the expansion plans mentioned in the interview is just doubling the existing capacities. i wonder why they require 50 mn dollars from the market. we are already having a cash of 115 cr. ( investment+ cash).

Disc- Invested

2 Likes

This question is coming up again and again – why the company needs the money. In the interview, Aditya Halwasiya mentioned that the existing cash is enough for organic expansion, while new funds would be used for acquisitions. I think going beyond that, a more pertinent point is that there is good amount of institutional interest in investing in the company. When cheap money is available in plenty, any promoter may want to take it and put it to good use, if he is ambitious enough and wants to go for aggressive growth.

In condoms, Aditya has spoken about retail expansion. Retail expansion is a very capital-intensive activity. Brand building, advertisement & promotion, deep distribution network, inventories and even getting top class talent – all of this requires investing huge amounts of cash for prolonged periods of time. People don’t think of them as investments since much of it is expensed in P&L, and hence the epithet “low margin business”. Condoms are a Rs.1500-odd crore market in the country which by itself is not large. But within that a lot of innovation and premiumization is happening. Last year, Raymond sold KS and Kamasutra brands to Godrej (GCPL). Listen to what the GCPL management has to say about the acquisition:

And this:

But going beyond condoms, Aditya Halwasiya’s comment seemed more oriented towards IVD kits and the broader medical devices business. This is a 10X bigger market and growing faster than condoms. Here, Cupid is starting from near zero, so growth can be very fast. In the interview, Aditya said Malaria, Dengue, Typhoid, Syphilis, HIV etc. all require tests to be made. Currently Cupid is manufacturing test kits for all. Though not an exact comparison, a small company called 3B Blackbio DX Ltd. which is into molecular diagnostics and biological devices such as RT-PCR tests, mutation detection kits, genetic sequencing kits and so on is trading at 9 times sales.

Beyond test kits lies the broader medical devices universe. Morepen Labs’ medical devices business grew 41 % in H1 FY24 and the company said the market itself is growing at 25 % CAGR. Morepen is into devices such as Oximeters, Glucometers, BP monitors, pregnancy kits and so on. TTK Healthcare’s medical devices division grew 23 % in H1 this year. This was on top of a 41 % growth in FY23 and 90 % growth in FY22.

And then there are exports. Aditya said they plan to participate in international tenders after getting regulatory approvals. Increasing adoption and usage of medical devices and health-tech is a secular mega trend. Besides, India currently is a huge importer of medical devices but there is a push towards import substitution and self-reliance under the broader Atma Nirbhar principles.

Coming back to condoms, the business will get a big boost if the next government brings in some form of Population Control Bill. Any such initiative may come with a complementary scheme for encouragement, popularizing, procurement & distribution, and subsidizing of condoms. ‘Mission Parivar Vikas’ was launched by the government in 2016 for increasing the access to contraceptives and family planning services in the country. It has been a low-profile scheme so far. But having focused on water, electricity, gas connection, housing etc. in its first two terms, the next term could see family planning being pushed higher up the priority list. Of course, I am speculating here – I do not know if there is any such move – but it is not impossible to imagine. May be someone in the government is already working on it, and the market has got a wind of it.

This is as far as we can see. Tripling of capacity is not the only thing that is changing at Cupid. An ambitious promoter with access to cheap money and a large opportunity size can do a lot of things. Aditya Halwasiya need not reveal all his cards at one go, there could be more up his sleeve. But so far at least, he has made all the right moves for sure.

(Disc.: Invested. Not a recommendation. Please do your own research)

13 Likes

The results are out. But I don’t think there’s any merit in discussing them until the New Management starts executing their plans.

There’s another interesting bit of activity.

48,000 Stock Options issued to employees at an Exercise Price of Rs. 140 with 50% Vested in the 2nd year and 50% Vested in the 3rd year.

3 Likes

These Options with such small vesting window should surely weigh on the future stock appreciation; unless the stock options have been given to the promotors only!

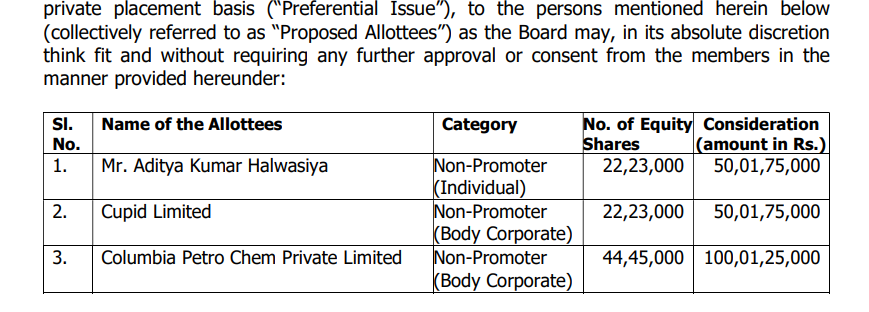

Warrants to be issued at 1750 convertible to a share face value 10 within 18 months

Also, Minerva fund last purchased 70K share at 1862 on 20th Jan

Bonus 1:1 and split from 10:1 face value would bring enough stock trading liquidity

disclosure: exited last week but interested

1 Like

Bonus, increase in authorised cap, board approval to borrow upto 1000cr,entry of big investors …

Looking for aggressive growth???

Let wait for concall

Exited at 1510…

Is it right to keep exercise price of ESOP to employees at 140 when market price is 1810? How to interpret this?

I think we need to understand to whom it was given.

If it’s to the employees, I think it’s a reasonable way of motivating them. Many companies have ESOP plans and I believe this specific plan began when Mr. Garg was still running the show.

Or course, any dilution is bad for Shareholders. What matters is what benefit the company gains from giving them out. It could be for retaining good talent, motivating employees or simply thanking them for years of service. If that converts to better work culture/ethic in the long term, that’s a win-win for both employees and shareholders.

I only hope that the new Management is open to discuss these matters in detail. If they’re not, I’d get suspicious for sure.

4 Likes

Big decision for me today.

I’ve completely exited Cupid @ 14x from the Average Cost and almost 18x from the Lowest Cost.

The primary reason is the Valuation. Even if the Revenue triples in 5 years as targeted and you apply a high growth rate post that (Say 20% for 20 years), the company would still be Overvalued. The Valuations could still support a very Bullish case, but I’m not comfortable with that.

Lessons I gleaned during this journey:

-

“Promoter Risk” is overrated (Unless in cases of fraud). At the best, it could be a Minor Risk. Of course a passionate and driven Promoter is excellent. But if the Business Fundamentals are strong, even a decent successor will be able to run it effectively. So, Fundamentals before anything else.

-

There will be thousands of naysayers for any given investment. It’s your job to monitor and justify the investment to yourself. Conviction is your rock. Conviction comes from cold, hard, self-introspected facts and not opinions. Opinions, especially from experts, do matter. But you’ve to verify them yourself against data once to build up Conviction.

-

Finally, an often repeated one — the patience to hold is one of the paramount virtues in investing. It’s as important as buying at the right price. If you’ve done all the work, then holding is the final lap. Do it well.

My sincere thanks to Mr. Garg and all the very best to Mr. Halwasiya for the future.

Note: I might consider entering again after seeing more proof of execution. At a much, much lower Price though for sure.

33 Likes

Hi Dinesh Sairam, really appreciate that you took time to mention about your exit! Really helpful. I am sitting at 12x position in Cupid and contemplating a partial profit booking.

Regards,

Dinesh

3 Likes

Did anybody attend today’s EGM? I logged in but was able to only see the speakers and could not hear anything, as if everyone was on mute. Was anybody able to hear the proceedings?

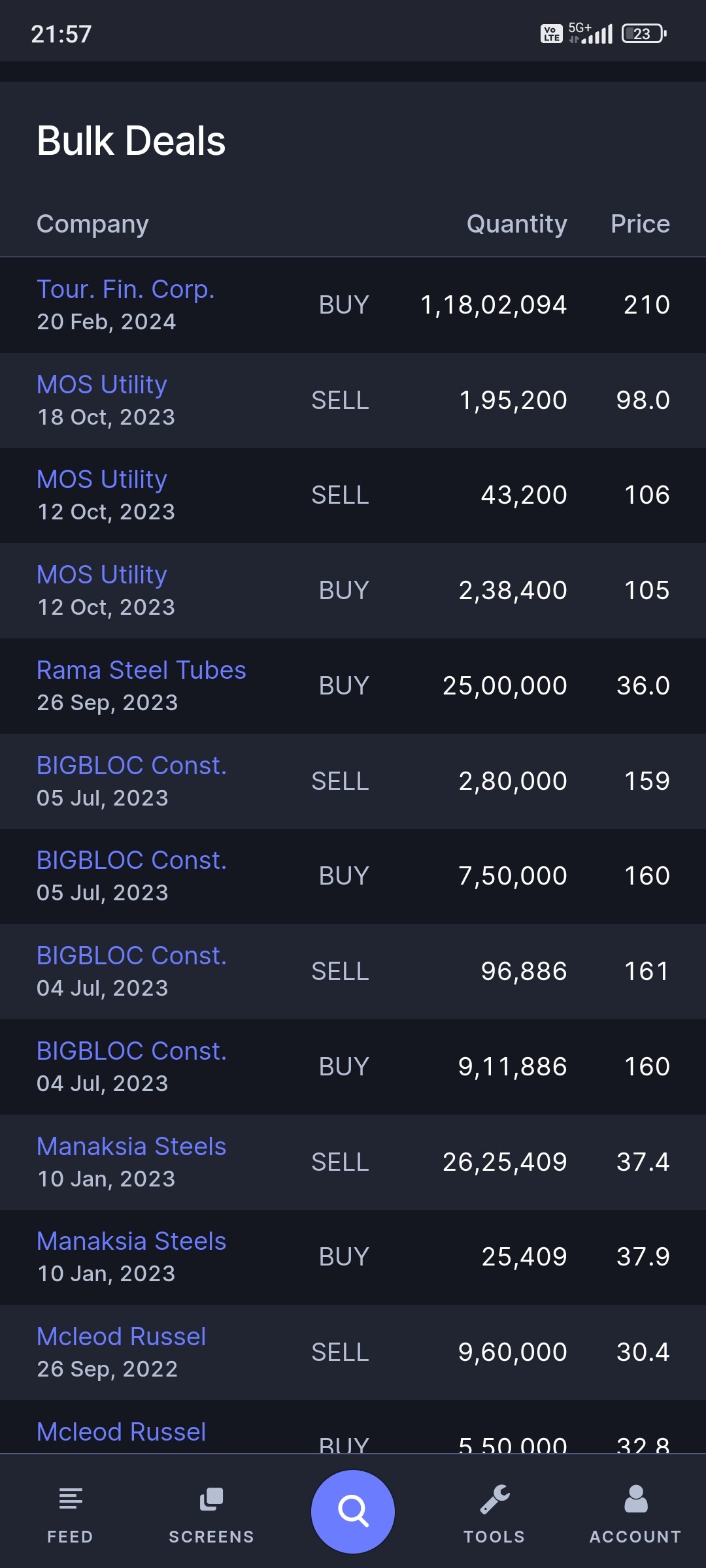

Adtiya buying stake in tourism finance …Any views ???

Bought in personal capacity as a financial investment, should be okay I think. So long as he hasn’t leveraged himself or pledged Cupid shares…

Ageed… Personally felt that the valuation of cupid is not comfortable for him to buy more …

Disc : i am exited at 1500

While its perfectly Ok for Mr Halwasia to invest in his personal capacity but just wondering out aloud, does this not take away management time and thinking from focusing on growing Cupid. Never saw that under the previous management of Mr Garg, hence a little uncomfortable!

Anyways the stock price has continued to do exceedingly well, regret having sold earlier ![]()

Does anybody know what happened with the EGM? There were proposal for stock split and bonus shares in January. Does anybody know what happened to that?

Rightly said… He invested almost 200 cr in TFCI as per the bulk deal… whereas investment in cupid is also similar…also he has stakes in other companies too which may become distraction

Exited fully at 2k.

1 Like

All resolutions were passed

https://www.bseindia.com/xml-data/corpfiling/AttachHis/3b4e4f90-1152-4ffd-9c2f-092b2357e883.pdf

1 Like

There should be no regrets in the market, only learnings! I resisted selling until this week, but have exited completely this week when the following information came to light:

SKM_458e24022810080 (bseindia.com)

Cupid is also buying Rs.50 crore of TFCI shares.

I haven’t studied TFCI, maybe it is a bargain at Rs.225 but I inherently don’t approve of such capital allocation decisions. It creates a future risk as well, since you never know what Cupid’s cash surplus will be used for.

10 Likes

Hi everyone! Been a while since i tracked valuepickr, its nice to see that the old timers have created good wealth by being patient with cupid.

A lot has been said about the valuation that its trading at and i have a viewpoint on it too… please share your thoughts if anyone has looked at the valuation with this perspective.

As we all might agree that the company was quite undervalued while mr. Garg was at the helm(though i am a fan) with 12 -15 kinda multiple. So getting in fresh management who is putting his own money on the line should definitely rerate the company… question is how much… so in a market like India with decent growth,roe, margins etc a multiple of 30 to 40 can be justified.

The kicker comes in with the fund raising… as i understand by raising 400cr, historically cupids roce has been 25%+ … lets say they are able to generate 20% on this 400cr conservatively which is around 80cr.

As they are already making 40 to 50cr steady state business. So a few years out( may be 2) we could see a 130 140 cr kinda bottom line… and hence the 3000cr market cap.

This is just my understanding as to why the market might value it in a certain way… its more in the art territory than science now, but as there are no revenues from ivd , nothing from usfda , nothing from Singapore tie ups, there are multiple optionalities attached.

Im not making a bull case, but only trying to understand why this valuation is justified and fiis are willing to invest.

6 Likes

The answer is simple and you most likely know it. The Valuation is not justified. We cannot use FIIs entry level as a gauge because we don’t know their thesis or most likely their investment could have been made based on their discussion with the new management.

The only way I can see the Valuation making sense is the bullish case I described before: Sales/Profits tripling in 5 years and then growing at 20% for say 10-15 more years. It was hard for me to envision that happening and the major reason behind my selling out.

8 Likes