Excellent result….once sentiments turn favourable towards small and mid cap….expect good upmove

https://www.bseindia.com/xml-data/corpfiling/AttachLive/9ea076dc-25f3-4812-9a8e-2ff801abd54f.pdf

Excellent result….once sentiments turn favourable towards small and mid cap….expect good upmove

https://www.bseindia.com/xml-data/corpfiling/AttachLive/9ea076dc-25f3-4812-9a8e-2ff801abd54f.pdf

Sharing few good points from concall::

Regular tender are being floated and we are regularly bidding in tenders

Bid order amount pipeline 800 Cr; conversion rate is around 30-40%

We are trying to get private clients also to reduce concentration risk.. we have been approaching to oil & gas players also for expanding our client base

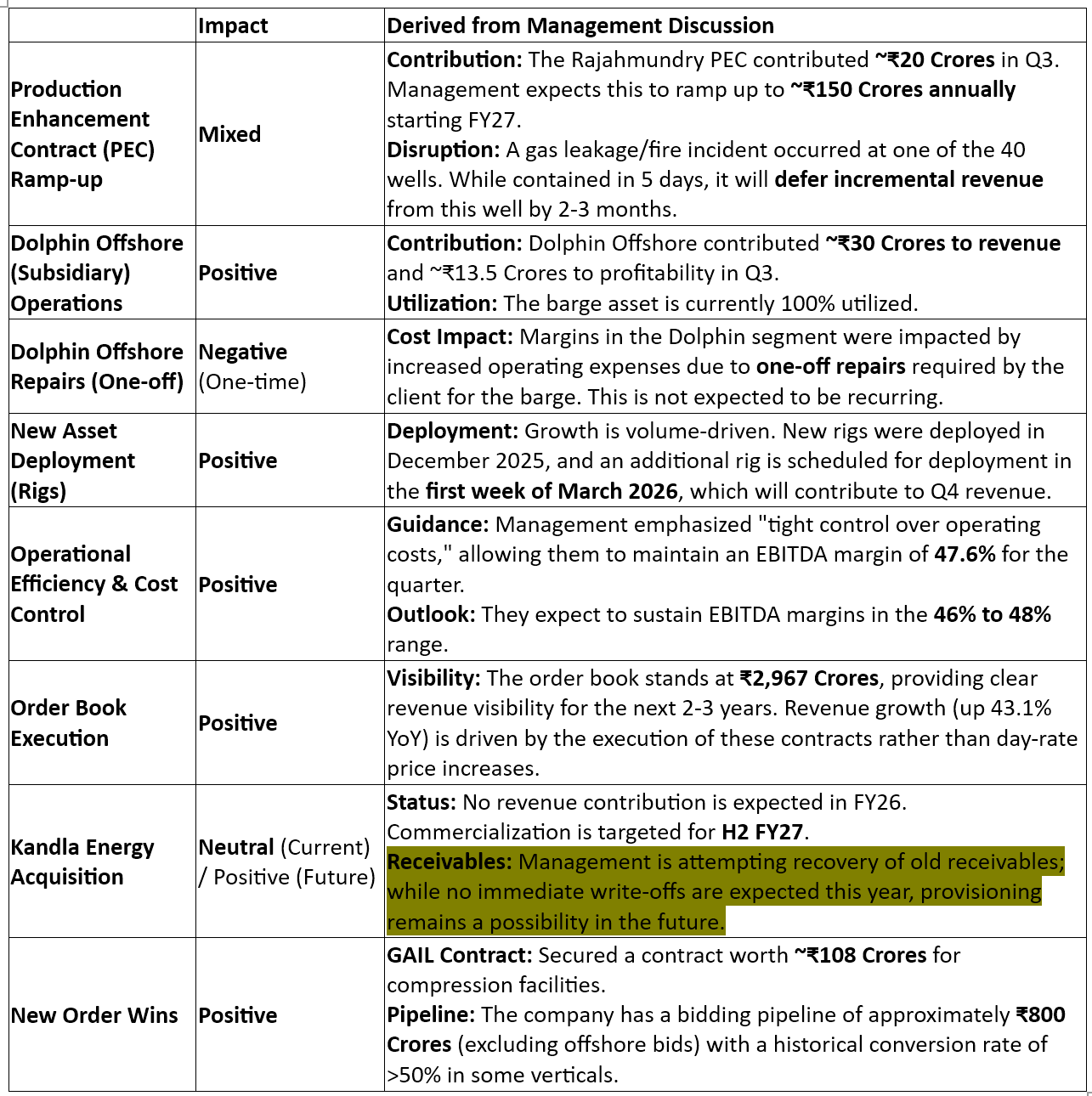

Production Enhancement Contract (PEC) Update

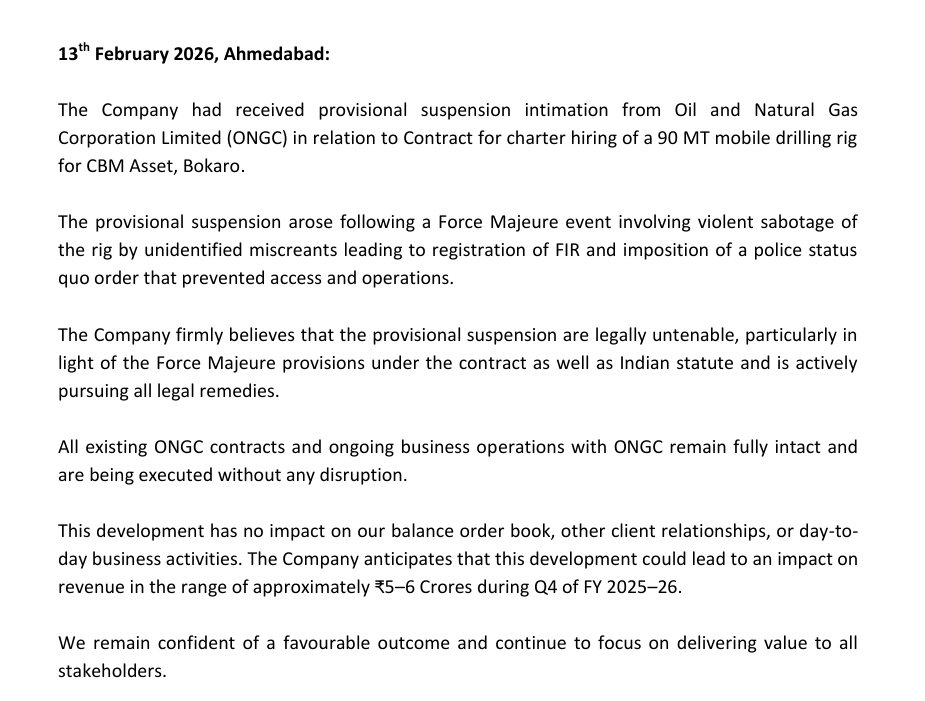

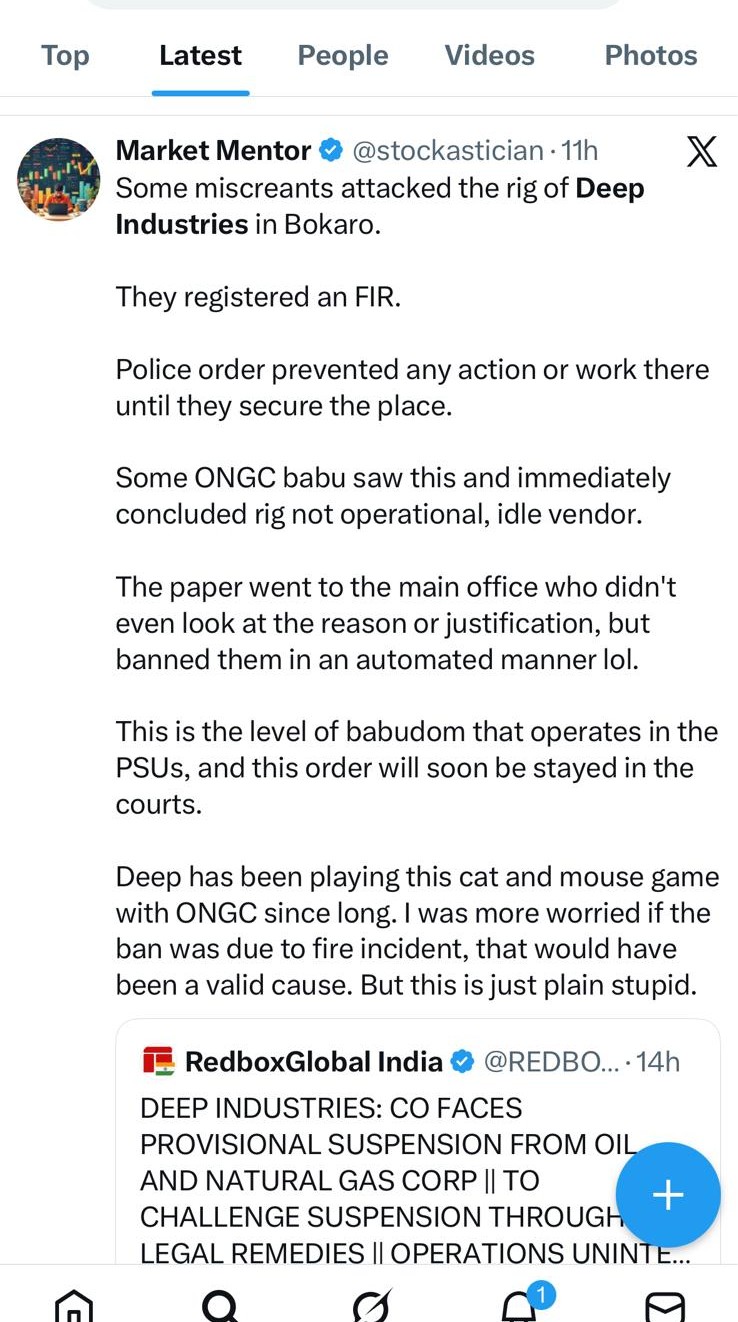

Gas leakage incident at Rajamundhary Field during drilling operations

Contained within 5 days with no casualties

Geological surprise encountered during operations

2-3 month delay expected in revenue ramp-up

Current PEC contribution: ₹20 crore this quarter

Expected annual revenue: ₹150 crore from FY27-28

Working on 40 different wells (incident affected one substantial well)

Offshore services contributing in full during quarter:

Dolphin barge: ₹30 crore revenue, ₹13.5 crore profitability

Prabha DP2 barge: ₹100 crore expected annual revenue, 100% utilized

Revenue guidance: 30-35% growth expected next year and following year

Evaluating new opportunities in carbon capture, biogas compression, hydrogen sectors

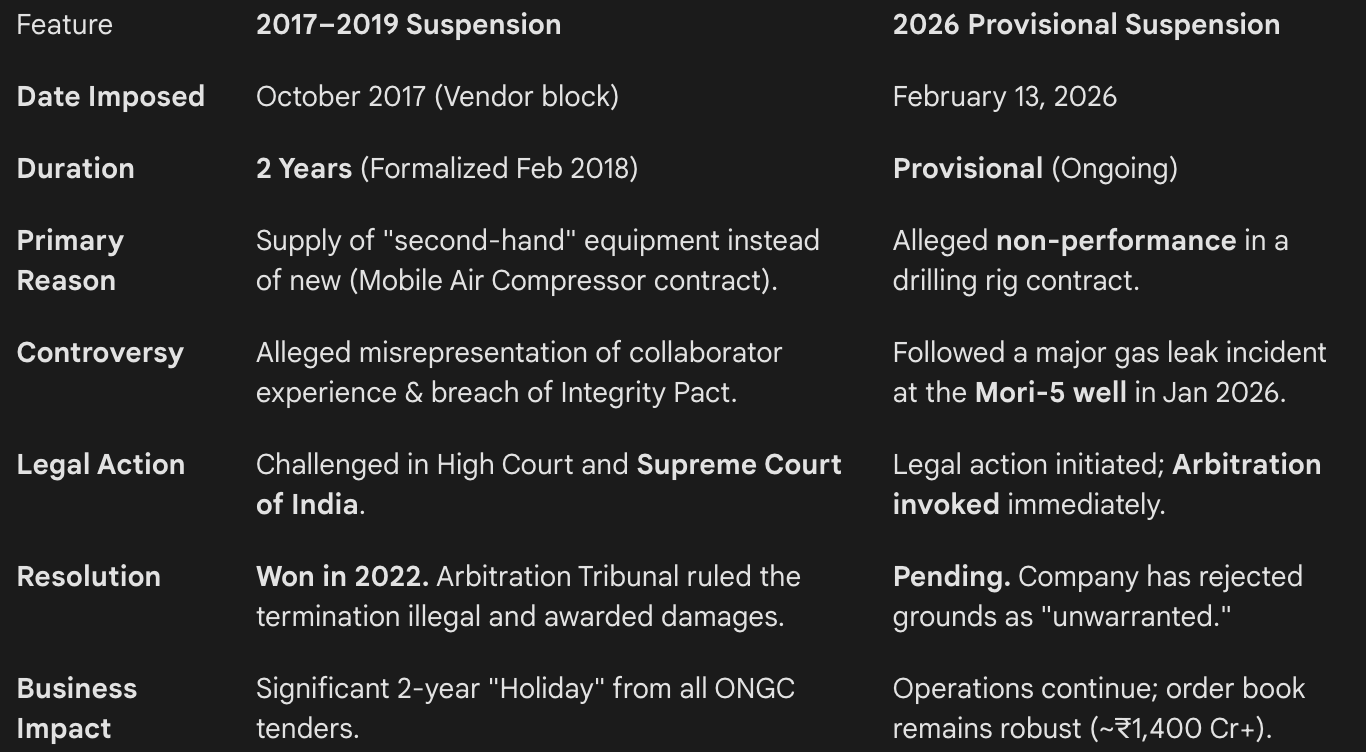

Promoters are master in dealing with PSU. They have excellent network within ONGC and know how to deal with them. Earlier also they got money against their suspension and other contract from ONGC were flowing!. I don’t see much impact considering growth in revenue and profit

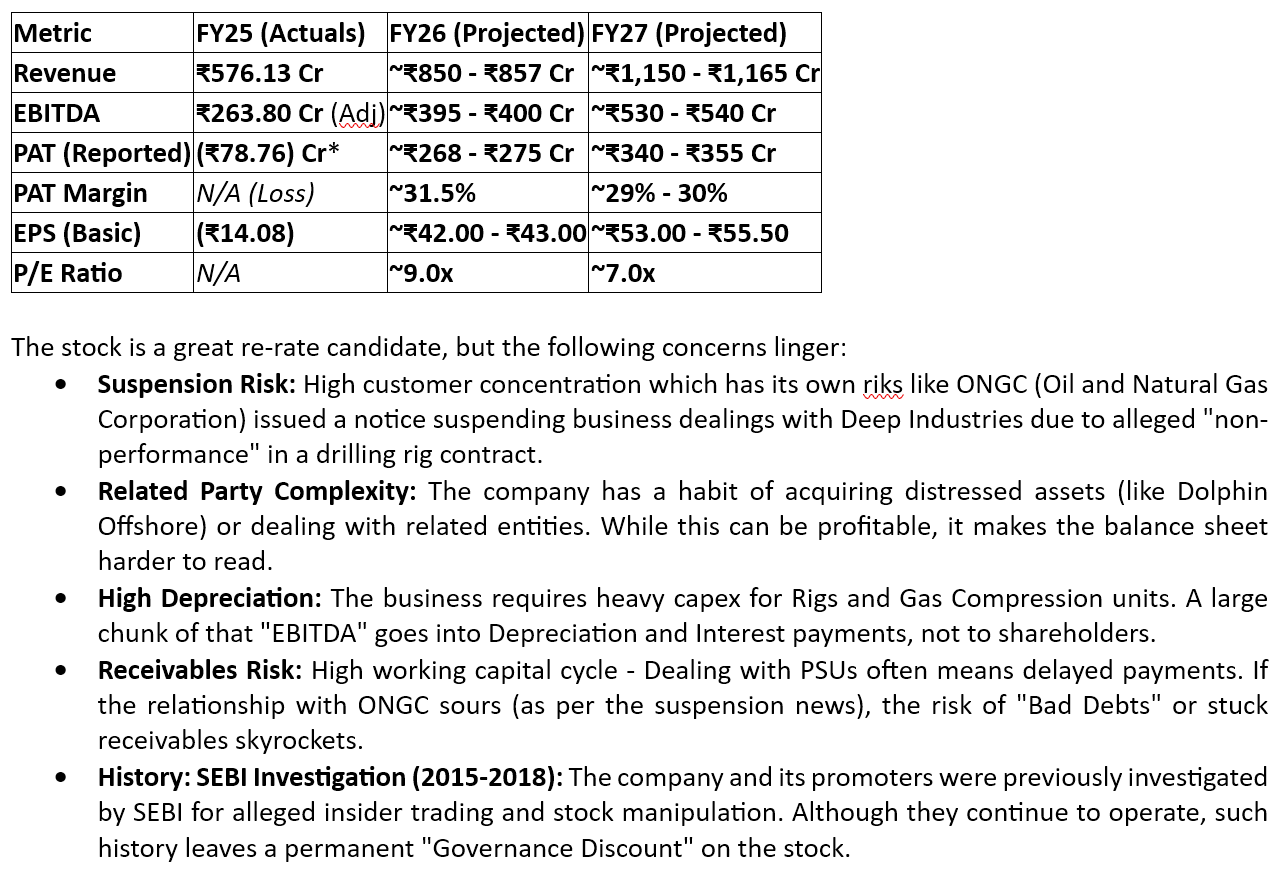

Good analysis and article on Deep - Deep Industries Ltd Q3 FY26 – ₹3,050 Cr Order Book, 45% OPM, 70% Market Share: Is This Oilfield Beast Just Misunderstood or Casually Ignored? - Eduinvesting

Deep is probably re-rate candidate with risks! Q3 Mgmt. summary & forward looking projections. Do highlight errors pls

Q3FY26:

• Company’s order book stood at ₹ 2,967 Cr as on date.

•

Q3FY26:

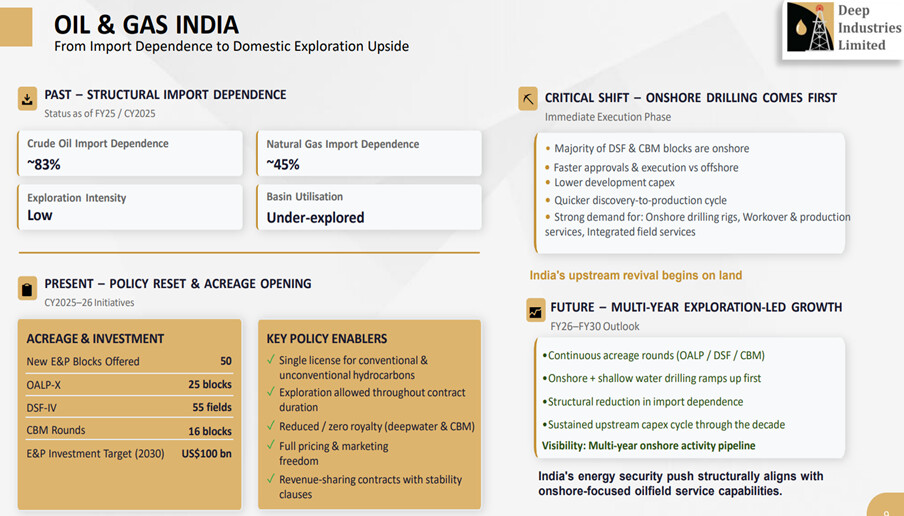

• INDUSTRY TAILWINDS: India’s energy sector is currently witnessing one of its strongest multiyear investment cycles. The policy focus has decisively shifted from energy security to energy independence with a clear road map to mobilize over USD100 billion of investments in oil and gas by 2030 and a broader opportunity of over USD500 billion across the energy value chain. This includes accelerated domestic exploration, expansion of gas and LNG infrastructure, high refining capacity and deeper integration across upstream and downstream segments.

Continued policy thrust on expanding exploration acreage, strengthening gas infrastructure and enhancing domestic production capabilities is supporting sustained demand for integrated oilfield services

• Gas leakage incident:

o The situation was successfully contained within 5 days, which is a rare outcome in such cases.

o We do not have any such provisions in the contract for claiming any loss or penalty.

o There would be a little delay in the revenue ramp-up of around 2, 3 months because of this. Other than that, we are not foreseeing any negative out of this.

o The well is not permanently capped. It is capped temporarily. And once we have our rig that is expected to come within 3 months, so once we have that rig going, we will try to recover that well and try to produce from that.

o On losses: One Rig has been destroyed. Certain portions of rigs have been destroyed. And we have the necessary insurance for ensuring that our losses are recovered. But we don’t find major losses towards any other thing. There would be a few amounts that we are not still aware about because that assessment is still going on. But we don’t feel that it should be significant. We have covered very well, not only on the rig side, but also on the well side.

o And today, with the PEC contract, we are working on 40 different wells. So, the one that the incident has taken place was one of them. Of course, that was a substantial of it. But having said, we have other 39 wells with us, and we are flowing a lot of gas from many other wells. So, there could be a little impact on the incremental gas that we were to produce from this well.

o Accidents, I not say that it’s very common, but this is part and parcel of oil and gas business. So even such kind of incidents happen with other contractors or with ONGC themselves. So, it is not something that because of this you have any penal actions and all. This is something that is a part and parcel of an oil and gas industry.

• Our current bidding pipeline is somewhere around INR800 crores. With a success rate is around 20%, 30% but in some of verticals, it is more than 50% as well.

• PEC CONTRACT: In this quarter, contribution from PEC was somewhere around INR20 crores.

Our expectation from this particular project is around INR 150 crores on a yearly basis from FY27-28.

• We are expecting good amount of conversion in Q4 based on tenders bidded and in 1 or 2 we are L1 as well. So yes, I can see the order win for this particular quarter was not as high as it was in earlier quarters, but that can spill over in Q4.

• We are also looking to get into a higher capacity rigs, which are the need of India today. So, we are actively working on those opportunities to get in that segment

• QIP: With regards to QIP, we have just paused that process as of now, and we are not going ahead with it.

Impact on future growth and capex plan: We are generating some handsome cash from business, and we are very much comfortable on our debt levels as well. So, we have a huge opportunity to raise debt as well as and when required. So largely we’ll be able to manage without QIP.

With regards to acquisition of targets, it can differ a bit or maybe in next year.

• Q-on-Q, there can be some projects maybe spilling over to next contract, and there can be 1 or 2 contracts or assets which may be in transit from one contract to another.

• Next two years we should have growth of 30-35%.

• Kandla should start contributing from second half of FY '27.

• Impact of lower crude oil prices: In our business, entire revenue is coming from services, which are more of support services to oil and gas sector. And these services are more of inevitable in kind of nature. And so, it has very negligible or, I would say, least impact on crude oil price because whatever crude oil price would be, these services would be required.

• On the industrial goods imported from America, since we are actually importing a lot of compressors and stuff from America, if duties would be reduced, it will definitely help us reducing our capex.

THINGS TO TRACK:

• PEC Contract –Will the capped well resume production in 2-3 months? Will the revenue generation be as guided? Can the segment surprise on the upside? Any future execution issues.

• New Offshore/Marine segments: Apart from the barge, what other segments/assets will the company get and how will its revenue and margins pan out?

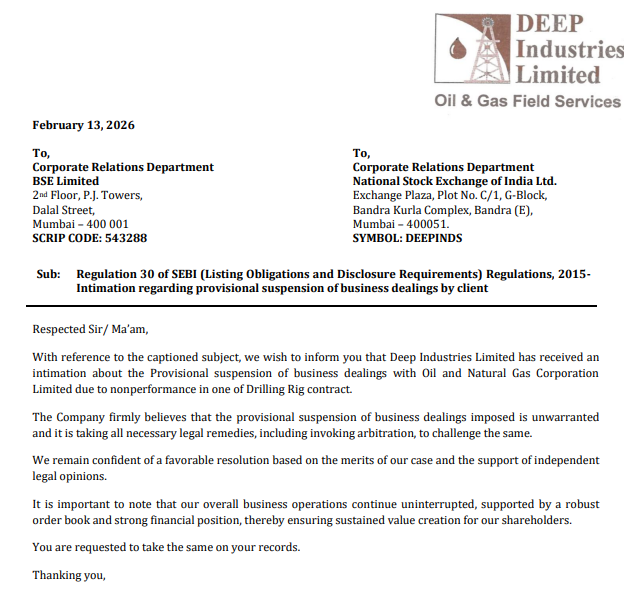

• ONGC provisional suspension: How quickly will they get it removed? Impact on orderbook going forward if it remains in place?

• Gas Compression and Gas dehydration segments: How much will these be affected by increased competition going forward? Would new segments be able replace their revenue contribution in the long run?

• Core orderbook slowdown?: As focus of the management turns to PEC’s and Offshore segment, will the core segment slowdown a bit? Increased competition in those segments may have led the management to pivot to these new growth segments.

• Kandla energy operations progress: When will operations start? Impact on Ebitda margins and cost savings.

• Loan to Prabha energy: Since Prabha has started operations on gas field, will the loans by Deep get reduced?

This will be my last post on Deep Industries Ltd (for real this time).

Insolvency petition against Deep Industries.pdf (862.0 KB)

An insolvency petition under Section 9 of the Insolvency and Bankruptcy Code, 2016 was filed against Deep Industries Limited by SES Energy Private Limited, an operational creditor, seeking initiation of the Corporate Insolvency Resolution Process (CIRP). The petition was registered as C.P. (IB) No. 252/AHM/2024 before the Ahmedabad Bench of the National Company Law Tribunal. Deep Industries Limited was arrayed as the respondent / corporate debtor in the said proceedings. The matter was adjudicated by the Hon’ble NCLT, Ahmedabad (Court–II), and an order was pronounced on 16 December 2025, rejecting the application.

The filing of an insolvency petition against a listed entity constitutes a deemed material event requiring mandatory disclosure under Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015. In terms of Regulation 30(1) read with Schedule III, Part A, Para A(16), the filing of an application or initiation of proceedings under the Insolvency and Bankruptcy Code, 2016 against a listed entity is specifically identified as an event that shall be disclosed to the stock exchange(s). The disclosure requirement is triggered at the stage of filing of the application itself and is not contingent upon admission, rejection, or the final outcome of the proceedings.

Further, Regulation 30(2) requires such disclosure to be made as soon as reasonably possible and not later than twenty-four hours from the occurrence of the event, while Regulation 30(4) mandates continuous disclosure of material developments and outcomes. In the present case, despite the insolvency petition having been filed and adjudicated, no disclosure appears to have been made to the stock exchange(s) at the time of filing of the petition.

Before someone reads the NCLT order and replies that the claim of the Creditor was only ₹15 crores, as against operational assets worth ₹2000 crores held by Deep Industries, here is some context:

Reliance Industries Limited, with an annual sales exceeding ₹10,00,000 crores and a QUARTERLY PROFIT of ₹20,000 crores discloses to stock exchanges a GST demand raised worth ₹92,00,000. Let that sink in. It was never about the Demand to Assets ratio. It was always about the intent.

SEBI Regulations are clear. Irrespective of the merits of the case or judgement provided by the Tribunal thereof, if there is ANY insolvency petition against a listed company, it should be disclosed to stock exchanges within 24 hours. Period. No questions asked.

Anyway, I had a lot of fun posting on this thread. Learned a lot. I acknowledge that now I have been asked twice to start a new thread, I probably will. I would be ecstatic if other participants contributed in that thread: how to use AI and find financial statements inconsistencies without being an accounting professional, how to use Google to find documents and orders that companies don’t want you to find, how to use Notebook LM to find statements made by management that contradict what is written in the financials.

I look for 3 things: Acquisitions, Goodwill and Pharma companies.

Until next time :)

It is a great business, but I find something unusual. An oil and gas promoter is bidding for a textile company. Why is this unusual? When we look at the promoter’s history, it has always been in corporate roles within related businesses like oil and gas. Bidding for a textile company does not seem rational. This does not mean the company is bad or that something wrong will happen in the business.

Dis : i am not Invested.

Deep Industries is master in acquiring asset through IBC when it is available at highly discounted price (100 rupee asset at 1 Rupee). Don’t just go by company name but go through their hard assets (land, building, machinery) owned by the company getting sold through IBC.

If company is getting corporate office in metro city at cheap valuation through acquiring the company, what’s wrong!

Do you honestly believe it is that simple? Getting a 100 rupee asset for just one rupee? Think about the logic here. We are talking about a company already buried under evidence based corporate governance allegations. Is this management really so brilliant that they can outsmart trillion dollar giants like BlackRock or Brookfield?

These global private equity institutes have the best brains and unlimited data to spot a deal. It makes zero sense that a company with a shaky reputation and no expertise in this specific sector can suddenly walk in and snag a massive discount that the professionals missed. If a deal looks this cheap, it is usually because there is a massive hidden skeleton in the closet.

Really think about it, brother — what is the history of recovering assets like this, except in the case of Dolphin?, Lot of subsidiary in this company.

Big fish are not interested to fish very small fish….for them this is is too small !

In spite of large banks like HDFC, ICICI, SBI..which has housing loan, gold loan portfolio, still many small housing finance companies surving and growing better than big banks. Hence, each company has its own core competency !

you mentioned that big and small both exists together right? So for this small fish[Small asset] there is lot of small players exists. so expecting that deep industries getting this deal at significant discounted value and others are completely ignoring it and this deal is so value lucrative that deep management going beyond their competency is simply too good to be true and almost certainly a value trap.

Deep Industries Ltd. has recently decided to expand its business into the green energy sector by amending its Memorandum of Association. This strategic move is expected to strengthen the company’s long-term growth prospects and align it with the global energy transition trend. Along with its existing strengths in oilfield services and production enhancement projects with ONGC, this diversification could open new opportunities in emerging energy segments. If executed well, the initiative may contribute positively to the company’s future revenue streams and overall business expansion. read more: https://www.bseindia.com/xml-data/corpfiling/AttachLive/0822b7eb-8fb3-493e-9949-072602d2e614.pdf

Every Tom, Dicky and Harry is jumping on this gravy train called Green Energy. As it is , it should ring alarm bell and raise question mark on management competence. Iam very circumspect on this, particularly when the space is so crowded and many companies are bound to go bust in this initiative, except for own use.

This is my view. I had some small investment less than 1% of my portfolio, which I have placed on watch category because of this unrelated expansion.

This analysis feels a year or two late. India’s green energy sector, particularly renewables like solar and wind, has seen explosive growth but is now entering a consolidation phase as of early 2026. While capacity additions hit records in 2025 (around 40-50 GW), challenges like grid integration, PPA delays, and transmission gaps are slowing new awards, shifting focus to reliability and integration.

Green Energy might unlock cross sell opportunities to Deep.

Two-year MOU (13-Mar-2026) with Advait Greenergy to jointly bid and execute green-hydrogen projects.

This is good move as it will maximise utilisation of DEEP assets. DEEP has good experience in gas compression & Gas Dehydration, Conditioning & Processing. This will increase their charter hire gas assets utilisation. I think this good move by DEEP to capture this new opportunity. DEEP has good track record of getting orders from PSUs, and this will help ADVAIT to get more order from PSU as per below communication

Hope, market now re-rate again upward!

Disc - Invested (avg buy price 255).

Deep Industries Ltd. has announced that the provisional suspension on certain business dealings, previously intimated in February 2026, has now been partially revoked following an amendment received on March 19, 2026. The company clarified that the suspension will no longer apply to its key service segments, including gas compression, gas dehydration, and drilling and rig-related services, effectively allowing core operations to continue uninterrupted. While the matter is not fully resolved, the development significantly reduces operational risk and is seen as a positive step toward normalizing business activities. https://www.bseindia.com/xml-data/corpfiling/AttachLive/432b88fb-64d3-47a6-955e-6c5076e335a8.pdf