|

Revenue contribution |

EBIT Contribution |

| Fertiliser |

9.3% |

4.7% |

| Shriram Farm Solutions |

29.1% |

16.1% |

| Bioseed |

9.5% |

16.5% |

| Sugar |

22.0% |

-19.1% |

| Hariyali Kisaan Bazaar |

6.6% |

0.0% |

| Chloro-Vinyl |

19.5% |

82.0% |

| Cement |

2.1% |

0.6% |

| Others |

5.0% |

-0.7% |

| Inter Segment |

-3.0% |

|

Numbers are for FY 2012-13

I have tried to look at the current business prospects, prospects of individual business in general and then have done a valuation (which attracted me to the company in the 1st place).

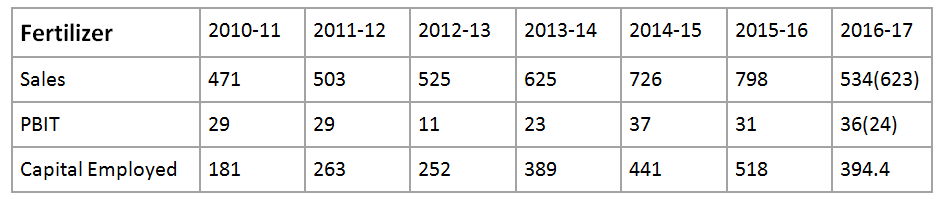

Business is surely going through a rough patch at the moment- fertilizers and sugar (for obvious reasons- fertilizer in absence of new urea policy and sugar due to higher cane price in UP and a weak global sugar market), are in trouble. Last couple of quarters was not so good for the seeds business as well with sale return from the two foreign countries it is operating and 3rd quarter as always will be seasonally weaker.

Chlor-Vinyl business is doing well though the cycle has started to come off and realizations have come down in last couple of quarters. Barring the capacity addition (which will come in next 3-4 quarters and will add about 4% capacity in chlorine business), think the upside in EBIT contribution is limited at the moment. PVC business though is going strong and there is a scope for some growth there (5-10% yoy).

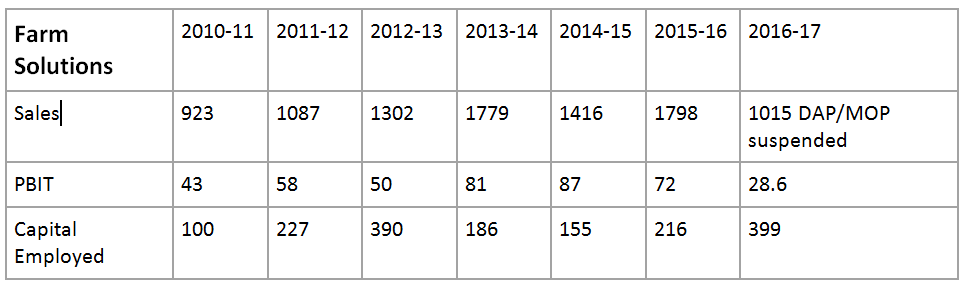

On the positive side farm Solutions is doing well- which is the trading business of imported bulk fertilizer (DAP etc with negligible margin) and some value added products like Pesticide etc (5-10% margins). Here also there is a receivable issue on subsidy from the government which is increasing the working cap requirements.

Business Outlook- Personally I donât

think that

the situation in the fertilizer and sugar segment is going to improve in the near term. Post-election we might see some clarity emerging on them but thatâs a tough call to take and is a known unknown factor. I wonât buy the stock betting on that event happening too quickly though I belong to the camp that believes it would happen eventually.

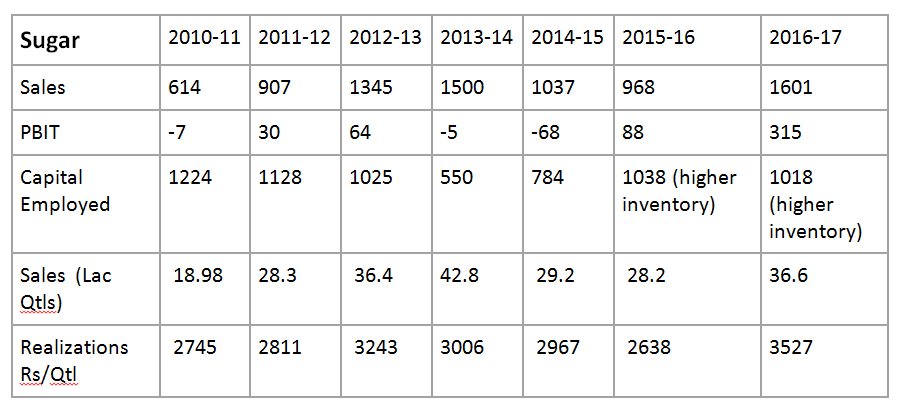

Global sugar cycle is obviously down- I have not studied much on this though I have seen some threads in the forum exclusively on this. I have taken a view that this is not going to change in 2014- but we might get some indication by the middle of this year looking at demand supply projections for 2015.

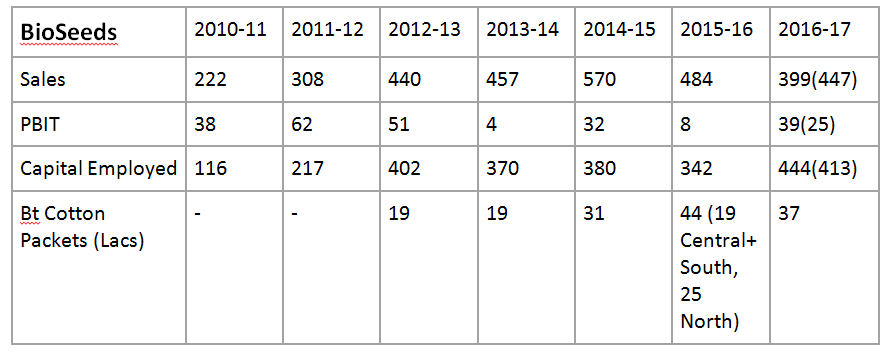

Seed business- though the last couple of quarters were bad outside India on account of sale return (Management has said that this is on account of inventory stuck in trade channels and not on quality issues but you will tend to take this with a pinch of salt), I think the situation in India is relatively better and it has gained a lot of ground in cotton seeds market in North India. In South India it has started aggressively and though the competition is tough I would tend to think that given its success in North Indian market it should make good inroads (quality comments is positive though I have not been able to verify it independently). Management is also confident on this- looking at the transcripts of the calls. Management thinks that over medium term it can maintain a growth rate of 25-30% in this business which seems reasonable to me. One comment here is that sale price is capped by state governments(so not a runaway story) and such higher cost is difficult to pass to the consumers, but with scale and experience I think the company should be able to increase margins in this business. Also, to maintain such kind of growth not much capex is needed which is good.

Farm Solutions- Farm Solutions outlook is closely linked with outlook on agriculture. This is low margin high volume business and company has given a CAGR of more than 50% over past 4 years. And expects to maintain 30-40% kind of growth in the medium term- again investments required to maintain the growth are not high. Company is also focusing on higher margin products- company has already established a very good distribution network and dealers and should benefit from that in the medium term.

Chlor-Vinyl- This is the business

which has contributed to more than 70% of group EBIT in all the last 4 years so effectively it has funded the losses in the rural retail Hariyali business. Margins have increased on account of higher realization (uptick in the chlor-vinyl cycle) as well as through cost rationalization. Company is in advantageous position on account of its captive power plant which is a very high contributor to total cost. Although the realizations have come down in the recent past and the cycle has turned, company is well placed in the segment (captive power) but not insulated. Demand of end products is still growing in India and though additional capacities are coming up India is still importing. Rupee depreciation has also benefitted the company.

PVC business is directly linked to economy of the country- Import duty is less India currently imports 1mmtpa and total demand is ~2.3mmtpa. No additional capacity is coming on account of lower import duty. Company is better placed due to in house chlorine and power.

As part of value addition company has also expanded in to PVC windows business under the brand Fenesta Building Systems. This manufactures UPVC windows (Un-Plasticized PVC) and door systems under the brand "Fenesta". Business has broke even in the last quarter and company expects to grow substantially in this segment- both retail and as well as industrial. Sales for this business was 42 crores in 2Q 2013-14 and it was profitable- company expects this to grow by 25-30% every year.

As per company a factor which can potentially drive demand of PVC is the expectation of per capita increase in the consumption of PVC resin which is currently at about 1.6 kg in India as against countries like Brazil which is about 4.5 kg and China which is about 9.2 kg

Hariyali Kisan bazar- Company has substantially downsized the operations in this business and only selling fuel which is a profitable business. Donât expect this business to grow. Company is disposing off lands- book value of which was 220 crores as at 31st march 2013. In last 2 quarters company has done 7-8 deals. Company expects to at least realize the book value over next 12-18 months which will directly flow through cash.

So overall the story- Seed and farm solutions to provide growth (with very less capex needs) though the business would remain quite volatile quarter over quarter- linked to kharif season in India. Chlor-Vinyl business will provide stability to earnings. While fertilizer and sugar business will remain the problem- might be even loss making in near term (facing a lot of head winds) and also will block a lot of working capital- government subsidy payments are very slow in last 3-4 months (current subsidy outstanding 420 crores which normally is in range of 200-225 crores)

After the story we come to the valuation - This is what attracted me to the company- company trading at 0.65 times its book value with decent growth expected in the medium term.

On the paper valuation surely looks attractive- with current m cap of 933 crores and a debt of 1000 crores the company is available for 2000 crores. Take out the 200 crores which will get realized from land in the Haryali Kisan bazar the value comes to 1800 crores. Again, the working capital is at elevated levels at 950crores from a level of 636 crores in FY 11-12. Out of this 200 crores is the land but balance is on account of higher government receivable- accounting 100 crores out for that the company is available for 1700 cores.

Now coming to individual business valuation:

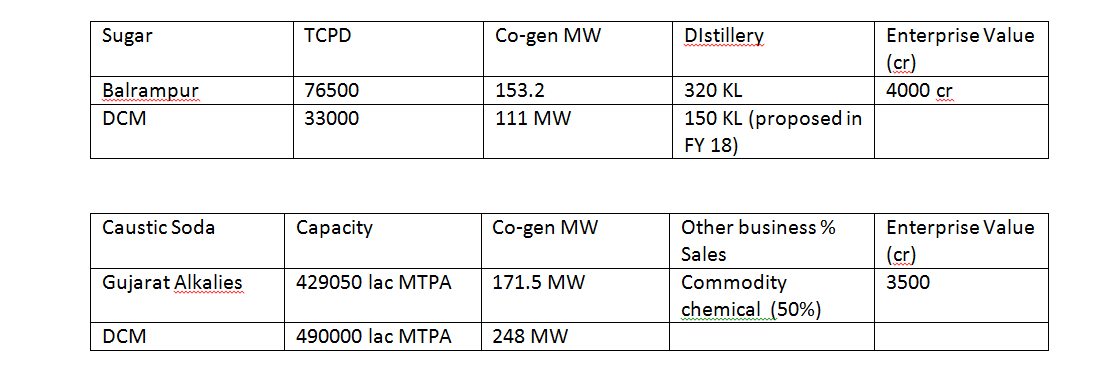

1st is the Chlor Vinyl business- two parts here- Chlorine and Plastics- Chlorine business capacity is approx. 245000tonne- valuing this on the basis of an expansion taken by the company (adding about 10K tonne of capacity for about 30 crores) valuation comes out as around 735 crores. With a business earning close to 250crore of EBIT and 170crores post tax (assuming both chlorine and plastic business to be of similar margin profile), this is on lower side.

Plastics business- have not dig deeper here- business is good, demand is good, turnover for 2012-13 was close to 300 crores- assuming 27-28% margin and 10% growth and a tax rate of 30%, I think a multiple of 5-6x is OK - using this we get a value of approx. 300 crores (1x sales)

Fertilizer Business has 3.79 lakh metric tonne annual capacity- surely the business is barely making profit at the moment and a lot of capital is blocked. Historically this business has earned a margin in high single digit. Conservatively valuing this at 75% of capital employed (most of this is their money anyways as subsidy would take a lion share of this, LNG payment is surely upfront) in the business we get a value of 150crores. Though my guess is that it would be valued higher but better to use this number till we get clarity on government policies.

Shriram farm Solutions- did turnover of 1302crores in 2012-13 and earned 51crores at a margin of 3.9%.Company expects a 30-40% growth in this business and expecting margins to improve little on account of scale and value added products we are looking at an EBIT contribution of 100 crores in 2 year time frame. Valuing at 6-6.5x we get a value of 320crores which is surely conservative if we are believing those growth numbers.

Bioseed Business- this

is a promising business with 440 crore turnover and 51crore EBIT in 2012-13, growing at 25-30% in the medium term. Though the business is more valuable for the sake of simplicity I give it the same value as the farm solutions business at 320 crores.

Sugar business- 4 factories in UP with total turnover of 1325 crores- business is in a downturn but makes about 50crore profit in a decent year- value this at 400crores (current capital employed is 774 crore and a lot of that is inventory).

Other residual business we value at 100 crores- this include Hariyali Kisan bazar, Cement, textile, and fenesta business- 420 crores turnover

Now, in addition the company has a captive power plant of 270MW- in the sugar plant and in Kota- admittedly the benefit of this is passing through the profit and loss account, but in the valuation above we have not considered any premium valuation on account of this. Generally a power plant coal based cost around 5 crore per MW, this gives a value of 1350crores- though this has not been captured fully in the valuations above, letâs give a random 50% discount- this gives a value of 675 crores.

Overall this gives a value of business around 3000crores-giving a conglomerate discount of 30% brings the value down to 2100crores- reduce 1000 crore of debt, add to this 200 crore of land and 100 crore of current excess working capital we get a value of 1400crore which compares to current market cap of 950crores (around 45% upside).

This is very much a pessimistic scenario-What could go wrong here, probably not much- sugar is a cyclical business and will turn around (company can survive the downturn)- fertilizer- India imports a lot and government would not do such a thing to kill the domestic players though it may remain in government controlled mode for a long time capping the upside.

Other businesses are also valued conservatively- seed business, agri solutions and chlor-vinyl. Recent deals in chlor Vinyl business are done at higher levels. Captive power is also more of an upside provider.

So the downside is very much limited even if the quarterly results are bad this time round- how much upside is debatable but with the current earnings, probable earnings growth in the agri businesses, presence in agri seed sector, probability of reforms in sugar and fertilizer sector, fair value of the company is much more.

Comment on management- Promoter familyis fullyinvolved in the business- they have good grip over numbers and business which is evident from the call transcripts- good disclosures- quarterly call transcripts are available on company website for last 5 years. Ajay Shriram, Chairman & Senior Managing Director and Mr. Vikram Shriram, Vice Chairman and Managing Director are promoters.

Mr. Rajiv Sinha, Joint Managing Director; Mr. Ajit Shriram, Deputy Managing Director and Mr. JK Jain, CFO of the Company

Triggers-

- Announcement on spinoffs or sale of some divisions- a lot of talk in the market I see on this but this is not going to come in a hurry.

- Recovery in sugar prices

- Margin and volume improvement in seeds and agri business- 1-2 years time frame

- Fertilizer policy clarity- again not coming in a hurry

So overall- a very solid company with very limited downside- upside is good if you are going to hold it for 2-3 years timeframe- many triggers but uncertain- can double or even triple from these levels. Need to weigh against other investment opportunities.

Not invested at the moment.

Views invited.