AGM link plz… Did anybody know agm outcome…kindly summarise if anyone does

There was nothing much. Mr Garg spoke a couple of lines stating that the company performed well in the last year and hoping to do similar this year also. He said we are trying to sign up a few new customers in new geographies but gave no specifics. In the Q & A, there were only two speaker shareholders. The first one did not speak anything meaningful. The second one had a long list of business questions, but Mr Garg said you can mail them to us and we would reply to you suitably. The AGM ended.

I have expected more… New management reason to acquire, their vision, etc…Thanks for reply

I looked at the Screener and BSE, saw that the Promoter & Director Om Garg sold all his holding and also Veena Garg also reduced her shareholding and sold around 178cr in offmarket This seems to be some murky. Anyone observed something similar.

First concrete statement from Aditya Halwasiya: …"As the segment and business grows we will plan for capacity expansion at Cupid Ltd with a strategic and long term view.”…

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b7e70097-30c9-4b39-98f1-41499b229bf2.pdf

Earlier when the takeover was announced the press release had said "…I believe that the Indian consumption growth story is playing out before our eyes, and the next decade belongs to BHARAT. Cupid fits in perfectly into this Bharat growth story with its innovative line of products to cater to our relatively young population, which is getting more conscious and vocal about their sexual health, safety, and wellness”.

Most likely a retail foray into the domestic market is on the cards.

6 Likes

I don’t know if that’s such a positive news.

Whenever we brought up the topic of Domestic Expansion with Mr. Garg in concalls, the response was always the same - that Indian Condoms Market has a lot of competition and hence Margins are paper thin. There was some value in operating as a Contract Manufacturer for existing players, which I believe Cupid was already doing.

I assume things haven’t changed much now to warrant a foray into the Indian market as a competitor.

I guess we’ll have to see who is right - Mr. Garg or Mr. Halwasiya (Only on the matter to expanding into Indian market).

7 Likes

Building a retail business requires heavy investments in brand building, advertisement & promotion and distribution channels. It is natural to assume Mr. Garg unwilling to commit such investments that will take 10-20-30 years to fructify. It would be easy for him to rationalize his actions (or inaction, in this case) by pointing to lower margins. But Aditya Halwasiya is 29 and will have no such qualms. Markets value retail businesses more highly than others, and for a good reason. Mr. Garg’s reasoning was good for him, but for Cupid to realize its full potential, what lies ahead may be better. At least that is what the price action so far seems to indicate.

9 Likes

Any fundamental reason for the price surge…??

1 Like

Next Conference Call, with the new Management Team, will be held on 09 Nov 2023 (Thursday).

https://www.bseindia.com/xml-data/corpfiling/AttachLive/fa2e3cbc-1280-41d5-a389-24ae599c9cad.pdf

If someone can take short notes and post here, it would be great.

Thank you in advance.

Also it seems that indeed, Mr. Garg will be retained in capacity of Senior Advisor, which is icing on the cake.

2 Likes

Aditya Halwasiya had his first interaction with the analyst and investor community during the Q2 FY24 concall, where he outlined his vision and plan for Cupid going ahead. Some highlights from the call, edited and reorganized for clarity and readability.

-

Why he bought into Cupid - We have been in business for the last 60 years as a Family Group Company, the business we are in is close to maturing, and we feel that the sexual wellness and health and family planning business in India is at its infancy stage still.

-

Capex - Cash on books is close to Rs. 125 Crores, enough to triple our current capacity, including land acquisition, plant & machinery, and human capital. Currently we are at 95 % capacity utilization, so we have very good reason to do so (i.e., increase capacity). We expect our capacity expansion plans to materialize within 16 to 24 months. Going ahead, we would like to have a capacity of more than 1 billion units of male condoms and more than 100 million units of female condoms per annum. For this we will need to add 7 dipping lines (of 70 million units each) which will need Rs.50 to Rs.60 crores and the time will be about 2 years. Current capacity is 50 million of female and 480 million units of male condoms which yields close to Rs.150 crores of revenue.

-

Marketing - With the new capacity additions we would like to enter the international B2C markets using our connects who are already helping us participate in the tenders. This will be done in South American countries as well as South Africa. Simultaneously in India we will also push towards B2C in terms of introducing a few new products along with our existing products to help increase sales. We can give competition to any existing brand in India in female condoms. In addition, we have a team who is working on a very good marketing strategy to introduce our other products like lubricant jellies, male condoms etc. We will be packaging these products together and selling it in the Indian market. We are working on launching a new packaging for our product and new bundling are being worked upon. We will try to make sure Cupid Brand is visible in as many shops as possible in India (where condoms are sold).

-

Growth & margins - I expect at least a 2x growth from there in the coming three years. At the minimum we look to get 15 % to 20 % year-on-year increase in sales. We expect to start expanding by quarter one of FY2025. In quarter two of FY2025 we will start participating in tendering of IVD test kits also. We have EBITDA margins today at 12 % to 13 % for male condoms and for female condoms it is 31 % to 32 % currently. On these EBITDA levels we will be seeing changes of 3 % to 5 %. Overall, our margins will be higher than 20 % on EBIDTA level from next financial year. We expect to end FY24 with a top line of close to Rs. 140 Crores. Using that as a baseline, we will be doubling the revenues and bottomline in 3 to 4 years with a ROC of 20 %.

-

HR - We will be adding many key managerial persons in the C-Suite roster. The current individuals we have hired in the company have built great brands and great distribution lines. Mr. Garg will continue with the new management for at least three years.

-

Housekeeping - We do not want to try and blitz the market in any way because it costs a lot of money to do so. We would like to have a very good number of receivables, good quality receivables going forward. We are doubling down our efforts to improve SOPs in place because we come from a manufacturing background.

-

US foray - Expecting sales from US from beginning of CY 2026. As of today, we sell Maxima brand of female condoms in Tanzania. We will be selling the same brand at a more than double price in the US after we get the US FDA approval because that is the going rate per unit in the US for female condoms. Presently, there is only one qualified manufacturer who has complete monopoly for sale of female condoms in US. The guidance of Rs.300 crore revenue is excluding the US business.

-

IVD Kits - Large export tenders’ business is worth Rs.300 to Rs.400 crores. It can start from 2026 onwards once qualification requirements and regulatory approvals are in place.

-

Contract manufacturing - Discussion with the US company is going relatively well. We are in discussion at the technical level and exchange of information in terms of our manufacturing capacity and capabilities and their marketing requirements are going on.

-

Dividend - We would like to continue with the dividend payout but in the coming years it will be slightly less than what the shareholders have seen over the last 3 to 4 years since we are investing in the business for growth.

(Disc.: Holding)

20 Likes

Thank you so much for the detailed notes. Just a few queries, would really appreciate if you could point in the right direction

- I tried looking up Mr Halwasiya to understand the business he was referring to in point # 1 of your notes. Will really appreciate it if you could help.

- The contract manufacturing in Point #9 is for the male or female condoms and is it for the same market leader in the us that’s referred to in Point #7

Thanks in advance.

Regards

Disc:invested

Hi Everyone

I am a newbee DIY investor (erstwhile only investing through passive mode).

I have been tracking Cupid since past ~1 year and found this thread really insightful to understand the historical perspective & commentry of the business.

Wanted to understand whether the recent open offer by Columbia Petro Chem Private Limited & Mr Aditya, will have any major impact on the future business.

Also wanted to understand as to why the share purchase is done through an open offer and not share buy-back by the company.

Note: I am invested in Cupid

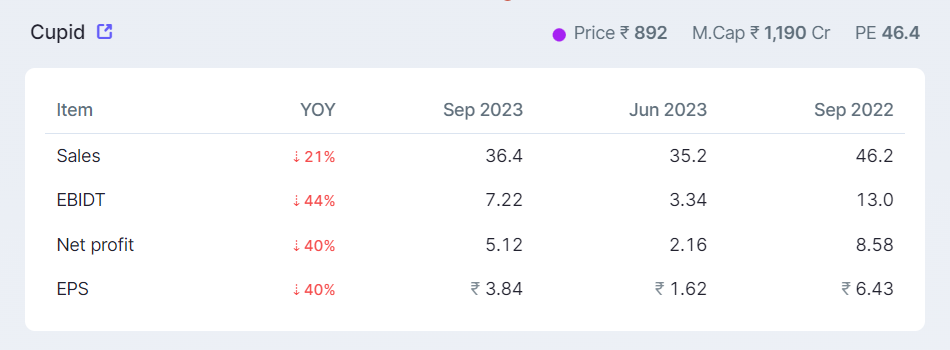

Looking at current rally…how much potential…sales and profit is not aligned with cost of share…is there something else?

Some details about the proposed fund raise emerge - company to raise $ 50 million, multiple FIIs have shown interest, says Aditya Halwasiya.

Some more points:

Funds to be raised for inorganic expansion

Aditya to be looking after day to day operations of the company

By end of FY26, capacity will be

- 1.25 billion MC

- 125 million FC

- 210 million 5 ml. sachets of lubricant jellies

- 30 million IVD test kits

4 Likes

The company had more than enough internal Capital to drive at least the initial phase of proposed growth. I fail to understand the immediate need for a fund raise.

But I guess we’ll have to give the new management some rope and wait for proof of actual execution.

6 Likes

Sold completely … Not sure of sustaining at current level…

1 Like

Looks like apart from fund raise they are also planning for stock spilt and bonus l…

New owners are using all the levers available to them to prop up the stock price…not a good sign for long term investors, although stock may perk up in the short term

1 Like

Though i partially agree, but considering the bull run we are witnessing, its not wrong for the promotors to raise some money for future growth. Just look around, recent IPOs like Motison Jewellers, or old names like Praveg, with much less business history and still lesser Profits are commanding higher market caps. But yes agree seeing the highs every day is dizzy and maybe prudent to book some partial profits…

Btw Praveg is also doing a fund raise on 23rd Jan; with preferential allotment to large mutual fund houses and HNIs at price of 670 while current price is 1200+… To be noted that the price at the time of the fund raise announcement was around 700!!