Too much headwind for this company.

Key headwinds as per rating rationale:

The ratings are, however, constrained by the agro -climatic and regulatory risks in the fertiliser business and the vulnerability of the chemical division’s profitability to the inherent price cyclicality along with the volatility in natural gas prices. The ratings are also constrained by the large debt- funded capex plan being undertaken by the company i.e., the technical ammonium nitrate (TAN) project at Gopalpur with a capital outlay of nearly Rs. 2,200 crore and the nitric acid plant at Dahej with a capital outlay of Rs. 1,950 crore. The large capex plan exposes the company to project execution risks and timely commissioning of hese projects and within the proposed capital outlay will remain a key monitorable going forward.

DFPCL is reorganising its operations under fertiliser and chemicals business separately. On a consolidated basis, ICRA does not expect the reorganisation to have any financial impact, as it will help in streamlining the company’s operations. However, ICRA will continue to monitor the developments on this front.

Further, ICRA also notes the appeal filed by MAL in response to the receipt of assessment and demand orders for the block period (assessment year 2013 2014 to assessment year 2019 -2020) pursuant to the search operation conducted by the income tax department in November 2018, resulting in a demand of Rs. 486 crore (including interest). ICRA will continue to monitor the development on this front.

Large debt - funded capex :The company has recently commissioned its 5,10,000- MTPA ammonia plant at Taloja in August 2023 with a capital outlay of Rs. 4,030 crore till September 2023 and will be incurring another Rs. 470 crore, including purchase of certain stores and spares within FY2024.

As on September 30, 2023, the company had an outstanding external long-

term debt of Rs. 3,175 crore. However, due to the long repayment tenure of the term loans, the annual debt repayments are likely to remain modest (~Rs. 122 crore in H2 FY2024, Rs. 389 crore in FY2025 and ~Rs. 535 crore in FY2026)

Their ultimate customer for TAN was Coal India and if Coal India itself is coming up with such huge capacity it will be very callenging for the Company to sell its TAN from upcoming new plant and Coal India plant is also coming up in Orissa.

7 Likes

Hi guys ,

Current situation

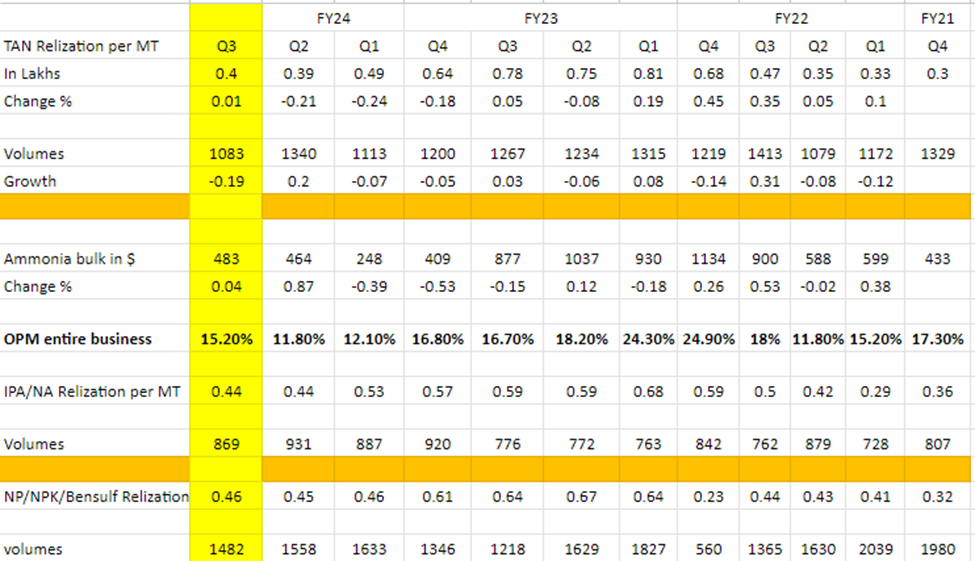

- From this table I just came up with this theory earlier that ammonia is a leading indicator of TAN realization with 1 quarter lag. Like Q3FY22 AM up by 53% from Q2 and in Q4FY22 TAN up by 45%. Now see this for the rest of the table.

What I am not able to understand is in Q2FY24 AM was up by 87% but in Q3FY24 TAN realization was same. (May be dumping effect)

So what management says already Russia was dumping in India + what they used to export to Brazil that is also being dumped in India because demand in Brazil is low.

QoQ the sales are down by approx. 600cr= 120cr of chemical and 410 of less fertilized trading + fertilizer margins also impacted (totally unexpected after last quarter volume trends) + this quarter we again had 34cr of stabilization loss. I was looking at a 150-200cr PAT for Q3 which was achievable if we did not have these 2 surprises. Totally unexpected!

QoQ fertilizer segment result from 42cr PAT to 76lakh loss. Figure in lakh

Next quarter

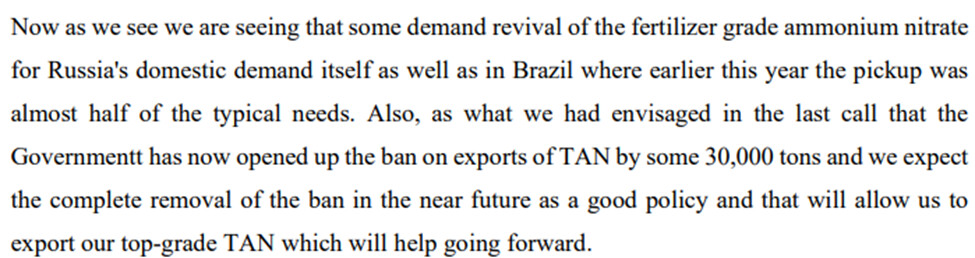

- TAN export is going to start + management is expecting Russia dumping to slowdown as their demand is picking(need to find a way to verify this) but this is going to be very less like 6% of overall capacity any more lift would be beneficial

- Fertilizer segment

Now with 10% PBT margins cap, approx. 6.5% to 7% PAT margins is what they can do going forward, this year fertilizer segment was a disaster. Last FY approx. 5000cr sales were done from fertilizer and until now 3000cr has been done. So assuming 4000cr of sales 260cr to 280cr from this segment is possible going forward

- Ammonia

So they are waiting for the eligibility certificate for the state government incentives, so this is I think the 9% GST wavier on sale price, so if they get it then they can realize all the benefit in Q4 or Q1FY25 for all the production since august.

Current economics are such that Cost of production 470$ (20$ drop qoq) and current ammonia price is 362$ + all benefits = 510$ so 40$ = 150cr about 40cr for Q4. They said plant has stabilized, so maybe next quarter we can see the benefit incase ammonia does not fall further

Lets say they do 6000cr in entire chemicals segment taking a margin of 20% (pretax, pre-interest) that would be 1200cr PBIT, approx. 400cr interest so PAT can be 600cr (this is just math, I have done it for the sake of it to have a number in front of me, plz correct if I went wrong anywhere)

For current 9FY24 months 800cr is PBIT for chemical segment I have taken the same above

All in all 600cr + 260cr + 110cr = 970cr is the PAT we can expect at current run rate for FY25 (purely mathematical)

Negatives for lower PAT is more surprise on fertilizer segment , ammonia price falling, continued Russia dumping, interest cost increasing.

Positives for higher PAT is Ammonia price stable/increasing, export ban complete lifting, anti-dumping duty, interest cost decreasing, debt decreasing from ammonia cash flow.

New contract done

New gas price from 1jan 2026. What is going to be the price, management gave some clue in previous concall.

360$ of GAS cost and taking current price of 360$ (long term average is 400 to 450) the savings is approx. 150$, taking 90% utilization = 570cr (this should be higher)

If we take avg ammonia price 450$ then the benefit can be 920cr and this is base case because we are taking avg ammonia prices

This is 2yrs and 8months away to begin with and 3yrs 8months away to realize the benefit

Now guys based on the assumptions above looks like it is a 1000cr business at current run rate but the business is so dynamic we don’t know which segment can eat way our bottle line . Now we need to understand what growth it offers on top line for next 2 to 3yrs and based on that what PE/valuations it deserves, this would give us a rough idea of upside and then we can take our call weather it is a good investment or not. (If somebody can do this exercise that would be helpful) i would do this sometime later and share my view

I would advise to consider their 2capex and TAN as a solution, entering into solar grade when doing the above exercise.

Thank you and sorry for the delay

12 Likes

@manhar Isnt valuation now more lucrative as per your analysis?

1 Like

As Company is mainly into commodity business, valuations may remain undervalued for a prolonged period of time. As the general market is in bull run one should factor in opportunity cost also.

2 Likes

I was going through research report of Aegis logistic here are some capex they are doing.

This initiative aligns with India’s National Green Hydrogen Mission (NGHM), which has allocated INR 19,744 cr to achieve a production target of 5 mn tonnes of green hydrogen annually by 2030. Green ammonia, a derivativeof green hydrogen,

will also be produced under NGHM and it will be especially relevant for the

fertilizer industry. Currently, Indian fertilizer companies primarily derive ammonia

from imported LNG, leading to higher production costs. Over the past three years,

the government’s subsidy for the fertilizer sector has been significant, reaching

INR 1.3 trillion in FY23, INR 1.4 trillion in FY22, and INR 1.1 trillion in FY21.

With the anticipated growth in fertilizer demand in India, the need for ammonia is

also set to rise. The government’s strategy to shift from imported LNG to a cleaner

and domestically produced feedstocks is expected to increase the demand for

green ammonia and its related transportation/storage infrastructure. AVTL’s

upcoming green ammonia storage facility is poised to be a key strategic asset,

potentially benefiting greatly from the NGHM.

3 Likes

Can you share research report or link of the report ?

This is in reference to note no.3 which is part of “Notes to the Statement of Standalone

and Consolidated Financial Results for the quarter and nine months ended 31st

December, 2023” submitted to the stock exchanges.

In terms of provisions of Regulation 30 of the SEBI (Listing Obligations and Disclosure

Requirements) Regulations, 2015 and in furtherance to the aforesaid intimation

submitted by way of note, this is to inform that the appeals filed for the period from AY

2013-14 to AY 2018-19 by the Material Subsidiary of the Company i.e. Mahadhan

AgriTech Limited (formerly known as Smartchem Technologies Limited) (MAL), have

been dismissed by the Commissioner of Income Tax (Appeals), Mumbai.

How much was the tax demand.

1 Like

485cr

i think TAN business is what looks more lucrative to me as mining as a theme will rise in india their tan facility and Consultancy services which they are providing, as discussed in latest concall will be of key competitive edge.

post demerger things will be interesting & i am looking forword to it.

1 Like

Thanks for sharing good article on the company!!!

1 Like

Does anyone have an insight into the nitric acid expansion. Historically, they have sold 20% of the produced volumes externally. I am wondering how to think about the upcoming capacity in those terms.

Hi VPers,

I found something peculiar in the AR FY23 on page 120 :

123 crores as commission?

Disclosure : have a tracking position

11 Likes

Thank you for bringing this to notice.

I see this as an oversight in my governance filter. Exited now…

Hello All,

I checked the following information on the topic above.

//Snippet from web starts//

What is the limit of remuneration to directors?

The overall limit on remuneration or salary payable to all managing directors or whole-time directors, collectively, is capped at a maximum of 11% of the net profits of the company.12 Feb 2024

//Snippet from web ends//

As per this guideline, Deepak Nitrite is not in violation of Corporate Governance topics.

I checked Annual Report of 2022 and 2023. Both figures seem to be in accordance to the policy above i.e. within 11% of NET profits.

4 Likes

ADD also imposed on imports of IPA or Iso Propyl Alcohol.

Deepak fertilizers and Deepak Nitrite (phenolics) both have major capacity here.

Positive for these two stocks.

IIFL Chemicals: Anti Dumping Duty imposed on IPA – Positive for Deepak Fertilizers and Deepak Nitrite

DGTR, Ministry of Commerce, has recommended an anti-dumping duty (ADD) on IPA originating in or exported from China. It now requires approval from the Ministry of Finance for implementation.

DGTR has recommended a duty of US$217/mt for imports from most companies in China. Imports from China nearly doubled in FY23, accounting for ~65% of total imports into India.

Deepak Fertiliser and Petrochemicals (DFPC) and Deepak Nitrite (DN) are the only manufacturers of IPA in India, with near similar sales volumes of ~65ktpa in FY24ii.

6 Likes

Key takeaways from investing accelerator summit

By , Ishmohit Arora (SOIC/ Persistence Capital), has excellent business insights on Deepak Fertilizer

1.Whenever business margins become consistent despite the volatility in the past, then those businesses create huge wealth for investors. Past examples, like Neuland and Garware Hi hi-tech

2. In Deepak Fertilizers, the volatility of the margins is going down as business is getting backward integrated.

3. Here, the product mix is changing from fertilizers to mining chemicals and industrial chemicals; the fertilizer revenue contribution has come down from 80% to 45% now.

4. In the TAN business, they are moving forward with integrating explosive chemicals, similar to Solar Industries.

5. Their margins are becoming consistent to 18–20%.

6. After the capex, they will have the capacity to meet 60% of India’s domestic requirements.

7. Fundamental triggers are ammonia prices going up, TAN spreads increasing,and support from the government with an increase in import duty

8. During FY25, they can do 950 to 1000 crore PAT if commodity prices remain stable; so they are trading at a 12-13x PE ratio.

Link below

https://twitter.com/ias_summit/status/1826865267802079408?t=5miKuCDO0rgzp_Q3Iytxbg&s=19

Disc - holding, not a buy/sell recommendation

16 Likes