I believe that, for some of the long term Financial goals, an investor can use PPF as an option provided you do not want to re-invest those funds in Equity in next 5-6 years. An investor can only deposit minimum balance of Rs. 500 at the beginning of FY, and then deposit booked profit from Equity for Debt: Equity balancing for few financial goals.

This is off course not useful if you need the cash back after few months or years. For that, Debt Funds and FD/RD is still better choice. There is no point in experimenting with other risky options just to save some tax. Few other options like tax free bonds are also interest rate sensitive so could be risky.

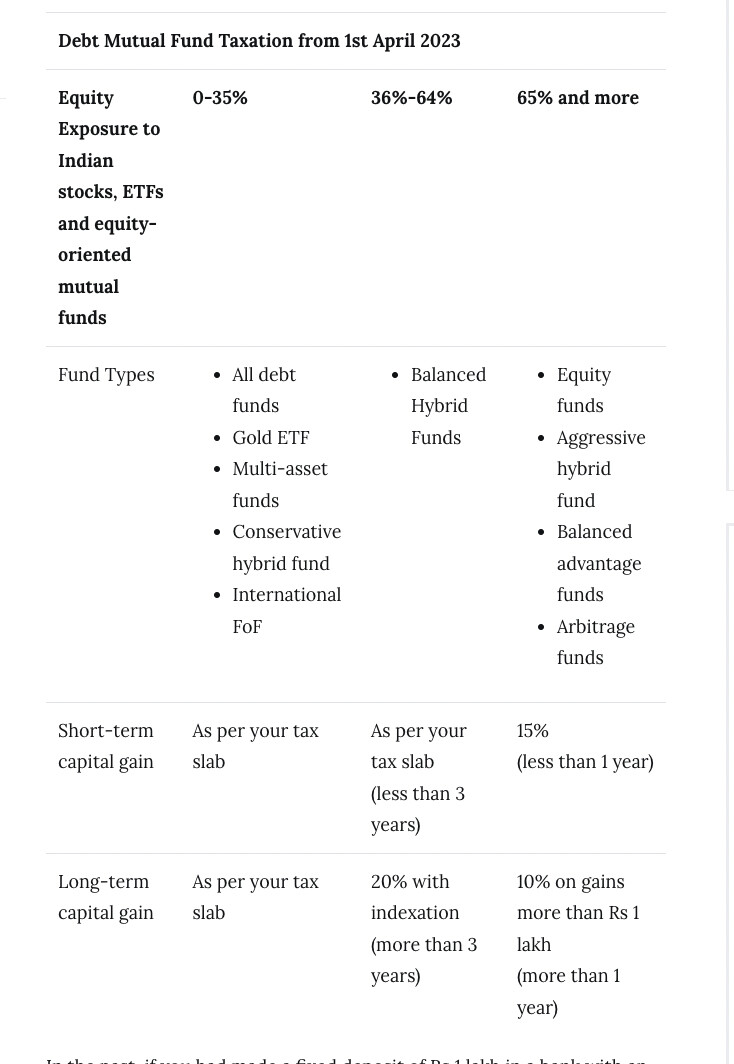

Simple options like Liquid Funds and Money Market Funds are still good provided an investor is ready to pay the tax.

This is my initial analysis and it may change as we get more clarity.

The max PPF deposit limit is 1.5L. It has a 15 year lock in.

I am suspecting that the next taxation dragon will be on equity LTCG and even the EEE in PPF might get a splash of red with tax…who knows?

With on the ground inflation anywhere from 25-50%/year in India, 22.5 L (15x1.5) in PPF after 15 years, may not even get through an year of rent !! and that is the sad reality

Yes, Equity LTCG, STCG, Real Estate LTCG and all other tax free instruments will be on radar.

Since fiscal deficit is on higher side for prolonged period, there will be increase in taxes going forward. This concern is there.

There are not much alternatives in such case.

Real life inflation is always much higher than the mathematical numbers, so Equity investments would remain one of the ways to battle it.

don’t forget the draconian wealth tax…that might be on the way too. The sadists and the politicians (read an awesome quote 'the only time politicians tell the truth is that when they call each other as liar")…will they dare attempt a tax on agricultural income? many of them are masquerading their black in that

I am not too sure of PPF removing EEE status for PPF, considering there are many who have invested in PPF compared to equity, so may be in the future, but not of a concern now.

So despite the interest rate getting reduced, it suits perfectly as a debt component for long term goals.

I have debt MF purchase transactions(money deducted) dated 29th & 31st March, but allotment NAV is that of 3rd April, will these purchases be eligible for indexation benefit ?

With the removal of indexation benefits, the debt funds may have lost a bit of its sheen. The point is instead of debt oriented mutual funds which other options should a SIP investor with a 3-4 years horizon look at. Are arbitrage funds a good alternative to debt funds?

Arbitrage funds: Taxation benefit (STCG @ 15% & LTCG @10%). Low risk. Pre-Tax returns are in 5-6% range.

The 1 & 3 year pre-tax return of Kotak Arbitrage fund is 6.92% & 5.27% respectively

The 1 & 3 year pre-tax return of HDFC Corporate Bond fund is 7.37% & 5.07% respectively

Nowadays FDs are giving 7%, I don’t understand the rationale in buying corporate bond or some other convoluted MFs which offer little risk premium. I personally am using using HDFC Gilt and PPFAS Liquid Fund, along with FDs.