Oil prices at 4 years low.

Thank God I didn’t join this community two years ago. Otherwise, I would have gotten confused by all the discussions and sold my investment of around 9,000 shares long before it became more than 3×! I don’t know much accounting. I just saw that the company was profitable, sales were growing, and the business was expanding — that’s why I invested. After reading the discussions here, it feels true that money isn’t always made by overthinking. If the company and its business are reasonably good, just buy and stay quietly invested — the returns come on their own! However, this is my personal opinion. I truly respect all the community members’ opinions.

14 Likes

If investing was just about numbers then all accountants would have been millionaries,

its the risk taking abilities and rosk mangement which ultimately pays you..

3 Likes

For individual investors I don’t think these things matter but if you are institutional investor and investing in crores in one stock so Ideally they have to do all these forensic analysis to determine risk metrics. A different scene is going on now a days due to SIP inflows even many institutions despite knowing many red/orange flags they keep burning money. Ultimately it’s retail investors money ![]()

When a stock you own drops 25% it’s an “opportunity”. When it drops 10% more you call the CEO to verify the thesis and buy more. When it drops 10% more you get annoyed insiders aren’t buying. When it drops 10% more you sell your stock to the investors that are going to make money on the stock.

Think about all the stocks you said you would buy if they ever dropped to a certain price.

When the stock price finally drops, you quickly pivot, “ehh.. maybe I’ll buy it 10% lower”. You do this three more times.

Watchlist companies = a list of stocks you tell yourself you would buy if they drop, but when they do drop you never buy them. You just watch them.

Then the stock bottoms and starts to rise. In an instant you mentally shift from “fear of loss” to “fear of missing out” and you take offers in the stock chasing it 30% higher to get a position.

Stock prices pull on our emotions like a dog on a leash. We all suffer from stock prices driving the narrative in our mind.

The truth is when a stock is down, many times nothing fundamental has changed. It’s simply the market sentiment flipping or a large holder selling.

When a stock moves up, many times the business really hasn’t changed. Investors just got more excited about the story.

When stocks go up everyone is willing to look the other way on almost any issue. When a stock is rising investors pull out a telescope from the closet, climb onto the roof, and look way out into the future to justify paying a higher valuation today.

15 Likes

With all due respect, an appreciation in the stock price does not justify questionable accounting practices.

Enron grew 10 times in 3 years before 2001. It’s stock price increased multifold by at least 5 times before it declared bankruptcy and now what is known as the biggest accounting scandal on Wall Street .

Satyam Computers was the fifth biggest company in India in terms of market capitalisation before Mr. Ramalinga Raju wrote to his board on how he inflated his books.

I am by no means saying that Deep is the next Enron or the next Satyam. Definitely not. But shares becoming more than 3x is absolutely not a justification for not questioning the management.

Skepticism is a competitive advantage. Sales are growing; how are they growing? Are the reasons provided by management justified for a 60% YOY growth performance? Stock is undervalued? Why is it undervalued? Management claims that they are the most experienced in this sector because they have 30 years of experience. If this is really such a high growing high margins sector, why are others not foraying into it. I didn’t see names of any competitors in discussions above. That is not how economics work.

It’s not about “overthinking”. It’s about what’s right and what’s wrong. “It’s about sending a message” - Joker (The Dark Knight)

I would really like others to find flaws in my report and not justify their holdings because the stock grew 3 times in the last couple of years.

Again, I say this with due respect and I apologize if you found the tone to be rude.

This is risk management. I am raising questions that I feel others missed so existing investors can better manage risks. That’s it

Objection, relevance?

P.S. I know I said that it would be the last you hear from me on this thread. But desperate times = desperate measures. I will not add any new thesis though.

4 Likes

Excellent post-mortem!

But I’ll repeat what I’ve said earlier — one doesn’t need to over-analyze or dig endlessly into every micro-detail to “make money in the market.” Investing, at its core, is quite simple. People make it look complicated because they’re either chasing intellectual satisfaction or trying to showcase analytical depth. But wealth isn’t built by collecting spreadsheets — it’s built by taking decisions, taking risks, and staying in the trend. Some people believe that great investing requires them to behave like forensic scientists — but history proves otherwise. Investing rewards clarity, not complexity.

Even legends didn’t get rich by demanding spotless companies.

Warren Buffett himself bought into businesses with risks, regulatory uncertainties, and governance questions — not because they were perfect, but because the risk-reward ratio was attractive. He didn’t wait for confirmation from every auditor on the planet. He looked at value, momentum, price, and business potential — and he acted.

And if someone wants to argue about compliance and moral purity, then they should study the journey of Rakesh Jhunjhunwala — The Big Bull. He invested in companies that weren’t PR-friendly, weren’t polished, and definitely weren’t flawless. Yet, he built wealth beyond imagination. Why? Because he understood one thing — “markets reward risk-takers, not spectators.”

Now let’s talk about risk management - Risk management, in my view, is not merely about balance sheets, compliance reports, or forensic accounting. It’s more about “accepting uncertainty and being willing to put your money on the table.” It’s about conviction. And no matter how perfect a company looks — pristine numbers, flawless compliance, squeaky-clean governance — zero risk simply means zero opportunity. Markets reward those who can live with calculated discomfort.

Now, regarding the so-called “potential non-compliance” being discussed — even ignoring it is a risk which isn’t everyone’s cup of tea! I genuinely believe that if someone truly wants to compound their money and build real wealth, they don’t enter the market to moral-police corporate behaviour or lead a crusade for ethical reform. If that’s someone’s purpose, I respect it — but it’s not mine. As far as I’m concerned, I’m brutally practical and I’m here for one reason, and one reason only: to grow my capital. If a stock is rising, enter based on position sizing capacity, set a stop-loss, manage downside, and ride the trend as long as it lasts because, ultimately, the market pays for performance, not perfection - Price first. Profit first. Noise later - that’s it. Don’t lose sleep over compliance gossip - because in the end, portfolios don’t care about virtue — they care about returns.

I don’t care what management whispers behind closed doors.

I care what the chart whispers on the screen.

I don’t judge companies by perfection.

I judge them by returns.

7 Likes

Haha I like your writing style.

Well according to your example of Mr. Buffett, those who think they can think like Buffett and make it big like him should ignore governance issues. I don’t think I am even worthy of saying his name and hence look at these things.

The two examples you gave, Mr. Buffett and Mr. Jhunjhunwala, are just that, examples. Exceptions. The sample size is too low.

What about all of the millions of investors who lost their life savings by investing in Companies like Enron, WorldCom, Satyam, Gensol, etc I can go on and on

Ignoring corporate governance just because one Buffett or One Jhunjhunwala made it big is not sound logic according to my humble opinion. Basing everything on what these individuals have done is not ideal.

The same Buffett talks about how the average Joe (people like me) should forget about analyzing companies and just buy a low cost ETF. If we were to follow everything Buffett said, then we should close down the ValuePickr forum. All of us here are average Joes.

In fact here is what I propose:

After taking into account the possible governance issues, how many of the existing investors increased their risk premium factor? How many demanded a higher margin of safety because of these issues? How many reassessed their holdings based on new findings, deciding whether the valuation is appropriate considering the new issues that came up?

This according to me is risk management.

I am not here to “make money in the market”. I am just an average Joe with a passion for accounting. That’s it. I would have zero regrets if Deep goes 100x from here on. Zero. I do this out of passion.

I don’t judge companies by returns. Returns are manipulated. They are deceptive. Returns are based on emotions.

I judge them by numbers. Because numbers are cold facts. No emotional bias, no confirmation bias. Just cold hearted facts.

4 Likes

And since you talked about Buffett, here’s what he has to say about corporate governance:

“I can’t afford the operation, but would you accept a small payment to touch up the x-rays?” – Warren E. Buffett

This is an extract from his widely read annual letters to investors (year is unknown)

"The letter described a conversation between a seriously ill patient and his doctor, just after an x-ray revealed the bad news about his condition. Rather than accepting the diagnosis of his deteriorating health, the patient immediately responded to the dreadful news by asking the doctor to simply touch up the x-rays. Buffett uses this story to warn investors about companies that try to hide the truth about their deteriorating business’s economic health by touching up the financial statements. Buffett then prophetically adds, “In the long run, however, trouble awaits managements that paper over operating problems with accounting maneuvers. Eventually, managements of this kind achieve the same result as the seriously-ill patient.” (Extract from Financial Shenanigans by Howard Schilit)

1 Like

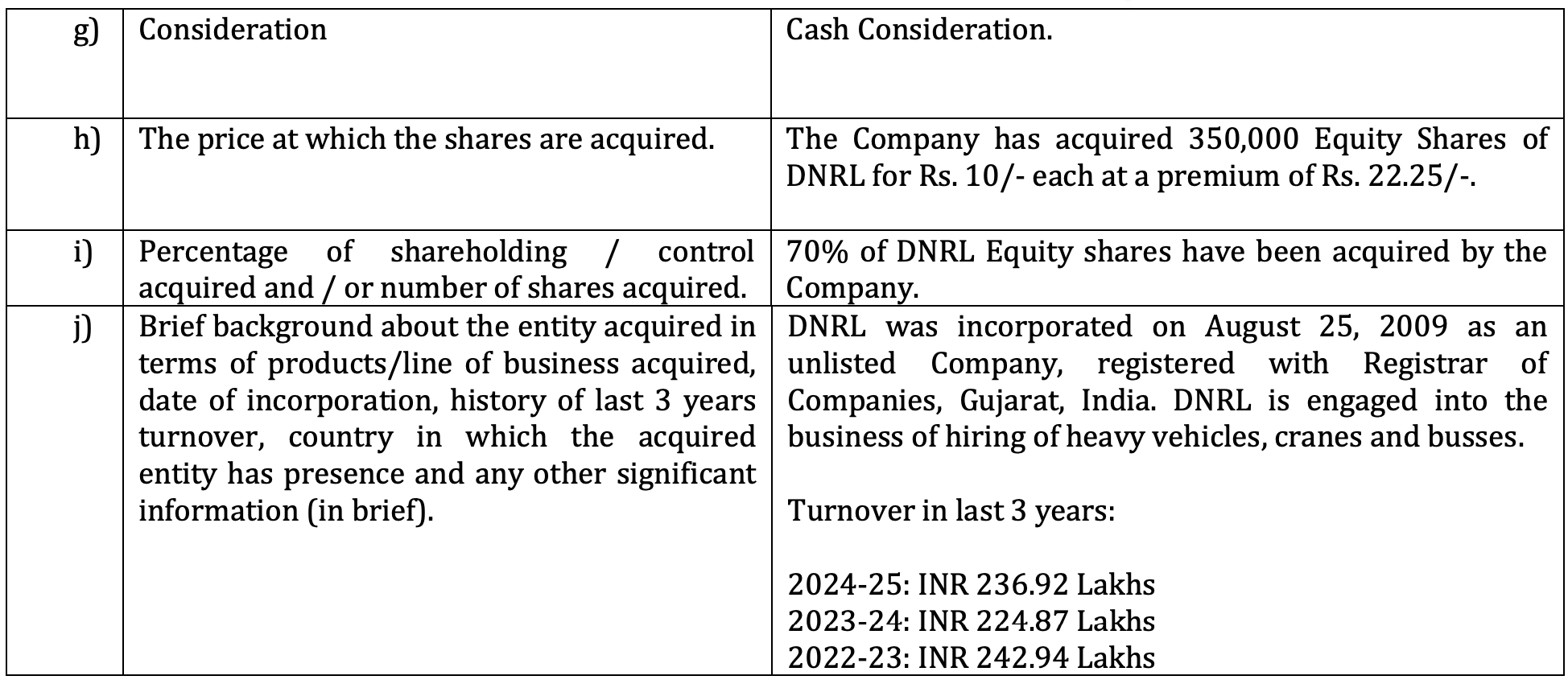

Another acquisition done by way of Shares purchase of Deep Natural resource (at Rs 32.25 per share). This company is engaged in busness hiring of heavy vehicles, cranes and busses. These are critical for carrying out drilling and other exploration services.

4 Likes

-

Rohan shah said in interviw 4 months back, P&L Affect due to TAX benefit in Future.

-

in ACCOUNTING term Kandla is a 100% subsidairy of the deep aquire via NCLT, writte off the Inventory & receivables heat the P&L for a TAX benefit in future But subsidiary not benefit becuase its a subsidairy so here deep trying to potential merger with kandla for a tax benefit, I am not a Charted maybe i am worng, any one charted here please verify this

-

One more thing Investor forgot the why Deep Aquired the Kandla, As per the Managegment KANDLA Aquired for the MARGIN EXPENTION almost 2% so here we compare FY 25 REVANUE - 576 CR so 2% margin Expention Benefit the almost 11 cr so this is a previous year but 2 cr aquisition cost save roughly 10cr so this is a good Aquisition as per my understanding.

-

Disc : I am invested.

1 Like

They have booked interest income in PnL (of ~12Cr). But in the Cash Flow from Financing Activities for FY25, they have just booked ~8.1Cr of Interest Received!

And surprisingly, on Prabha’s Consolidated CF statement, under CFF: The cash interest paid by the company is just 15Lakhs for FY25.

I am not able to understand how this transaction is working out!

You should also look into it.

And even if they are capitalizing the interest costs under CWIP, still the interest payment needs to be made in Cash to DIL.

Am I missing something in this equation?

To update investors, i have exited completely. Didn’t get any reply on RPT iro direct calls. Company likely to post VG results in future and can create wealth for inv, but for me CG is negative, so exited position with ab avge returns..

2 Likes

With a deep sense of righteousness and a mildly unhealthy passion for accounting and auditing ethics - dedicated to Nate Anderson, Founder of Hindenburg Research.

Deep Industries Final Report.pdf (1.3 MB)

Please read important disclaimer on page 2.

5 Likes

This was being operated by Deep industries. Could be a reason why the stock was down more than 4% today.

The Prices of Natural gas falling is also an anti-thesis pointer for DIL as the 1400Cr contact is a variable pay one dependent on the price of Natural Gas market prices (although that prices is in Indian Gas Prices) but still I feel that if global prices fall this much then Deep’s Revenues, realization and hence margins might also fall !

1 Like

How would this mishap affect the PEC contract? That remains a question to ask the management during Q3 concall.

According to first article, No equipment failure occurred , so maybe it won’t affect the contract much. Let’s see

An actual worry for real investors of the company, instead of all the ramblings above on non-issues.

Also, lower oil prices and prospects of even lower prices along with the extreme bearish sentiments in the broader market is dragging the share price down even though next 2 years 35% growth seems secured.

Welspun corp reported wonderful numbers with extremely strong orderbook. Yet stock price is now at 766 from 995.

The effect of Deep operating in O&G industry may keep its valuations compressed even if oil prices don’t affect it, since India is in a big energy production deficit and Efforts and policies are there to increase it substantially, thus keeping demand strong for Deep over medium to long term.

Maybe the market will reward it’s consistent performance once current bearish sentiment turns around or maybe not.. That’s why this game is such “fun”

4 Likes

I am also in the same boat. No matter where global oil prices go, India has no other option than to increase focus on domestic exploration and production. Can’t rely on Russia, US, Venezuela or anyone else in these troubled times.

1 Like

NFRA Order No.: NF-23/14/2022 dated 12th April 2023

2023041290.pdf (6.7 MB)

In the Matter of M/s ASRMP & Co (‘Firm’ hereafter), statutory auditors of Coffee Day Global Limited (‘CDGL’ or ‘the company’ hereafter)

"They failed to evaluate their potential conflict of interest and failed to maintain their

independence from CDGL by having audit and non-audit relationships with a large number

of Coffee Day Group companies and the promoters’ family members".

Ring a bell? My first post on Deep Industries was how the Savla family contributed more than 45% of the total audit fees received by the auditors in the listed audit space citing serious concerns on the independence of the auditor.

"..performed audit in a perfunctory manner resulting in

non-reporting of misstatement of Rs 132.37 crores in the consolidated financial statements. "

Capital Reserve is overstated by Rs. 256 crores due to incorrect treatment of inventory as per Ind AS 103 (Business Combinations). Also as per the landmark judgement of NFRA in the matter of Vikas Proppant & Granite Limited dated 5th July 2024, where NFRA convicted the auditor for not providing Expected Credit Losses on receivables despite prolonged ageing and strong indicators of credit deterioration (like Insolvency), there exists an overstatement of Deep Industries’ receivable balances to the tune of Rs. 400 crores

"They failed to perform appropriate audit procedure to identify misstatement of Rs 69. 77

crores in related party disclosure relating to purchase of coffee beans from MACEL."

The company (Coffee Day) misclassified “advances to related parties” as “purchases”.

Remember this analysis? NFRA found that misrepresentation of related party disclosures (like the one between Deep & Prabha) was a fraud risk factor and ordered that this was a misrepresentation of the true nature of transactions under Ind AS 24 (Related Party Disclosures) and that the auditors should have reported the same under section 143(12) [Reporting fraud to Central Government]

Deep Industries NFRA Precedents.pdf (689.0 KB)

The above pdf establishes previous NFRA orders that relate to Deep Industries (non-provisioning of ECL, issuing improper audit opinion, impairment of goodwill allocated to subsidiaries acquired through insolvency process, lack of mandatory disclosures in financial statements, lack of external confirmation procedures to name a few)

4 Likes