Holding All 3

1 Like

Dhruv, heard it in one of Samit Vartak’s interview, if I remember correctly. Recorded it in notes, missed noting the date.

2 Likes

LIC increased his stake in Deepak Nitrite to 1.68% in previous quarter it was 1.32% and Axis mutual fund is started fresh buying in company

3 Likes

2 Likes

From my reading the countries which make a difference to Deepak Nitrite re imports of sodium nitrite, are Russia and China. The ADD has not been revoked for those countries.

Invested.

1 Like

Yes you are right…Manufacturers costing in Europe is atleast 20% higher than India. Only South Korea has competitive pricing but that too right now is mostly being diverted to China as per industry sources.

1 Like

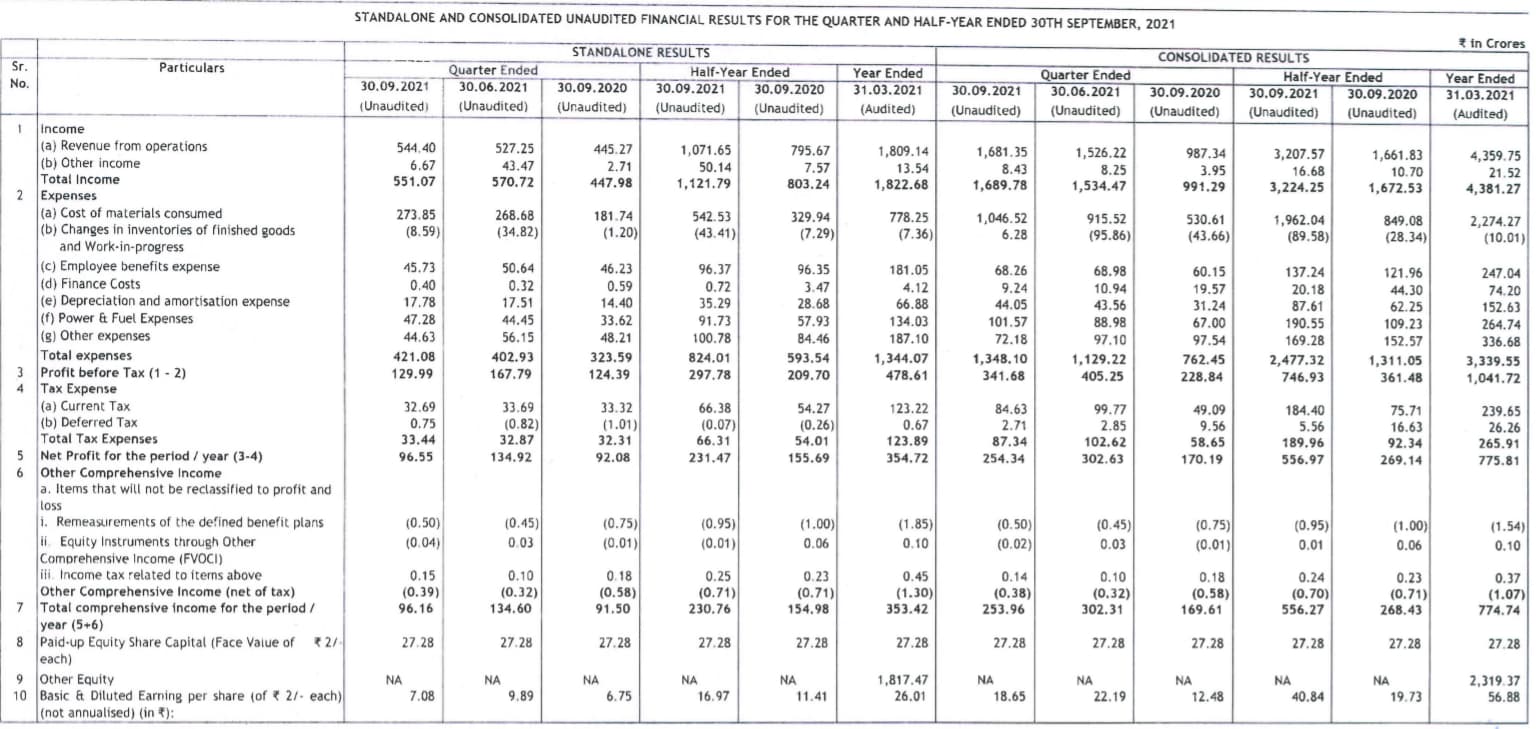

Net profit of 254 considering that last qrtr they had an inventory gain of 95 crores in that light this is an amazing result.

2 Likes

Quarterly results of period ending 30/09/21 came out at 18.42 hours, post market

Rotating the landscape view and presenting a snapshot here…

At first glance (the expectation these days is shiny shiny, for even firms like this, to do sequential growth in QoQ ; and that may not be have been met in net profit/EPS QoQ;)…rest looks good but needs a far more deeper look

1 Like

what does inventory gain mean? does it mean the inventory was at a lower cost and they sold at higher realizations?

Exactly. QoQ is decent whereas YoY is amazing growth. Deepak is not overvalued compared to peer group at these valuations.

3 Likes

Change in the inventory of finished goods refers to the costs of manufacturing incurred by the company in the past, but the goods manufactured in the past were sold in the present/current financial year.

A negative number indicates that the company produced more products in previous qrtr than it managed to sell.

7 Likes

Hi from the con call I gathered that Brownfield expansion of Basic Chemicals will kick in over Q3 with 15% increase in capacity.

Also IPA2 is to kick in from Q3 - any idea how much this would add to revenues?

1 Like

Assume that the capex is 150 crores, DN asset turnaround is 1.5- 2 consider an average of 1.75, or make it two , then the first year the addition to revenue is 75 crores assuming that they can utilize the new installed capacity at 100% , which given the DN capability that they could do . so i think you got your answer.

5 Likes

4 Likes

from a valuation point of view, it doesn’t look like the CMP is factoring in any major margin improvement in the next 3-4 years. If we forecast a 15-17% CAGR topline growth and a EBITDA margin around 20-22%, at 30 times EPS the stock seems to be around its estimated value as of now.

Q3,Q4 results are going to be interesting with more visibility on effects from expansion plans.

1 Like

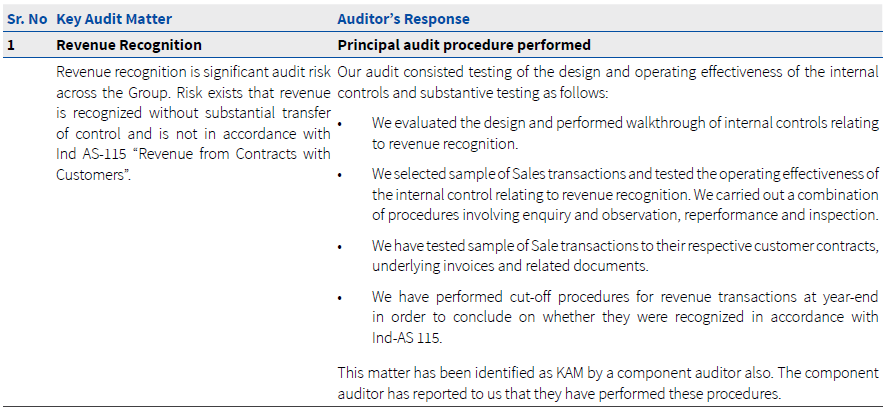

In the annual report auditor has highlighted about issue with revenue recognition. They did not further explained it so wanted to get some perspective on the comment.

9 Likes

@vedvyas Interesting observation. Thanks for the info. Are you going to check with management on this?

In a large number of cases, you will find Revenue Recognition mentioned as a Key Audit Matter. Auditors are required to mention something as Key Audit Matter and if there is nothing unique to report, they mention Revenue Recognition as the default Key Audit Matter, simply because it is very important. Unless there is any specific concern here, this looks like a routine comment.

3 Likes

+The cash conversion is really healthy. Immaterial matter in my view.

4 Likes