I was surprised to find there was no thread on Daikaffil Chemicals or on Open Offer Investing, so I thought I just make one myself. This presents details on Open Offer Investing as well as my thesis on Daikaffil Chemicals with the anti-thesis and risk factors.

Open Offer Investing

One of the interesting methods of investing which I’ve learnt off late is open offer investing. This term refers to a regulation which requires any company that has acquired more than 25% equity in a business to necessarily launch an open offer for 26% of the equity. This regulation is meant to protect small shareholders and ensure they get a fair deal if a takeover takes place.

I learnt about open offers from @Tar in his Wrap subscription and also he was the first person to cover this idea.

Open offers are inherently slightly messy, so you have to leave behind he traditional ways of thinking about and valuing businesses and focus more on three objective factors:

1. Who is acquiring the business: What is their net worth and related businesses

2. What do they intend to do with this business and why are they acquiring it: What are the future plans and how will that lead to alpha creation

3. How long will this transformation really take

I’ve participated in 5 open offers, and I’ve only been successful with at least three of them: the open offers of Windsor Machines, Popees Cares(Archana Software) and Daikkafil. Other open offers have generated returns, but they have not been as sustainable. Here’s a list:

- Sir Shadi Lal Enterprises

- Windsor Machines

- Popees Cares

- Daikaffil Chemicals

- Zodiac JRD MKJ

Daikaffil is a stock which has already doubled from my first buying price and on my average buying is up by 50%. However in this correction, I am aiming to add more to the stock and just wanted to lead VP through my thesis on it once.

TLDR: I also made a video on Daikaffil which you can watch on 1.5X to just get through this quicker. It is linked here: https://www.youtube.com/watch?v=eBXpmxS3Q7g&t=561s

So lets just dive into this thesis:

1. Background on the Open Offer

2. Triggers and Potential Thesis

3. Upside Assessment

4. Risk and Antithesis

Background on the Open Offer

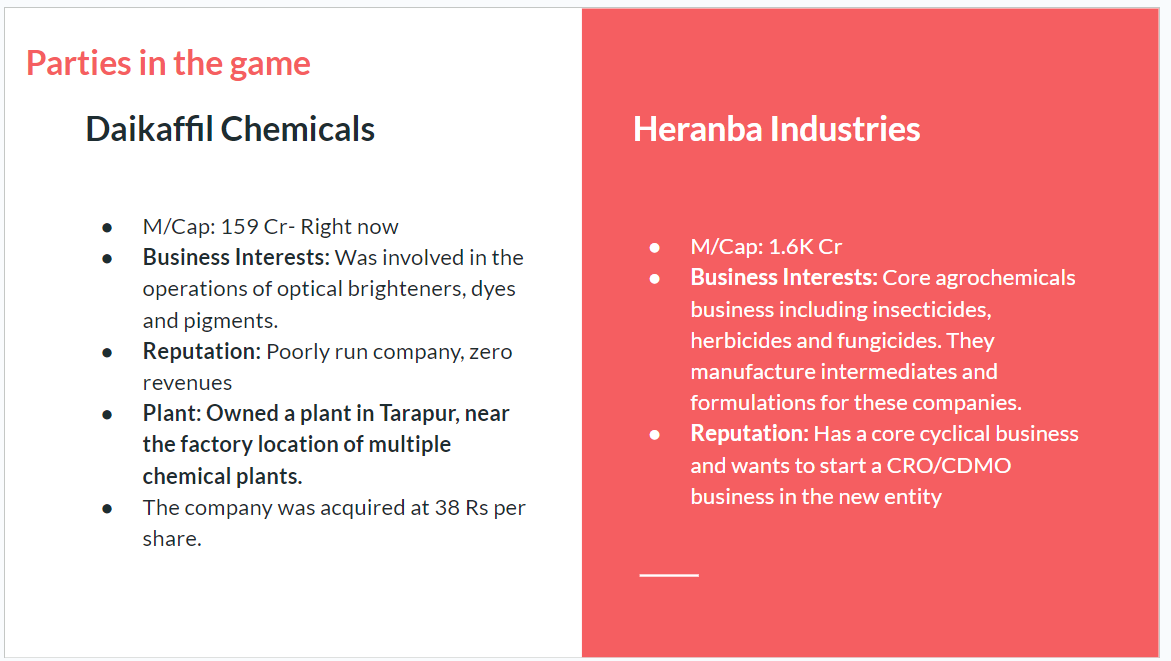

Background of Players: There are two major players in this open offer and their background is summarised below:

Essentially Heranba Industries which is a Agro chemical player engaged in manufacturing intermediates and formulations has acquired Daikaffil Chemicals at a price of 38.5 Rs.

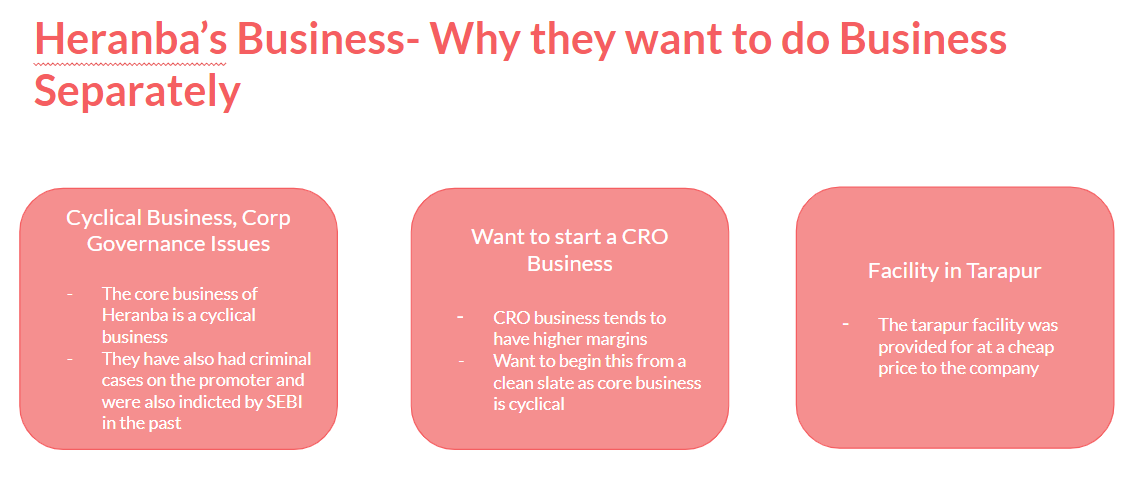

Heranba’s core business is pretty cyclical and it has been their aspiration to start a CRO/CDMO business which is more structural as revenue.

Apart from core cyclicality, Heranba has also had several corporate governance issues in the past which have meant that it has always traded at a poor multiple as compared to other agrochemical companies. The details of this are highlighted in the VP thread of Heranba here:

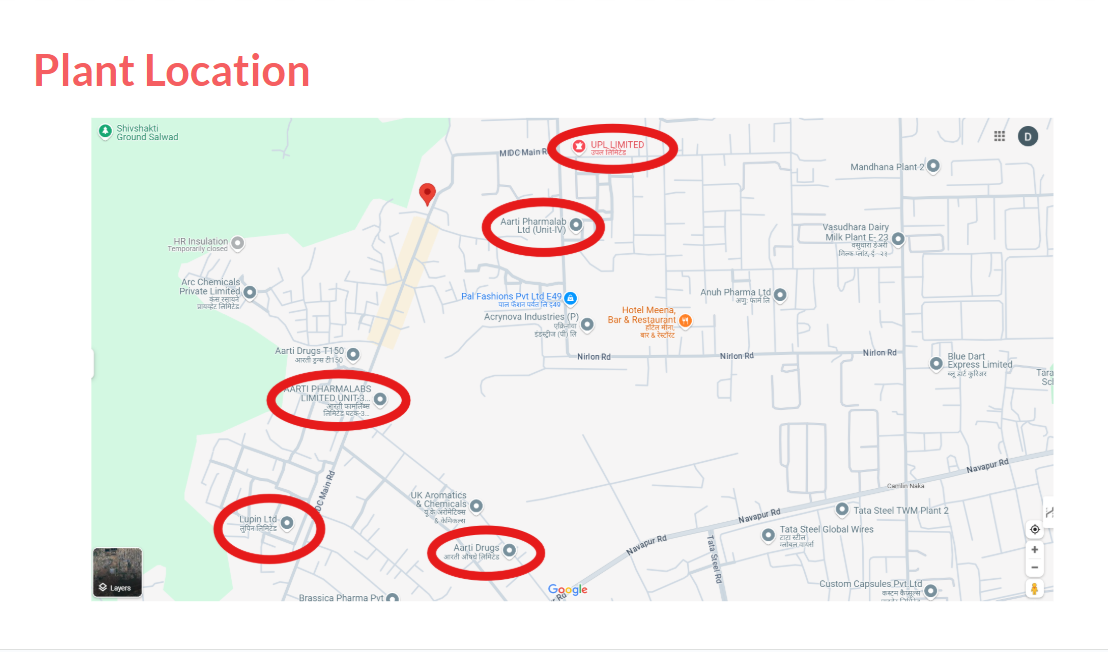

Daikaffil was a shell company listed on the exchanges that owned a strategic plant in MIDC Tarapur, near Palghar.

Further their plant is extremely close to manufacturing locations of UPL, Aarti Pharmalab etc

Heranba sought to acquire this company to get access to the plant at a much cheaper price by buying the promoter stake in the company.

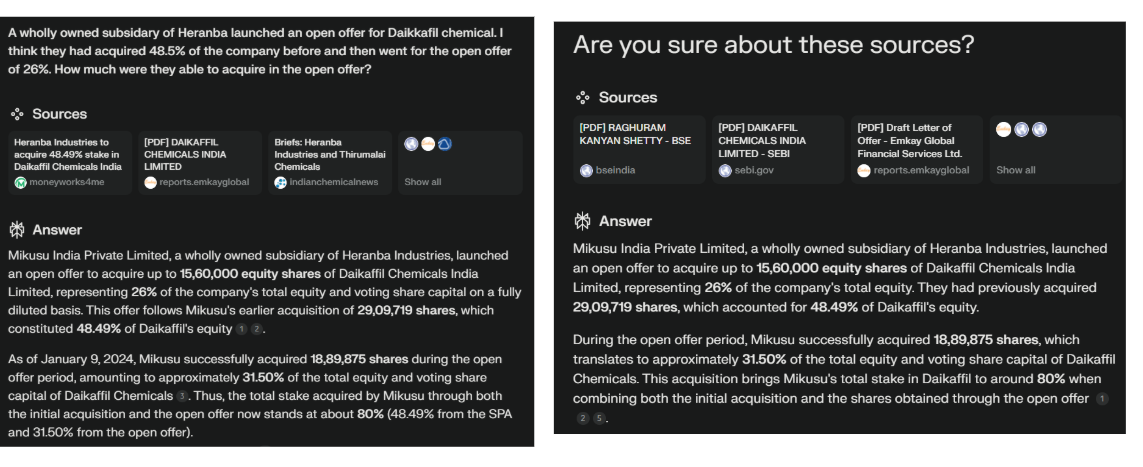

Timeline of Open Offer

This sheet shows the timeline of the open offer, Heranba’s Wholly Owned Subsidiary, Mikusu acquired 48.5% of the stake of Daikkafil off the market for 7 Cr and post this, they gave an offer for other equity.

In Novemeber, they shared a plan divided into two phases on what they want to do with the business. Since Sep 24, the promoter has continuously been buying shares in the company and they have acquired 2% of the company.

Objective of Open Offer:

The open offer is being done as discussed above to start a new CRO kind of business for the purpose of which the company has sanctioned 50 Cr for repairs of the plant and has stationed 30 scientists in the new entity.

Triggers:

There are three major triggers in the business:

*** The phase wise plan that has been shared**

*** Continuous promoter buying**

*** Entry of major shareholders**

Let’s dive into them one by one

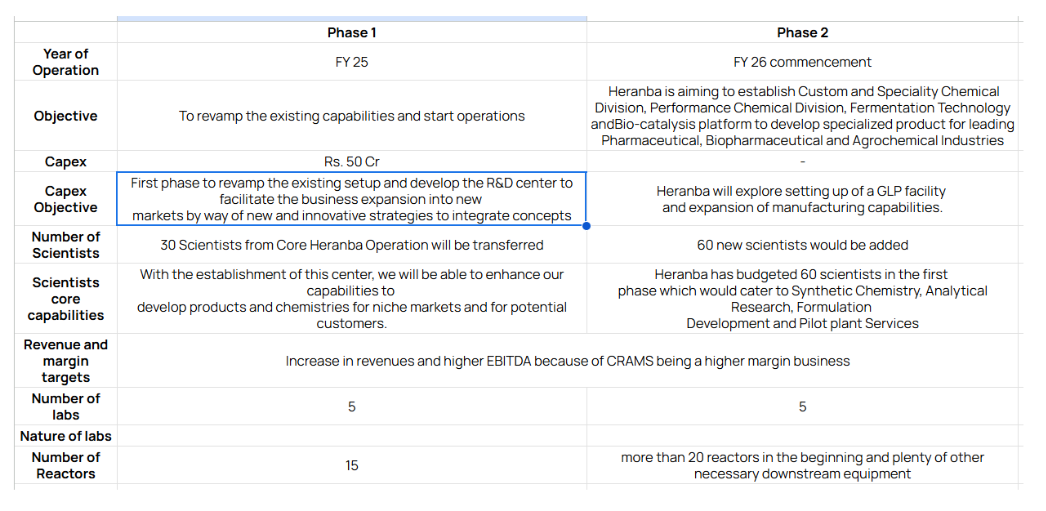

Phase wise plan

The company shared a two phase plan on how they will develop the plant for Daikkafil. While the first phase will all be about setting up the place for production, the second phase is set to expand the capabilities.

I’ve summarised the plan in a tabular format below:

Further, my sense is that once the basic lab and its amenities are in place, Heranba will then look to get more funding for this business and grow it more rapidly in the coming few years.

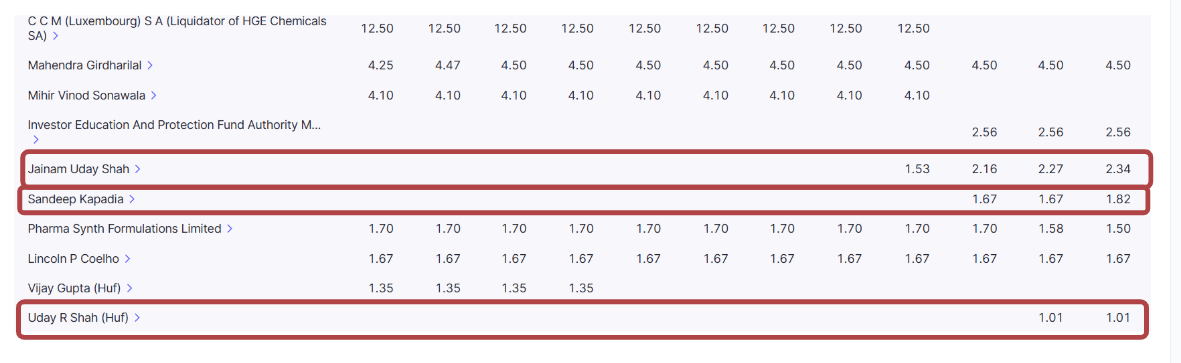

Continuous promoter buying

The promoter has bought equity worth 2.91 Cr in the business which is about 1.82% of the company, starting from September 24 till December 24.

I am also attaching a table summarising the buying below:

Sourced from The Wrap tools by @itstarH

Entry of shareholders

Several good investors, like Sandeep Kapadia have entered into the business and have bought stakes in the business. Uday R Shah is another prolific investor who has bought in his own account as well as for his son

Sourced from Screener

These three make me feel that there is a disproportionate upside possibly in this business which can be utilised. This is extremely risky, but I suppose I really want to take the risk here.

Upside Assessment

To assess the upside, if you look at any CDMO, CRAMS company, you’ll see that they trade multiple times of their netblock.

Syngene for example trades at 20X their netblock. Syngene is the best CRO business in India, so we can assume a 2X-5X netblock kind of multiple, reasonably.

Till now, Daikkafil has put in a netblock of about 50 Cr in the business, if this is accelerated, and the company puts in more than this money which they would, considering the next phase is now lined up, the valuations and the company can move into a completely different orbit.

However, even with the current 50Cr net block, the company is valued justly at 150 Cr right now.

If this goes anywhere, literally the sky is the limit. However it might take an entire cycle of 3-4 years for this to actually fructify.

So I am willing to be patient here.

Risks and Anti Thesis

There are four major risks in the business:

- A possible delisting

- A possible merger

- Change or delay in plans

- No revenues in the company yet

A possible delisting:

According to Perplexity, even before the promoter buying in Septermber-December 2024, the promoter owned more than 80% of the business

Screener reflects otherwise, it says that the current stake is only 49%

If the perplexity bit is correct, the company may well be on its path to delisting.

A possible merger:

Since this is a much higher quality business than the one being run by Heranba, I’m not sure how well the investors in Heranba would take it that Daikaffil will now have all their scientists, they might push for some kind of amalgamation which will disrupt the thesis again.

Change/Delay in Plans and No Revenues:

Till now, this seems like a completely hope driven story. And I understand the pitfalls of falling into the trap of something like this, but I want to practice a kind of investing where Heads I win big and Tails and I don’t lose much and this company fits into that model. However for a conservative investor, this doesn’t make as much sense.

I would really like it if more senior members can comment on this or if other contributors add more to/critique the story.

If you want to learn more about open offer investing, I’m also linking my X posts on the Open Offer of Sir Shadi Lal here: https://x.com/search?q=from%3A13gaurdevesh%20%23SSLEL&src=typed_query