Ammonia price is increasing which will generate good delta for newly commissioned Ammonia CAPEX…

Hi,

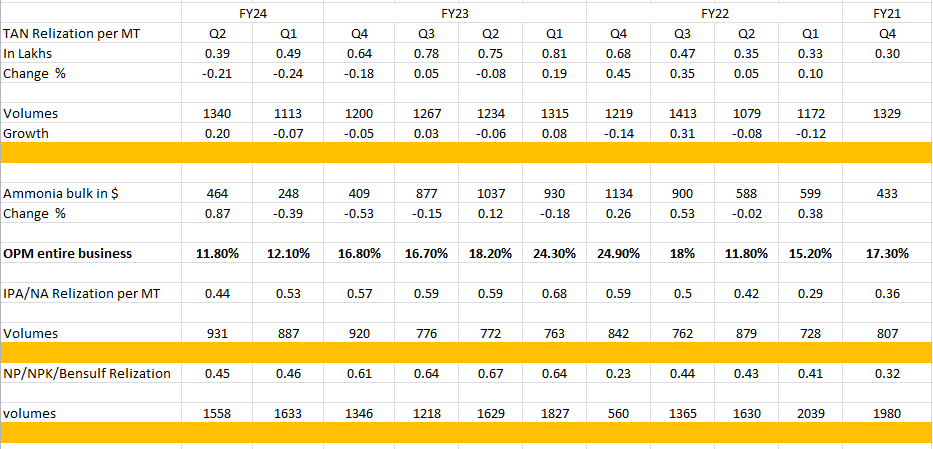

Can you plot Q1 and Q2 number on excel and share the calculation?

1 Like

I explained above how you can interpret this table, so this quarter we had 87% increase in prices so the effect would be visible in next quarter, so TAN realization should go up next quarter.

My guess is next quarter should be 200cr + unless another fertilizer subsidy effect (This is just a guess no hard facts)

I also tried to explain ammonia cycle in one of my post

So I am thinking this way if gas prices go up then ammonia prices go up through out the world (gas is raw material) so if the beta of deepak fertilizer GAS prices compared to rest of the world is low they benefit big time because their savings increase in ammonia + TAN realization. Vise versa they loose more when gas price fall.

This comparison is purely of gas and ammonia, gas is just one of the factor in ammonia price fluctuation.

Yes you are correct, 110$ = 114cr per quarter at current rate subjected to full capacity utilization. At 75% or 80% utilization 85cr to 90cr

@vikashkota attaching the excel here so that you can add the future quarters and share with us

2 Likes

Thanks for your Indepth sharing.

- You can also factor cheap Russian FGAN (Fertilizer grade Ammonium Nitrate).

- Benefit of Economic of scale is added advantage of Deepak, but its take 1 or 2 Quarter.

- Nov’23 contract of Ammonium on SGX $ 600+

3 Likes

Any update on NCLT hearing for demerger ?

You can track the progress in NCLT. The link is already mentioned in the following post

However this would not be a material event in the short term. The is a demerger with in the listed company and the demerged cos will be subsidiaries of the listed co i.e. Deepak fertiliser.

The management tries to bring institutional investors to these subsidaries (i.e. demerged companies) and then list them seperately later. I hope it can happen by Fy 2026

Disc: Holding small position

Praveen

1 Like

While going through company website, surprisingly, company has Creaticity Mall

in Pune (https://www.creaticity.co.in/) . Why company is in non-core business? - any one has any idea / more information about it?

Based on reported result - normally this business always reports losses!

Back in 2021 management had said they are considering selling non core asset including this Pune mall. Back then they had valued it around ₹700-800 crores.

Source: https://twitter.com/Nigel__DSouza/status/1453236123334057992?t=JlJW62-bjjcxMaruKvf9Vw&s=19

1 Like

Ammonia prices going down will have negative impact on newly commissioned Ammonia CApex.

5 Likes

The Consolidated result for the quarter includes loss from Ammonia Business amounting to Rs. 3,420 lakhs, and loss for nine-month period is Rs. 18,101 lakhs emerging out of initial stabilization period and low Ammonia prices globally. During the current quarter the Ammonia Plant has achieved a stable capacity utilisation.

6 Likes

Some of the key points from earning presentation are (Q3 FY2024):

DFPCL has successfully commissioned its greenfield ammonia plant, which reduces its risk exposure from ammonia to downstream products and enhances its efficiency and competitiveness. The plant has also received state-approved incentives that are expected to kick in during this year.

DFPCL’s mining chemicals business (TAN) is facing challenges from increased imports from Russia, but expects the demand to remain stable in Q4 FY24. The company is also exploring export opportunities for its high-quality LDAN product.

DFPCL’s pharma and specialty chemicals business (IPA and nitric acid) is witnessing a recovery in demand and prices after a period of low demand from downstream industries and imports of nitroaromatics from China. The company has also commissioned a new solar grade nitric acid plant that is expected to have better volumes.

DFPCL’s fertilizers business (CNB) is impacted by lower-than-average rainfall, limited water for irrigation, and unseasonal rains and hailstorms in its core markets. However, the company is launching innovative and crop-specific products such as Solutek and Croptek that are gaining acceptance among the farmers. The company also expects a good fertiliser Kharif season with the prediction of normal monsoon for the current year.

DFPCL has reduced its promoters’ pledge to zero and has no encumbrance of any kind on its promoters’ holding. The company also has a diversified and reputed institutional investor base that includes International Finance Corporation, Axis Mutual Fund, BNP Paribas Financials, Habrok Capital, Life Insurance Corporation, Aequitas, Government Pension Fund, New India Assurance, Vanguard and Abu Dhabi Investment Authority among others.

10 Likes

Investors are excited about Ammonia plant commissioning. However, we need to take following points -

(1) Gas based ammonia plant economics depends on Gas prices. As Gas prices are fluctuating a lot, economics of the ammonia plants also get fluctuating a lot ! As per management, new ammonia plant pay back period is 7 to 8 years !!. If Gas prices goes high, imported ammonia gets cheaper!!.

(2) Government also pushes green ammonia (what is green ammonia - Link) to minimize reliance on import gases. This concept is very much linked with green hydrogen economics. Considering innovation and world push on green hydrogen, this one should not ignore . (Good article link)

Regarding Ammonium Nitrate - Government is more focused on farmers and do all they can do to reduce burden on farmers by controlling fertilizers prices and its inputs. Russian and China has excess capacity. Slow down in China, could be another risk of cheap AN import. (Cheap Import of AN increasing - link)

Main customer of TAN - Coal mining. Coal India looking all option for cheap TAN and govt always help them by allowing cheap import form China and Russia.

(3) Additional capacities coming for TAN (Link)

Company has significant debt on its book and invested capital has future risk. Hence, we need to wait and watch for few qtrs. I think company has tough time ahead and unless there is significant margin of safety, it might not give good return on investment for investors

Disc - Not invested but tracking as I believe promoters capability of execution !! Comparing Coromandel International and Deepak Fertilizers … I am more inclined towards Coromandel International (invested and keep adding it on poor result correction)

10 Likes

Management itself admitted that high margins in previous year were an aberration. DFPCL seems to be a pure commodity play and therfore valuations will also adjust accordingly.

EPS will be in the range of Rs 5 per quarter (i.e annualised EPS of Rs 20 ) for next 6 to 8 quarters. Now it is upto individuals what PE they can give for a commodity player.

Even if we give a PE of 15 to 20, there is a long head room for correction in valuation.

Further there is an over hang of 2 major CAPEX undertaken by the Company of around Rs 4000 to Rs 4500 Cr (TAN & Nitric Acid)

Fertiliser business is making losses, overall margins are squeezing, Ammonia Capex of Rs 4500 Cr is making losses and Gas for Ammonia plant has been contracted at a higher price.

As per my calculation, Cost of production of Ammonia for the Company would be upward of 450.

After listening to Concal, I got a feeling that CFO is not hands on with critical figures like margins, spreads, total/net debt etc. and Mr Tarun TAN head seemed to flattering chairman in every statement he made. ![]()

Disclosure: Exited position and now tracking for knowledge purpose.

13 Likes

post deleted as not related to current topic

I feel the risk and opportunity cost of time is not worth it. Exited this position in pursuit of better opportunities.

1 Like

Btw CFO will be resigning

but there is no exchange notification in this regard…

A Big Step Towards National Coal Gasification Mission, the Plant is expected to Produce 2000 tons of Ammonium Nitrate per day

https://pib.gov.in/PressReleaseIframePage.aspx?PRID=2009826

This is big negative for Deepak Fertilizers as Coal India is the biggest customer for them!

1 Like