One risk/drawback of Deep Industries business model is that they have to constantly pour capital into the business for growth. They have to do capex for new equipments for new contracts. This is good when business environment and end user demand is showing growth but if demand slows down after a few years, then they’re saddled with idle equipment. Also, continuous capex for growth means FCF (last 2 years negative FCF) and ROCE will remain lower (Though ROCE is improving now)

4 Likes

Found an excellent article by Mr.Shankar Nath Deep Industries: Rigged Up for 55% Growth

6 Likes

Deep has PBT margins of ~30% (very good) TTM from screener. And ROCE of ~10% (not so good).

I know both the ratios are very different and does not make sense to compare them straight out. But i always believe both should go hand in hand roughly.

Is it possible they are not taking enough depreciation for their assets on the PnL.

Need comments on this.

Due to this low ROCE, deep is a short term bet for me, until i can see visible growth.

Disclaimer: Invested

1 Like

Deep operating ROCE is nearing 14-15% now. There’s an accounting entry of 300cr which had happened during demerger of the company back in 2020. So, because of that ROCE looks optically smaller.

Coming to difference between margins and ROCE, Deep is Capex heavy business. Initial outlay to buy equipment is high. So, that’s why they have to charge higher margins or else there will be no economic sense to this industry

3 Likes

The ROCE is on the rise. For FY26 (Mar 2026), I’m estimating it at 18.7% i.e. est. EBIT of ₹311 crores divided by est. capital employed of ₹1,662 crores

4 Likes

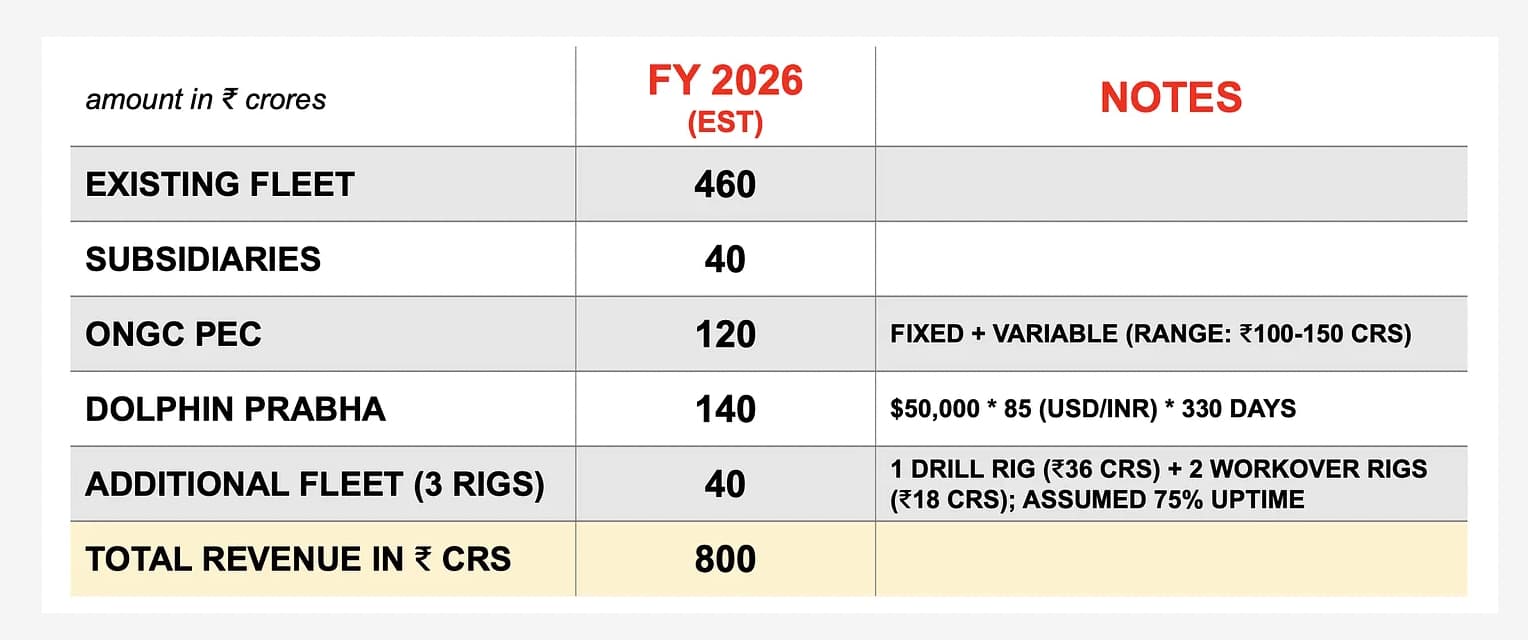

I’m projecting FY26 revenues at ₹800 crores. The PEC, Prabha & those 3 additional rigs are expected to deliver ₹300 crores in the coming FY

11 Likes

What kind of acquisition is this? Total investment is 11,000 INR only !!

Any idea what does this mean??

NDTV Profit know your company series - DEEP Industries. Management preparing for QIP for future capex and growth

4 Likes

What could PAT look like according to your calculations?

There can be multiple roadblocks to achieve that number and if even done I believe it might not be very easy to hold onto that.

For growth this business needs to employ high amounts of capital. But as you mentioned the company is at a very good position of transitioning to better results and the management is providing good conviction. All the reason for my short term 1-2 years thesis on this.

Disclaimer: Invested

3 Likes

Good numbers from Dolphin Offshore

https://www.bseindia.com/xml-data/corpfiling/AttachLive/48c1c5a0-0b23-452d-ba39-565c325656ee.pdf

3 Likes

Deep Onshore Services Private Limited is promoter of the company. And Deep Onshore Services Private Limited is wholly onwed suscidary of the Deep Industries limited ( Further acquisition of equity shares of Deep Onshore Services Private Limited wholly-owned subsidiary.pdf

1 Like

Very good result as expected !

Investors presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/1f8ae595-c558-48d8-a45d-25fa08485e3f.pdf

6 Likes

Q3FY25:

• Order Book: 2,701cr

CONCALL NOTES:

• We continue to explore opportunities in production enhancement contracts, charter hiring of entire gas processing facilities and integrated project management services, the 3 segments that are expected to drive our growth over the next few years.

(With increased competition in gas compression and dehydration segments, management is pivoting to these other segments as focus areas.)

• PRABHA BARGE: has reached Mexico after completing dry docking and is in its final refurbishment stage

We have completed, more than 95% of the work. Unfortunately, we are waiting for only one of the equipment, which is a little critical equipment, that has to come from U.S. and that has taken a little long time.

We maintain our status that we should be able to get certain portion of revenue for this quarter, barring that it has got a little delayed, but now it’s completely now on track.

Contract not signed yet – We purposely kept this area open, keeping because the markets are very dynamic. We had an opportunity to close the deal, but we thought that it is more feasible for us to wait by the time we have our barge ready - We are also trying to explore if we are able to get a little higher rate to what we had anticipated

• We have not bidded any PECs as of now. It’s my expectation that within a year, we can see some of such PECs coming out and getting awarded. So, our focus definitely would remain on bidding this kind of opportunity, which gives the clarity over a period of 10 - 15 years or plus.

• ONGC PEC contract: We are taking handover of this particular field by end of this quarter, and we’ll start operating on this and we’ll start applying our expertise to increase the production. So primarily, for FY '26, we are anticipating revenue of around 6 months or so out of this PEC.

So, initial revenue would not be that great. But from FY '27 onwards, we can expect more than INR 100 crores out of it.

Service revenue and production revenue sharing: So, the revenue or fixed price, which we will be getting to maintain the existing level of production, would not be that lucrative, it can take care of the cost which we would be incurring to maintain that. So, our bullseye is on incremental production as we’ll get share in incremental revenue.

For production enhancement contract, we are estimating capex of around INR160-odd crores, and this we would be doing in 2 years’ time

There are no penalties for not increasing production.

• GUIDANCE: We are expecting growth of more than 30% CAGR for next 3 years

Organic growth (Without PEC and Offshore services) is at 18-20%

We are quite hopeful to maintain this type of margins. So, it should be in the range of 45% to 47%.

• Can do Shale/Coal bed methane (CBM) drilling as well with current equipments and would be ready for it if opportunity arises in the future.

• DOLPHIN: In Q4 also, we can look for a revenue of around $2 million, $3 million in Dolphin without the Barge revenue.

And with regards to next financial year, the revenue would majorly from Barge. This particular opportunity, which we are working as of now, is not recurring opportunity. And so as of now, we cannot comment that in next financial year what other revenues we can book other than this Barge.

• EUROGAS JV: In JV with Euro Gas, we had bidded a few projects for supplying gas processing equipments, but we didn’t get award of it. So as of now, we are just waiting for a few such tenders to be bidded under JV. So not sure how it will shape up in the coming future.

• QIP: So largely, it would be required for capex and 1 acquisition opportunity, which we are on advanced stage

On why the QIP size is so big:

Participant: So why are we liquidating so much about 10% of equity when we can easily raise about INR 100 crores, INR 200 crores of debt, and you have anyway INR 200 crores of cash flow coming in? Please, can you explain me your understanding of why it is so high, the QIP?

Management: The markets are very dynamic these days and the kind of demand and the demand of the services, the way it has evolved, we feel that in a period of next year or 2, there would be immense flow of orders to come in. We feel utilizing whatever the current cash flows are, along with the equity that we are trying to raise, will definitely need a huge amount of debt also going forward. So, we feel that it’s always better to have an amount of liquidity on hand because it could be also used to acquire. As I think we had already mentioned in the call earlier, that we are looking in some opportunities to acquire some ongoing businesses. Of course, it has not finalized it yet, but the market is very, very dynamic these days. So, it’s always better to have the liquidity on hand. So as the opportunity gets finalized, you can always use that fund to acquire the businesses

• Our current bidding pipeline is in range of around INR 700 crores to INR 750 crores, which we expect to get converted in next 3 to 6 months based on success ratio.

See, generally, it is almost 50% is what we believe our success rate is, depending on different verticals. In some verticals, we have even higher success rate. So, on an average, you can take as 50%.

• MARINE SERVICES: So, with an acquisition of Dolphin, we have started entering into offshore segment with our first services under category of marine services, where we are planning to add a fleet of some tugs and vessels, like diving support vessel and platform supply vessels and anchor handling tugs. So, our plan is to add these equipments in our fleet 1 by 1 and to put them on charter.

One anchor-handling tugs, we have already acquired and we have acquired under Dolphin’s subsidiary with JV with some international partner. And that tug will start operation by end of this quarter itself. And eventually, we would be adding a few more equipments in coming time.

So, contracts are available for both long term and short term, depending on the time and opportunity, we may choose entering into for long term or short term. Margins are quite lucrative. They are more than 50% EBITDA margin business.

•

• INCREASED COMPETITION IN GAS COMPRESSION AND DEHYADRATION: Participant: Do you think the gas compression business has become a little commoditized in the sense of there are many players in the business. There is a lot of undercutting of prices? Sometimes we see that your quotations are higher than most of the other joining some lately kind of players in the market.

Management: It’s doing very well. And we have been strategizing it, looking to the demand supply and as I mentioned, we are still holding a reasonable amount of market share in that segment. I think we’ll continue to do that.

• POTENTIAL ACQUISITION: It won’t be possible for us to disclose to whom we are currently talking with because the deal is not yet finalized. But just to give an idea, it would be definitely with the equipment or the asset holders in various areas. Those are the target companies that we are looking at

THINGS TO TRACK:

• Prabha Barge contract – When will it be signed? What terms and duration? Will there be delay in signing contract suggesting trouble in finding customer?

• PEO Contract – Will execution start in time? Will they face technical difficulties as this is a new segment? Will the revenue generation be as guided?

• New Offshore/Marine segments: Apart from the barge, what other segments/assets will the company get and how will its revenue and margins pan out?

• QIP and Potential Acquisition and Capex

• Gas Compression and Gas dehydration segments: How much will these be affected by increased competition going forward? Would new segments be able replace their revenue contribution in the long run?

9 Likes

All in all, Deep’s medium term future looks very bright with multiple growth drivers taking shape.

With the QIP, Management is seemingly extremely bullish on the near term demand and wants to have its war chest ready.

Let’s hope they are proven right and that they will show financial prudence going ahead as they’ve shown in the past

DISCLOSURE: Invested (A core holding)

4 Likes

Deep Industries Q3FY25 Concall Notes:

95% of the work on the barge has been completed. Some revenue will come in this quarter.

Contract is in final negotiation stage. Rates :With open around $50k to $60k and without opex around $30k.

Looking to deploy in international markets. In international waters, the workings are almost 10 to 11 months, whereas in Indian waters, the season is close to around 8 to 9 months.

PEC Contract from ONGC : Taking handover from ONGC by end of this quarter. 6 months revenue in FY26. Initially not very great numbers but 100 crs + from FY27. For current level production will get fixed amount to maintain those levels and get share in incremental revenue. Will do capex of around 160 crs in 2 years time. A group of geologists and reservoir engineers as a part of our company evaluate these wells. Can get more PEC contracts in next 1 year.

Guidance : Guiding for a growth of 30%+ yoy. Traditional services will grow 18% to 19% YoY. Rest will come from barge and PEC. Targeting INR 800 crores revenue by FY '26. FY25 570-575 crs. Current TTM Revenue 525 crs.

Drilling technology from coal bed methane and shale gas is same if opportunity arises company is ready.

Dolphin with give $2 to $3 million in Q4 without Prabha. Next year revenue will mainly come from Prabha.

QIP : Capex of 500cr next year for the projects already awarded + plus some acquisitions. So 350 cr equity and rest debt. Planning to add a fleet of some tugs and vessels, like diving support vessel and platform supply vessels and anchor handling tugs 1 by 1 and to put them on charter. These will be 50% EBIDTA margin contracts. One such tug has been already acquired.

ONGC has challenged arbiration award of 85cr in High Court.

Current bidding pipeline is around 700 crs which will be concluded in next 3 to 6 months. 50% success rate.

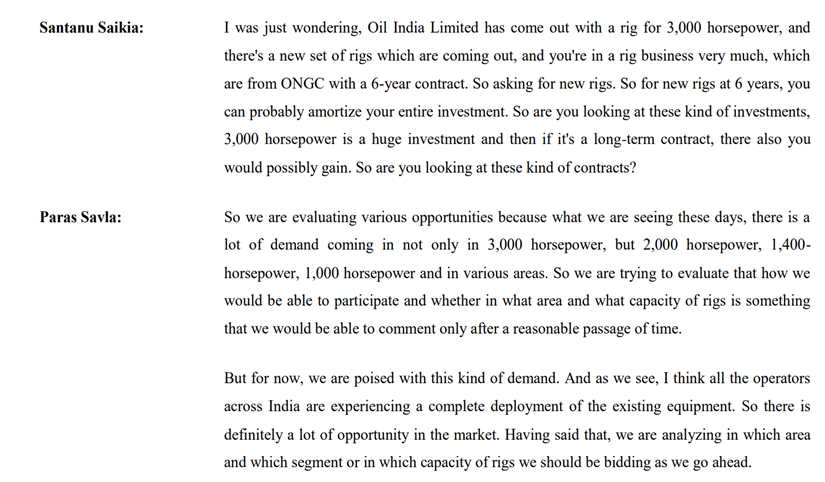

Lot of demand in market for 1000, 2000 and 3000 HP rigs.

Disc : Invested

6 Likes

Are there any details regarding Dolphin Offshore Enterprises?

1 Like

Dolphin Offshore Enterprises (India) Ltd also a Listed company you can check the details in screener.in

1 Like

Yes it is listed but there is not much data available, if anyone is having their future guidance and on going capex related info then please provide. Thank you

1 Like