I don’t see it that way.

India Power demand is growing 6 to 7% annually. There’s plenty of room to grow for Coal India inspite of giving away mines. Key is the Imports we do. If the new players substitute the imports with their coal, then Coal India would not need to lose anything. It will still grow.

Govt needs money post-covid so will look to Cash in from Coal India, so should minority share holders as well.

3 Likes

Renewables are catching up! Coal is passe. It is also a dirty fuel. I’d rather invest in green energies than in coal. It is just not sustainable in the longer run.

For:

I can’t agree more.

Gas (CNG/LNG/PNG) cheaper & more efficient & less pollutant, also government regulations & incentives prefer gas

Solar: Renewable, but I believe that it’s costly than electricity produced from coal, correct me if I am wrong!

Hydro: This alone has led to shutdown of thermal power plants in large number

Against:

India still import a percentage of coal requirement & the push to reduce import dependency has led to increased target on total coal produce, next 1-2 year has aggressive plans to increase the throughput, this should benefit Coal India.

2 Likes

Natural Gas is a good bridge fuel. I would rather better on IGL and Adani Gas than on Coal India and/or NTPC. IGL is one of my current favourites at the moment.

Coal may be dirty but renewables isnt the answer yet.

Two main problems with Renewables

i) Availability (its seasonal in terms of when energy is generated)

ii) No cost effective way to store Renewable energy

Unless, there are technologies invented for proper cost effective way of renewable storage, Renewables will only be a support infrastructure to coal than a reliable substitute.

Did you indirectly tried to prove @Avinash_Venkata’s point?

LPG/CNG/PNG are non-renewable source of energy!

If not, then the caveat in your logic is Natural Gas , as its neither dirty(relatively speaking) nor renewable!

I am not sure I understood you correctly.

Let me clarify where I stand :

i) Solar & Wind - renewbale. Great to see us expanding there. India is producing one of the cheapest Solar power. Wind power cost is also reduced thanks to innovative technologies. But this is largely seasonal. Since its seasonal, there is a need to store energy. But it cant be done on scale. No such tech available. So, Solar,Wind will be a addon rather than substitute

ii) Natural Gas is a clean fuel but Non-renewable. Manufactred by drilling & fracking. While drilling wells as in Qatar is not a big problem, Fracking technology used in US is a environmental problem. Fracking requires huge amount of water. There are lot of environmental scientist/activist who are against Fracking. It is cleaner than coal but still polutes in way it is produced. India imports significant Natural gas. Currently its cheaper due to macros - but it could turn again in few years.

iii) Coal - Dirty fuel - but this is what runs country today. We have 4th biggest reserve in world, yet we import coal. Import bill is atleast 1lakh crore a year. Cost of Indonesia coal we prefer on import + transport costs makes coal PPAs expensive than Solar/Wind PPAs (correct me if I am wrong)

My simple point is, Coal while is not desirable, its going to be required for years. For LNG, we need to keep increasing storage infra & import…at same time hope that prices in globe are cheaper. At same time, we need newer storage technology for Solar/Wind to make use of them efficiently. Power demand set to grow 5%-6% a year. So, IMO, Coal is there to stay.

5 Likes

My thesis is that coal has been a dominant source of energy for India. No doubt about that.

Natural Gas comes into picture here because it has a wide application in many industries that are important to India. For eg., fertilizers. Even if one were to look at electricity generation - natural gas is slowly displacing coal with the increase in number of gas fired plants. I see a more prominent role for natural gas. Much more than coal actually. The energy landscape in the country is evolving and with it, the role of natural gas in the energy mix too.

Hi All,

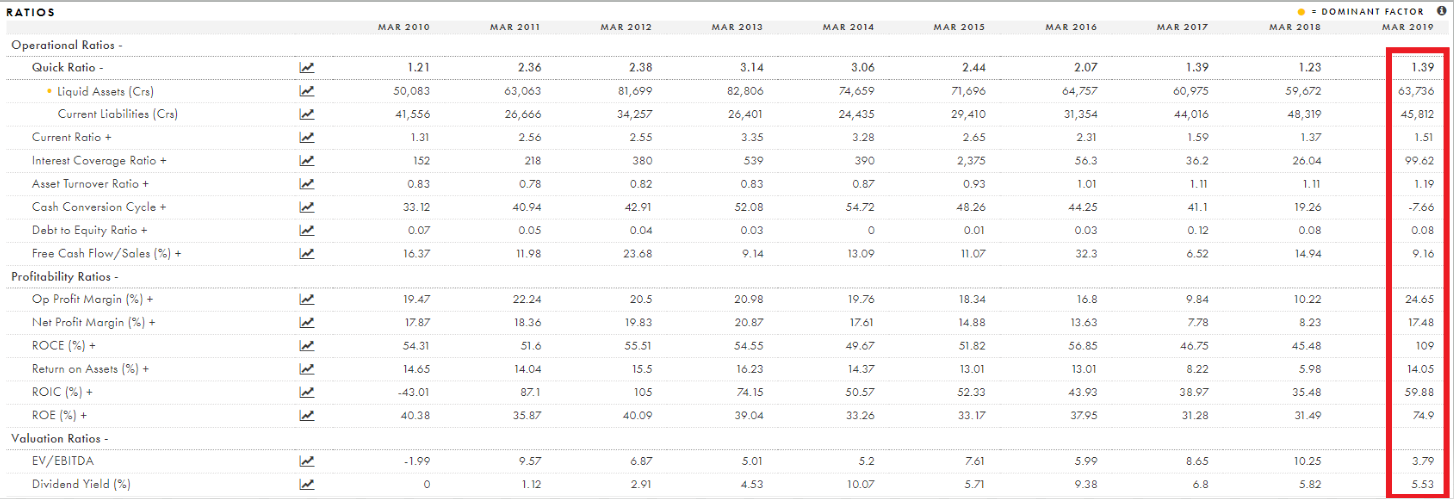

I’m also quite perplexed by the current trend in Coal India. If we look at the 2019 numbers, they show great promise. Yet, it seems to be a non-starter for many. I’ve held it since IPO & unfortunately CMP is 100 bucks less than the IPO. I’ve tried to read through the annual report for 2019 & the prospects seem to be good, gauging by the numbers. I’m a novice, still learning to read Financial statements; what am I missing here?

Please have a look at this insightful article on Coal India published on moneycontrol:

What we can learn from Coal India’s faulty capital allocation

1 Like

Hey Hardik,

The article is behind a paywall. Any chance you could paste PDF version of it?

Cheers

Also read this article on PSU stocks published by Marcellus Investment Managers:

What’s to lose in a 6x PE stock

4 Likes

All PSUs met the same fate due to pathetic bureaucracy. You name any PSU in like of SBI, Coal india, ONGC, and the list goes on and on. Bureaucrats are appointed in top management of these PSU who gets changed every 2-3years and most importantly they dont have any zeal to grow business rather they have zeal to grow their personal wealth only by using their position as office of profit

Thanks, mate. Did read through the article and now I feel the correct thing to to do is bite the bullet, book loss in Coal India & get out. Sad part is that I’ve been holding it since IPO, so I definitely saw better days than today. Should’ve cashed out when had a chance but then was busy in career etc (insert appropriate excuse) ![]()

1 Like

Coal India is trading at a low valuation now (EV/EBIT =2 and PE = 4.5) => Even if it continues whatever it is doing for few years, ull get your money’s worth in earnings… I would suggest to w8 out the down cycle unless u have another high conviction opportunity lined up/need the cash for something… Few years down the line when the fortunes change, it should go up again ideally and u can exit with profit

1 Like

The last decade was bad for PSU companies. The erosion was more in terms of PE ratios than absolute earnings. Please check in screener for yourself.

(Coal India Median PE is 16, now it is 4.5

GAIL - Median is 14.6, now it is 8.8

ONGC - Median is 11.2, now it is 5)

The kind of companies Marcellus loves had significant increases in their PE ratios.

There is a strong concept called “Mean reversion”… Buying a company at 100 PE blindly because it has been going up and selling PSUs at 2/3 PE because they have been going down makes no sense…

Warren buffet quote - “What the wise do in the beginning, fools do in the end” is apt here. My 2 cents for what it is worth - It would have been wise to sell many PSU stocks at higher PEs over the past decade and it would be wise to sell some of the stocks Marcellus likes now (> 50-60 PE and paltry growth)

6 Likes

While I do hold Coal India and a couple of other PSU stocks, I tend to agree with Marcellus’s take on PSU stocks and would not discard them at all. Time and again we have seen the government take minority shareholder unfriendly decisions leading to erosion of value. Even though Coal India’s PE is very less, the threats that the government will waste this money in non-value added acquisitions or unnecessary expenses or simply hold them as cash with no returns at all are real. I also believe that coal is pretty much a dying industry and these businesses won’t last beyond another 20 years and will most likely be loss making between years 11 to 20.

The only reason I hold PSU stocks is because I believe that as the Govt will be short of cash due to nil GST collections for nearly 2 months they will dip into these cash rich PSUs to take out the cash in the form of dividends. This, I hope will not only expand the P/E of these stocks but will also provide a more than satisfactory yield.

3 Likes

I believe that potential stake sales of PSUs to partly meet the ever increasing fiscal deficit of the Government is likely to be a key overhang on their stock prices.

Further, one of the key factors in my evaluation of stocks is Management. As has been highlighted earlier in this thread, PSU leadership undergoes frequent changes which does not incentivize them to strategically grow the business - plus there is always red tapism and bureaucracy.

PSUs may be good dividend payers with attractive valuation ratios but because of the reasons mentioned above, I’m not confident of their growth potential.

While I’m not advocating that we buy stocks suggested by Marcellus, I would personally stay away from investing in PSUs.

I agree many PSUs are problematic but some are grossly undervalued and should be very safe investments now. Considering many are giving dividend yields between 5-10%, their price cannot go down significantly further unless earnings suffer. And there are many PSU’s whose earnings just cannot decrease due to their nature of business…

Examples:

SJVN : Till Sutlej flows and people need electricity, this hydroelectric dam will make money. Considering the longevity of business and earnings visibility, it still trades at 3 EV/EBIT and 5 PE. Every 3-5 years, I will double my money even without PE re-rating or any new revenue from the dams under construction

PowerGrid: Again who can compete here with inter-state power transmission… This will keep making money for many many years and trading now at 8PE (It has grown at ~20% in the last 5 years and should continue growing as Industrialization increases)

Gas distribution and pipelines are another example. Unfortunately Indian railways is not listed (yet)

These form the backbone of the country and its a joke that they trade at 3 PE as if they have no future beyond few years. Apparently similar thing happened when England privatised its utilities and energy companies (Read in Peter Lynch’s book… He says whenever her Majesty sells, I buy ![]() )

)

The probability of next 10 years being good for select PSUs is high precisely because the last 10 years were so bad. Hope I am making sense…

11 Likes

@shivramrca

Thanks for the explanation & I hope what you guess regarding the dividends indeed turns out to be true.

@alexander

Incidentally, I hold Power grid as well from its IPO days. It has doubled from its IPO listing price in approx 10yrs which is nothing great really. However, still better than Coal India which is nearly Rs 100 lesser than its IPO price.

Apparent conclusion from these two stocks are that govt. run businesses are not good options for compounding wealth over a long period of time.

Cheers