Thanks @Anant bhai for presenting a very detailed thesis. I have been reading up on the company and following are some notes →

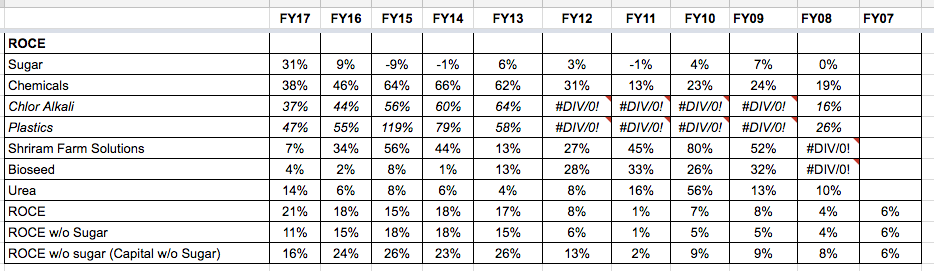

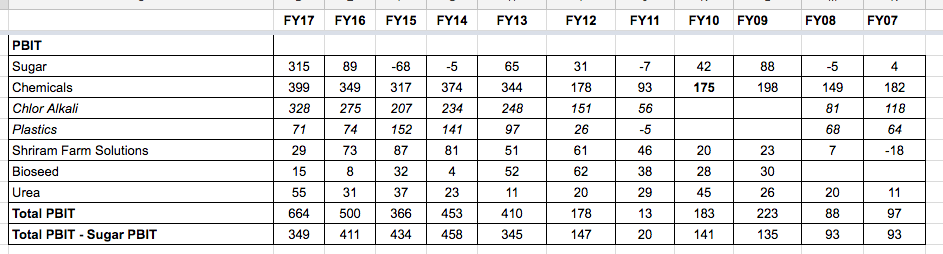

ROCE Data

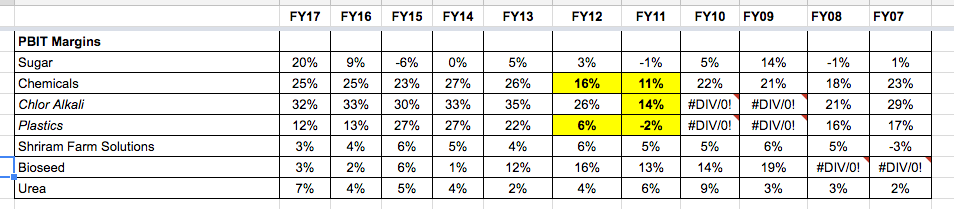

PBIT Data

- As it can be seen from above, Chloro-Vinyl business is the main business that generated a lot of cash and warrants spending more time. I feel that this business will determine the base valuation for the business.

- Sugar is in the cyclical upturn from FY16 into Q1FY18 and needs to be monitored. As DCM is conglomerate, they have some options to deploy the bumper cash generated by this business in good years. So far the cash is going into good businesses like Chloro-Vinyl/Fenesta/BioSeeds.

- BioSeed has vastly underperformed since FY14 with poor ROCE. Seed businesses generally have very good economics (PBIT margin of 20%+) and with kind of R&D spends (8-10% of sales) company is doing, it would be good to get more information about underperformance.

CHLORO-VINYL BUSINESS

Since caustic soda and PVC resins are both commodities and are supposed to be cyclical, it is important to understand the cycle.

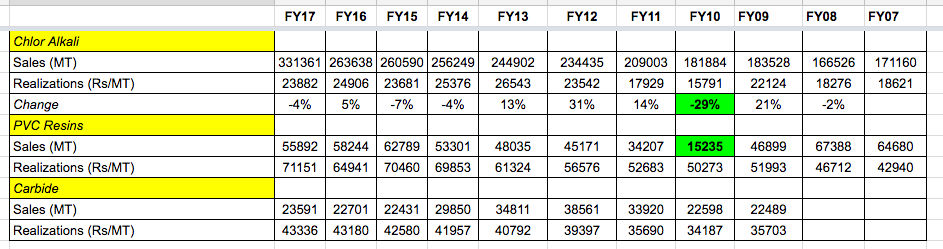

As it can be seen from above data, FY10, FY11 are the two years in which caustic soda realisations went from 22k to 15-17k & sales of PVC resins declined from 46k to 15k-34k.

PBIT margin picture also confirms the same with caustic soda margins dropping below 20% in FY11, FY12. Plastics business recorded negative margins in FY11 and 6% margins in FY12.

Sales

So let’s look at what ARs say about these in these years →

Chlor-Alkali

FY08: ECU prices are at $500-$530/tonne

FY09: ECU prices touched a high of $650/tonne and then crashed to $250-300/tonne post Oct 2008 (Lehman Crash)

FY10: International prices dropped to around $5 FOB & domestic prices dropped by 50%.

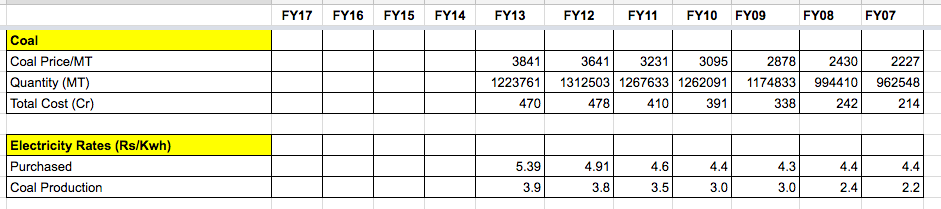

FY11: PBIT dropped (from 175Cr to 93Cr) because power realisations dipped below the cost of production. The company used swing capability to produce more chlor-alkali products compared to power, coal prices hit the margin.

FY12:: Higher RM costs (Coal, Salt etc.) caused lower margins in Chloro-Vinyl business.

FY15: Chloro-Vinyl prices fell due to global decline in the commodity prices.

FY17: The company reported chlorine sales as negative 63Cr.

Q1FY18: Power costs were on higher side due to higher coal costs.

So my conclusions →

- Chlor-alkali prices depend on international prices and any major crash (like FY08) which causes global GDP to go down might impact ECU.

- Since company has large portion of of its power generated from coal, coal prices have a bearing on margins. In Q1FY18, due to higher coal prices - bottomline did not grow as fast as topline in this business.

- The company had option of comparing realisation in power vs. caustic soda/PVC and maximising profit. Question in mind: Was this a one time opportunity because of policy mess (coal block) around FY11-13? What is current trend? At what ECU vs. Power Unit cost one makes sense over another?

If company does not have power option then next downturn in chloro-vinyl might hit company really bad.

One thumb rule about cycles that I learned from a friend is - upturn/dowturn = time taken to put up new capacity e.g. In gold mines, up-cycle can last for 5+ years as putting up new mine takes a long time. Since Chlor-alkali capacity can be usually operational within a year, the cycles shall be short at least from supply side of view.

Another thing is - since DCM (and GACL, Andhra Sugar) continue to report decent absolute margins & ROCE even in bad years, these players might have some advantage. To get a textbook demonstration of cycle, we might have to look at little bit weaker players.

Following table captures various data →

PVC

The company has 70,000 TPA capacity of PVC resins and 112,000 TPA capacity of Calcium Carbide. 80% of Calcium carbide capacity is used to create acetylene needed for PVC resins and 20% is packaged and sold. PVC consumption depends on GDP growth and primarily growth of Infrastructure + Real Estate sector.

Lower chlorine prices help the margins in the PVC business but impacts the Caustic Soda business. In that sense, they are somewhat counter cyclical. Recent capex announced for Anhydrous Aluminium Chloride shall hopefully solve this problem and provide best margins for both the businesses.

Another question, barring bad years, ROCE of plastics business has been consistently 50%+. Why isn’t there capacity expansion in this segment if India imports 1 MTPA PVC Resins?

One AR mentions that capacity expansion is halted due to lower import duty & a lot of unregulated imports. Still true?

OTHER

DAP/MOP/SSP

- In FY17, the company stopped trading of DAP/MOP fertilisers but not SSP. What is the difference in economics/subsidy of DAP/MOP vs. SSP?

- I almost want to say that stopping the trading of DAP/MOP is good capital allocation decision but company had stopped and restarted DAP/MOP trading in the past as well (Stopped DAP/MOP trading in FY08 and restarted in FY11).

Views Invited.

Disc - Invested, more than 10% of portfolio. No activity in last 30 days. My views are biased due to my investment. Investors are advised to do their own due diligence before investing.