As you all know indexation benefit for debt funds will be removed irrespective of the time of investment and will be taxed as per slab, from April 1st.

I have debt MFs and one of the reasons for choosing them is because of the indexation benefit, and I do move regularly the gains from equity to debt, and choose debt funds for this, because of the irregular nature of equity gains, and now I have to look at other alternatives, if any. I am guessing some of you must be in the same boat, so I would like to know about your thoughts and the route you want to take.

Although, the other advantages of a debt fund over a FD still exist, this will have some impact, and as such, an appropriate if not a replacement product have to be searched.

MF houses have started to change their fund mandate within the confines of the SEBI categorization, and some clarity will emerge in the coming days of this FY, but I would like to know about your thoughts.

I think Equity Saving schemes will bump up there equity exposure to 35% to take advantage of indexation. They have option of taking real equity exposure or increase equity exposure to arbitrage. But arbitrage portion would result in only liquid fund like returns. But something like 25% equity and 10% in arbitrage should not impact returns a lot. .ome like HDFC already has 35%+ exposure. These would be good option to take advantage of indexation. And investors can reduce equity exposure elsewhere if they feel equity exposure if higher.

Yes, going for hybrid funds is one option, but pure debt options should be looked at first, if someone wants to keep their equity and debt separate. Even with hybrid funds, there could be some short term losses, unlike pure debt funds, where the chance of that is very low.

AMCs are coming up with changed mandates, so may be there could be some reasonably suited category, which are relatively better for the long term.

Just to clarify, for investments made till 31st March 2023 will have LT taxes as well as indexation benefits in future, right? I am asking as you mention “irrespective of the time of investment”

Of course, debt funds too can have losses for a few reasons, but for the most part they have been good except for a few instances in the past few years. Liquid, MM, UST have been good.

For someone who shifts the gains from equity to these debt funds, and with time these funds grow, when indexation is removed, the impact could be big. So despite the occasional downgrades and defaults, some exclusive to FT like fund houses, debt funds as a category have served a purpose for many.

Good opportunity is for chit fund network that operates among close trustworthy group…

I have seen many professionals working & being part of such group, but officially anything and everything which will come to replace debt mf, will be brought under taxation…

International Funds fall under the equity bucket and will have high beta.

I think OP was asking if there are any alternatives in fixed income space other than FD, I suppose not. Debt Funds have lost their charm but people who are interested in deferring their taxes can still stick with them, considering all other risks.

Now, this could play out in MFs trying to outperform FDs by buying riskier bonds and the conservative ones could lose some market share.

Yes, looking for a suitable debt product, that could match with debt funds, satisfying the attributes of debt funds.

Yes, MFs may buy riskier bonds, but since FT fiasco has happened in not so distant past, looks like the PFs of the funds should be checked from now on, so as to see if there is any new inclusion of lower grade bonds.

Maybe the AUMs of debt funds will decrease in the coming months.

I have funds parked in liquid funds, which i need after 5 years and over as a part of my debt allocation

They usually earn like 4 to 6 percentage interest

Given this new tax situation, shd i move them to long duration maturity debt fund , before 31st, as these funds prob give 8 to 9 percentage as of now?

Also would i be able to pull it off. As I would have 5 days only to execute this

A lot of people may do the same, so there could be demand for such long term bonds, and the funds may have to buy the bonds at higher rates, so some profit may be lost here.

Also, long term interests rates may or may not happen the way we think they would, and if rates start falling in 2 years, the remaining period of your investment may not yield much.

Calculate how much would you gain by staying in the same funds, how much have liquid funds appreciated since the rise in interest rates, and how much would you gain if you sell and buy new funds etc.

I have liquid funds too, not yet to decided of anything.

Existing investments in Bharat Bond which merges into another Bharat bond retains the tax benefits. So Investments in Bharat Bond 2023 which merges into 2025 retain benefits … investments done before 1st April in say Bharat Bond 203X which IF merges into any future Bharat bond would retain the benefit… and so on in perpetuity.

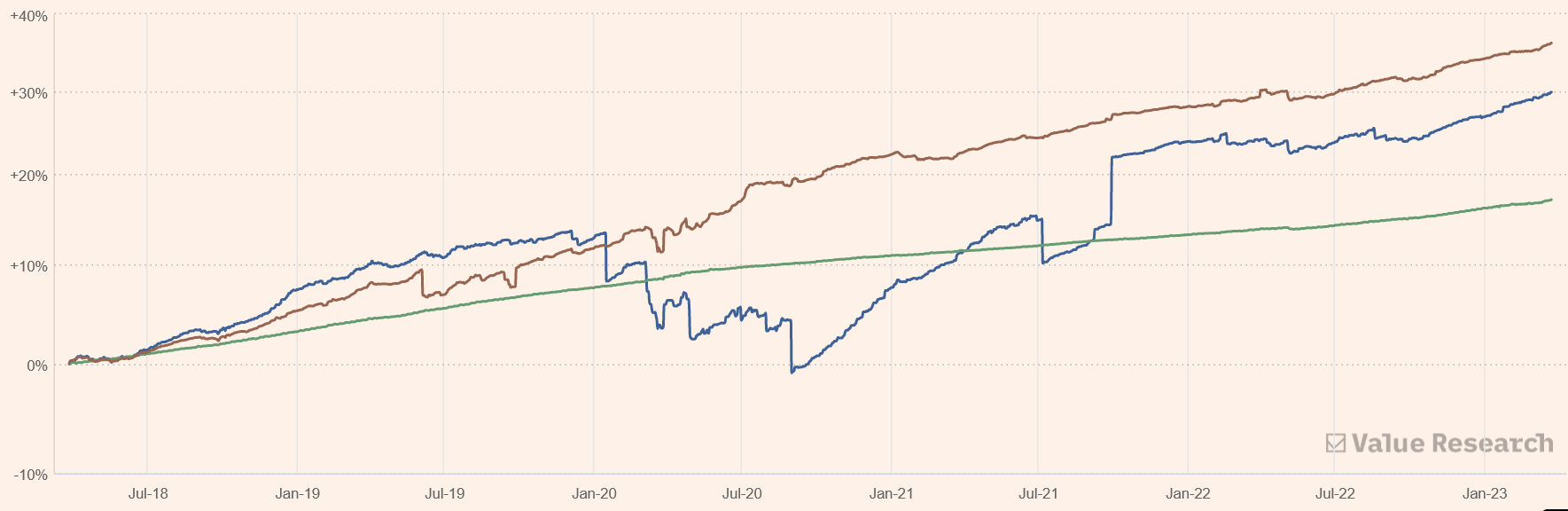

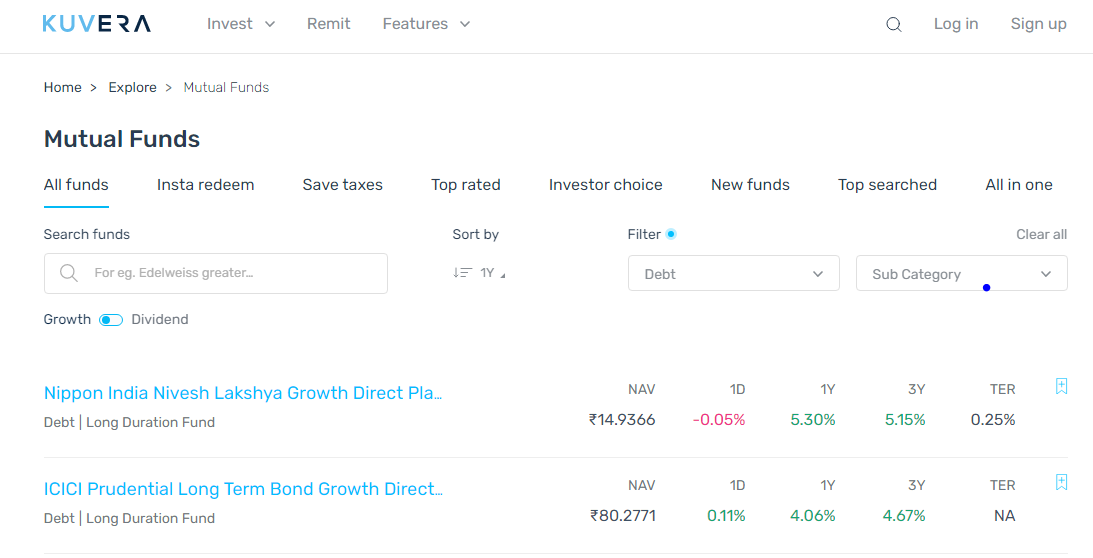

8 to 9% in debt funds? I am yet to see them anywhere in last 3-4 years…maybe some odd outliers will be there but even the long duration (sub category filter below screen shot - long duration)…

There used be such returns in debt funds some 8, 9 years ago. Even liquid funds gave such returns. So a possibility of such returns with rising interest rates in longer duration funds may exist.

Most of my emergency funds are in debt funds and most of them will complete 3 yrs from April to Sep 2023.

I am considering some part of above proceeds to arbitrage funds and rest to decide : balanced/conservative hybrid funds may be an option if can get FD returns with lowest possible risk

Yes, they are options, but it is said that as the participation has increased in the market, arbitrage opportunities are not available like in the past, so returns could be low and hybrid funds despite having debt component may go down at the time of our redemption.