Background:

Dabur (derived from “Da”ktar “Bur”man) is an Indian consumer goods company founded in 1884 by S. K. Burman. In 1936, Dabur business got formalised in corporate structure with Dabur India Private Limited which was converted into a public limited company in 1986. The company came out of with IPO in 1994. It manufactures Ayurvedic medicine and natural consumer products. It is one of the largest fast-moving consumer goods companies in India.

Despite promoted and controlled by family, the company has successfully handed over management of business to professionals in 1998 with family members limited there role to non-executive directors. The company has successfully blended organic brands (classic brands like Hajmola, Lal Dantmanjan. Pudin Hara, Chawyanprash, Real Juice, Vatika) as well as inorganic growth strategy (acquisition of Odomoss, Promise, Fem etc).

Past performance

Since listing in 1994, Dabur has performed reasonably for it’s investor provided XIRR of 26.1% (including dividend reinvestment) over a period of 26 years. The value of Rs 9500 invested for 100 share in IPO in 1994, would be valued at Rs 27 Lakh as on March 2020 + Dividend assumed to be reinvested. My calculation of return as well as other financial highlight of the company is enclosed in excel sheet. Key table is as under:

Over last 25 years, the company sales and net profit grew at CAGR of 12% p.a. and 17% p.a. respectively. This has been done reasonably well ROE of 32% over period and healthy dividend payout for shareholder of 38% (average dividend payout). In 1999, when professionals were given operational control, the company was trading at around 65 times PE ratio. If an investor has entered at such high valuation, still one would have generated 17.5% XIRR over period of 21 years. This would be quite commendable performance of the company over any parameters in opinion.

Positives

130+ year business showing 30+ business attitude

Ayurveda and Herbal can be defined as Core to Dabur business. The company attempt to use century old tradition of Ayurveda and applied successfully to modern science test. The company has filed 43 patent till March 2020 (of which 1 Patent application filed in FY20) and have 8 patent granted till March 2020. The company has 98 employees in Research and Development.

Since many of the products of the company are coming from Ayurveda, with age, brand develop more and more strength as against recent research brands. Chywanprash, Hajmola and Pudinhara can continue to grow and strengthen their brand equity with ages. This I consider unique advantage of company. Dabur is the world’s largest Ayurvedic and Natural Health Care Company with a portfolio of over 250 Herbal/Ayurvedic products.

In order to get authentic ingredients and herbs, the company has engage with farmer to grow rare medicinal herbs in over 4,800 acres of land spread across the country with over 6,900 farmers benefiting from the exercise. Similarly, it has been using Nepal and Indian farmers support to source authentic Honey supply which provide unique sustainable supply of Honey to the company.

The company see Ayurveda as a core of business. This has assisted company not only in Indian market but also expand its global footprint. Ayurveda/ (Natural) products are getting increasing acceptance among customers. Dabur mission statement articulate this ethos very well ” Contemporise Ayurveda and make it relevant for the new generation”

The company annual report in 2018 highlight finding from a survey carried out by Euromonitor International reveals that over half of Indian consumers reported that ‘natural or organic’ features are known to influence their hair and skin care purchase decisions. About 71% of consumers surveyed said that they would pick up a face cream or lotion provided it claimed to be ‘natural’, while 38% said they would buy a shampoo or hair oil, if it was made with ‘botanical’ ingredients.

In my opinion, this trend to Ayurveda/Natural products would increasingly find acceptance of customer. This is also illustrated when Colgate launched Vedika toothpaste and Hindustan Unilever launched “Ayush” range of products. The 130 years of goodwill of Dabur would provide definitely key advantage to the company. The company is also using various studies conducted by its research team in marketing its products. For instance, Dabur Chyawanprash , which was otherwise, seasonal product with higher demand in winter is now launched with chocolate flavor for kid and now positioned as immunity booster. Similarly, Dabur honey is now market as product which can assist consumer in controlling its weight.

During 2015-16 Dabur entered into a license agreement with the Government of India to commercially produce two new Ayurvedic drugs – Ayush-64 for treatment of Malaria and Ayush-82 for management of Diabetes. A clinical study conducted with Madhumeha (Non-Insulin Dependent Diabetes Mellitus, NIDDM), demonstrated that Dabur Madhurakshak Activ (AYUSH 82 powder) reduced fasting and postprandial blood sugar levels, along with clinical improvement in diabetic subjects after 24 weeks of treatment.

This blending scientific attitude to Ayurveda can augur well for future growth of Dabur India.

“Indian” King of distribution

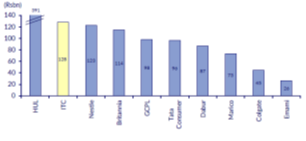

While I have been holding small tracking position in Dabur for 5 years, my interest in the company developed after I came across CLSA note on ITC which provided some key input about distribution strength of FMCG companies in India. Since ITC was my top holding, I carefully read the report and observed an unique chart which attracted me to write this post.

While the company is 7th largest listed company by revenue from FMCG products, it is second still largest in distribution reach in India among listed players and largest in Indian Owned enterprise.

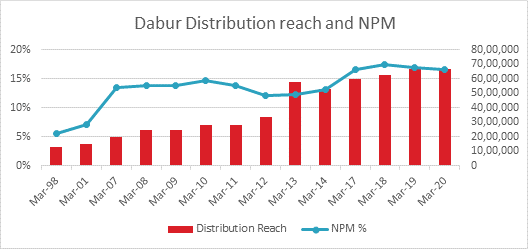

In order to get more understanding, I tried understand how company has scaled up its distribution over period and what has been impact on net profit margin? Find enclosed my compilation from various annual reports of the company:

This was my effort to understand how increased distribution along with proper blend of old and new brands can do wonders to profitability of company (driven by operating leverage).

High penetration in Rural India

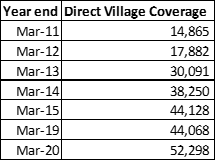

The company has pushed special efforts to increase its reach in rural area. As per internal study, nearly 10% incremental sales in the key brands was driven by high penetration in rural market. Find enclosed map providing special efforts to cater to “Rural India” directly. As against total village of 650,000 in India, Dabur has direct reach 52,298 villages as on March 31 2020. This has been achieved special emphasis and hard word of the company over the years.

Power Brands Focus

With just 3 brands over sales of Rs 100 Cr in FY1998, the company has now increased to 18 brands with sales over Rs 100 Cr in FY2020 (significant impact is also due to inflation over period). The company now intend to focus on key brands, which is call “Power Brands” and plan to increase marketing spending on such brands. Dabur has identified 9 Power Brands – Dabur Chyawanprash, Dabur Honey, Dabur Lal Tail, Dabur Honitus, Dabur Pudin Hara, Dabur Red Paste, Dabur Amla Hair Oil, Vatika and Réal fruit juice – that account for more than 70% of its total Sales. It is important to note that all power brands are developed by Dabur management in-house and are related to Ayurveda/Natural products, which has been core to Dabur business proposition.

Good capital allocation: Using Capital to acquisition of brands

The company in past has worked on inorganic route to pursue extra growth. Most of the times, the company management ensured that acquisition is at reasonable terms and company post acquisition have managed to turn around well. For instance, the company acquired Balasara group of companies along with brands Odonil, Odomos and Promise and manufacturing facilities in FY2005. Dabur bought the entire promoters’ stake of three Balsara companies through an all-cash deal of Rs.140 crore. This acquisition is expected to add approximately Rs.200 crore to Dabur’s revenues. However, the brands were not making major profit at the time of acquisition.

In FY2006, total operational and business integration of the two companies was achieved; and on the financial front, the erstwhile loss-making Balsara entity has generated profits of Rs 14.9 crore.

This was followed with successful acquisition of Fem Care Pharma Limited, a leading woman skin care products company which was acquired for total cash consideration of Rs 203.7 Crore.

Similarly, in international market, in FY2011, Dabur completed two overseas acquisitions within a span of just four months. In October 2010, Dabur completed the acquisition of Turkey-based Hobi Group (Revenue US$ 30 million and consideration US$ 69 million), This was followed in quick succession by the acquisition of Namasté Laboratories LLC (Revenue US$ 94.7 million and acquisition cost US$ 100 million), giving Dabur an entry into global African hair care market. These acquisition has assisted company to increase its footprint in global market. In FY2020, International business contributes 28% of consolidated sales as against 17.6% FY2010.

The company has also divested from capital requiring business, Dabur Pharma in FY2003. The shareholder of Dabur India was given 1 share of Dabur Pharma for each 2 shares held in Dabur India. Dabur pharma was leading oncology players. However, demerger of pharmaceutical businesses, assisted management to focus on core FMCG business and grow over time.

Negative

Threat from Competition:

While the company is largest and among oldest player in Industry, recent competition from new players (Patanjali) and increased focused of competitor (from Colgate to Hindustan unilever to Marico) to adjust to new market normal can adversely affect Dabur prospects.

Patanjali entry in Indian market has shown true potential for Ayurved products in India. While I cou;ld not get details about Ayurved based product sales, enclosed link provide good insight about market size and growth potential for relevant segment. As against Rs 6300 Cr consolidated domestic sales by Dabur over 130 years long joinery, Patanjali achieved total revenue of Rs 10,000 Cr in FY2017 only. Although due to logistic and lack of professional management, Patanjali has faced problems which adversely affected its performance, one must credit Patanjali Management to reach second largest FMCG company in India within a decade of its operation.

Baba Ramdev's Patanjali is in a free-fall & it can't be blamed on the slowdown alone

Top Credit Rating Agency, Credit Monitoring Services in India, Credit Quality Rating – Care Rating

Similarly, increasing competition intensity from other established players like Hindustan Lever, Wipro, Marico and Colgate may adversely affect performance of Dabur.

Managing supply of key ingredients

As already said, Ayurved products soul of Dabur business model as described by management, sourcing authentic products and herbs may pause major challenge to the company. FY2018 report provide more insight about company preparedness to address this risk. It state that the company use 249 medicinal and aromatic plants (MAPs) for its various Ayurvedic and natural preparations. Of these, Dabur has identified 100 MAPs as being critical to its operations in terms of their availability, value and volume. Through its biodiversity initiatives, Dabur has put in place direct interventions for either cultivating or sustainably collecting 58 of these 100 critical MAPs. In 17 species of MAPs, Dabur is 100% self-sufficient in a way that the entire requirement of these 17 herbs are managed through its biodiversity program and interventions.

While the company is addressing the issue of sustainable supply, getting sustainable supply of these ingredient appears to be key challenge in my opinion.

Valuation

At current valuation of Rs 500+, the stock is trading at 61 times PE ratio. This provide very limited margin of safety to investor in my opinion.

Disclosure: I have tracking position ( less than 0.1% of my equity portfolio) in the company since last 5 years. My view may be biased due to my holding. I am not SEBI Registered investment advisor. I am also not recommending any investment action in this company. The reader shall do his/her own due diligence before making any investment decision.

Dabur Past Return.xlsx (824.5 KB)

https://www.screener.in/company/DABUR/consolidated/

, the PE ratio shall revert to market PE ratio sooner as pathway is limited and growth would be broadly from premiumisation.

, the PE ratio shall revert to market PE ratio sooner as pathway is limited and growth would be broadly from premiumisation.