave to earnings, you can’t punish the stock just because they have not been that great in the past or have had some operational/ financial challenges.

I find it interesting that Dr Malik stresses the importance of analysing consolidated returns of a company (in this case from 2014 onwards) and then uses a chart of crude oil prices from about 2006 to stress the fluctuations in crude oil price.

If I look at the crude oil price chart he has used, and use the date range from 2015 to 2022, I find that the price fluctuation has been within a much narrower range of 40 to 80 dollars barring one blip in 2020 to 20 dollars.

Just wondering whether this is a fair way to stress a point or not.

Invested in Deepak Nitrite

Point of post is for new investors ( like me) to be cognizant of facts and risks that are attached to management past patterns, some may have not dug deeper / longer time horizon given bull mkt narratives. Exit decisions in unforseen risks triggering need these facts handy.

Business can do well for many reasons, some by mgmt capabilities and some by sheer luck or combination. We should be able to segregate both.

Chemical biz has inherent risks( for that matter every biz), How would one describe what’s happening to Hikal? Numbers are great for them as well. Mgmt pedigree was top class , narrative was great till few days back.

Invested in DN