I am writing this post to evaluate my own understanding of valuation and future earnings prediction. I would like the fellow members to share their views on this post.

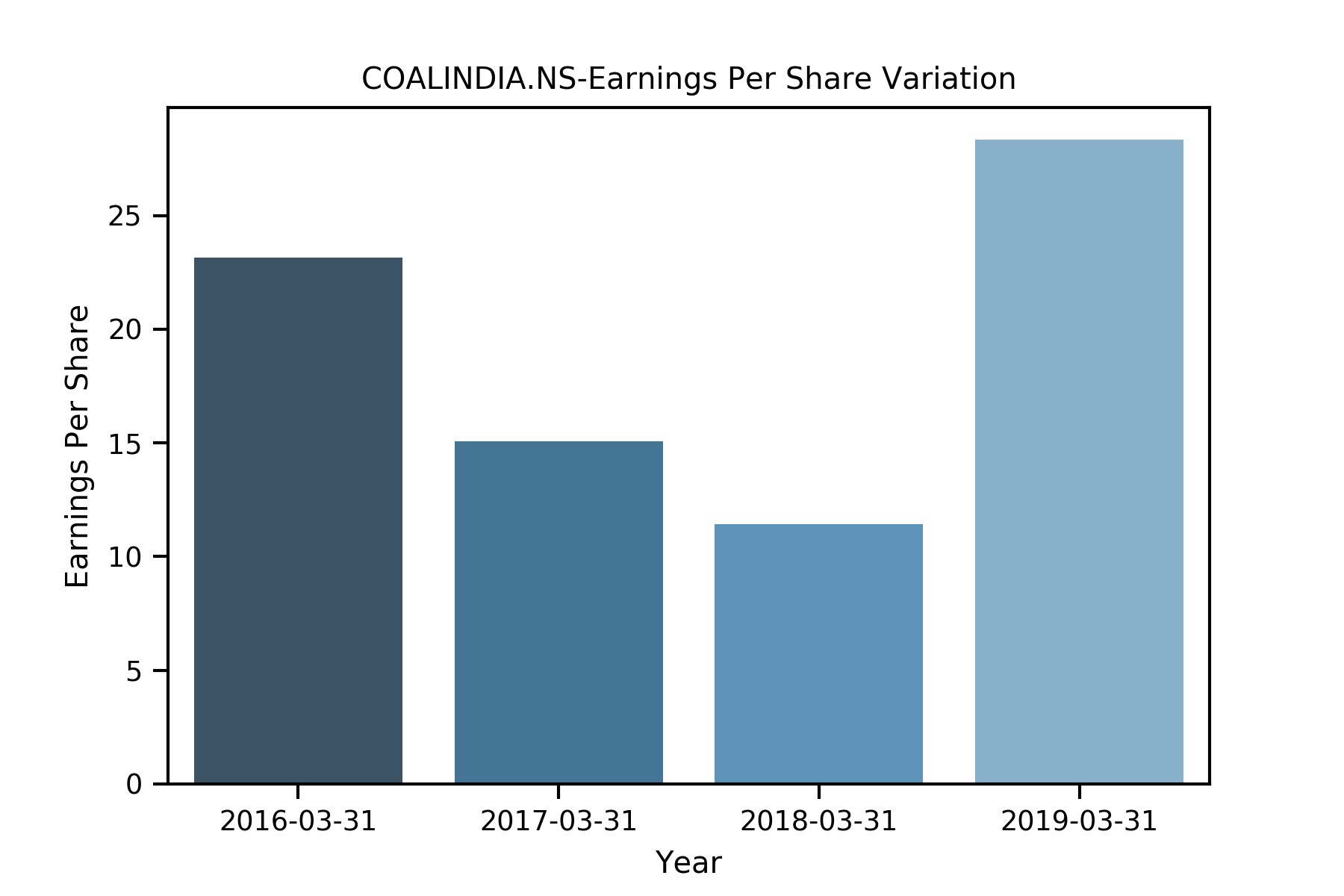

So given the NPM at 26 for Q4. and we also have the total offtake for Q1 (153.43 MT) and with realization to be greater than 157 (e-auctions have been higher this qtr), we can arrive at sales of 24089 cr. Using the NPM of 26% we can arrive at a profit of cr 6263. against FY18 annual profit of just 9266!!

Positive Triggers:

Govt is keen to cut down coal imports to save forex. current coal imports stand at ~150MT FY19.

Economic growth in-turn increases Power consumption which catapults Coal production. we may reach 1billion tons of coal by 2022.

Current logistic concerns will be eased out with Dedicated Freight corrider, Sagarmala projects and own CIL initiated rail projects.

Govts will use coal for foreseeable future due to employment it generates in rural areas.

AK Jha MD of CIL is a dynamic leader coming from Mahanadi Coalfields and has a credible record of making MCL a stellar subsidiary of CIL.

~20% of additional thermal capacity is coming up in various states of the country. No matter how much solar power is generated, the Coal mix will stay atleast for the next decade.

Its like owning a proxy for Power companies in India which has a clear monopoly.

Coal-bed methane could be another revenue in future.

Current Negatives

Logistics

Labor issues / Wage hikes (but looking at their cash flows and future needs, this could be minor)

Disclaimer: Heavily invested in CIL from Rs. 250; Views may be biased.

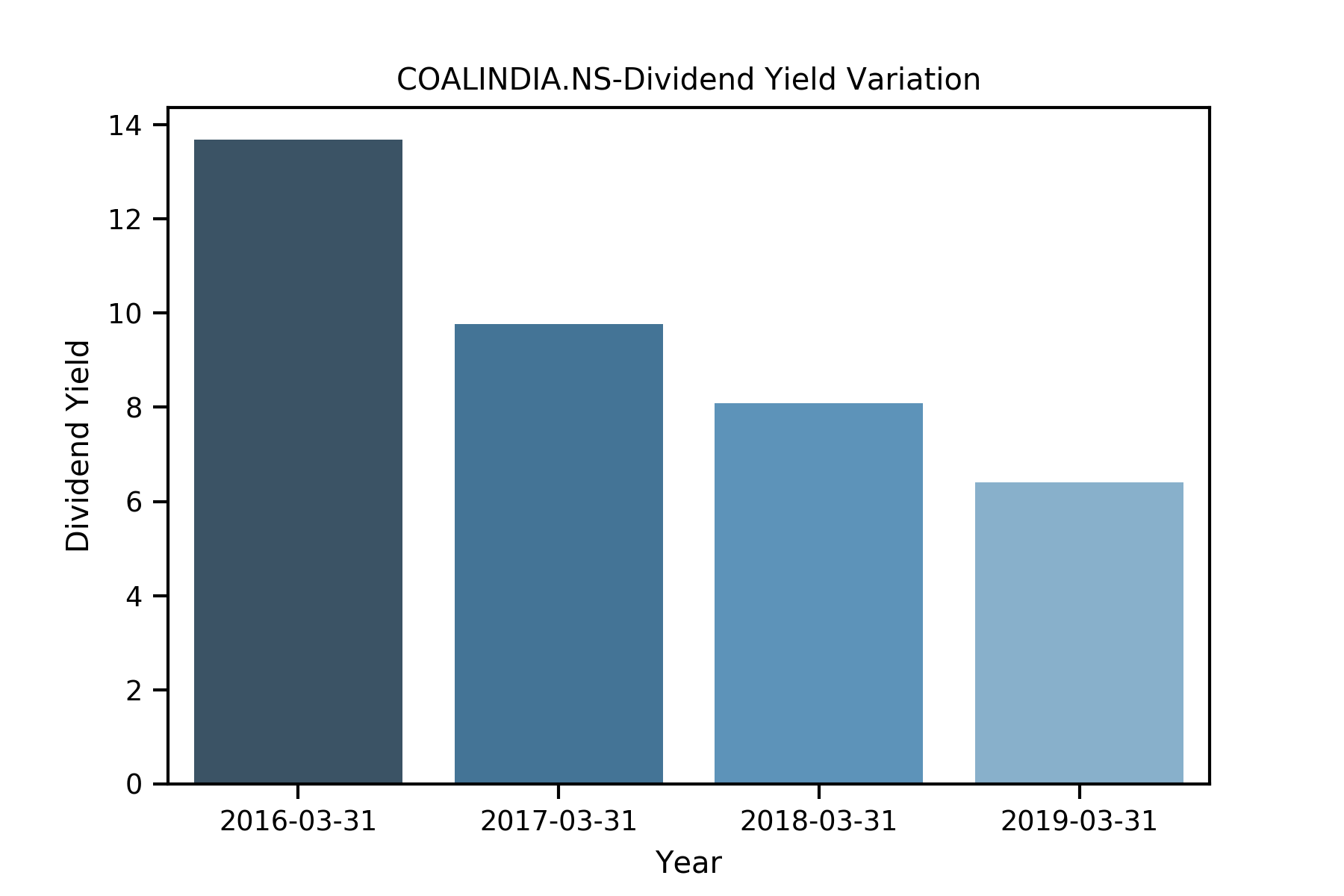

Coal india with a div yld of 9% at cmp single digit PE has been hammered mostly by arbitragers of Cpse etf which gave 4.5% discount n closed today. So its quite attractively priced imho at cmp of 240 odd. Tailwinds also there in form.of severe coal shortage in india n 80% of coal oputput is already contracted at a fixed price with customers. Remaining can go thru e auction at lucrative rate.

I am treating as a tax free FD at 9% of which a major chunk one will get by March 19. Downside seems v limited . Hydro renewables are lagging behind n Demand in India of power is galloping .

Concerns remain a commodity play with intl prices correcting n PSU work culture . But more mines n rail tracks coming in n growth seems to be there in last qtrs.

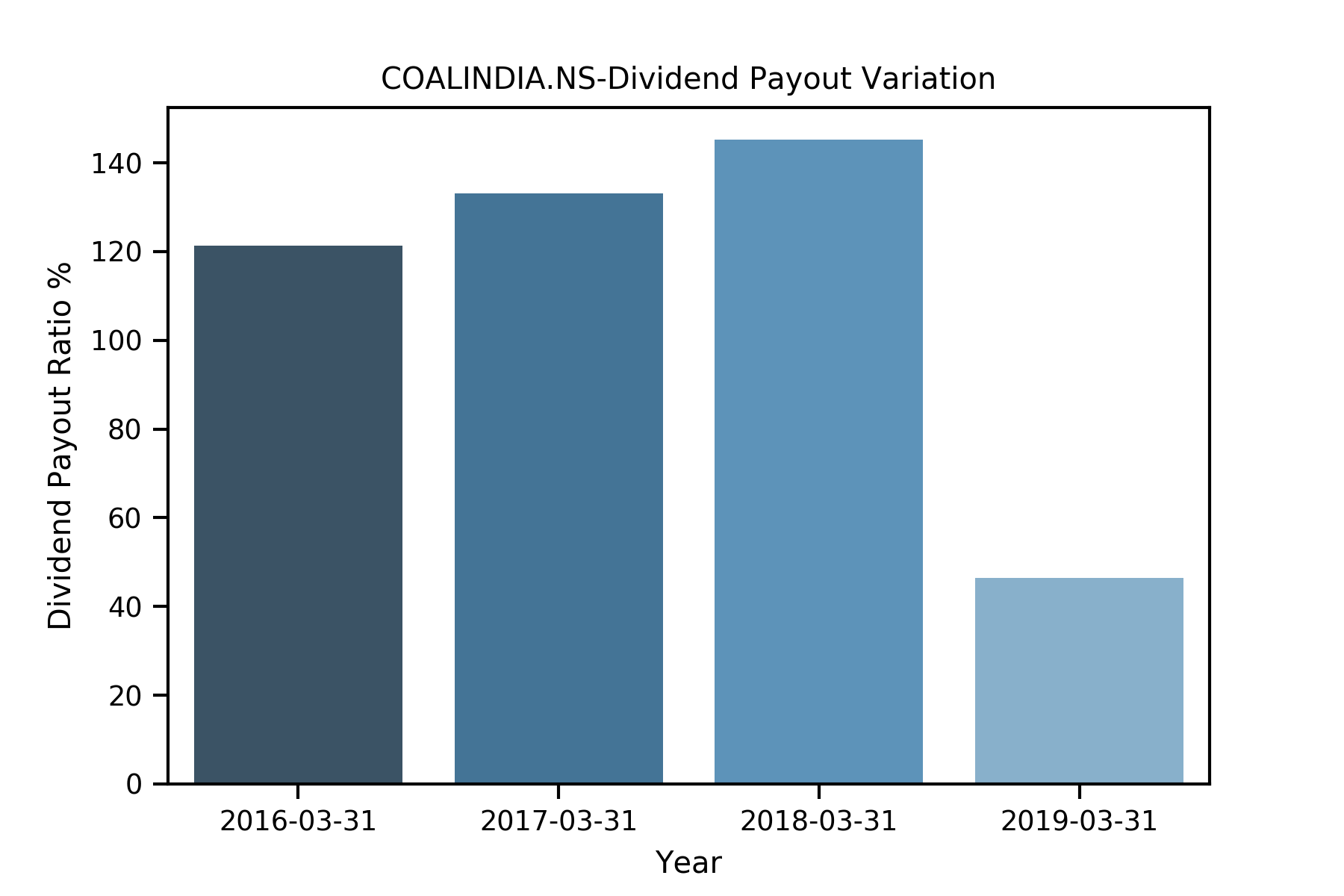

Their dividend payout has vaired between 33 and 51% during 2008-2013 and 121 to 133% during 2014-2018. If one goes by the argument that the present govt is using Coal India as a cash cow, what are the chances that such high dividend payout ratio will continue if the govt changes?

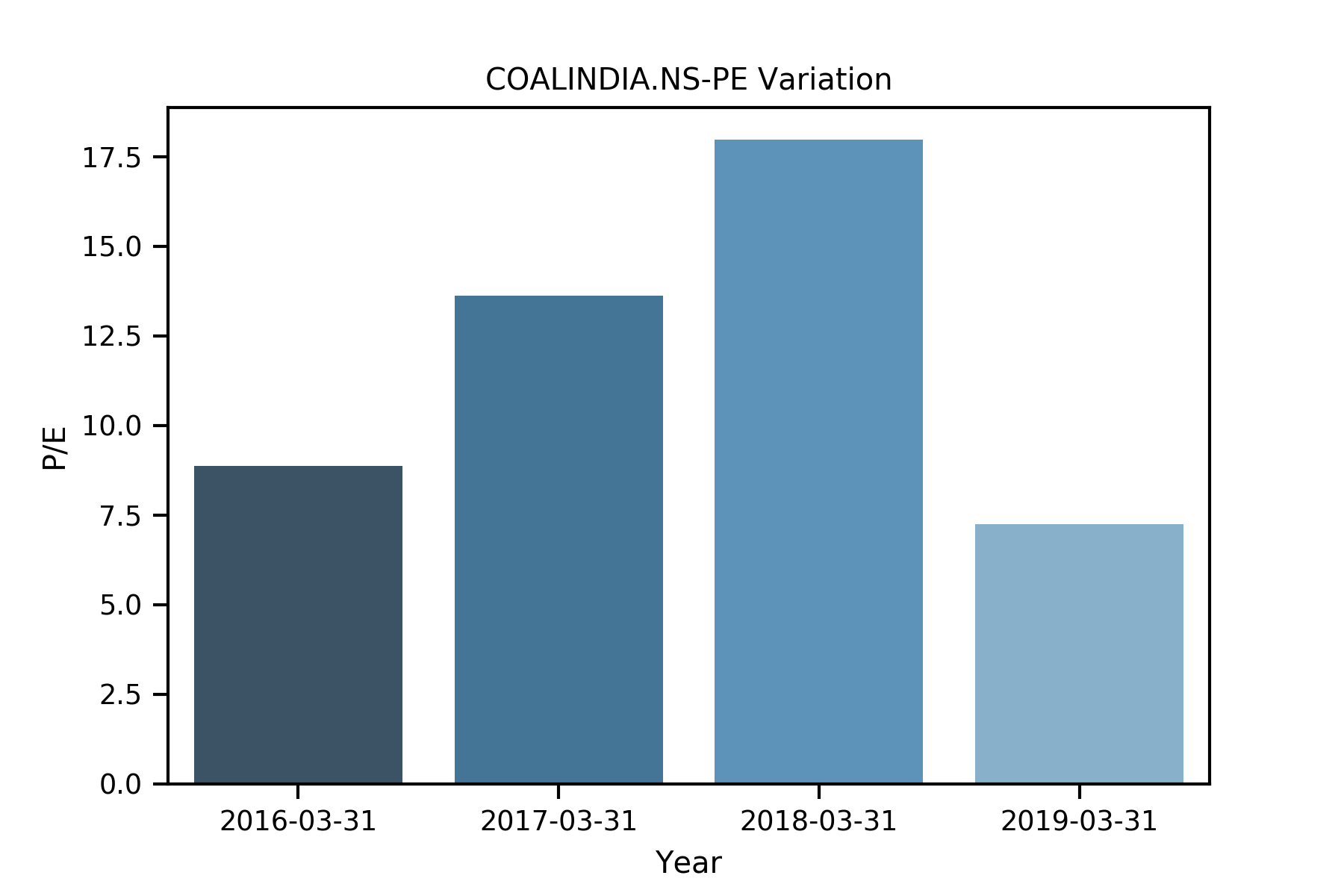

Btw, according to screener, Coal India has a dividend yield of 6.7 and PE of 13.x.

I think GOI has no option but to control fiscal deficit from.all routes of Buyback OFS Cpse etf n high dividend.

Hopefuly Modi if he comes back wud be more pro reform as per RJ n also he will now be having majority in Rajysabha with allies and key decision makers from.Bjp .

I think Nda will hv no.option but to privatize more PSUs. Lets hope for the best as then these langushing PSUs will multiply . But thats a big IF

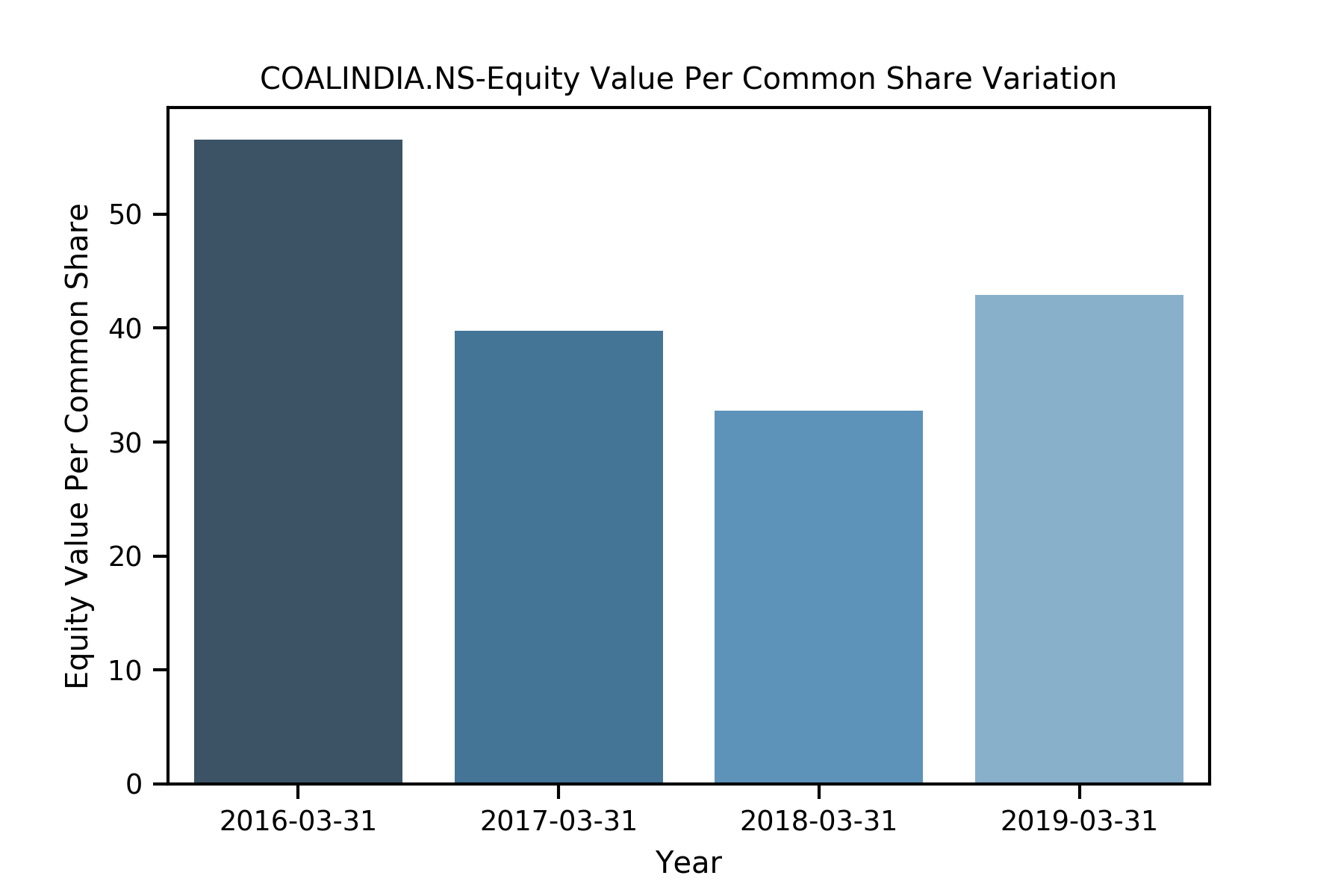

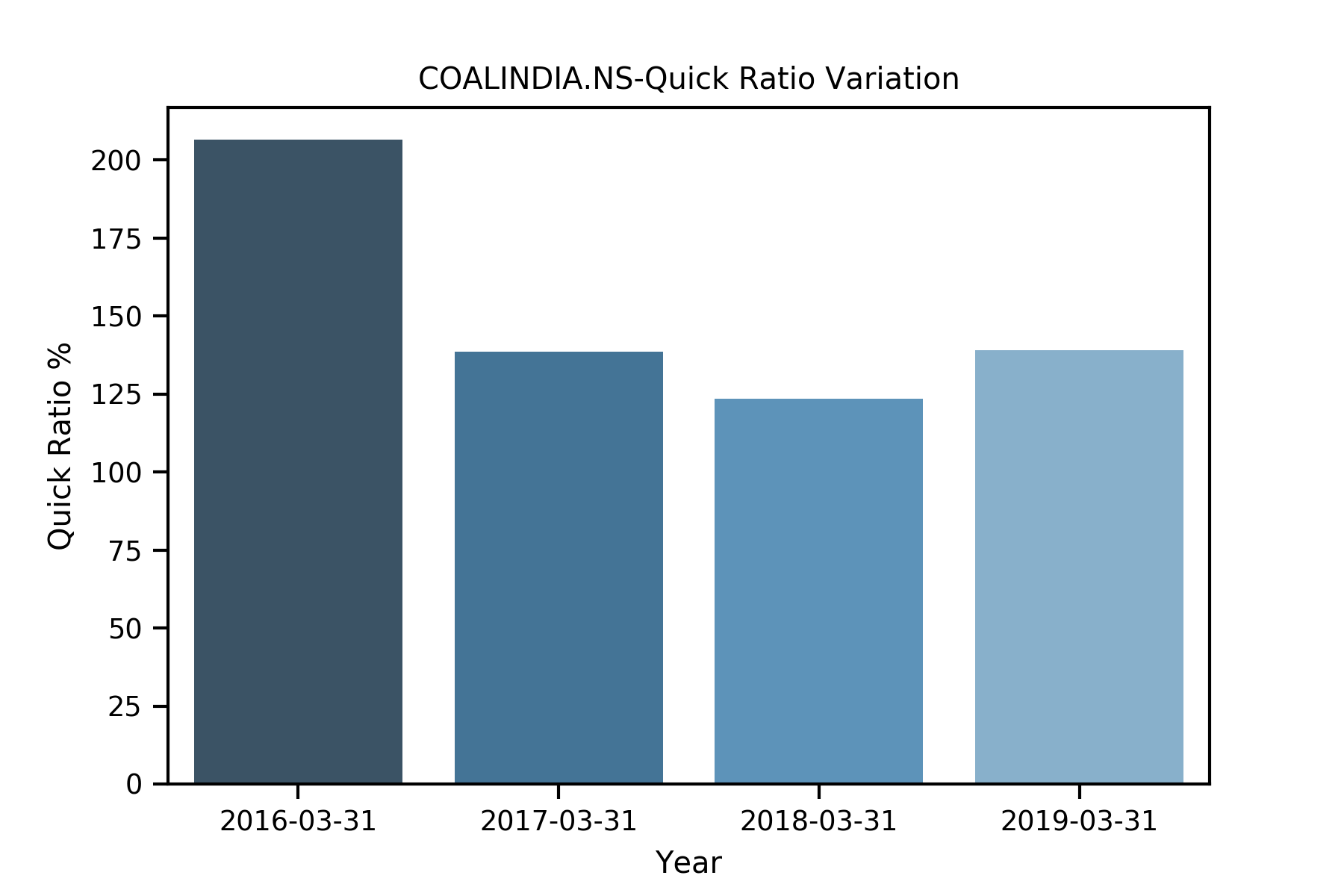

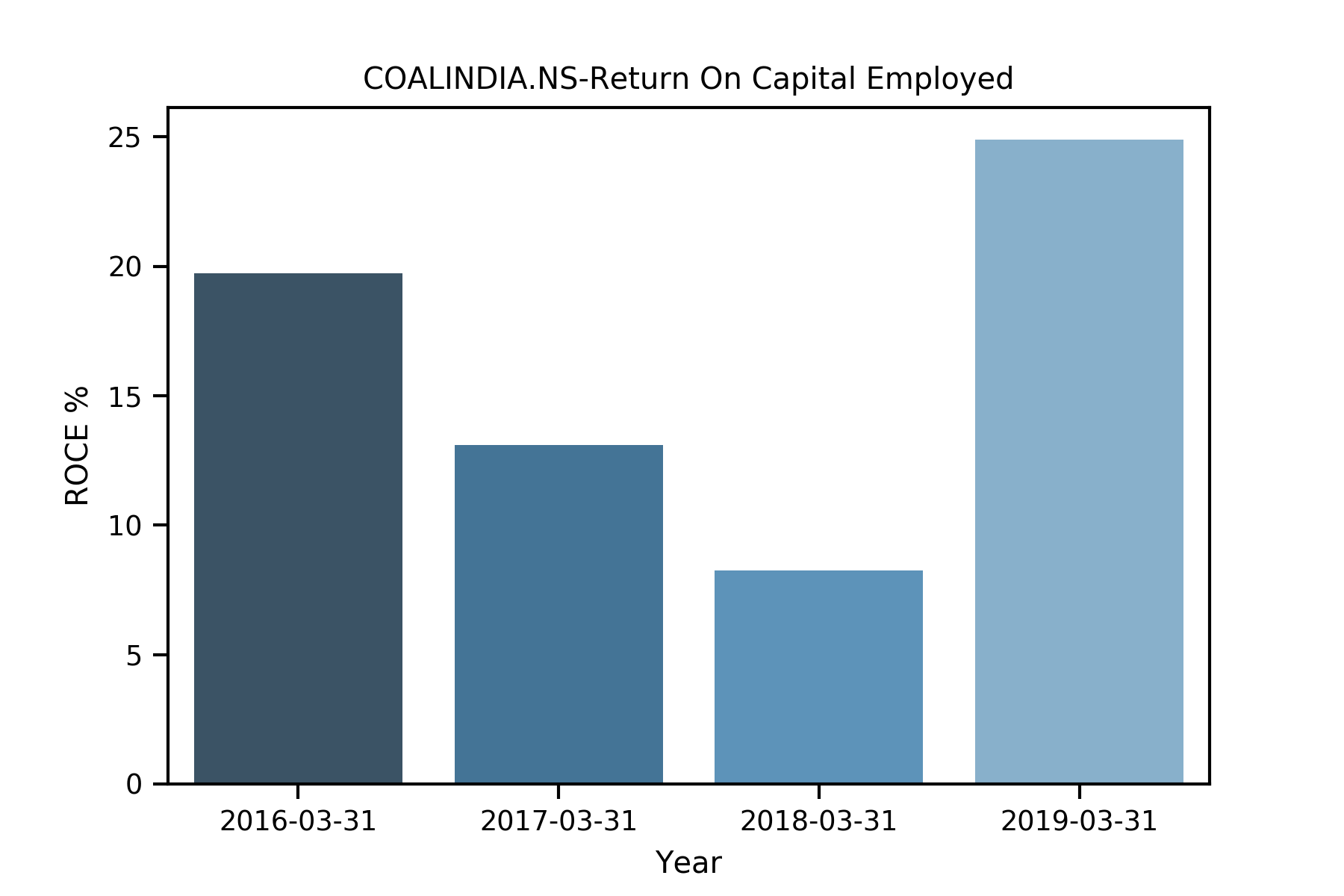

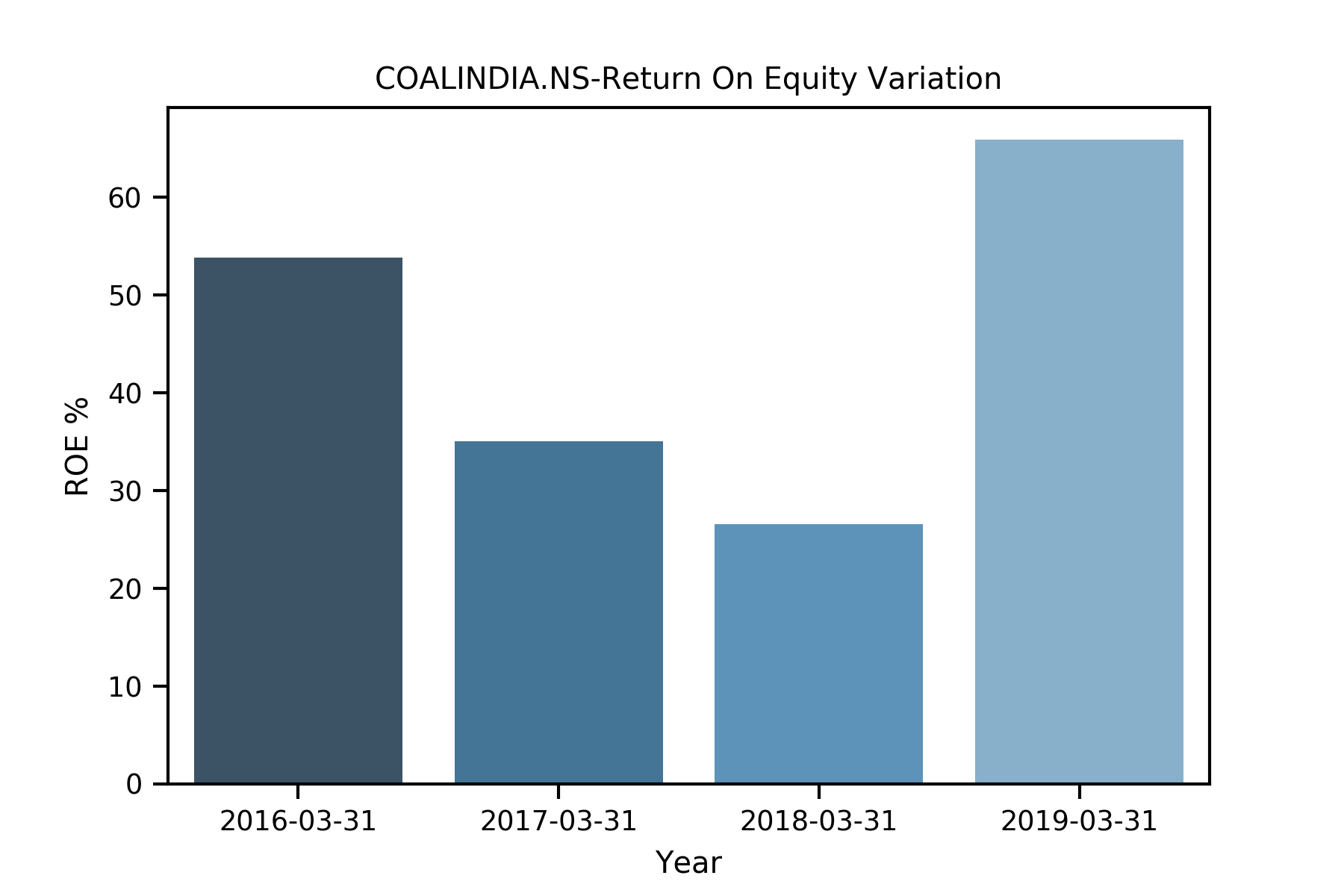

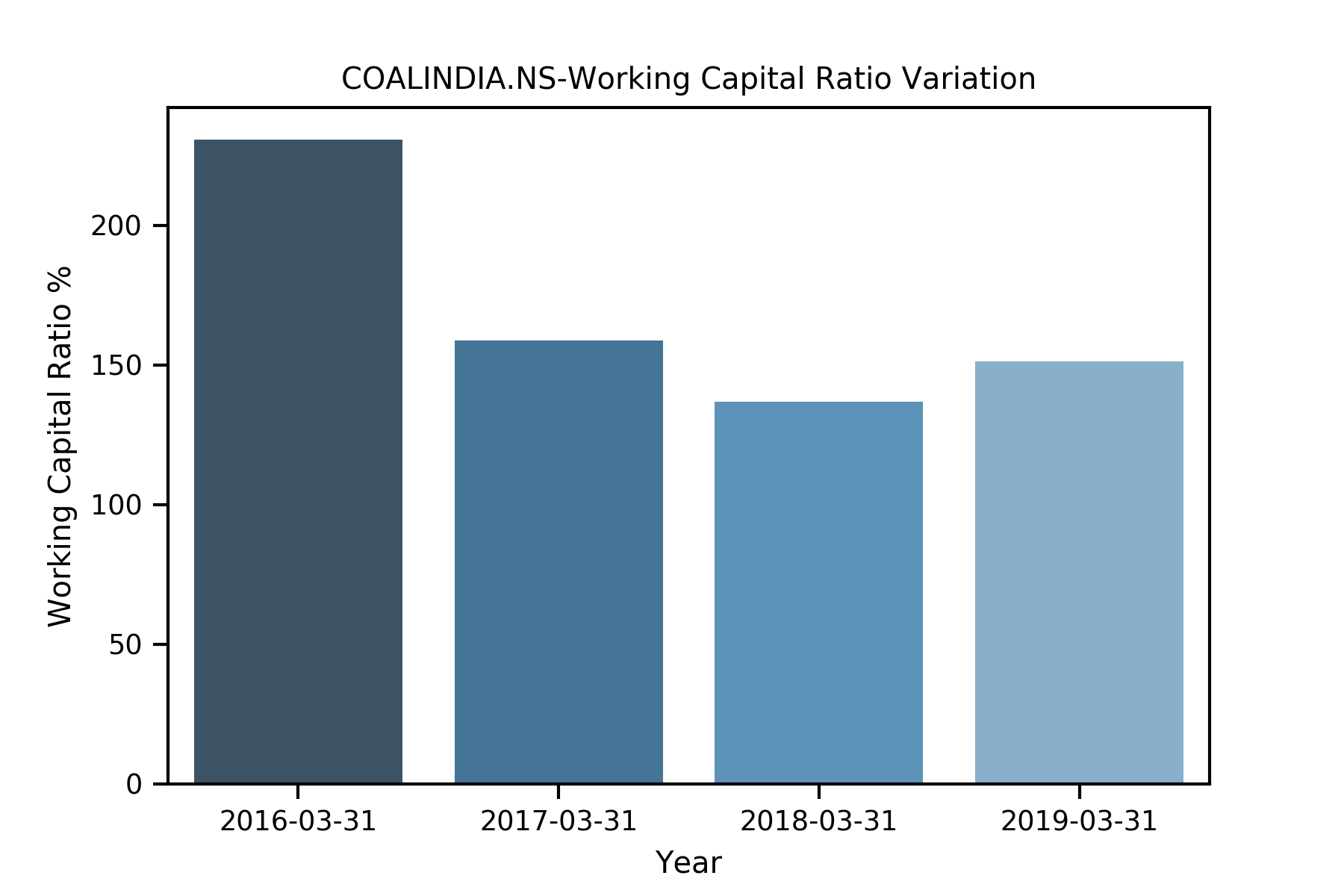

Finding Coal India to be quite cheap looking at historical P/E & P/B vis-a-vis ROCE, ROE, Debt etc.

Also assuming FY19’s dividend of current dividend yield is ~6.5%.

With EV/EBITDA coming out as 3, lesser than historical average of 7, valuation-wise looks quite attractive. Though, I would also like to know the impact of government regulations/next steps, etc. Looking for more expert / detailed views/opinions.

Disc: Invested since 3 years at higher MP. Currently in watchlist.

Coal India appears to be cheap on all measures with PE at around 7 wrt historical average of 14. ROCE and ROEs have been great. Dividend yield is 6%! I dont understand why is it available so cheap? Is it just PSU aspect or theres more to it? If a private company had such return ratios then it would have been a multibagger now.

Can someone who understands this throw some light on why it is so cheap? Were latest results exceptional? or Is it at a cyclical high?

Bought some today as a deep value play and with very good dividend yield. Will it go broke - no way.

Will its business be affected in the short term - yes, may be,but they will be back doing business again

Everything is moving towards an electric future. Based on that theme, how sustainable will investments be in Coal India? I am somehow not very comfortable based on that line of inquiry alone.

And from where you think electricity will be generating ? More than 60% of electricity in India is generated using coal. Besides, there are many other industries that find its application.

It has huge contingent liabilities. What is the probability of the case going against Coal India, wherein it will need to pay these liabilities. In such case its entire cash reserves will be gone.

It is negative for coal india as the private players might capture some of its market share. Don’t value a stock solely on pe basis especially for cyclicals and near term earnings de growth cos. The 4 pe is delusional. Reason is that earnings may fall in the coming quarters, so the result is denominator in pe decrease and thereby pe gets increased. As u said , the co has no debt but it has 83100 cr contingent liabilities which might have significant impact on the business when claims get materialised.

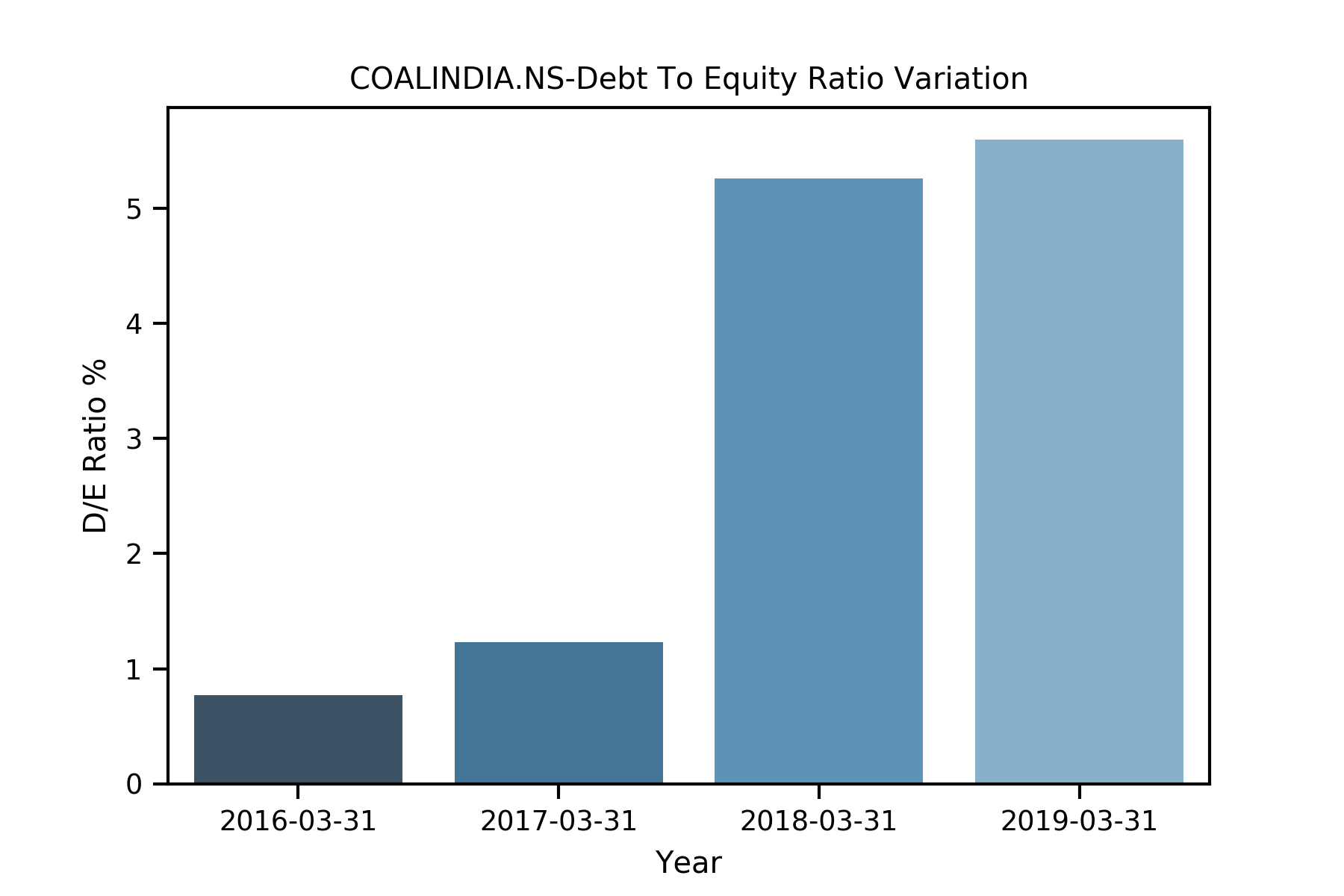

Company will have debt soon. Because of Covid 19, the company had to supply coal to gencos without receiving money in advance. Company is already in process to issue bonds

{kind=link}