Deepak Nitrite Q4FY21 Con Call

Business:

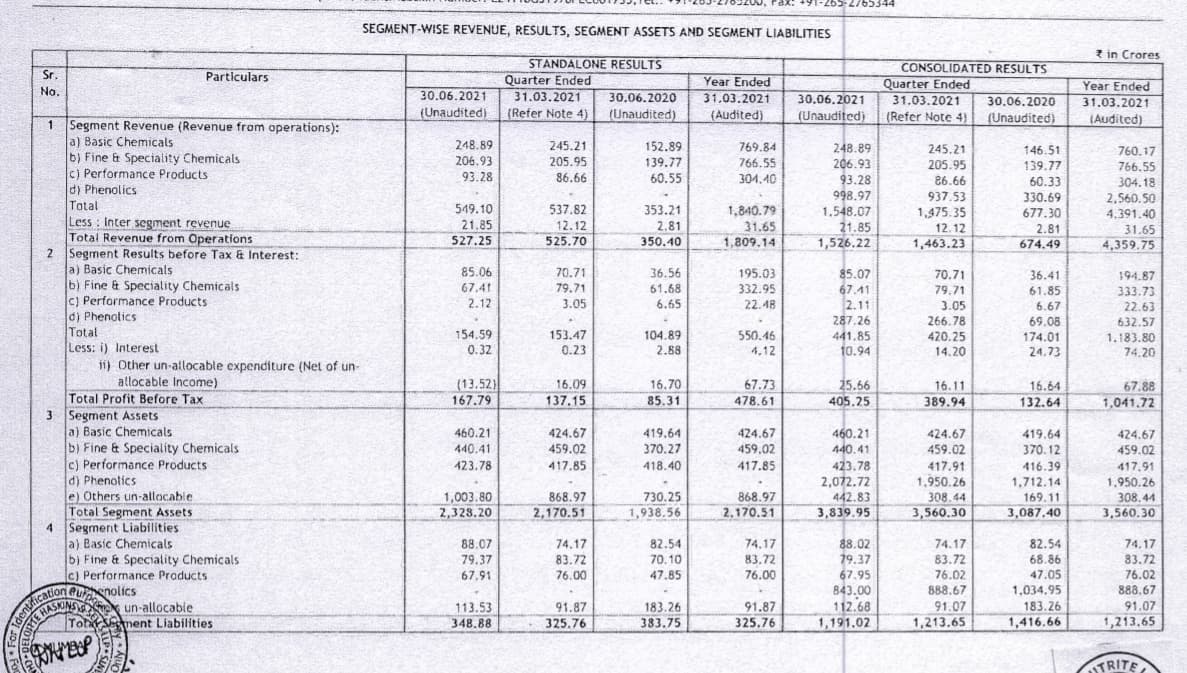

• Revenues in Q4FY21 were ₹1,469 crores (Up by 39% YOY & Up by 19% Q on Q). This was bolstered by volumes as well as realisation gains in the phenolics business that witnessed an incrementally favourable environment in the end user industries.

• Revenue growth was supported by basic chemicals & Fine & Specialty Chemicals Segment which witnessed volume growth & price firming.

• EBITDA stood at ₹ 461 crores in Q4FY21 (Up by 75% YOY & 36% Q on Q) EBITDA Margin improved to 31%( versus 25% in Q4FY20) as a result of increased productivity & operating leverage. DNL was able to build on the buoyant realisation for the phenolics product basket led by improvement in plant productivity in the operating team which was supported by efficient material handling & logistics.

• PBT stood at ₹ 390 crores (Up by 94% YOY) Primarily owing to strong results in BC, F&F & Phenolics businesses. Apart from DNL’s positive performance, PBT improved due to lower interest rates & substantial debt reduction over the last year

• PAT ₹ 290 crores in Q4FY21 (Up by 68% YOY ) as result of better operational & financial efficiency further aided by the revenue growth.

• Segmental Performance: Basic Chemicals segment revenue stood at ₹ 244 crores in Q4FY21 (Up by 9% compared to Q4FY 20 with ₹ 226 crores ) supported by strong volume growth as a result of a sharp turnaround in key end user industries along with higher realisation for specific products. This was achieved despite a significant increase in raw materials almost across the board and the company was able to pass on a lot of kickoff. EBIT increased by 27% to ₹71 crores (EBIT Margin of 29%)

• Fine & Speciality segment revenues grew by 30% to ₹ 206 crores as compared to ₹ 158 crores in Q4FY20 ,revenue growth backed by volume increment of 15%. The performance was propelled by strong demand and an appealing product line-up that is tailored to a broad diverse array of application. EBIT margin improved by 57% to ₹80 crores with an EBIT Margin of 39%.

• Performance Products segment reported revenue of ₹ 87 crores during the quarter. Performance Product segment reported lower revenues in Q4FY21 due to the impact of DASDA pricing in the base year which is exceptionally high & it is very very low at present. However, due to strong demand there us a segment volume increase of 12%. There has been significant impact in raw material price increases in performance products & the nature of the business here is that most of the revenue comes from contractual agreements which require either a price pass on or a review over a quarterly period or somehow at some point it is perfect for a 3 or 6 month period.

• Deepak Phenolics delivered an outstanding performance with revenue growth of 77%, EBIT expanded by 319% YOY translating to an EBIT margin of 28% as compared to 12% in Q4FY20. Plant efficiency measures culminated in utilisation levels exceeding 115% of defined capacity vs 98% last year as a result of healthy demand & firm realisations during the quarter, revenue for both Phenol & Acetone significantly increased to last year’s level.

• During the quarter, land development being our newly acquired Dahej site for 55 acres out of a total of 127 acres is nearing completion. The site will support capacity enhancement for key products in a standalone business & will be developed in stages.

• Plans for forward integration products based on Phenol & Acetone are being finalised & will be sharing them at an appropriate time.

• Deepak Nitrite throughout FY21, for almost all the products has maintained or gained market share for all the key accounts

• The company is reducing debt through cash flows & the Debt-equity is now at 0.5.

• In the end usage for Deepak Nitrite, Agrochemicals continued to see a strong demand for the whole year. The products which go into unique applications like personal care and in Q3FY21 & Q4FY21, we saw a resurgent in the demand for Dye Intermediates.

• Capex in Deepak Nitrite would be around ₹ 400 crores

• For Deepak Phenolics: Plans to grow in terms of our own capacity & go downstream but at the same time the right strategy would be to internally consume between 25%-30% of our basic chemical. That gives us resilience in our value chain also but at the same time we have successfully created a good niche for ourselves in our domestic market and we intend to maintain the market share.

• We are investing in greenfield production in the new sites and these will in addition to our existing technology platforms add fluorination & photo chlorination so what I want to clarify is that these are platforms. We put up the processes, we put up the towers, we put up the reactors and we have a good stable products that we look forward to making and the important point is that they fit very nicely with our existing value chains also.

• This is for us to integrate the new platforms with the existing core technologies that we possess so the investment is into products which will use all of these platforms in some permutations & combinations to give us value added new products.

• In the last 6 months we have done fantastic business selling to China also, so Deepak’s products are sold info China at very good margins.

• We are fine tuning on the long-term arrangement on a very advanced level for Contract manufacturing

• There is a bias towards fluorination & photo chlorination

Management:

• CEO: Maulik Mehta, CFO: Sanjay Upadhyay

• Deepak in partnership with its philanthropic arm has put up a 40 bed covid center with ICU & oxygen beds purchased & deployed medium & large sized oxygen PFA plants at nearby facilities. This is an addition to expanding medical & life insurance coverage for all employees & workers.

• Despite a loss of 1 month of production last year due to the lockdown, Deepak was able to record growth in the second half to erase the effects of the first half.

• The company was able to maximise utilisation of its facilities resulting in higher earnings.

• The board has recommended a dividend of ₹5.5 per share in FY21 equal to 275% of Face value. It does include a 50% special dividend to mark the company’s 50th year of operation

• Believe that the growth trajectory will continue across all of the SBUs fuelled by increase in capacity from brownfield expansion, new products that come out of Greenfield capexes & continued strong demand from our target end segments

• “We can run the plant efficiently, we know our team. We can do much more than what anybody else is doing and if you run your plant beyond 100%. If you run your plant at 115% to 120% and that too on a continuous basis. This adds a significant advantage to your operating cost. Your overhead cost is spread over to a large volume sp it reduces that. Any component of cost will have a fixed & variable component both. The fixed component gets distributed over larger & larger volumes. The key over here is how you utilise your plant to the maximum. These product in Phenol are a bulk commodity, it is more important to run your plant efficiently. How efficiently you manage makes all the difference” - Sanjay Upadhyay

• “Mr.Mehta mentioned to a group of investors that Phenolics business seems like a logistics company that happens to make Phenol & Acetone”-Maulik Mehta

• We are the largest benzene merchant buyer in the country

• “It all depends on a very simple question that we ask ourselves- what is the right to win that the company has ? Is it by going downstream because we have a particular relationship with the customer and then working upstream or is it going upstream because we have a better relationship with the supplier and what is the technology that is used? Is it something with familiarity which gives us the benefit or not. So nothing is a one trick pony. In Phenol we certainly took the decision of starting with the basic and then move downwards instead of the other way around. Luckily there is a lot of downstream application of Phenol which are all import substitutes. Many of them are now manufactured in India but there’s ample opportunity which is around”- Maulik Mehta

• China is now importing Phenol

• The volume uptick in Deepak Phenolics will happen in the first half of FY22, the one that we announced last year ( Power plant & IPA) and we have not yet announced capex in Phenolics.

• “We have a very strict template that we follow, any new investment which we call ‘Deepak’s right to win’ and that means that there must be a good reason for Deepak to invest in this product not just because it is currently looking very attractive. When we do our internal evaluation, we ask ourselves at the lowest price of the last 3 years and the highest raw material price of the last 3 years, would we still be able to make enough money to have between a 3-4 years of free cash flow position.

• There is raw material price increase

• Looking at 1.75x to 2x asset turns.

• Expecting to see a tepid demand for fuel additives in the coming quarters

Risk:

•Impact by raw material cost