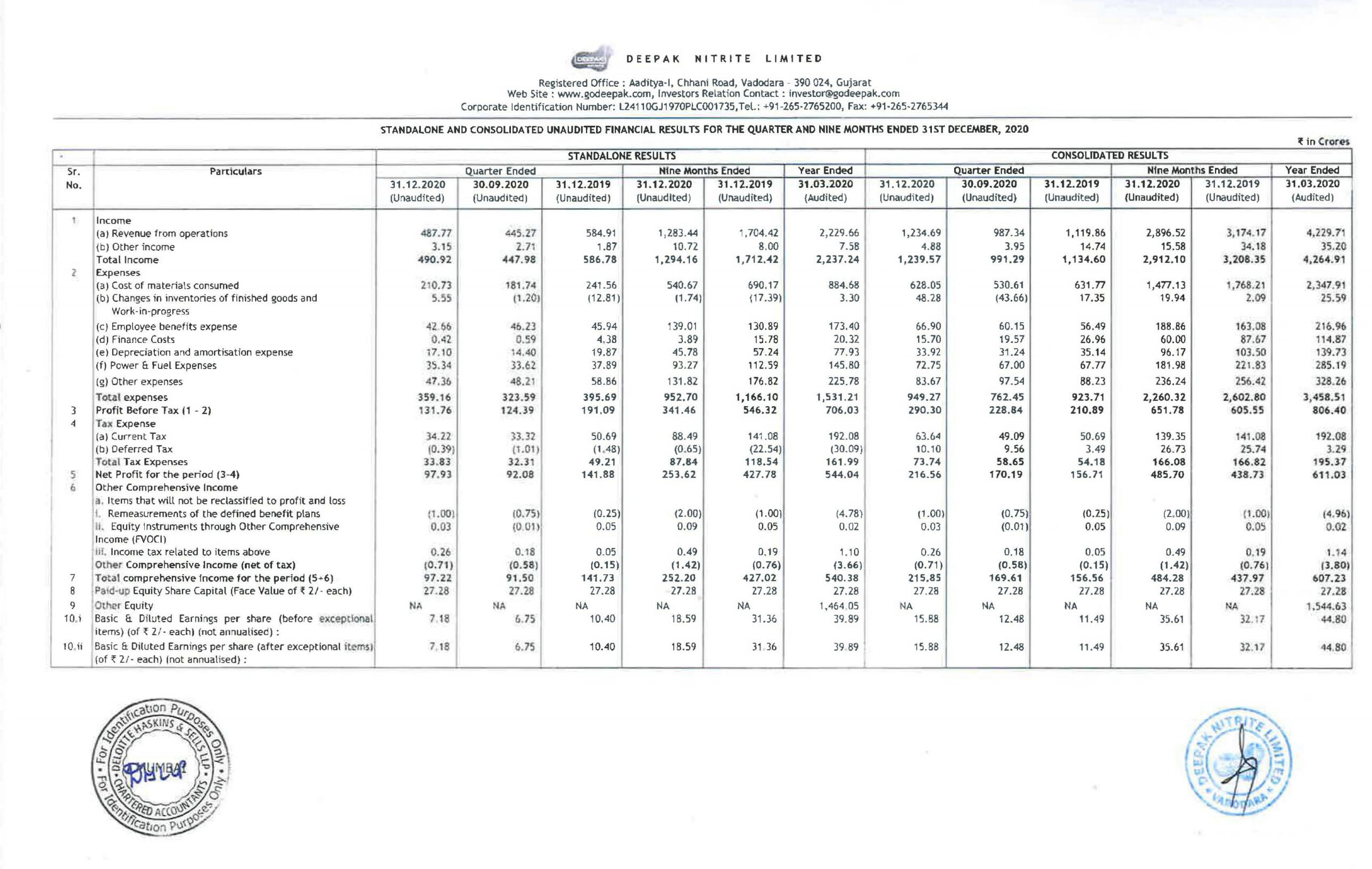

Very strong performance with 38% growth in PAT Y-o-Y, with EBITDA margins at 27.4%. Please note that 87% of revenues and 83% of EBIT profits are from phenolics and fine and specialty chemicals in Q3FY21.

| Consolidated (Rs cr) | Q3FY21 | Q2FY21 | Q3FY20 | Q-o-Q | Y-o-Y |

|---|---|---|---|---|---|

| Revenues | 1,240 | 991 | 1,135 | 25% | 9% |

| EBITDA | 340 | 280 | 273 | 22% | 25% |

| EBITDA margin | 27.4% | 28.2% | 24.1% | ||

| PAT | 216 | 170 | 157 | 27% | 38% |

You are confusing IPA with Phenols. Phenol has use cases across different industries and is not used in sanitizers.

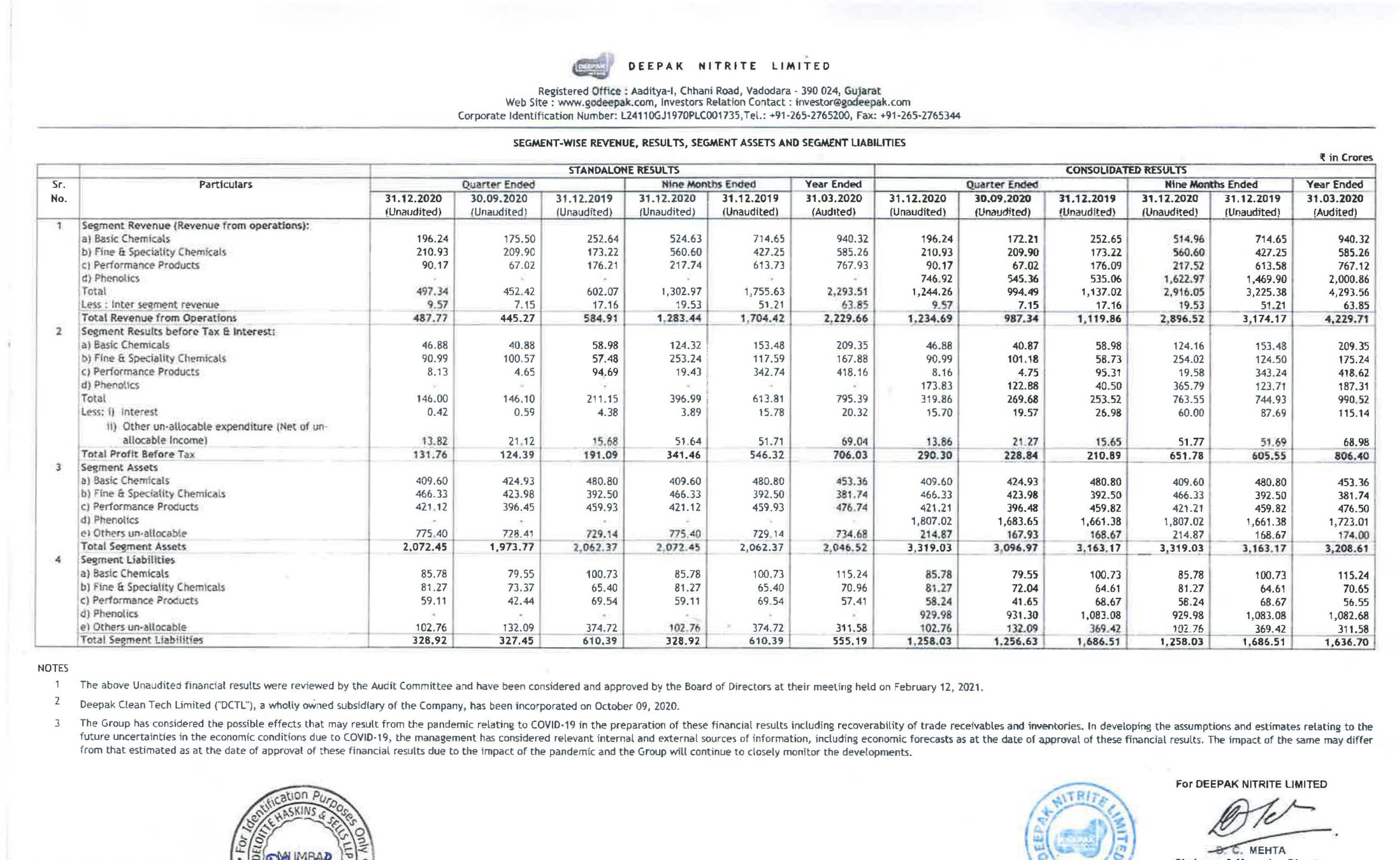

Deepak Phenolics is a 100% subsidiary where majority of the investments have happened in recent years. It is in the same line of organic chemicals intermediates, hence accordingly found consolidated financials more relevant. This is as per my limited understanding.

Disc: Invested

Looking at liabilities of performance products looks like more to come from it in near future.

looking at assets, revenue and profit of Performance products

HDFC Sec initiates coverage on Deepak Nitrite

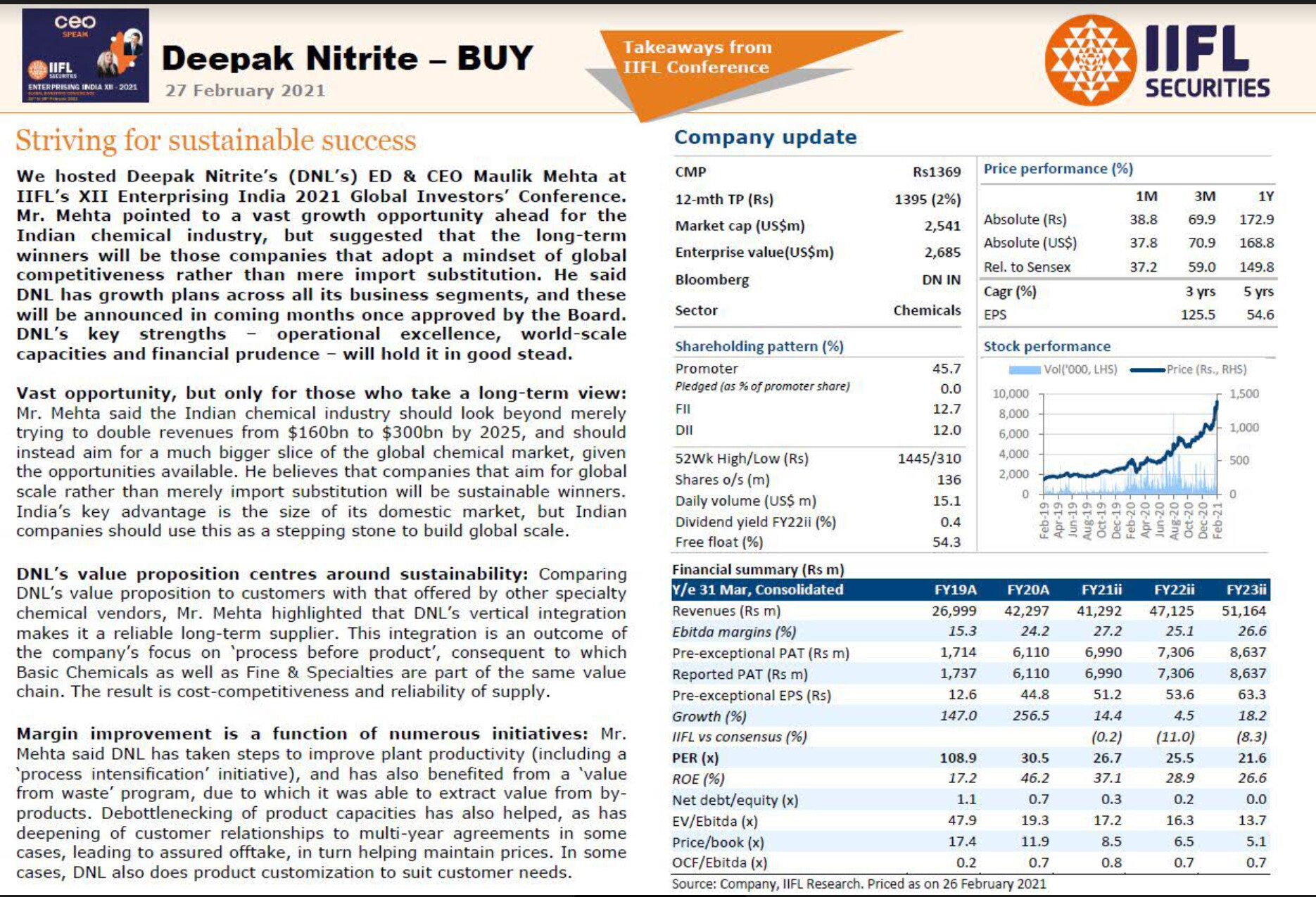

IIFL hosted Mr. Maulik Mehta, ED & CEO of Deepak Nitrite (DNL), at IIFL’s XII Enterprising India 2021 Global Investors’ Conference.

• Sees vast growth opportunity for Indian chemical industry: Mr. Mehta said the Indian chemical industry should look beyond merely trying to double revenues from $160bn to $300bn by 2025, and should instead aim for a much bigger slice of the global chemical market, given the opportunities available. He believes that companies that aim for global scale rather than merely import substitution will be sustainable winners. A key advantage India has versus other countries is the size of its domestic market, which helps Indian companies build scale and hence competitiveness.

• Growth projects to be announced in coming months: While DNL’s management has not yet received approval from the Board to announce specific growth projects, this should happen within the next 3-4 months, upon which the company will make formal announcements. DNL has multi-product and multi-process plans for growth, which will be executed over the next few years. Mr. Mehta has previously said that the company has aggressive internal targets for growth, but has refrained from sharing specifics.

• Key success factors: Highlighting the reasons for DNL’s successful track record over the past 50 years, Mr. Mehta pointed to the company’s financial prudence, strong execution skills across hazardous operations, and operational excellence initiatives. Additionally, he said that the last 5-7 years have also brought significant tailwinds for the overall chemical industry.

• Differentiation vs. other specialty chemical companies: Compared to other leading peers in the Indian specialty chemical industry, DNL’s value proposition to customers is somewhat different, in that the company is typically vertically integrated across all its products, which makes it a more sustainable supplier compared to most others, while also giving rise to better resilience in margins. Additionally, the company takes efforts to cater to bespoke requests of customers for product customization.

• Key focus areas as new CEO: Mr. Mehta said ‘Depend on Deepak’ is a key initiative he is focused on deploying: encompassing how DNL fulfills the needs of three key constituencies – employees, customers and investors. For employees, the company aims to become a great place to work and grow; for customers, one that offers cost excellence, product development and adherence to customer values (e.g., on environment, health & safety); and for investors, a company that offers a clear growth strategy, financial prudence and transparent communication. Another focus area is to judiciously add new competencies and products. And a third area is driving synergies across four key business functions: Finance, R&D, Business Development and HR.

https://trendlyne.com/posts/2831185/deepak-nitrite-will-the-phenomenal-growth-continueThe-Indian-chemical-industry-Unleashing-the-next-wave-of-growth.pdf (2.9 MB) Chemicals - Monthly Update - 26 Feb 21.pdf (863.9 KB)

Another good one Deepak vs Alkyl

Equity_Research_1614687541.pdf (1.4 MB)

Anti-dumping duty on phenol imported from Europe and Singapore increased till June 7, 2021

Analysts see further upside despite 135% rally in 6 monthshttps://www.business-standard.com/article/markets/deepak-nitrite-analysts-see-further-upside-despite-135-rally-in-6-months-121030500331_1.html

Hello friends, my earlier post on Deepak Nitrite was flagged due to containing a link to my personal blog. I have copy pasted the entire article onto this message, apologies for it being lengthy (some of my graphs may not load).

Deepak Nitrite: Can the Bull Run Sustain?

About:

Deepak Nitrite is an Indian chemical company. It is an expert at demonstrating how value can be extracted from commodity chemicals and how it can be added through specialty chemicals.

Deepak Nitrite is the domestic leader (market share over 70%) for much of their product portfolio and has based its product strategy on ‘import substitution’.

The company’s business segments can be broken down into (on a consolidated basis):

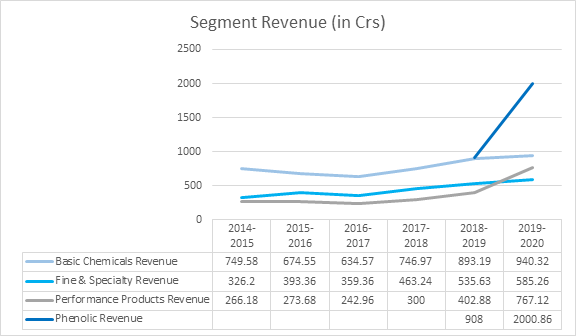

Basic Chemicals – 21.9% Revenue Contribution

- This segment is characterized by the commodity nature of its products. Sales from this segment tend to be high volume with low-moderate margins.

- Pricing power is poor and to a large extent depends on the underlying raw material prices.

- Moderate entry barriers due to high initial capital outlay.

- The lowest cost producer dominates the market.

- Key Products of Deepak Nitrite,

- Sodium Nitrite / Sodium Nitrate (80% Domestic Market Share)

- Fuel Additives (75% Domestic Market Share)

- Nitro Toluidine (50% Domestic market Share)

- Nitrosyl Sulphuric Acid

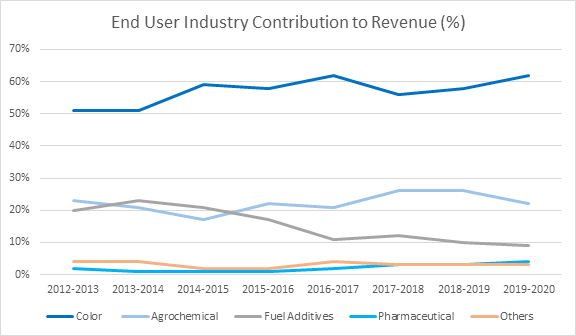

- End User Industries – Colorants, Petrochemicals, Rubber

Fine & Specialty Chemicals – 13.63% Revenue Contribution

- High value intermediates that address the direct needs of the customer.

- Low-Moderate Volume with High Margins.

- Client stickiness is a lot higher and contracts tend to be longer.

- Key Product Portfolio of Deepak Nitrite,

- Xylidines (Amongst the Top 3 Global Producers, Domestic Market Leader)

- Oximes (Amongst the Top 3 Global Producers, Domestic Market Leader)

- Cumidines (Domestic Market Leader)

- Specialty Agrochemicals

- End User Industries – Agrochemicals, Pharmaceuticals, Personal Care, Colors & Pigments

Performance Products – 17.87% Revenue Contribution

- Encompasses special ‘optical brightening agents (OBA)’ that are used by the Paper, Textile, and Detergent industries (OBAs impart the ‘whitening effect’). The company offers OBA formulations in either liquid / solid / powder forms as per the exact needs of the customer. The value of the OBA is tied directly to the characteristic it is expected to provide.

- Entry barriers tend to be high due to the need for international certifications and customer approval.

- The company has two main products in this segment,

- DASDA – Diamino Stilbene Disulfonic Acid

- OBA (75% Domestic Market Share)

- This segment is fully backward integrated right from the feedstock (Toluene) to the intermediate (DASDA) and finally to the end product (OBA). Deepak Nitrite’s manufacturing facility for OBA and DASDA is amongst the largest in the world.

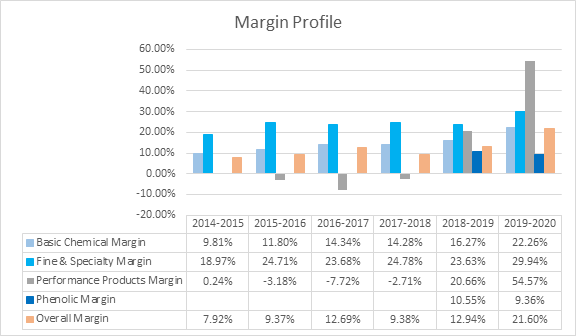

- The previous year saw abnormally high DASDA prices and realizations due to a major shutdown in China causing supply constraints (margins crossed 45%!).

- The recent Covid-19 pandemic has hit the end user industries incredibly hard and demand has been poor. This has led to a situation of oversupply. Going forward, the margins for the segment should move towards normalized margins of 15-20%.

Phenolics – 46.6% Revenue Contribution

(Setup through a wholly owned subsidiary – Deepak Phenolics Limited – DPL)

- This segment primarily manufactures Phenol, Acetone, and Iso Propyl Alcohol (IPA) today.

- The core emphasis of this segment is on ‘import substitution’. Earlier, India’s consumption of Phenol and Acetone was met through primarily through imports (over 80%). Sensing the opportunity to manufacture these products locally, Deepak Nitrite set up a massive manufacturing plant capable of producing 200,000 MTPA of Phenol and 1,20,000 MTPA of Acetone (started in 2014, commissioned in 2018). With such a large capacity, the company can address around 70-80% of India’s demand (maybe even more). It has already captured roughly 65% of the domestic market.

- Phenol and Acetone can generally be classified as Bulk Chemicals with commodity type behavior. However, the company also manufactures pharma grade high purity acetone which has much higher and stabler margins.

- The company has undertaken vertical integration to become the lowest cost producer (backward integration) as well as improve realizations by moving towards value-added derivatives (forward integration),

- Backward integration into the key raw material, Cumene, which will be captively consumed (Capacity of 2,60,000 MTPA).

- Forward integration into products like IPA (derivative of Acetone) which offers higher and stabler margins. Today, Deepak Phenolics is expanding IPA capacity from 30,000 MTPA to 60,000 MTPA. It has several other value-added derivatives in the pipeline (Possible candidates – Bisphenol A, MIBK).

- This business has also been aided by anti-dumping duty imposed on countries like Taiwan, South Africa, and USA, where oversupply of these products exists. Furthermore, some capacity in China has been removed and Chinese imports have reduced due to higher domestic consumption in China.

- The segment has also enjoyed ample and steady supply of domestic Benzene (key raw material used to make Cumene) which has allowed them to scale up incredibly fast (currently operating at over 100% capacity utilization). On the flipside, rising Benzene prices can shrink this segments margins drastically.

- End User Industries – Plywood & Laminates, Paints, Pharmaceuticals, Sanitizers, Rubber, Adhesives.

Another subsidiary, Deepak Clean Tech Ltd has been incorporated this year which will focus on developing a new product range using Deepak Nitrite’s core chemistries and Deepak Phenolic’s base product range.

Deepak Nitrite has over 700+ clients belonging to a diverse set of industries. Its client list includes,

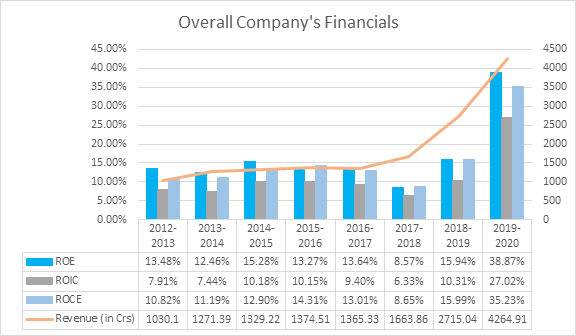

Image taken from Deepak Nitrite’s Financial Report

Manufacturing and R&D:

- Nandesari (Gujarat)

- Basic Chemicals and Fine & Specialty Chemicals

- Dedicated centralized R&D facility (Over 70 scientists and 35 patents in hand)

- Taloja (Maharashtra)

- Synthetic Organic Chemicals and Fine & Specialty Chemicals

- Roha (Maharashtra)

- Intermediates for Agrochemicals, dyes, and other specialty chemicals

- Hyderabad (Telangana)

- DASDA and other OBA Intermediates

- Dahej (Gujarat)

- Deepak Nitrite – Basic Chemicals and Performance Chemicals

- Deepak Phenolics – Phenol, Acetone, IPA

Competitive Advantages and Economic Moats enjoyed by Deepak Nitrite (Consolidated Basis):

Unparalleled and Clear Focus on each Segment

The business segments that we see today were formulated in the year 2012 as a strategic decision to drive growth independently in each segment. This clean and precise segmentation has worked wonderfully for the company with each segment capable of driving growth and covering for other segments in bad years. In recent times, the Phenolics segment has been a lifesaver for the company, filling in for the Bulk Chemicals and Performance Products which have been facing headwinds.

Economies of Scale and Low-Cost Producer

Deepak Nitrite’s Basic Chemicals and Phenolics segments tend to be commoditized and hence it is paramount to be a low-cost producer to be successful. In both these segments the company drives massive volumes, evident from their large market share in these products. The Phenolics segment has been operating consistently at 100% capacity.

Vertical Integration

If you observe, the company has been backward and forward integrating into much of their commoditized businesses. The backward integration helps lower costs, cementing their position as a low-cost producer. The forward integration allows for premiumization by moving into value-added derivatives, thereby boosting profits and sales.

The integration also helps reduce the effect of commodity cycles.

Strong Execution and Strategy

Deepak Nitrite’s strategy seems to revolve around identifying suitable products for ‘import substitution’ and then executing them with agility.

The Phenolics project was a massive undertaking for the company. It required large fund raising via bank debt and QIPs. With the amount of time and money that was required, it seems like the management had decided to go all in. The agility and efficiency with which the project was completed and commissioned is admirable and is a testament to the management’s ability.

The company has tied up with leading research institutions such as National Chemical Laboratory (Pune), Institute of Chemical Technology (Mumbai), IIT Bombay and others to bolster their R&D capabilities and expand their knowledge base.

Diversified Customer Profile and Product Profile

The company’s customers belong to a diverse set of industries and hence overall cyclicality is low. The company (on a standalone basis) continues to derive healthy diversification of revenues from its business segments. Historically, Sodium Nitrite, Nitro Toluene, and OBA have been their key products (DASDA was a key product last year due to abnormally high realizations).

Risks Faced by Deepak Nitrite (Consolidated Basis):

Short Lived Boosters to Growth

The Phenolics segment has been aided by a large plant shutdown in the US as well as anti-dumping duty imposed by India. The DASDA manufacturing shutdowns in China led to abnormally high DASDA realizations for the company with margins jumping from -2% in 2017 to 54% in 2020. Going forward, these margins are expected to normalize at around 18-20%.

Hence, while the company has done phenomenally well, its important to be cognizant about the factors that led to it.

Commoditized Business Elements

The company has exposure to commodity cycles through its Basic Chemicals and Phenolics segment. Furthermore, the Performance Chemical segment caters to Paper and Textile industries, both of which are cyclical. Hence, we cannot downplay the cyclicality of the business.

However, Deepak Nitrite enjoys leadership position, economies of scale, and robust vertical integration in its product range.

Raw Material Risk

While the company has adopted formula based pricing, it still requires a few months before it can pass on the raw material price volatility. Hence, raw material price volatility can affect the company especially in their commoditized business segments.

Opportunities:

- Rising disposable incomes and purchasing power should boost demand for the company’s end users.

- Import Substitution.

- De risking of supply chains from China.

- Ability to move into value-added downstream derivatives.

Financials:

The company had taken on significant debt to fund the setting up of the Phenol and Acetone plant. Over the years, the debt has reduced considerably (from well above Book Value D/E of 100% to about 37% today). Although operating cash flows have been largely positive over the past few years, Free Cash Flow (to the firm) has been largely negative due to significant capital expenditure (last year the company finally posted positive FCFF).

Valuation:

Based on my narrative and understanding, Deepak Nitrite has the right growth levers which should allow it to grow its topline consistently. I expect normalized margins (terminal year) of about 15-16% with a Cost of Capital (terminal year) of 9.47%.

My intrinsic value for Deepak Nitrite is INR 615.24 (conservative basis). While the intrinsic value range is between INR 557.74 and INR 723.36!

Conclusion:

Deepak Nitrite has had a stupendous run on the bourses, surging nearly 5 times since March 2020 in line with the rapid improvement of its fundamentals over the past two years. As we have seen, most of these improvements have come via new projects and abnormally high realizations on some products. Going forward, I will keenly continue to track Deepak Nitrite to get a better understanding of the ‘normalized’ and ‘sustainable’ fundamentals of its business.

I feel that Deepak Nitrite will continue to improve fundamentally, but today’s price of INR 1523 does not offer any margin of safety when compared to my intrinsic value!

Can you please elaborate your assumptions on

- Terminal year ?

- What is the % revenue contribution from BC, FSC & PP are you expecting?

- Margins for above segments in end state?

- Also what would be the triggers for current margins to “Normalize” ?

- Used a 10 year DCF model

- Expectations in Terminal Year - Basic Chemical (14%), Fine & Specialty (18%), Performance

Chemical (15%), Phenolics + Clean Tech (52%) + Other Income (1%)

3.I used blended margins (16% is between the 75th and 80th Percentile of Comparable Firms).

4.The expectation is that the current elevated margins are not structural in nature and eventually will get eaten away. Hence, basing your valuation off of the recent abnormally high realizations would lead to gross overstatement of value.

There were few pointers from management in recent concalls, here is from my notes:

- Network effect: Base setup & new industry position. Growth with accelerate.

- Large volume basic chemicals is base for specialty chemicals. MNC expects strong backward operations.

- We will focus on pharma intermediate, more open to CDM opportunities

- Fine & Specialty Business – EBITA 40-44% Margins, (avg 140 crore for last 8 qtrs) 200 crore revenue, greenfield and brownfield. It is sustainable (40-45% export). Brownfield expansion, debottleneck

If one do not see growth in high margin business (FSC) then there is no point betting on Deepak Nitrite. As rightly pointed out by your model. May be market (including me!) are betting on increase in FSC business in future. I always remember a line from recent management interview “Deepak in next 5 years won’t be same as today”. Let’s see if management walks the talk.

Deepak Foundation - CSR Arm

Hi everyone,

Have compiled a document on Deepak Nitrite based on Motilal Oswal’s QGLP Checklist- having 5 broad buckets for Business, Growth, Management, Risk and Price (have laid less emphasis on Price/Valuation since I’m not an expert on the subject)

Having been invested in the company for the past 6-7 months, the motivation to create the stock analysis was to gather all my scattered notes and other available information on the company in a structured manner for my own understanding.

Posting it on the forum so it becomes easy for any new member researching the business to get upto speed.

Have added screenshots for some information available from various public sources instead of creating my own charts/tables to save time (since beautification of the document wasn’t a priority).

There is a good chance that I’ve missed something in the analysis/from QGLP checklist since this is my first attempt at a proper deep dive.

Have given due credits wherever possible, apologies if I’ve missed it anywhere. Most numbers are sourced from screener.in

Laying down some sources for people looking to study the specialty chemicals sector (have also referred to these sources in my analysis)

- PPFAS Chemical Sector Breaking Bad with the Chemicals Sector - YouTube

- Vivek Mashrani Chemical Sector Analysis Chemicals Sector Analysis | Top 5 Specialty Chemical Stocks - YouTube

- SOIC Deepak Nitrite Deepak Nitrite| Stock Analysis: A Diversified Chemical Company - YouTube

- Deepak Nitrite ValuePickr Thread

- VP Chintan Baithak 2019 ValuePickr Chintan Baithak 2019 - Chemicals 2.0 sector presentation

Disclosure: Invested from sub 600 levels. This is not an investment recommendation and I’m not a SEBI Registered Advisor. The views presented in the document are my own and not the views of my employer. Views may be biased, please do your own due diligence before investing. The analysis is only for education purposes.

Deepak Nitrite_Deep-Dive_vF.pdf (2.3 MB)

Deepak Nitrite - Leading Indian producer of Sodium Nitrate

The company dictates 80% domestic market share in sodium nitrite and 50% market share in nitro toluene. Also, nitro toluene acts as a key raw material for the Performance Chemicals segment. The end-user applications of DNL’s products vary from agrochemicals, dyes, and pigments to pharmaceuticals, rubber chemicals, refinery, textile, and colorants.

In FY 2019-20, the Company invested 270 Crores towards initiatives on capacity expansion and debottlenecking of existing plants. This expenditure also covers the new 125-acre land purchased at Dahej during the year. This land is strategically located surrounded by key suppliers and customers paving the path for ample opportunity for growth.

Improved Financial Ratio

The company demonstrated strong all-around performance led by healthy growth across its Strategic Business Units (SBUs). On a Standalone basis, revenues climbed to 2,230 Crores, 25% higher than the previous year.

EBITDA registered at 804 Crores, up by 161% from the previous year resulting to EBITDA margins of 36%, higher by 18.77%. Profit Before Tax (PBT) was recorded at 706 Crores, up by 232% from last year. Profit After-Tax (PAT) stood at 544 Crores, representing an improvement of 294% compared to FY 2018-19.

Capacity Build-up

With future CAPEX to be incurred largely through internal accruals, the Free Cash Flow to the Firm (FCFF) should turn positive. On the back of sustained CAPEX, debt in absolute terms will largely remain flat.

In FY 2019-20, the Company invested 270 Crores towards initiatives on capacity expansion and debottlenecking of existing plants. This expenditure also covers the new 125-acre land purchased at Dahej during the year. Deepak Phenolics, which is now in the process of safe scaleup to capacity. DPL had it first full year of operations in FY 19-20, wherein its Phenol production volumes were just short of 200,000 tons or above 90% capacity utilization.

My observation or Focus point from the results was Cash Flow.

They are not able to generate Cash in sync with top-line.

Was it due to their efforts towards cleaning balance sheet and reducing debt.

As i mentioned earlier also in Normal Environment Performance products will further augment the top-line but covid related catalyst wont be there.

So question is , With current capacity has the peak reached ? or if they are to do Capex further without cash in hand Balanced sheet will be stressed again ?

Let me know if i am wrong in my understanding.

Thanks in advance.