Management meet

3 Likes

Section 129 (Financial Statement) of the Companies Act, 2013

Sub-section (1)

The financial statement shall give a true and fair view of the state of affairs of the company or companies, comply with the accounting standards notified under section 133 and shall be in the form or forms as may be provided for different class or classes of companies in Schedule III:

Provided that the items contained in such financial statements shall be in accordance with the accounting standards:

Sub-section (7)

If a company contravenes the provisions of this section, the managing director, the whole-time director in charge of finance, the Chief Financial Officer or any other person charged by the Board with the duty of complying with the requirements of this section and in the absence of any of the officers mentioned above, all the directors shall be punishable with imprisonment for a term which may extend to one year or with fine which shall not be less than fifty thousand rupees but which may extend to five lakh rupees, or with both.

Section 448 (Punishment for false statement) of the Act

Save as otherwise provided in this Act, if in any return, report, certificate, financial statement , prospectus , statement or other document required by, or for, the purposes of any of the provisions of this Act or the rules made thereunder, any person makes a statement,—

(a) which is false in any material particulars, knowing it to be false; or

(b) which omits any material fact, knowing it to be material,

he shall be liable under section 447.

Section 447 of the Act (Punishment for fraud)

any person who is found to be guilty of fraud involving an amount of at least ten lakh rupees or one percent of the turnover of the company, whichever is lower , shall be punishable with imprisonment for a term which shall not be less than six months but which may extend to ten years and shall also be liable to fine which shall not be less than the amount involved in the fraud, but which may extend to three times the amount involved in the fraud:

Provided that where the fraud in question involves public interest, the term of imprisonment shall not be less than three years.

Explanation (i) “fraud” in relation to affairs of a company or any body corporate , includes any act, omission, concealment of any fact or abuse of position committed by any person or any other person with the connivance in any manner, with intent to deceive, to gain undue advantage from, or to injure the interests of, the company or its shareholders or its creditors or any other person, whether or not there is any wrongful gain or wrongful loss;

2 Likes

I just wanted to bring attention to the kind members of the forum on how serious my allegations are. Complying with accounting and auditing standards is not “voluntary”/“optional”. Standards don’t care about “economic reality”. What they care about is providing for receivables which are due from 3 years with serious credit risk deterioration indicators, proper acquisition accounting treatment, proper audit opinion, mandatory disclosures etc.

Standards do not care about Deep paying only Rs 2 crores for the acquisition and saying that even a 5% recovery is a win. They do not care about the “9000 shares” that grew 3 times over the last 2-3 years. They do not care whether the company is paying out dividends.

If the management too doesn’t care, well I laid out the penalties. Imprisonment was common though. Definitely not a slap on the wrist.

3 Likes

Hi

I had absolutely decided to cease my posts on this thread but when my posts were termed “nonsense” or “ramblings” that irked me.

I have no monetary incentive to do this. I do this because I care about proper financial reporting in the Indian capital markets where retail investors like you and me invest their hard earned life savings.

And I didn’t expect a thank you but terming my posts, which I made, in the forum’s interest (not mine) as “ramblings” or “nonsense” was where it became personal to me.

You have absolutely no idea how much time I have spent on this company when I knew I was never gonna invest. Why? Because I had a short position? No. It’s because I wanted to. In the investors’ interest. I am serious, you cannot imagine the number of hours spent on doing this and I am not even counting the drafting part. Reading Annual reports, 80 NFRA indictments, Corporate Law, Insolvency Law, drafting report, making excels, all for what? Terming it as nonsense?

I am open to criticism. But disregarding posts just because you have a position and a survivorship bias without any logical reasoning is illogical.

Apparently, this nonsense costs you 3 years of jail.

And for the record, I haven’t received a single rebuttal on the n number of allegations I have made. Not a single rebuttal.

5 Likes

And I wasn’t planning on revealing this but here goes

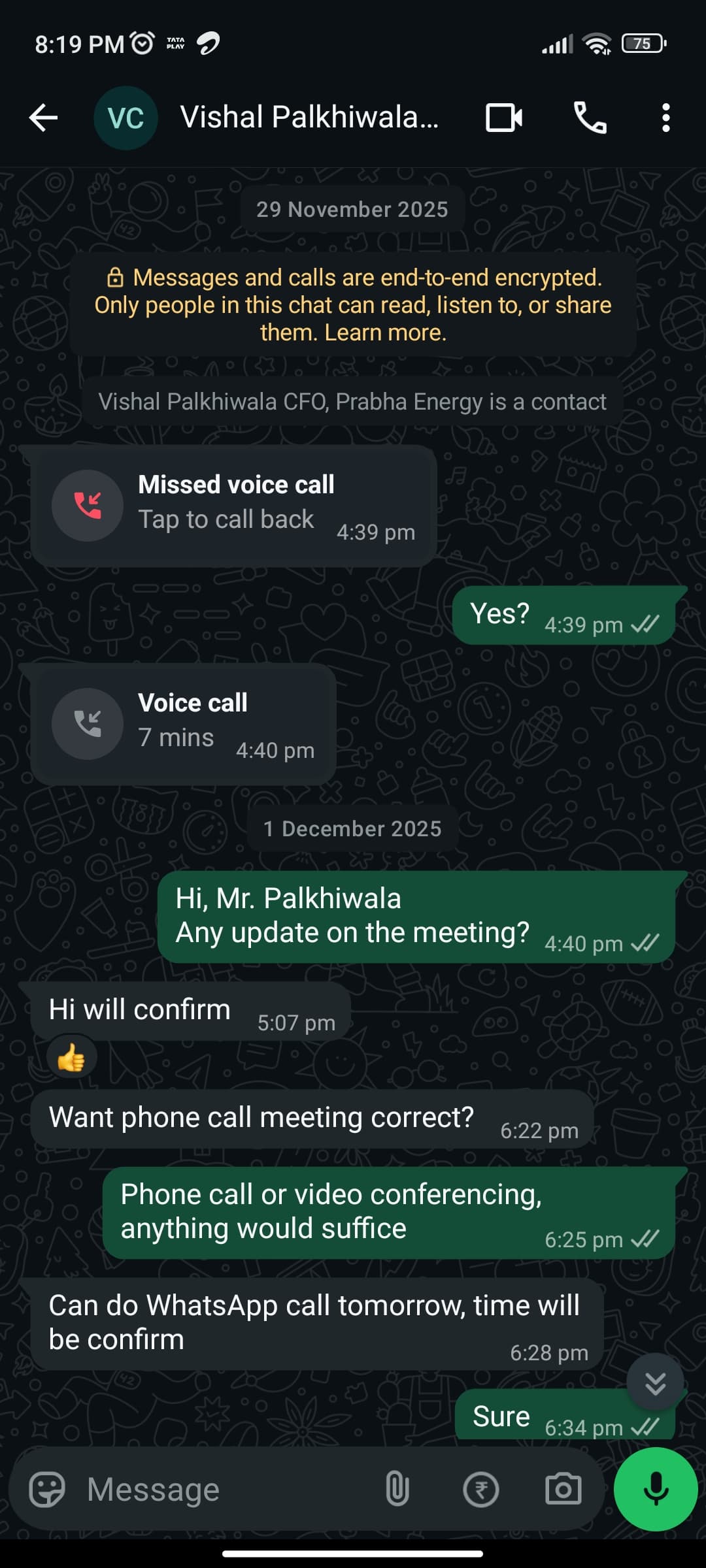

When I first threatened to file with NFRA, the CFO of Prabha Energy, Mr. Vishal Palkhiwala, tracked me down, somehow got my number, called me, and insisted on a phone call with the top management.

Then as you can see, a WhatsApp voice call that lasted 30 minutes was with the CFO of Deep Industries Mr. Rohan Shah.

We had a fun talk where I raised my points, he answered, but the answers were not satisfactory. Now I know anything that I quote from that call will be hearsay but Rohan Shah, CFO of Deep Industries told me that nothing in the report is factually wrong. Period. We exchanged pleasantries and he hung up.

When was the last time you saw the management of a 3000 crore company calling a random dude (I don’t even know how they got my number) over a report he threatened to file. There’s no smoke without fire.

But sure, ignore my “ramblings”, ignore my “nonsense”. It’s not my money on the line. If you want to invest in a company with shady accounting practices and whose auditor is not independent and will sign his father’s will if the management asked to do so, be my guest!

17 Likes

I hope you can take this with an open mind.

This forum is a space where people collaborate and share their understanding.

When something truly helps others, appreciation naturally follows, there’s no need to seek it.

Trying to prove a point here rarely leads anywhere meaningful.

Everyone here brings their own experience, so it’s worth remembering that no one is naive.

If your post didn’t receive the kind of response you expected, it might help to reflect on why that was,

especially if appreciation was what you were hoping for.

Through reflection, you might find the clarity you’re looking for.

And please, don’t take any of this personally.We’re all learning and sharing from the space we’re in.

4 Likes

It was not appreciation I was hoping for.

I just didn’t like that no one, not a single user questioned my thesis, raised actual logical points against my allegations yet dismissed them as “nonsense”. How does that work?

If they had proven with numbers, with facts why my allegation is wrong, I would have happily agreed. I would have been ecstatic.

But statements like these, when I have been nothing but respectful irks me. Did he specify why my points were ramblings? No

He just wants others to believe that these are ramblings? Why? Because he said so.

No questions asked.

This was what changed me. It was all fun and games before this. But he called me a naysayer while all I was doing was for his own interest.

Anyways I am done. For real this time. I couldn’t care less if Deep goes 100 x from now or becomes a case study in CA Student’s study material.

Peace out

6 Likes

My 2 cents.

Most people from non-finance background may not have the skill set required to respond to your points in either positive way or negative. Hence keeping silent, when we don’t add value to the discussion is quite normal and expected.

Your posts did add value to the whole discussion, at the cost of some repetition ;)

Human brain loves repitition of good news and wants bad news to be muted. We have to make peace with it. Appreciate your inputs.

15 Likes

Sometimes, the wisest response is no response at all. When faced with someone driven more by lofty ideals rather than reality, responding only leads to endless arguments and accusations, waste of time few of us can afford. Silence, in such moments, is true wisdom.

1 Like

To update everyone

In order to “walk the talk” and prove the utmost confidence I have in my analysis, please find the official letter to the Board of Directors, Deep Industries Ltd. via their email- cs@deepindustries.com

To: The Board of Directors / Independent Directors, c/o: The Company Secretary, Deep Industries Limited.

Reference: Compliance with Section 129, Section 134(5), and Liability under Section 448 read with Section 447 of the Companies Act, 2013.

Dear Members of the Board,

I am writing to you as an independent analyst acting in the public interest. I am submitting this representation to caution the Board regarding the statutory certifications and the Directors’ Responsibility Statement to included in the Annual Report of financial year ended 2024-25.

The Statutory Requirement: Under Section 129(1) of the Companies Act, 2013, the financial statements must comply with the accounting standards. Furthermore, under Section 134(5)(a), the Directors must affirmatively state that “applicable accounting standards had been followed.”

Evidence of Material Non-Compliance: My forensic analysis (attached) identifies that the Company’s financial statements materially deviate from the Indian Accounting Standards (Ind AS):

Violation of Ind AS 109: Non-provisioning of Expected Credit Loss (ECL) on ~₹405 Cr of unverified receivables .

Violation of Ind AS 103: Inflation of Capital Reserve by ₹256.07 Cr via incorrect inventory valuation .

Violation of Ind AS 36: Failure to disclose Goodwill allocation and impairment assumptions .

- Legal Implications (Section 448 & 447): I draw the Board’s specific attention to Section 448 of the Companies Act, 2013 (“Punishment for False Statement”). This section states that if any officer makes a statement in any return, report, or financial statement that is false in any material particular, or omits any material fact, they shall be liable under Section 447.

Therefore:

Section 129(7): Any contravention of the accounting standards under Section 129 renders the Directors liable to imprisonment and fines.

Section 448: If the Board approves financial statements claiming compliance with Ind AS despite knowing of these material deviations, such an act may constitute a “False Statement” under Section 448.

Section 447: This triggers the penal provisions for Fraud, which includes imprisonment for a term of not less than 6 months (up to 10 years) and a fine of up to three times the amount involved.

I urge the Board to independently review these non-compliances and restate the financial statements to avoid attracting personal liability under the aforementioned sections.

Thanks & Regards

Kautuk Yemdey

Copy to:

Chairperson, National Financial Reporting Authority (NFRA)

Chairman, Securities and Exchange Board of India (SEBI)

Investor Services, Bombay Stock Exchange Limited (BSE)

Let the truth prevail

2 Likes

To mark my 51st post, a letter to the Nodal Officer of the Vigilance Mechanism of the company and the Audit Committee therein, sent to:

nodalofficer@deepindustries.com

cs@deepindustries.com

To: The Chairman of the Audit Committee & Independent Directors, c/o: The Company Secretary, Deep Industries Limited.

Reference: Material Irregularities in Financial Reporting / Violation of Regulation 33 of the SEBI (LODR) Regulations.

Dear Sir/Madam,

I am writing to you in your capacity as the guardian of the governance of the company to formally report significant accounting irregularities and material misstatements in the financial records of Deep Industries Ltd.

- Nature of Complaint & Regulatory Obligations: In accordance with Section 177 of the Companies Act, 2013, I am submitting a detailed forensic analysis highlighting discrepancies that constitute potential violations of Regulation 33 (Financial Results).

Furthermore, I draw your specific attention to Regulation 18(3) read with Part C of Schedule II of the SEBI (Listing Obligations & Disclosure Reauirements) Regulations, which explicitly mandates the Audit Committee to review:Major accounting entries involving estimates based on the exercise of judgment by management.

Significant adjustments made in the financial statements arising out of audit findings.

Related party transactions.

My analysis suggests that the financial statements currently approved by the Board may fail these tests of scrutiny.

- Key Discrepancies Identified: My forensic review indicates:

Overstatement of Capital Reserve: Inflation of Capital Reserve by ₹256.07 Crores arising from the recognition of obsolete inventory at book value rather than fair value in violation of Ind AS 103.

Overstatement of Trade Receivables: Material overstatement of assets due to non-provisioning of Expected Credit Loss (ECL) on approximately ₹405.77 Crores of unverified, long-outstanding receivables in violation of Ind AS 109.

Disclosure Failures: Material non-compliance with Ind AS 36 regarding Goodwill impairment testing assumptions and Ind AS 24 regarding the transparency of Related Party Transactions.

Improper Audit Opinion: Issuance of an unmodified opinion with an “Emphasis of Matter” regarding unverified receivables instead of the required Qualified Opinion under SA 705 and SA 706.- Conflict of Interest & Demand for Independent Review: I note that the designated Nodal Officer for the Vigil Mechanism is a member of the Executive Management/Promoter Group. Given that these allegations involve financial reporting under the current management, I explicitly request that this report be placed directly before the Independent Directors and the Chairman of the Audit Committee for an unbiased investigation, bypassing executive management.

I request an acknowledgment of this complaint within 48 hours and a confirmation that it has been tabled before the Audit Committee as per your duties under Regulation 18. Failure to act on this report may be construed as “Willful Negligence” under the Companies Act & SEBI Regulations therein.

Thanks & Regards

Kautuk Yemdey

CC:

Chairperson, National Financial Reporting Authority (NFRA)

Chairman, Securities and Exchange Board of India (SEBI)

Investor Services, Bombay Stock Exchange Limited (BSE)

How this materially differs from the above email: This particular email is for the supposedly Independent Directors and Audit Committee who supposedly govern the company in “shareholder’s interest”. By failure to acknowledge this whistleblower complaint, the independent directors and the audit committee could be scrutinized for gross negligence of their duties as specified by SEBI.

7 Likes

Explain one thing - How is there an overstatement of capital reserve by 256cr arising from obsolete inventory recognition when they’ve already taken write-off in income statement and thus reducing capital reserves by the similar number in the FY25.

There’s an increase of 377cr in reserves from FY24 to FY25. That’s mostly because of old receivables of Kandla and dolphin shipping and nothing related to inventory.

Also, at the end of all this, even if they do write-offs of old recievables, it will be a non-cash one time entry. Nothing to do with cash flows, and business fundamentals.

1-2 years needed to be given to the management to see if there’s any chance of recovery. It is your opinion that “Since receivables are more than 3 years old, it suggests their non-recoveribility and they should be immediately written off since”. You don’t have the details which the company has

“The value of a company is the present value of all future cash flows.” Since, all your ‘accusations’ have zero impact on cash flows, no value is reduced for Deep.

And on following accounting standards to the T, you’ll find hundreds if not thousands of companies doing something/ taking advantage of something which is the grey area.

If they were doing it to harm minority shareholders and actual cash flows involved, then it would have warranted a serious look. But if they’re doing it for the benefit of shareholders, let’s say to be able to bid for bigger tenders, then I’m all okay with it and so would most of minority investors.

That’s what I have been trying to say since the very begininning. No cash is actually involved in all this and no harm to minority shareholders is there in all this. That’s why the terms " don’t care" and “ramblings” which are harsh but after 51 posts one doesn’t get it, then it comes out a bit harsh.

One can use all the smart jargon of IND-AS and long paragraphs from similar cases etc etc.

But coming down to it, the basics are simple. 2 cr paid for acquisition, receivables need time to be verified for recoveribility and in worst case scenario there’s no cash impact, making all this redundant to the Deep investment thesis!

It’s not bias that makes me call this useless. Actually arguing this is making me more emotionally biased to Deep unnecesaarily

2 Likes

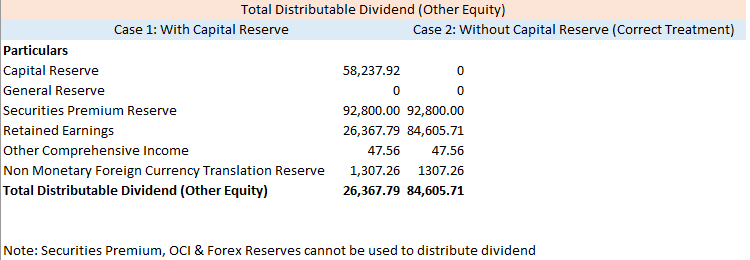

The write offs (extraordinary item) were from retained earnings and not Capital Reserve. There still exists substantial capital reserve. While I acknowledge that after the write offs, the “Other Equity” as a whole remains same, that doesn’t mean that the line item “Capital Reserve” is not misstated. Now, let us analyze why this blunder is actually destructive for minority shareholders.

Capital Reserve is a restricted reserve. Dividends, as per Section 123 of the Companies Act, 2013 cannot be paid out of restricted reserves (including capital reserves). So, keeping this inflated inventory and receivables on the balance sheet in the form of capital reserves reduces the total dividend that the company can distribute in the future by Rs. 400 crores in aggregate.

So, this accounting treatment, contrary to your belief is even worse for minority shareholders as it restricts the right of dividend.

If you read the NFRA precedent case law, management optimism or time needed is NOT an excuse for not booking provisions for receivables. In the matter of Vikas Proppant, NFRA clearly established that receivables outstanding for more than 3 years arising out of insolvency process warrant LIFETIME ECL irrespective of the current verification status or management optimism.

I agreed to this point long back. There is no cash impact. But just because there is no cash impact does not mean you do not follow accounting standards. Accounting does not care about whether cash impact exists or not.

In fact, I have never once said that Deep industries as a stock is under/overvalued. My posts have always been purely based on accounting and auditing. And hence I am least bothered about Deep Industries as a stock investment. I do not care about present value of future cash flows. What I care about, is proper financial reporting. Period. Nothing more, nothing less.

That’s like justifying I committed murder because thousands other commit murder. Just because hundreds and thousands take advantage of grey accounting, does not justify the company doing so as well. And this isn’t even a “grey” area or a subjective management “estimate”. It’s just a pure violation.

Dolphin was acquired in FY 2022. How much more time one needs? And for the record, if the management cannot verify receivables, it shouldn’t even have recognized an ASSET in the first place. Because it does not meet the definition of asset (Resource CONTROLLED by an entity, from which Future Economic benefits are expected to flow to the entity)

Summary:

No “real”, “non-cash” or “economic impacts” for shareholder does not justify improper accounting treatment because accounting doesn’t care about these things.

And even if such expenses are non-cash, so what? Since this thread mentions Buffett or Munger, let me quote them as well. Both of them said that non-cash expenses like ESOP Expense, Depreciation, Impairment of Assets, Write-offs, though non-cash are real business expenses. “What do you think they are? Gifts from shareholders?” - Warren E. Buffett (when asked whether ESOP, Non-Cash expenses like Impairment or inventory write offs are real, year is unknown)

By the same non-cash logic, even depreciation has no impact on cash flows. So let us ignore depreciation too then? In fact, let us just ignore accrual basis of accounting and follow cash system

Non cash does NOT mean Non existent, Non real Expense

3 Likes

Case 1: Company’s accounting treatment

Case 2: Correct Accounting Treatment

So to respectfully refute your claim that this doesn’t negatively affect minority shareholders, it does. The amount of distributable dividend reduces significantly because of this incorrect accounting treatment.

Note: Correct treatment should be construed as correct classification and not mesasurement.

Disc: This illustration is only to show how classification (& not measurement) of capital reserves/retained earnings affect dividend. The retained earning figure will be less because Ind AS tells me to record acquired asset at fair value (Fair value of inventory would be NIL & Receivables would be much much less than the carrying amount of 420 crores)

2 Likes

From the above posts you have really gone Deep into Deep Industries and looked at the company from quite a lot dimensions.

First through the lens of Bernard’s Law for possible accounting fraud to actual statements of Trade Receivables and impact of non-provisining of ECL. I am a newbie and learned a lot. Thanks a lot.

Since you have raised the question of accounting fraud and the company has already failed the Bernard Test. Could you also perform the M-Score test and revalidate the results. Give detailed analysis of the M-Score if possible. Asking this to you cause I found that you are one of the few who shares the method of deduction.

2 Likes

I guess you meant Benford’s Law. The company passed the Benford’s law. (Test statistic 13 was less than critical value 15)

I’d rather use the phrase, non-compliance with Ind AS than the F-word.

Quite frankly, I am not really well versed with the M-Score Test. But yeah I mean a couple of Google searches can sure help. Regardless, I really don’t have the motivation to research further. I am just open to answering questions on existing allegations.

Glad I could help!

3 Likes

This is precisely the disconnect. You don’t understand the business or fundamentals and clearly are not interested in making any efforts in doing so, yet you flood the thread with posts in a forum where most folks try to understand the business and the fundamentals of a company and then invest in the stock in the hope of making money.

Your posts would be very suitable if this was a forum for CA/CS. Or even if your posts were made in a separate thread on VP where you did your accounting checks and gave your opinion on accounting standards followed by various companies and issues with them. I am sure forum members would appreciate that. There are other forensics related threads that get traction on VP. Do consider doing that instead of hijacking a company thread highlighting a matter that most Boarders don’t connect with or think is important.

Having understood the business, I am 100% sure that the recent issue of an ONGC well managed by Deep getting blown-up is 10x more material to its future prospects than the impact of your accounting allegations. Yet how many posts do you see discussing that vs your accounting related posts? The funny thing is you understand that (You’ve mentioned that many times), yet continue to make posts on a subject which would be more suited to other forums or at least in a separate thread.

Finally, would like to say, the work that you have done is important, even for an investor. For example, the nuance that you highlighted about Deep’s dividend paying capacity getting impaired due to the wrong equity head being written off was very interesting. If true, it has implications that an investor should be aware of.

Its just that in the hierarchy of things that matter for an investor, the concerns you have raised don’t rank very high. Said differently, there are many other business concerns which rank way higher. And therefore they don’t merit a thread being hijacked by said concerns just because for you, accounting sanctity is everything and you couldn’t care less about the business or fundamentals. By not recognising that point, you are being insensitive to the forum’s ethos. That’s the limited point I want to make.

I hope you start a new thread where you highlight interesting cases of accounting lapses or frauds. I would be a keen reader if any of those posts pertain to companies I am interested in.

23 Likes

All members are requested to not repeat and post the same findings/opinions, and Also refrain from getting into 1:1 arguments in public. One can flag the posts if found irrelevant and leave it to mods review.

14 Likes

Can you send the same Deep Ind for clarification and to NSE if they are not responding. Couple of years back I sent NSE about not getting a clarification. I got the reply from Company in few days and as I saw the chain of email, from NSE they had sent it to the Company, asking them reply to that query.

2 Likes