lets wait for the Q2 con call.

Coal India stock is continuously falling and seems to be a value trap due to uncertainty on following factors. Still looking at the stock very closely as its a monopoly and demand is unlikely to be an issue for next 10 years.

- Insufficient increase in production - higher allocation under FSA leaving less for higher margin coal auction

- Supply overhang - Govt continuously selling and FII wont buy much of dirty coal leaving more to FIs/ insurance companies who are already carrying large quantity at a loss

- heavy capex without much clear IRR requirement - mentioned in presentation that whole 600 MT coal evacuation costs Rs 3400 cr. while planned railway line development cost (excluding already executed capex) is ~Rs 20,000 which at 8% interest and 80:20 D:E leaves very limited RoE (Rs ~1300 cr int + Rs 1000 cr. principle repayment).

3 Likes

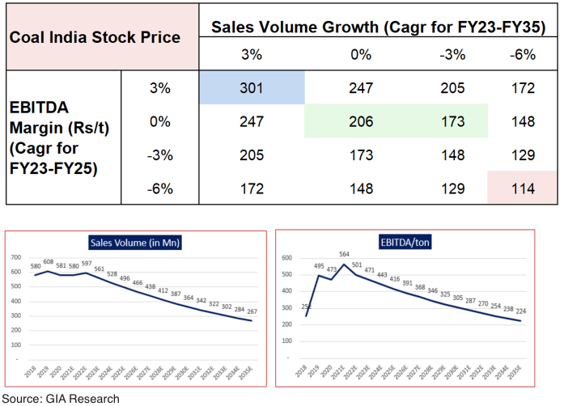

I tried to do NPV calculations for Coal India trying to figure out what is build in the stock price. The assumptions that one has to make to reach current market cap is absurdly pessimistic. I think fair value of Coal India is between Rs173-206. However you can make your own assumptions on volume growth and EBITDA/t trend to see what value you get.

Source: How cheap is cheap enough?

3 Likes

Absolutely true. How much value has been destroyed. However, now Coal India’s valuation is building in a scenario in which the business will close down in 12years. This is abject pessimism and hence the opportunity.

1 Like

Interesting, if market was to value any company in a manner that it’s business would close down in 12 years, it would be available at close to 0 market cap with only some punters trading in it.

Really? In that case who gets the free cash flows in next 12 years? If a business is to shutdown in a decade, it simply means that their terminal value should be equal to or at a discount to their stated book value (assuming that’s liquidatable). Market can assign any valuation to a company, however that valuation doesn’t drive the cash flows earned by that company in the future. The only place where reflexivity has a role to play is in lending companies which need to raise equity money to fund growth.

4 Likes

Harsh thanks for explaining it so well. The whole point of my exercise was to find what scenario of cashflows is build in current market cap, and what comes out is an unlikely pessimistic scenario. Coal India is a 100year old company and should easily last another 40-50years

2 Likes

Ans 1: If a company is likely to close down in 12 years, it would be available at close to 0 market cap

Ans 2: What about the free cash flows over the 12 years, and what about the liquidation value of assets at the end of 12 years?

Ans 3: The company may throw up a good amount of cash over the 12 years. But shareholders may never see much of that cash. Very few companies that are likely to shut down in 12 years have the wisdom to realize this, and can accept this outcome. Most are likely to plough back and use up a big chunk of the cash they generate in a bid to “improve efficiency” (which will not solve the core problem). Or to “get into the future” (just for saying - perhaps clean energy for Coal India) in which the company may not have any real experience or ability to compete. Hence, the market may discount the expected “free” cash flows far steeper than one might expect - because the expectation is that the shareholder will never see that cash. So you might actually end up closer to answer 1 than answer 2!

P.S: I don’t have a view on Coal India, and what discounting might be appropriate.

6 Likes

A rare interview from CMD Coal India which gives good amount of insights into thougth process within the company.

Disc : No position.

1 Like

With stock valuations so cheap and infrastructure investments in the latest budget. I think overall coal to power ratio will improve and given the growth rate of tier 2 cities and energy consumption is going to increase. Please check out the below link

Disc: no position

There had been changes in key managerial personnel last year.

- Chairman cum MD: Mr. Pramod Agrawal (since 01.02.2020), Mr. A. K. Jha (18.05.2018 to 31.01.2020)

- CFO / Director (Finance): Mr. Sanjiv Soni (since 10.07.2019), Mr. S Sarkar (01.10.2018 to 09.07.2019)

Are these usual in PSUs? Timelines of these changes and major fall in stock prices seem to coincide (I may be too paranoid).

Disclosure: Not Invested

This is from September 2020. Looks like 14% of the toilets constructed by Coal India (of the ones checked by CAG) don’t exist or not fully constructed. There are issues with the some of the remaining ones: 72% toilets lacked water supply, etc.

Disclosure: Not Invested

1 Like

Hi everyone.

Would very much appreciate if anyone can explain the “Stripping Activity Adjustment” in their accounting - why is 60,000 Crores lying on their Long Term Provisions against this charge!!!

It is a non-cash charge, I understand that - about 5,000 Crores is added back on their Operating Cash Flows every year.

Look forward from someone in the Community helping me wrap my head around this.

Key takeaways from the management interaction

-

The management said it may need to revise its earlier dispatch/production targets of 740mt/670mt for FY22. Of this, 130-140mt was set for e-auction. As per the company, dispatches would depend on how Power demand and a likely third COVID wave pans out. On a normalized level, COAL expects its dispatches to increase by 40-50mt annually.

-

COAL expects capex to be at INR170b for the next couple of years. This comes on the back of replacement of machinery. Works for R&R, first-mile connectivity, evacuation, and land acquisition would contribute to capex. As per the company, this run-rate should not sustain post FY23 and may even be lower, although much depends on overall demand

1 Like

This is one of those stocks, where it seems one needs to go by the adage “I’m happy to own this even if the market closes down tomorrow”. One needs to be mentally prepared that this stock will always have a supply-demand imbalance. Buyers are likely to be an increasingly rare species, due to ESG and a “sunset industry” tag. Of course, it might all play out differently, with the company posting great results due to favourable coal prices, and many buyers emerging simply to chase performance, ignoring perception issues.

But it will be better if one is considering buying today that she be okay with a scenario where the stock price keeps falling as buyers dwindle over time, and returns are made in the form of dividends/buybacks/routes other than capital appreciation. At around 11% dividend yield, this could still fit the requirements of some investors. But they must be mentally prepared to see the stock price continue to languish, or even fall consistently. Just keep pocketing the fat dividend, laugh at Mr. Market and his idiosyncrasies, and be comfortable with your choice.

Discl: Not invested

4 Likes

Stripping activity adjustment-In case of opencast mining, the mine waste materials (“overburden”) which consists of soil and rock on the top of coal seam is required to be removed to get access to the coal and its extraction. This waste removal activity is known as ‘Stripping’.

In opencast mines, the group has to incur such expenses over the life of the mine (as technically estimated).

Therefore, as a policy, in the mines with rated capacity of one million tons per annum and above, cost of Stripping is charged on technically evaluated average stripping ratio (OB: COAL) at each mine with due adjustment for stripping activity asset and ratio-variance account after the mines are brought to revenue. Net of balances of stripping activity asset and ratio variance at the Balance Sheet date is shown as Stripping Activity Adjustment under the head Non-Current Provisions / Other Non-Current Assets as the case may be.

(Source-Company annual report)

7 Likes

No post here in a year, stock has given good return during this time.

4 Likes

When the emerging trend is Renewables, Green Hydrogen & EV, Coal India is something which most people would ignore.

Now by hindsight due to global energy crisis (created due to Russia-Ukraine war) most analysts are giving a buy call to Coal India.

Well, I have a Basket of PSU stocks with high Dividend yield 6 -12 % which includes Coal India among other high Div yield PSU stocks such as REC, Power Grid , IOC, BPCL, SJVN, NHPC, NTPC, NALCO and some defence stocks such as BEL, HAL, Mazgaon Dock.

While I don’t look at day to day price movements of these stocks as I dont intend to make a trade-my basic objective being to earn some fixed returns by way of frequent dividends awarded by these companies, I find of late there has been 15-20% capital appreciation on the PSU basket which constitutes 15% of my overall portfolio.

Discl: It is not an investment advice. Please do your own assessment before you invest.

3 Likes

Time we updated the views on Coal India? I have invested a small amount in Coal. How many companies have a PE of 5.44, and ROE 43.6%, and ROCE even better at 54.3%?

Of course, I am also concerned that coal is destructive of environment, so alternatives have to be found. However, total elimination of coal seems to be far away. In fact, I was shocked that at Buxar, in Bihar, a thermal plant for SJVN, a PSU is under construction.

1 Like