an office in Ahmedabad and some land in Kutch. They paid 2 cr for this

My notes from Deep Industries concall (Not exhaustive, only covering what I remember and what I thought was important)

-

Seeing strong order pipeline in the standalone business, management expects it to convert to orders over the next few Qs (They have been saying this for some Qs, lets hope nos. start getting in the OB soon)

-

Expect to grow the standalone business by 20-25% YoY

-

Dolphin barge Prabha is undergoing final stages of refurbishment. They have spent 11-11.5mn $ in refurbishing the barge and getting it to working condition. They may have to spend 10-20% more. Prabha is expected to start earning revenues in Q3. Prabha will be deployed in Mexico and management is hoping Prabha can be contracted out for 320 days in a year at a per day rate of ~50000$/year. So annual revenues can be INR 130Cr in FY26. Management expects 50-60% EBITDA margin on Prabha revenues

-

Apart from Prabha, Dolphin has bagged an INR 50Cr DSV (Diving support vessel) refurbishment contract where in they will get paid to bring the client’s DSV to operating levels via repairs and refurbishment. The contract is to be executed in FY25. Thanks to this contract and Prabha, management expects 70-80Cr revenues in Dolphin in FY25

-

Other assets in Dolphin are anchor tugs which are need of significant repair. Management has no immediate plans to repair them. Instead they are on the lookout for acquiring an OSV/DSV in the second hand market. This is difficult in my opinion as OSV/DSV rates have gone through the roof due to supply shortage and any vessels purchased at current prices may lead to sub-par returns on capital

-

Overall I feel in FY26 Deep Industries can deliver 170-180Cr PAT (with 25-35Cr PAT

coming from Dolphin) in FY26 if management executes smoothly in the standalone business and Dolphin. Management quality is not pristine as highlighted in this thread earlier and O&G is inherently a volatile business subject to oil price fluctuations. But given GoI’s thrust on increasing domestic oil production, over the long term, O&G ancillaries like Deep Industries and Seamec could be interesting plays.

Disc: Invested

13 Likes

Management interview on growth plan, capex and margins.

Disc: invested

2 Likes

Sir, did you get any reply from management on break up cost of the dolphin assets interest cost and depreciation to conclude the PAT.

1 Like

DEEP Q1FY25:

• Order book for Deep Industries - INR 1246 crores, reflecting a 12% year-over-year growth. Company is witnessing highest ever bidding pipeline which could further enhance the order book going forward.

• Industry news: The winners of the ninth round of Centre’s Open acreage licensing policy (OALP) are likely to be announced in next couple of months. There have been news reports that to accelerate the exploration and production, the government is also planning to announce 10th round of OALP. Both these rounds put together would bring in around 50 blocks under exploration, thereby providing immense opportunities for the Company for oil and gas support services.

As you all might be aware, prior to OALP under hydrocarbon exploration and licensing policy (HELP), separate rounds of new exploration and licensing policy (NELP), Coal – Bed Methane (CBM) and Discovered Small Fields (DSF) were also held by Government. Under NELP, 32 blocks out of total 254 blocks awarded are operational. Additionally, 33 CBM blocks and 2 DSF blocks recently announced are also potential opportunities for the Company.

• Dolphin offshore:

o PRABHA BARGE: The update on Barge asset Prabha is that the refurbishment is now in the final stage of completion and we expect it to contribute to revenue from next quarter (Q3) onwards.

Prabha would be deployed in the markets of Mexican region. So optimistically there operating day rates are more than 320 in a year, and so the rates what we are getting expression are in range of $50,000 a day. So, this particular asset would be deployed on those regions with similar kind of day rates.

We already are in advanced talks with few clients and we are deliberately not closing because we are trying since it is under refurbishment; we are of the view that we have a good amount of time to explore and get the better rates. So, contracts and expressions are already available with us. We are just looking in for the opportunity and we are going to time it in such a way that on one hand and we have equipment ready and on the other hand we have an order to be executed ready for signing.

So, we believe that on full year basis, a single barge can earn revenue of 90-100 crore. Could be 130-140crs if deployed on 300+ days and 50K$ rates.

o We have few opportunities available for Diving Support Vessel (DSV), Platform Supply Vessel (PSV) and Anchor Handling Tugs (AHT) in both local and international market and we are evaluating the same in terms of their margins and payback.

DSV and PSVs are not available as of now with Dolphin, so we are evaluating opportunities on getting some good contract. We may buy those assets. Targeting more than 15% ROCE from those assets. (Currently market is tight for these assets)

We have tugs (Tug Handling Boat) available, but they a not in class condition, so we’ll have to do refurbishment in that tug as well. So, we would be taking that in task based on the award of contract. We have SDS as well which is diving support system. So, in addition to tugs we have SDS as well. Those assets are also not in working condition, so we’ll have to get them in class.

o We have reported revenue of around 8 or some crore. So, this is particularly for a project which we have taken for execution for one of the DSV which we would be executing for our client where in our scope, it is sourcing, preparing and getting that asset is in class. So, with our experience of getting Prabha in class, we have taken parallel project for some small project, the revenue for which may be spread over three or four quarters, yeah. We are expecting total for us would be in range of around 40 to 50 crores over a period of projects.

We have kept ourself open for evaluating similar and other type of opportunities which are coming in our way.

o Dolphin shipping: it’s an associate or a sister company of Dolphin Offshore Enterprises. They also have one office in Mumbai and one or two tugs are also there with some receivables are also there.

• We are clearly expecting some awards to get awarded in one to 2 quarters.

• INCREASED OUTSOURCING OF INHOUSE OPERATIONS: One of the ideas was especially for the gas business or the gas processing business was that not only are the new orders being more prone to outsourcing, but existing operations could also be outsourced because people are just tired of managing the business themselves. Are we seeing that in actuality, are some of the bids that we’re bidding or some of the business that we’re winning, is it coming from captive processes now being outsourced?

Yeah, yeah. We got awarded some tender only last quarter. I think it was in this quarter or last quarter like I’m not very sure about it. So, we got the gas processing, gas compression facility which our client had and they outsourced the facility for smooth operation and maintenance. And that was also the one of the contracts that we got awarded. So likewise, we are sure that this concept is now getting very popular. And going forward, those will also be adding to our stream of business.

• Kandla Energy and Chemicals: It’s a very small investment of around 2 cr. They are owning one office in Ahmedabad and one land in Kutch, which is very much ideal land for setting up factory. So, few assets are still left. And since the value was not that much, and the manufacturing which they used to be in can be helpful in our synergy of drilling, so we decided to go for it.

So, we are going to set up a new plant over there? We as of now, we are just evaluating various opportunities what we can do out of that particular land and their original capacity of manufacturing those chemicals. So as of now, it is little early to say what exactly we will be going to do.

• In booster compressor, the demand is not coming up as per our anticipation and so there we are going slow. RAAS, we would be doing around 18 to 20 crore this year, that is what our expectation is.

• Euro Gas JV contract is still under evaluation.

• We’re looking at buying 3 new rigs during the year, which is again firm orders. In next four to six months, we’ll commercialize them.

4 Likes

Ratings upgrade for Deep Ind by CARE.

dr.vikas

1 Like

New order from ONGC. Order value 1,402 Cr (single order is > 50% of current market cap of the company !!)

In addition, company has mastery in acquiring asset at vary cheap valuation through insolvency resolution process under the Insolvency and Bankruptcy Code and converting them in efficient asset generating good revenue and profit with minimum investment on it.

Disc - Invested earlier. 8000 @ 201 INR

4 Likes

15 year order. Don’t extrapolate this with market cap.

5 Likes

Recent rating upgrade received, and the receipt of bulk order (to spend over 15 years) shows clear growth path with strong potential.

3 Likes

For simplicity’s sake, divide total order (1402 crores) for each year by 15 (93 crores per year)

If you discount that value of the order over the years to the present (10% discount rate) the present value is still 710+ crores which is quite significant.

5 Likes

Management interview:

- Revenue to grow at 35% CAGR over 3-4 years

- Blended EBIDTA margin to remain stable

- ONGC contract of INR 1402 crores: target to complete it within 10 years [instead of 15 years contract tenure]

To monitor:

- additional order wins [not factored in revenue guidance of 35%]

- margin in ONGC contract

- competition in the space from the likes of RBM infra [won a much larger order of INR 3,500 cr from ONGC]

8 Likes

Deep Industries operates in a cyclical industry, with its revenue and profitability fluctuating based on global oil and gas prices, economic activity, and the energy sector’s capital investments. Therefore, its stock performance and financials can also exhibit cyclicality, with periods of strong growth followed by contractions

3 Likes

Deep Industries Ltd Q2FY25 earnings call:

- Deep Industries Limited reported strong Q2 and H1 FY25 results, driven by robust order flows and a promising billing pipeline. Consolidated revenue from operations rose 29% to ₹130.62 crore in Q2 FY25 and 25% to ₹254.07 crore in H1 FY25. The company’s order book grew to ₹2,622 crore, nearly 119% higher than in Q2 FY24.

- The company secured a significant 15-year production management contract worth ₹142 crore from ONGC. This contract, the first of its kind from ONGC, aims to enhance production from ONGC’s mature fields in Rajamundi. Deep Industries expects to earn service revenue linked to production increases through this contract. The company anticipates margins above 40% for this production enhancement contract.

- The refurbishment of the Prabha asset, an offshore support vessel acquired through the Dolphin Offshore acquisition, is in its final stages and is expected to contribute to revenue from Q4 FY25 onwards. The refurbishment process took longer than initially estimated due to unforeseen circumstances. The company expects Prabha to generate minimum revenue of $50,000 per day.

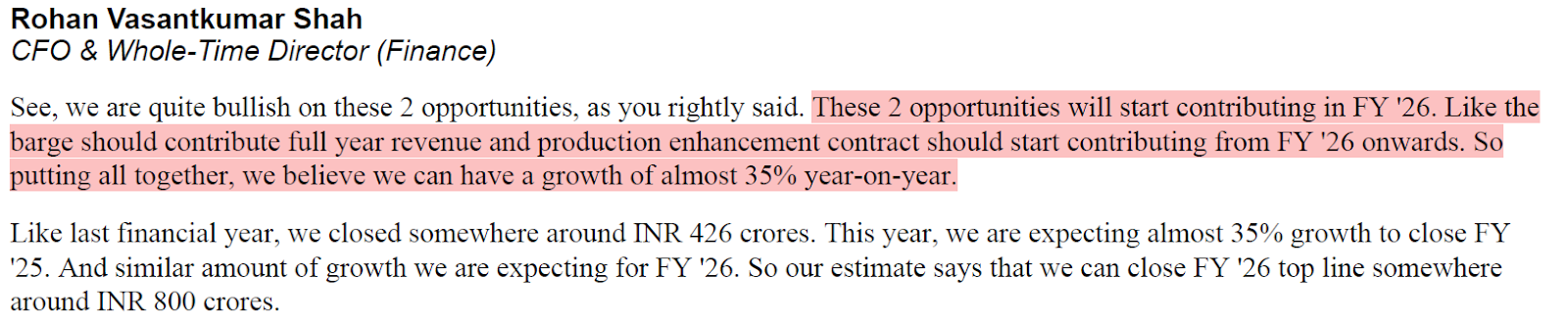

- Deep Industries is optimistic about its growth prospects in FY26, driven by the production enhancement contract and the deployment of Prabha. The company projects a consolidated revenue of around ₹800 crore in FY26, representing a year-on-year growth of approximately 35%.

- The company’s core business order book stands at around ₹1,250 crore, and the management anticipates securing additional orders in the next 3 to 6 months. The bidding pipeline for traditional business is approximately ₹800 crore.

- Deep Industries clarified that its high debtor days are primarily due to old receivables from the Dolphin Group, amounting to approximately ₹141 crore. Excluding these old receivables, the company’s normal debtor days are in the range of 90 to 100. The management is pursuing the recovery of these receivables, including through arbitration awards.

- The company emphasized that its business is not directly linked to global crude oil prices. Deep Industries operates primarily in the services business, with fixed-price contracts for the duration of the contract. The company’s focus is on natural gas, and its business is largely domestic, insulating it from global crude price fluctuations.

This earnings call highlighted Deep Industries’ strong financial performance, significant contract wins, and optimistic growth outlook. The management addressed investor concerns regarding the delayed Prabha deployment, old receivables, and the impact of crude oil prices.

8 Likes

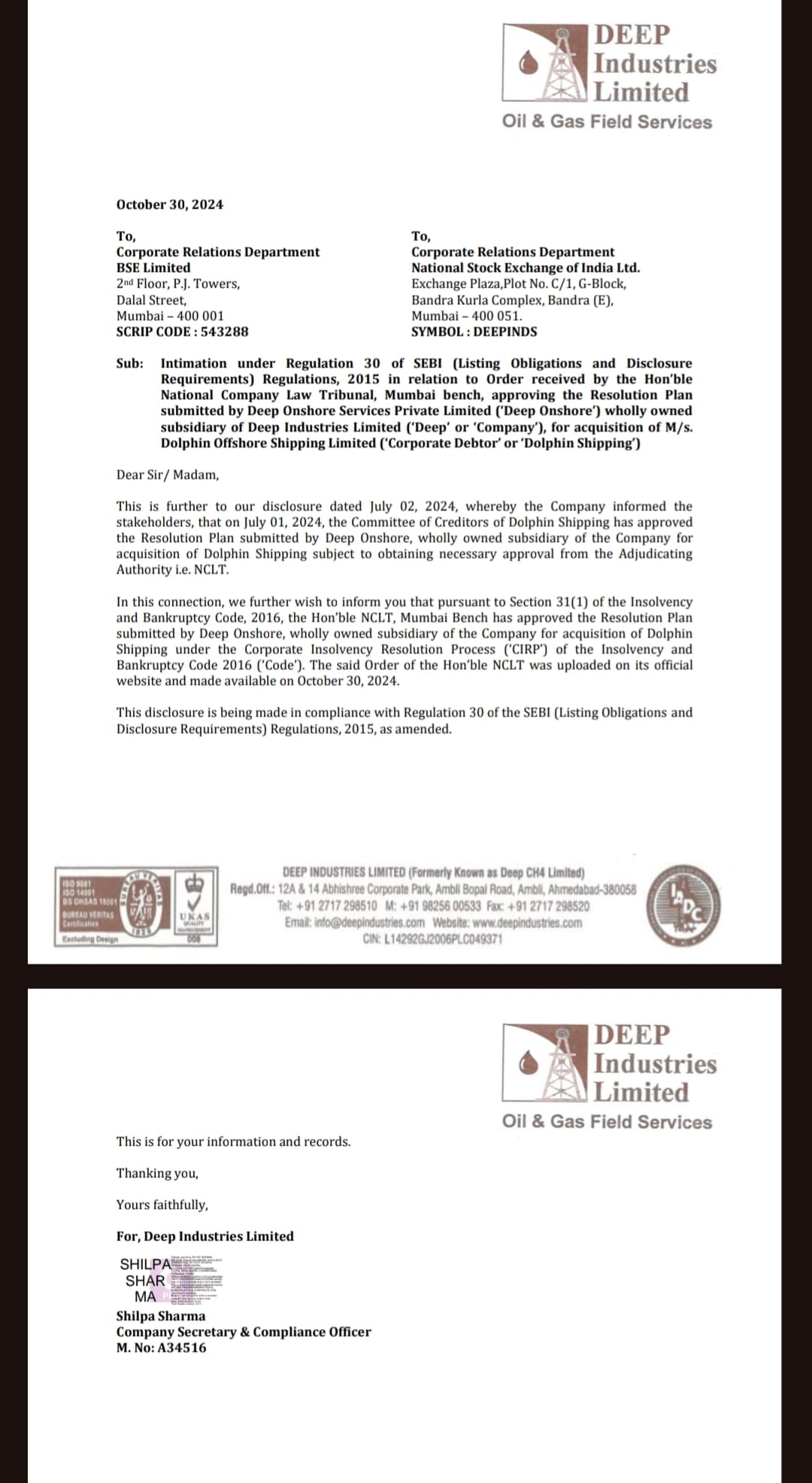

Deep Industries Limited has received approval from the NCLT for the acquisition of Dolphin Offshore Shipping Limited.

1 Like

Contract from ONGC Valued at more than Rs. 1400 Cr.

1 Like

Management has said in recent concall, that they will book INR 100 crores every year from this order.

2 Likes

Deep Industries Limited (DIL) Earnings Conference Call Summary Q2FY25: My Notes

Financial Performance

- DIL reported strong quarterly and half-yearly performance.

- Consolidated revenue increased by 29% to INR 130.62 crore in Q2 FY25 and 25% to INR 240.7 crore in H1 FY25.

- EBITDA rose to INR 64.6 crore in Q2 FY25, with EBITDA margins at 46.9%.

- Half-yearly EBITDA grew by 46% to INR 126.4 crore, maintaining margins around 45%.

- Q2 FY25 net profit stood at INR 41.5 crore, up by 40% year-on-year.

- Half-year net profit was INR 80.29 crore, marking a 32% year-on-year increase.

- The order book reached INR 2,622 crore, a 119% increase compared to Q2 FY24.

Operational Performance

- Contract with ONGC is for INR 1402 crore while majority of revenue is expected to be booked in the first 10 years only. Through this contract, all services revenue linked to production increases.

- The update on the Barge asset Prabha is that the refurbishment is now in the final stage of completion, and company expects it to contribute to revenues from quarter 4 onwards. The refurbishment process has taken a little more time than their initial estimates.

- Barge rate is in the range of USD 50,000-55,000 per day, while management expects it will be operational for 330 days in a year, although only 90 days revenue will be booked in FY25. Approximately INR 130 crore opportunity from Prabha in FY26. Management is evaluating whether to put it on charter hire for long term or short term.

- Considering the production enhancement contract and “Prabha” asset deployment, the company anticipates 35% growth in top-line in FY25. They estimate FY26 top-line to reach around ₹800 crore.

- Going by the guidance of 35% growth in FY25, this year Deep will do INR 570 crore topline, out of which standalone will contribute INR 450 Crore, other subsidiaries will do INR 50 crore and Dolphin will contribute INR 70 crore.

- Estimating USD 2-3 million in H2 from Dolphin contract immediately after Diwali.

- Arbitration award of INR 33 - 35 crore is expected to be received by this year, taking time since these clients are PSU’s.

- Excluding Dolphin debtors, normal debtor days are in the range of 90-100 days only.

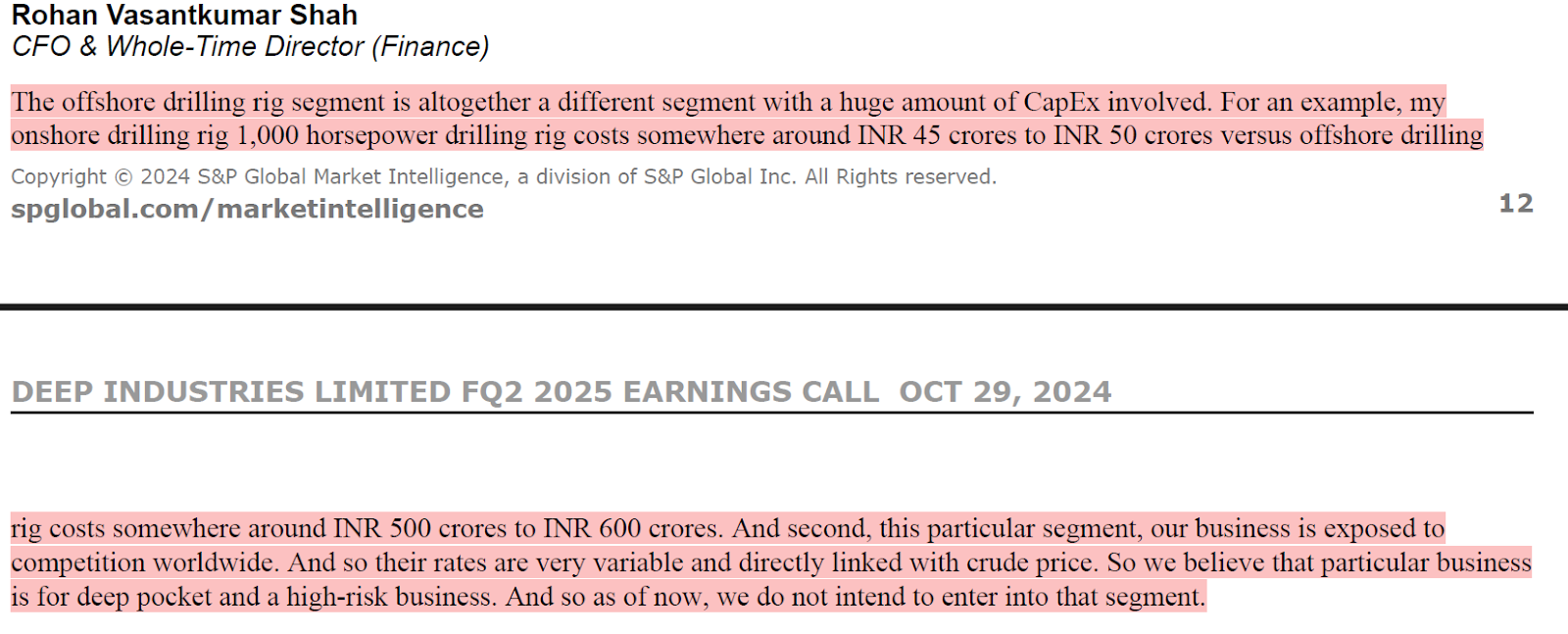

- Reason for not going in the offshore drilling business as explained by the management.

- Breakdown on the revenue contribution on the 3 rigs which is going to be operational in next year.

- RAAS will not contribute more than INR 15 - 20 crore a year, as demand is not picking up in the booster segment.

5 Likes

DETAILED Q2FY25 CONCALL NOTES:

• PEO CONTRACT: Through this contract we will earn service revenue linked to production increase. Although the contract spans 15 years and since it is front loaded, majority of the revenue will be booked in the first 10 years.

Our estimate says that every year, we should book more than Rs. 100 crore a year.

This contract is the first of its kind from ONGC, with more rounds likely to follow. Our public sector units and private clients are also introducing PECs and with our 30+ years in the industry, we are well positioned to secure similar projects in the future.

We anticipate margins above 40% for this production enhancement contract as well. Such high value contracts with excellent margins are expected to significantly improve both our top and bottom lines. Execution of this contract will commence in 7-8 months targeting the next financial year.

In the production enhancement contract, we will have to do a certain amount of CAPEX, but that has been staggered over a period of 10-12 years. The exact CAPEX plan will be formalized once we take over that field and start implementing the strategy which we have planned.

The asset which we have got is not under APM price. We can sell the gas at market price.

Revenue model: Revenue is split in two different modes. One is fixed, which is for their existing production line and whatever incremental production we achieve, we will get our services charges which are similar, or you can say equivalent to 64% of revenue of that particular incremental gas.

The contract was ordered considering $7 of natural gas price, do you think there is any chance of in the near term maybe the gas prices falling below that? Rohan Shah: Not at all, because currently it is trading somewhere around $12.5-$13 MMBtu and price falling below 7, we don’t foresee even in rarest of rare thing kind of.

So, in this particular kind of business, the selection of field is very crucial because if you do not have any data or knowledge about geology of that particular field, then getting such contract may not be that fruitful even if you get contract for 15 years because you will have to understand and evaluate the geology of those particular fields well in advance before even applying for those fields, because at the end of day your revenue is more linked with incremental production. And so, we have been able to select the field which we believe is very resourceful and from which we can definitely increase the production and get our best part of revenue.

• We anticipate additional valuable contracts to be added in our order book in the coming 3-6 months, alongside strong bidding pipeline conversion within our regular business verticals.

Bidding pipeline of almost 800 crores for our regular traditional business

• PRABHA BARGE: The update on the Barge asset Prabha is that the refurbishment is now in the final stage of completion, and we expect it to contribute the revenue from quarter IV

$50,000 is what we expect minimum revenue per day. Currently, the rates are even higher than 50,000.

Contract hasn’t been signed. So, currently, the discussions are already going on with potential clients and we are evaluating both possible options whether to put on a charter hire of long term more than 5 years plus or to have a short-term charter hire.

• H2 has always been higher than H1. And so, we believe this year will also continue the same trend and our H2 would definitely be higher in terms of revenue than H1.

• We believe we can have a growth of almost 35% year-on-year like last financial year, we closed somewhere around Rs. 426 crores and this year we are expecting almost 35% growth to close FY25. And similar amount of growth we are expecting for FY26. So, our estimate says that we can close FY26 topline somewhere around Rs. 800 crores.

• DOLPHIN CONTRACT: In H2, we are estimating something around $2-$3 million to be added into revenue from this particular contract and with regards to receivables collection, it should start immediately after Diwali for this particular contract.

• DOLPHIN RECIEVABLES: Received 3 arbitration awards in our favor. 33 - 35 crores amount awarded. Amount yet to be received. Ideally, it should have come by now, but since these clients are PSU’s, we will have to give some more time to them.

Other debtors, we are pursuing for recovery of the receivables, which we believe should definitely come to us.

• For customers like Vedanta and ONGC, how is the contract structure generally? Is it a maintenance contract or is it just a one-time installation and then it runs for a particular lifetime. How is generally that particular business, is it repetitive?

Rohan Shah: So, these are service contracts and largely these contracts have been awarded in the range of 3- 5 years. And on completion of those 3-5 years, they will come up for rebidding. And our revenue generally depends on the quantity of gas we process. They are more of annuity contracts.

• Regarding offshore drilling, we do not intend to enter into that segment as it is a very capital intensive and risky segment

• In the current financial year, we are adding three new rigs, which will definitely start contributing in revenue probably in Q4 or in Q1 of next financial year.

We are adding 3 rigs, out of these three rigs, one is 1000 horsepower drilling rig and other two are workover rigs of which one is 100 ton and other is 150 ton. So, all these three rigs are having different rates, and we have already confirmed order for these rigs. And based on those orders only, we are importing them

1000 horsepower drilling rig should bill somewhere around Rs. 3 crores a month and workover rig billing should range from Rs 50 lakhs to 75 lakhs a month.

• So, as a policy, we always go for CAPEX only after getting a confirm order and it varies from contract to contract, order to order.

• Loan of Rs. 58 crores has been given to a Company called Prabha Energy, which is our group Company, and it is a short-term loan recoverable within a year’s time.

• Have bidded for another PEC. It is still under evaluation.

• OVERSEAS OPERATIONS: In Middle East, we provide various gas processing services from compression, dehydration, and processing to countries like Egypt and Oman, and this particular Company is contributing around Rs. 40 to 50 crores a year. And we believe it should continue contributing this similar amount with growth of around 10%-15%.

• RAAS: With regards to booster compression business, under RAAS, we are not anticipating much growth because the GA’s which have been awarded for City Gas distributions are getting extensions and so the demand of those booster compressors is not picking up as per our expectation. So, that particular Company is contributing not more than Rs. 15 to20 crores a year.

• LINKS TO CRUDE PRICE: Our business is not at all linked with crude prices or their fluctuation because primarily we are into services business. And our service contracts are fixed price contracts for the tenure of contract. So, once we have entered into a contract with X rate, those rates will continue for the tenure of contract. They are not at all being affected by crude price.

Second, in our overall service mix, our major focus is on natural gas rather than on oil because in our drilling rigs or workover rigs, if my client is giving me to drill oil wells, then only we are exposed to crude oil. Otherwise, we are drilling gas wells also and oil wells also. Other than that, our entire service portfolio is pertaining to natural gas, which is not directly linked with crude oil prices.

And since our entire business is largely domestic within India, so we haven’t seen any direct relation with crude oil prices in last 30 years. In fact, we have seen sometimes where crude was going down and our services rates were increasing. So, I don’t think we have any direct impact of crude price in Deep Industries’ business.

• Developing a field is required 1, 1.5, 2 years’ time and so I don’t think with reduction in crude price, exploration activities will start dipping and largely with clients which are PSUs like ONGC, they largely run on national interest rather than making it profitable, and so to meet the country’s energy requirement, we haven’t seen such clients reducing their exploration plans in any crude oil price.

1 Like

THINGS TO TRACK FOR DEEP:

-

Prabha Barge contract – When will it be signed? What terms and duration? Will there be delay in signing contract suggesting trouble in finding customer?

-

Core business Orderbook growth – Will big orders come in next few qtrs? Or will stagnant growth continue in core business orderbook suggesting slowdown in that segment?

-

PEO Contract – Will execution start in time? Will they face technical difficulties as this is a new segment? Will the revenue generation be as guided?

Deep is doing very well and is poised for significant growth in next 2 years. Any additional PEO contract will make the growth even faster. So lets hope the management executes as it has been doing for last couple of years.

3 Likes