Any update on Q2 FY24 result and business outlook

I think the Q2 results and call was pretty decent. Numbers are back filling. Yet to reflect in numbers IMHO.

Some brief updates are

- Q3, Q4 expected to better. Overall 400 cr. revenue and 120 cr. bottom line for FY24 seems a done deal with some minor scope for positive surprise. For FY25, a ~20-25% growth in topline in deep business doesn’t look out of place, given the order book. So FY25 rough expectation could be 480-500 cr. topline with 140-150 cr. PAT.

- Dolphin will start contributing to topline from Q4, with majority of contribution to come from FY25. 100 cr. topline with ~60% EBITDA margin is expected in FY25. We can say, PAT could be roughly between 40-50 cr. as there could be some tax benefits due the accumulated losses.

- So overall it seems FY25 could be a 580-600 cr. topline with ~200 cr. bottom line. This is of course a picture perfect bull thesis

All this for an EV of nearly 1500 cr.

You can build the bear thesis.

3 Likes

Deep Industries Limited Q2 FY '24 Earnings Conference Call, the company provided detailed insights into its financial and operational performance. Here’s a comprehensive summary of the call:

Introduction:

- The conference call was hosted by S-Ancial Technologies Private Limited and featured Mr. Paras Savla, Chairman and Managing Director, and Mr. Rohan Shah, Director of Finance and Group CFO of Deep Industries Limited.

- The call began with a reminder that participant lines were in listen-only mode, followed by an opportunity for questions.

Key Highlights:

Order Book and Revenue Growth:

- The company explained that there is a lag of about six months between order book growth and realizing revenue.

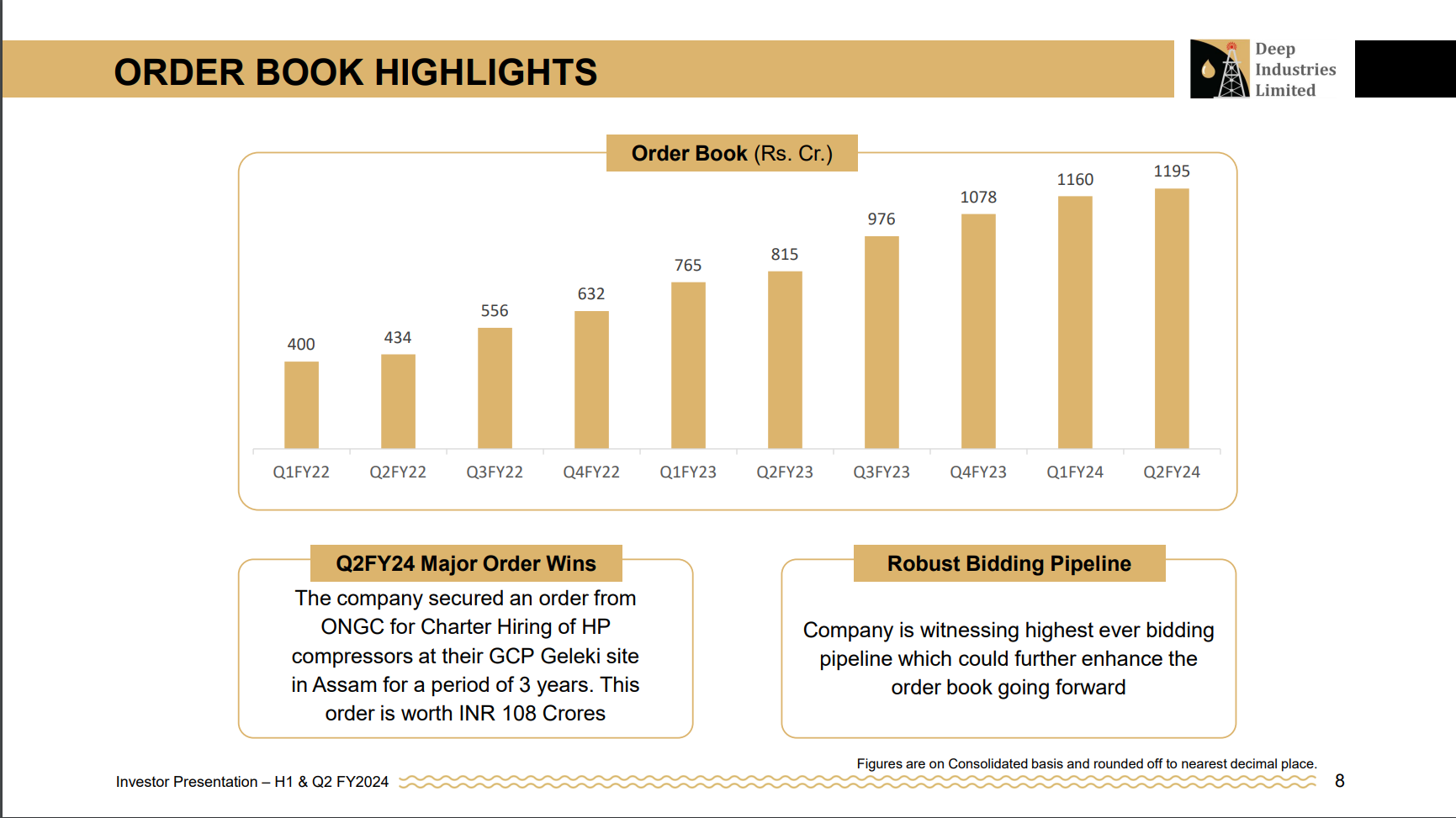

- The order book stood at INR 1,195 crores, reflecting a 47% year-on-year increase.

- Deep Industries was confident about exceeding INR 500 crores for FY '25, driven by the order book and Dolphin Offshore revenue.

- They anticipated revenue growth in Q3 and Q4, expecting to achieve their growth targets.

Funding and Capital:

- Deep Industries reassured that they were financially well-equipped to handle the expected growth in the business. They had minimal debt and were net debt-free.

Dolphin Offshore:

- The company discussed their plans for Dolphin Offshore, including refurbishing a barge and shifting its jurisdiction for potential tax benefits.

- Revenue from Dolphin Offshore was expected to commence in Q4, with strong margins in the range of 60-70%.

Capex Plans:

- Deep Industries had capex plans for acquiring drilling rigs and gas processing packages.

Joint Ventures:

- They discussed two joint ventures, with the first JV failing to qualify for a specific drilling rig requirement.

- The second JV with Euro Gas was still under evaluation, and they expected results in the coming months.

RAAS Segment:

- Deep Industries reported that the order book for RAAS was around INR 50 crores.

- Execution had faced delays due to customers seeking extensions for their projects, but demand was expected to pick up in FY '25.

Order Inflows:

- The company had a substantial bidding pipeline of around INR 800 crores, with high expectations of conversion in the coming months.

- While the percentage of successful conversions could vary, they remained confident in securing significant orders.

Client Contribution:

- ONGC was the largest client, accounting for around 65% of the order book, followed by Vedanta and Oil India.

Cash Flow and Investments:

- The INR 100 crores listed under the “sale of investments” in the cash flow statement represented the transfer of funds from investments to fixed deposits.

Conclusion:

- Deep Industries expressed optimism about future revenue growth and order book conversion, particularly in the second half of FY '24 and FY '25.

- They emphasized a strong focus on margin maintenance and improvement, along with preparedness for business growth.

Overall, the call provided a comprehensive overview of Deep Industries’ financial and operational performance, order book growth, and plans for the future, including the expected contributions from Dolphin Offshore and joint ventures.

2 Likes

Some of the Points, I would like to see in future: (Base on presentation)

1.Implementation of fully mobile units, facilitating swift relocation to any part of the country within a few months. Proactive forecasting of contract renewals enabling optimal resource planning in advance. Minimization of time drag for subsequent optimization and utilization of equipment between contracts for any re-engineering or client related re-configurations as they are finalized in the final 3-4 months of the prior contract period.

2. Expertise in providing Value added services for our clients which in turn improves their revenue generating ability as well as profitability at large and provides a diversified service mix for their product portfolio.

EV: Yes, more or less is same in my calculation.

1 Like

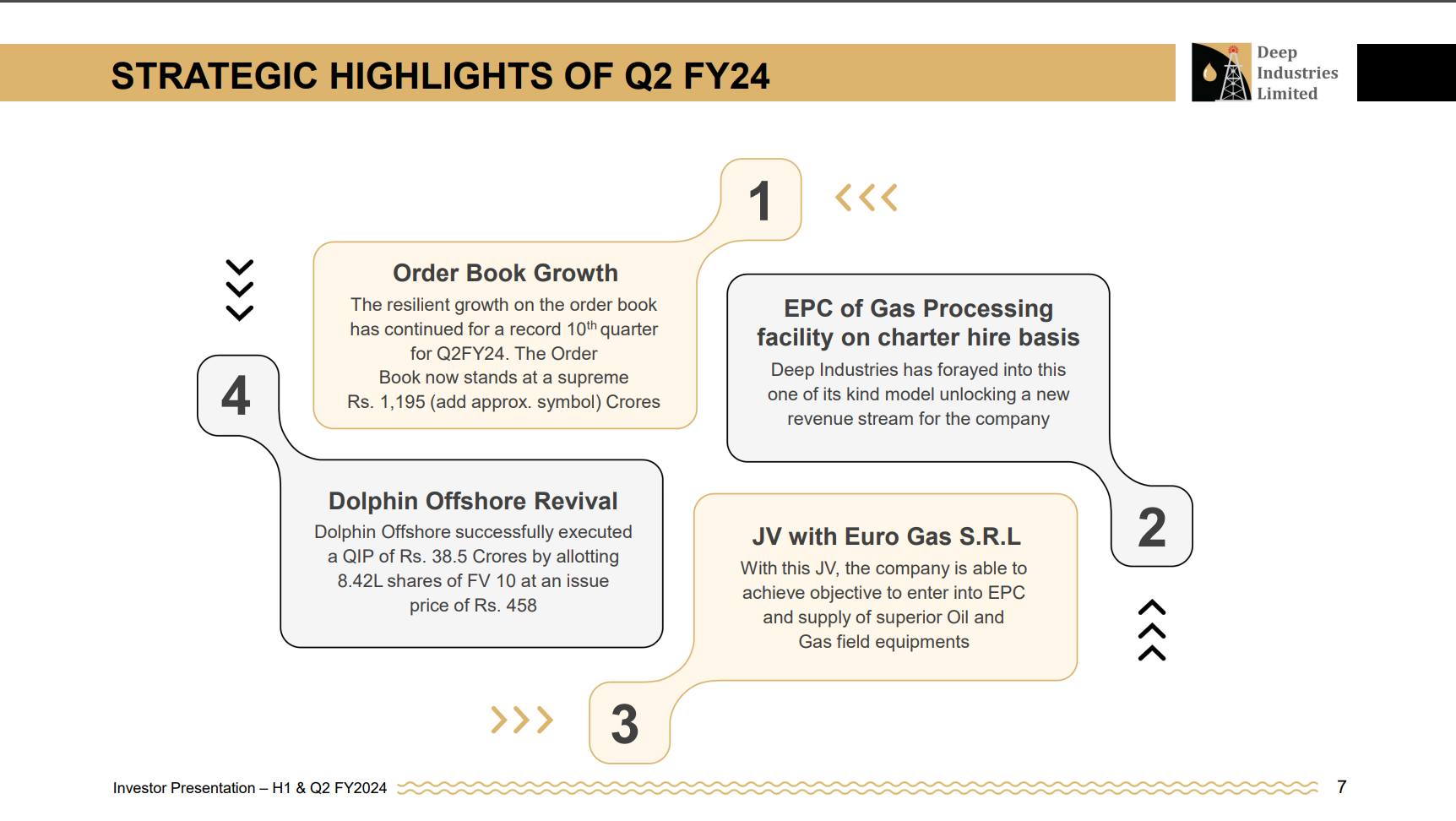

- Order Book Growth: The company’s order book has shown resilience and continuous growth for ten consecutive quarters. It now stands at an impressive Rs. 1,195 Crores.

- EPC of Gas Processing Facility: The company has ventured into the charter hire basis for gas processing facilities, opening up a new revenue stream.

- JV with Euro Gas S.R.L: The joint venture allows the company to enter the EPC and supply of superior oil and gas field equipment.

- Dolphin Offshore Revival: Dolphin Offshore successfully executed a QIP (Qualified Institutional Placement) of Rs. 38.5 Crores, allotting 8.42 lakh shares at an issue price of Rs. 458.

- Order Book Highlights: The company secured a significant order from ONGC for charter hiring of HP compressors in Assam worth INR 108 Crores. Additionally, there’s a robust bidding pipeline, indicating potential future order book growth.

Does anyone have any more information on why they didn’t qualify for the bid with the JV? The con call didn’t quite specify why. Thank you!

1 Like

Any update?? What is happening in the company?

Q3FY24:

• 97cr new awards for the quarter. Order Book at Rs. 1200 Crores.

• International: Deep International DMCC has supplied a modular compression station for a client in Egypt to counter well head pressure reduction and maintain well head gas production. The project was executed on a Build/ Own/ Operate basis with the partner in Egypt.

Middle East Fast Track Compressor Overhaul – The Company has supplied quantity four gas compressor packages for a debottlenecking project in Gulf for a client.

Deep Onshore Drilling Service Private Limited, a subsidiary company of Deep Industries, entered into a JV with Euro Gas Systems to enhance the company’s technical expertise and know how to further support gas field services.

• Beluga International DMCC100% Dolphin owned subsidiary incorporated in Dubai The charter hiring of Dolphin’s Barge would be done under this entity

• Kuwait Oil Company (One of the largest Oil Producer in the world) exclusively shortlists qualified enterprises, with Deep, being one of the selected few. Moreover, the favourable day rates in the Gulf region should potentially enhance our margin expansion.

• The industry exhibits relatively subdued competition, largely attributable to its significant capital-intensive nature, operational efficiencies and extreme discipline in leverage.

• a history of never exceeding a D/E ratio of more than 1, signifying sound financial management and a low-risk profile.

CONCALL NOTES:

• Bidding pipeline of around INR500 crores plus with increasing trend.

• Demand environment is particularly looking very exciting, as fresh large capex plans have been announced by not only the PSUs, but also large private players. Further, the current demand scenario is so strong, the services business like us are operating at nearly full capacity, which is facilitating benign pricing environment in medium to long term. Strong demand environment, coupled with benign pricing outlook is ensuring profitable and durable growth in coming years

• In oil and gas, Vedanta Group Company has announced $700 million investment to enhance drilling infrastructure at its 100 exploratory wells in the country. We remain optimistic about the robust bidding pipeline for Deep, which is expected to remain strong in foreseeable future.

• DOLPHIN OFFSHORE: On a full year basis, expect almost INR90 crores to INR100 crores top line from Dolphin. Dolphin, we are looking operating margin of more than 50%.

We have already started giving some expressions to our clients. We are working on bidding some of the tenders in offshore space. So I think it will still take us a quarter more to get – because there was a lot of things to be done to revive the company, get the documentation done and all. So I think in next quarter, we should be in a position to bid for these tenders. And we can – we are sure that we will have a huge amount of outcome coming in because as it is, there is a huge demand in the industry and there is a lot of vacuum for the services provider in this segment.

• 20-25% sales growth for next FY. So, we are anticipating minimum 25% growth year-on-year in Deep Industries itself. So, the way our bidding pipeline is increasing and the conversion which we are expecting out of this bidding pipeline can definitely help us in growing 25% CAGR.

• Steady state operating margin should be in the range of 42% to 45% EBITDA

• Euro Gas (EPC JV) tender is already bidded and it is under evaluation and we are expecting the tender to convert soon.

• KUWAIT OIL: So, in Kuwait Oil, we got qualified for various capacities of rigs. The tender is already published by Kuwait Oil Company. And I believe it is due in March or April. So, the size is huge, but our company in India intending to bid some of the rigs in that region. So that will depend on the market intel that we are working on. So having said that, getting qualification in KOC in itself is a big task. So, once we have got qualified now, that stands another chance that we would be allowed to bid for those tenders. Outcome, of course, depends on the tenders once they are submitted. But the opportunity is big. In terms, I believe they would be asking more than 25 to 30 rigs, although we are not going to bid for all of them, maybe a few of them. But that will depend as the dates progress near.

• 2 NEW RIGS: Selan rig is already under mobilization and maybe a week from now, the operations will start. Regarding the rig that we had ordered for Bokaro is already ready. We had already done a third-party inspection. It’s lying in China. So, in all probability, we expect that the rigs would get shipped in March and we would be in a position to start the operations probably in April or May.

Q3 and Q4 put together, the quantum of capex would be around INR100 crores.

• Q4 to be better than Q3.

3 Likes

One more point to be added on based on concall:

20-25% sales growth excluding Dolphin and expected full year Dolphin revenue 90-100 Crores.

3 Likes

Can Dolphin🦈 Offshore give extra miles to Deep?

Q1 (Standalone Revenue): Considering the bid pipeline and the current order book that we have, what kind of numbers are we looking for FY '25 in terms of top line, and bottom line internally as a target?

A1: We are anticipating a minimum 25% growth year-on-year in Deep Industries itself. So the way our bidding pipeline is increasing and the conversion that we are expecting out of this bidding pipeline can definitely help us in growing 25% CAGR. (Estimated revenue for the current FY ~ 440-450 Cr)

Q2 (Standalone Margin profile) : what should we consider to steady state operating margins?

A2: State operating margin should be in the range of 42% to 45% EBITDA.

Q3 A (On Dolphin) : All right and that is just for Deep Industries. And sir, for if we add Dolphin as well, that should add another INR80 to 100 Crs, if I am not wrong?

A3 A: Correct

Q3 B: What was the revenue contribution for Dolphin in FY '24?

A3 B: Dolphin in FY '24 is negligible. So – since its major asset is under refurbishment, it has contributed around just INR8 crores in this year.

Q3 C: What kind of operating margins are we looking at for Dolphin?

A3 C: Dolphin, we are looking operating margin of more than 50%.

Part 1:

Now clubbing Q1 & Q3 A: FY 25, Projected revenue of the company

Deep: Rs 450 + 25% incremental revenue or conservatively 20%, then Rs 550 Cr

Dolphin: Rs 80-100 Cr ~ conservatively Rs 50 Cr

Total FY25 (P) Revenue: Rs 600-650 Cr

Part 2:

Q2 & Q3 C: Estimated EBITDA

Deep: Rs 550 X 42% = Rs 230 Cr

Dolphin: Rs 50 X 50% = Rs 25 Cr

Total FY25 (P) EBITDA = Rs 255 Cr (~ Minimum Rs 250 Cr)

And Maximum Side ~ 300 Cr

4 Likes

Non cooperation by Issuer

CRISIL Ratings has been consistently following up with Deep Industries (DI) for obtaining information through letter and email dated January 05, 2024 among others, apart from telephonic communication. However, the issuer has remained non cooperative.

‘The investors, lenders and all other market participants should exercise due caution with reference to the rating assigned/reviewed with the suffix ‘ISSUER NOT COOPERATING’ as the rating is arrived at without any management interaction and is based on best available or limited or dated information on the company. Such non co-operation by a rated entity may be a result of deterioration in its credit risk profile. These ratings with ‘ISSUER NOT COOPERATING’ suffix lack a forward looking component.’

I learnt from @Worldlywiseinvestors that it is a red flag … not personally but through their videos .

Your views please noob here

Credit Rating Letter dated 04012023 (1).pdf (1.2 MB)

Actually, they have discontinued with CRISIL and shifted to Care!!!

4 Likes

Deep Q4 FY24.pdf (7.3 MB)

Quarterly and Annual result - FY24

Management is very confident about ~ 25% yearly growth and maintained overall EBITDA margin ~ 42% + in next 2-3 years

Q4FY24:

• Order book of INR 1210 crores, reflecting a 12% year-over-year growth.

• Innovating into Charter Hire of entire Gas Processing facilities

• Owns & Operates 9 Workover Rigs with capacity ranging from 30T to 100T, 5 Drilling Rigs with capacity of 1000Hp.

CONCALL NOTES:

• We have added two new drilling rigs in previous quarter of which one has started operation in February 2024 and the other has started operation recently in May 2024. So both put together, it can add INR 5 crores a month going forward.

• Management has delivered on revenue growth guidance of 25% and EBITDA margins of 42% (including other income)

• BIDDING PIPELINE: Highest ever bidding pipeline – 1000cr (This is generally 500crs).

Our routine business has exceptional response in almost out of INR1,000 crores, almost INR700 plus crores is from our regular services, including rigs, compression gas processing and integrated jobs. I would say more than 70% 75% is from our current services portfolio itself.

NEW SEGMENTS: And there are a few good opportunities. We are working on it, which includes production enhancement contracts and enhanced oil recovery business which we believe can change the table, so we have started bidding those opportunities as well.

• DOLPHIN OFFSHORE: We anticipate the revenue stream to commence in the first half of FY '25.

For barge, our expectations are EBITDA around 60%- 65% for that particular asset. On full year basis, revenue of almost INR90 crores to INR100 crores is expected from that particular barge. 65cr should be for FY25

OTHER SEGMENTS: We have begun exploring platform supply vessels opportunities in both local and international markets. Early indications suggest a substantial demand for PSV services.

And in addition to PSVs we are also looking for some diving support systems, which we already have to mobilize. So as a strategy, currently, we are focusing on 1 asset to put in operation, 1 asset will start operating, we’ll add other assets to get into operation and we’ll definitely, going further, we’ll acquire a few more assets as well.

• INDUSTRY TAILWIND: In February 2024, Prime Minister announced that the country is expected to see investments worth USD 67 billion in the gas sector over the next 5 years to 6 years. This focus on domestic natural gas production is expected to attract significant investments given the goal of the increasing gas share in the primary energy mix to 15%. These developments are reassuring growth drivers for our company

• Our ex-goodwill adjusted ROCE has improved to 12.42% from 10.27% previous year. And our ex-goodwill adjusted ROE has improved to 11.83% from 8.18% previous year

• MARGINS TO IMPROVE: our margins would definitely improve as the year passes. And we have always been maintaining our EBITDA above 40%. So yes, we are very much confident that with new service mix added into our revenue stream, this margin will tend to improve

Dolphin margins to be 55-65% range so FY25 Margins will be better than FY24 as dolphin sales kick in

So, in FY '25, we expect it should reach 45%. And in FY '26, it can further improve as well. (Including other income)

• GROWTH GUIDANCE: “Minimum’ 25% sales growth. Orderbook is 1200cr with 2.5-year execution timeline. So, 1200/2.5 = 480 (that’s 12% growth over fy24 revenues of 427) + Dolphin offshore revenues of 60-65cr = 540-545 cr sales in FY25 at MINIMUM. Any new orders will further increase the growth

• Didn’t get business for Kuwait tender.

• INR196 crores is the total investment. And the other income is largely interest and mutual fund income

• We are operating currently for more than 40 different contracts

5 Likes

With another 25-30% sales growth year along with improving margins and new segments being added, all backed by robust industry tailwinds, the future seems promising for Deep industries

5 Likes

Any one knowns what about this acquisition?

What Deep Industries going to get from this deal?

Investor presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/39749e88-c57e-4ccb-90fe-02644fd5c25c.pdf

2 Likes