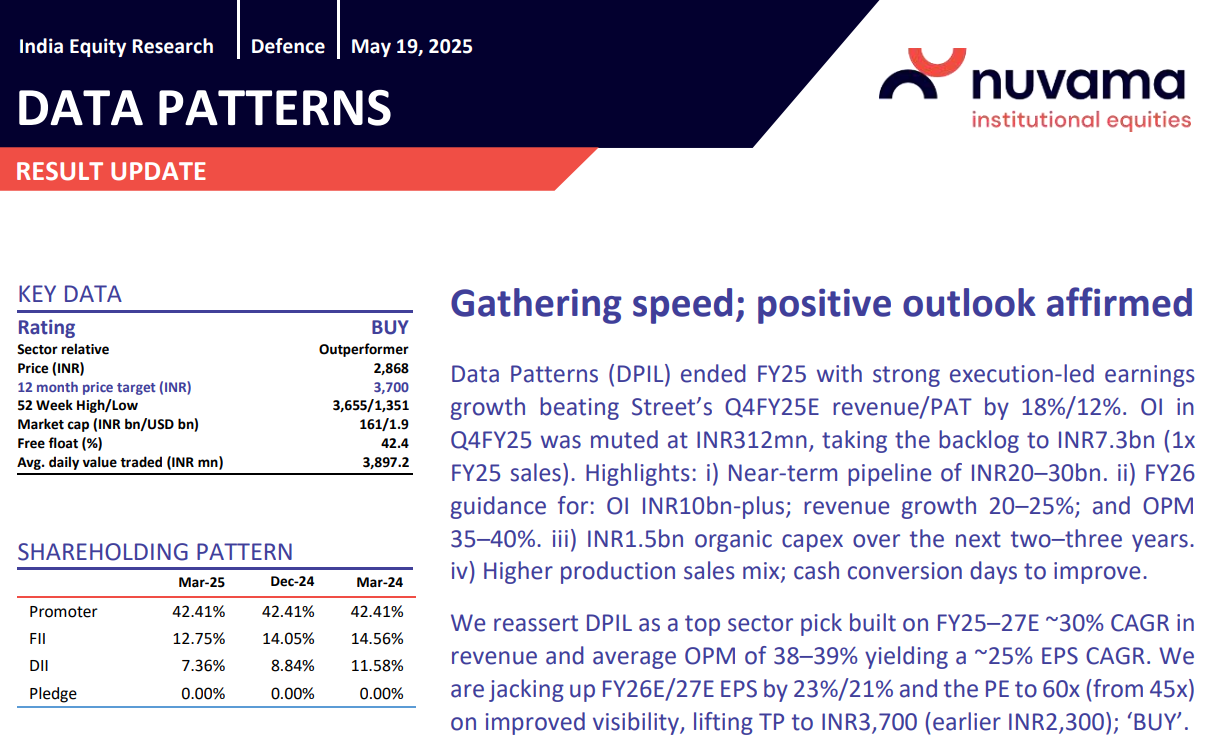

Nuvama increased target to 3700 from 2300

5 Likes

Super results of Q2:

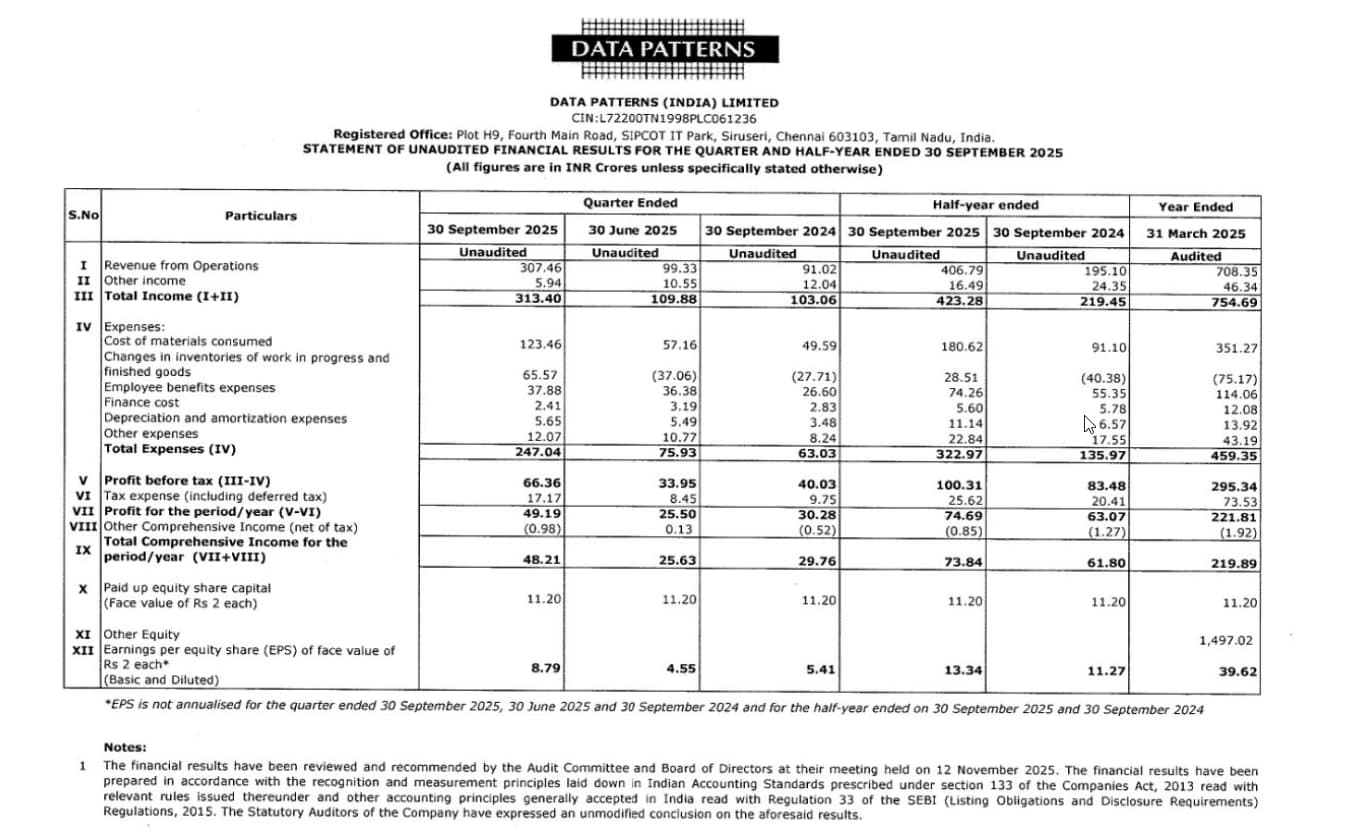

Net profit of ₹49.2 crore for the quarter ended September 2025, up 62.4% year-on-year from ₹30.3 crore in the same period last year.

Revenue for the quarter rose sharply to ₹307.5 crore from ₹91 crore YoY. EBITDA increased 97.4% to ₹68.1 crore from ₹34.5 crore in Q2 FY25.

Worth Noting: The company’s gross margin for the quarter was 38.52%, down from 75.96% in Q2 FY 2024-25, primarily due to the delivery of a strategic low-margin contract. The company expects to achieve its regular historical margins for the remainder of the year.

4 Likes

Q2FY26 Concall Notes:

- Revenue 238% YOY, PAT 62% YOY.

- EBITDA Margin 22% vs 38% YOY. Q1 at 32%.

- Lower margin due to execution of a strategic project worth INR 180 Cr.

- The contract was taken at a competitive price considering long term opportunities.

- Ex of this contract, EBITDA margins were ~35-40%.

- Margins are expected to improve in H2 due to more balanced product mix.

- Order book INR 1300 Cr (includes orders negotiated pending receipt).

- Fresh order inflow of INR 351 Cr during H1.

- Confident of crossing INR 1500 Cr OB for FY26.

- Orders received from Brahmos and ECIL.

- Expecting high value orders in coming quarters.

- Export order book at INR 80 Cr.

- 31% of the order book relates to AMC (Annual maintenance contracts) for BrahMos ground systems.

- TPAR (Transportable Precision Approach Radar) exported to a European customer completed client acceptance. Expect positive traction from international markets.

- INR 122 Cr utilized from QIP funds for product development.

- Transitioning from a subsystem supplier to a full systems integrator, designing complete radar and EW systems in-house.

- Working capital is well controlled at 343 days (Will maintain at similar level for full year).

- Will collect most of the current receivables in H2.

- Still remain a debt free company as for most of the contracts there is advance given by the customer.

- New contracts should have even more advances and that will improve the cash conversion cycle.

- Expects WC to improve from 343 to 270 days gradually as they move from long gestation development contracts to production orders.

- Developing complete EW suite for the Super Sukhoi (4.5 gen fighter jet)

- Developed Jammer pods which are currently in testing.

- Developing BrahMos Seeker. Waiting for a contract.

- Focusing on the export market going forward. Management believes they build complex systems for which there’s not much competition worldwide.

- Developing products in radar, EW, avionics, ESM, electronic intelligence, drone detection and jamming, next gen seekers.

- TAM INR 15,000 - 20,000 Cr.

- AMCA (Advanced Medium Combat Aircraft) Consortium with BEML and Bharat Forge.

- Data patterns bring state of the art avionics (cockpit solutions, radars, EW).

- Currently at the RFI stage (Request for information), RFP (Request for proposal) has not been published yet.

- Expecting contracts in the next 6 months.

Disclaimer: Invested & Biased.

4 Likes

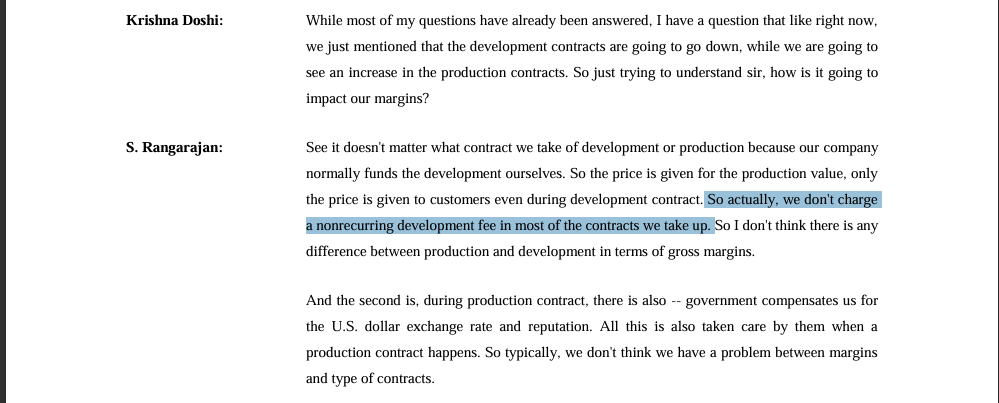

There is no development fee because it is a buyer’s market. It must be the same with others as well, not just Data Patterns.

1 Like

If I am not wrong, then in the development orders the MoD or DRDO asks the companies to build a prototype which is able to perform certain specific function, shouldnt the company be paid for this? Or is it something like if development order is approved production order is guaranteed?

1 Like

They are paid, it’s not free. That’s why he says gross margins are the same for development & production contracts. But the big money will made if & when you get production contract. Because production will have volumes and EBIDTA margins will be much higher.

7 Likes

For some reason this thread is quite for a while. I found some interesting info on Hawk-I-2700 radar related.

- Hawk-I-2700 is definetly a technological superior to DRDO Virupaksha radar.

- IAF is planning for a super sukhoi upgrade for about 200 active aircrafts with a budget of INR 63,000 crore. Out of total aircraft cost,>10% would be the radar cost. This means oppurtunity size if 6,000 Crore INR.

- The only challenge here is getting a share from govt. owned entity DRDO (Virupaksha radar is already under trials with HAL).

- Export market need validation (similar to Akash, Brahmos success during Op Sindoor), then many countries those operating Sukhoi’s would be supper happy to upgrade their fighters to Super Sukoi’s.

- The best part is the ~40% EBITDA margins.

Let’s see how things will playout on this.

Disclosure: Invested

1 Like