The chaiman is willing to sell at Rs300/share which is a valuation of 5.5 times in terms of EV/EBITDA. Why is he eager to sell at such a low valuation ? Only cyclical commodity companies get such a low valuation. Cupid deserves 10 times its EBITDA. Can someone clarify on this price mentioned by CMD.

5 Likes

Wonder why has the employee cost increased so much from last year June of 285L to 485L? Is it the ESOPs which are being amortized over quarters? Till when will this cost be deducted?

If ESOPs are being given, why is paid share capital remaining constant at 1333.8L?? Also what is captured in Other expenses which has also doubled over last year June from 743L to 1516Lakhs?

1 Like

The market also does not believe he will sell at 300! Or is it the general bull market in small caps ![]()

Any reason for today’s rally???

get out. management undervaluing the company is a very serious red flag.

I don’t find it as a red flag. That’s why continued buying even after his statement at 250 levels. It could also be a loose talk from the chairman. He could have chosen not to answer because the question itself is unusual one for a earnings conference call. He might have thought that he conservatively told minimum 300/share but unfortunately it creates panic among retail investors. But intrinsic value is 400/share. Thats for sure. Sold half of my holdings today.

2 Likes

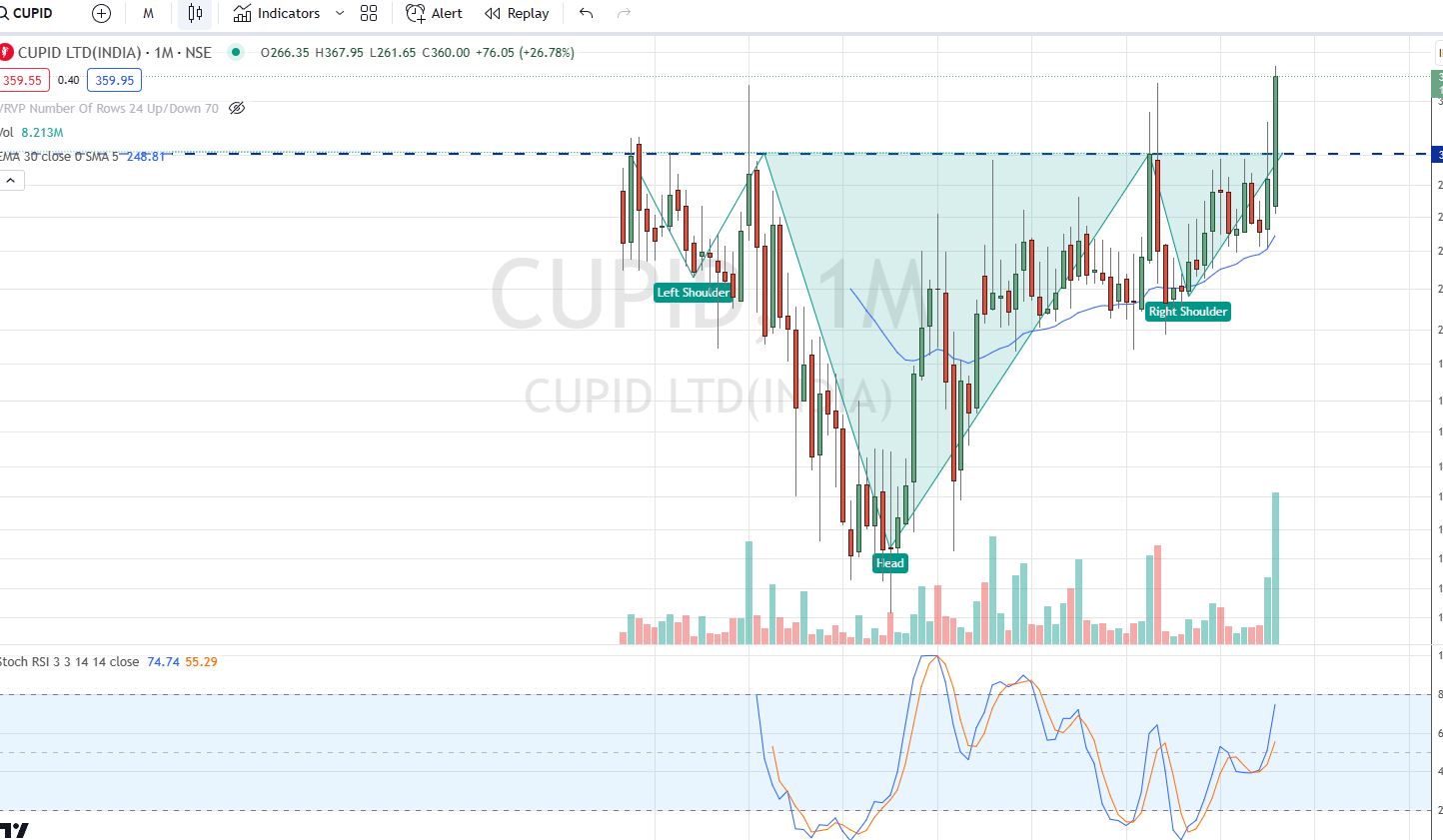

Cupid after 6 years , breaking out of the Inverted Head and Shoulders pattern on the monthly chart with high volumes.

3 Likes

Cupid’s sales growth and margins peaked in March 2017. Thereafter sales have shown a jump in FY20 but stagnated since then. Last 10-year sales CAGR is 19 % but last 3-year CAGR is almost zero. Management has indicated no growth in revenue and profits for FY24 as well. Clearly, business is very lumpy by nature. For example, in FY21, Brazil business was more than Rs.50 crore but in FY22, it was Nil. In FY23, South Africa contributed Rs.43 crore but in FY22, it was nil or very small. Such lumpiness is not good for stock valuation.

Margins have declined from 41 % in FY17 to 26 % now. Q1 FY24 was worse, with margins at less than 10 %, part of it due to a penalty for quality issues. But even excluding the penalty, margins were sub-20% which are lower of the range.

Over the years, capex has been minimal, gross block is Rs.73 crores. Most likely, an old, depreciated plant produces products that just about meet minimum quality standards to help bid for tenders. The recent penalty on account of quality issues could be a reflection of this.

ROE / ROCE is good in the range of 20 % plus aided by low denominator. Dividend payouts have been okay at around 30-40 %, which indicates management has been able to sweat the existing assets well but has refrained from deploying more money into the business.

Going ahead, the IVD business can take off meaningfully only from FY25 if at all, not before. In this, the management expects Rs.50 to Rs.100 crores business per year from FY26, and though the margins in this are said to be good, it will also consume Rs.30 to Rs.40 crore working capital per year. The U.S. business too will not happen before FY25, after which the company expects about Rs.8 crores of revenue in the first year. And, though the long run potential here is much larger, it will also be a tougher market. The current management, with their reluctance to make investments in branding, distribution, or technology, may not be best placed to realize its full potential.

This brings us to the point that only an ambitious, aggressive management can realize the potential of the business. But at the current share price, management’s stake sale efforts are unlikely to find any takers.

Current market cap is Rs.500 crores but free cash is around Rs.100 crores, so business is valued at around Rs.400 crore. It generates around Rs.20 crore of free cash flows per year, so excluding cash in hand, current valuation is about 20X the CFO, or a 5 % yield. Will someone pay Rs.400 crores for a business which generates Rs.20 crore of FCF and has less than Rs.100 crore of assets? Generally, buyers justify M & As on grounds of intangibles – brands, technology, distribution network et al but here there are none. Cupid’s assets are registrations and approvals, but the existing ones have been fully harvested and impending ones are at least couple of years away. And when the promoter is on record saying he is expecting “minimum Rs.300 per share”, it is unlikely someone will pay anything close to the current market price to buy the promoter stake.

The only other trigger is a possible buyback. Though Cupid has Rs.100 crore cash, note that a company can buyback only up to 25 % of its capital & reserves, which comes to around Rs.40 crore in this case. With Rs.40 crores, Cupid can buy back 8 % of its equity at say Rs.400 per share. This is a good proportion but does not help promoters exit the company, which is necessary for the business to realize its potential. At the most, it will help retail investors liquidate a part of their holding.

(Disc.: Holding)

11 Likes

I fail to understand why U.S. will be a tougher market. The only competitor for the Prescription Female Condoms in the U.S., FC2, produces in the U.S. itself. Cupid, producing in India, has a large margin to compete on price if required. FC2 itself recognises Cupid as a threat to their business (Evident from their Annual Reports and other releases).

I am on the fence about the IVD business. If they can achieve the targets provided, it will be a lucrative business. A lot depends on execution.

But agree on the comments about Management Sucession. The search for a good CEO or Sucessor to Mr. Garg has been nothing short of disappointing, especially with the intent of Mr. Garg wanting to sell his stake in the business becoming quite apparent.

5 Likes

Hi, My assumption is based on stricter regulatory scrutiny, more powerful distribution channel (pharma companies are facing this) and more competition. But I am surprised to hear there is only one player in the market at present. I stand corrected to that extent. I will dig deeper into this sometime later when time permits. Thanks for pointing out.

3 Likes

So here it comes…! Promoters exit at Rs.285 per share. Open offer at Rs.325 per share.

3 Likes

Couple of things I wish to understand:

- How come the open offer is at a price higher than what the management sold at? 325 vs 285! Does it indicate the short term base for the stock? with the new promotors willingness to purchase price 325

- Also why did the price run up during the late Friday trade, it seems the deal got leaked yet the market price kept inching up… was the market hoping to extract more for surrendering their shares… however point 6.3 in the PAC clearly states “The Open Offer is not conditional upon any minimum level of acceptance pursuant to the terms” of Regulation 19(1) of the SEBI (SAST) Regulations.

- What is the background of the new acquirers; can they really take this to the next level?

2 Likes

Aditya Kumar Halwasiya is additional director in Apollo Micro system and his bio as below (from AR):

Mr. Aditya Kumar Halwasiya holds a Master’s degree in Global Finance from Fordham University, New York, USA, and a Bachelor’s degree in Commercefrom St. Xavier’s College, Kolkata. He is a Dynamic 3rd Generation Entrepreneur, Investor and Scion of the Pan - India Universal -Halwasiya Group founded by the Late Shri Madan Mohan Halwasiya in the early 1960s. The Universal-Halwasiya Group has a Turnover in excess of INR 2,000 crores annually. He is a shareholder & director in the automobile, industrial oils and specialty chemicals Manufacturing company Universal Petro-Chemicals Ltd and actively looks after business marketing since 2019. He has an advisory role since 2019 in the family concern Columbia Petrochem Ltd also in the automobile, industrial oils and specialty chemicals business. He actively manages and oversees a sizeable portfolio of Capital Market Investments and Real Estate Investments & Projects in India.

7 Likes

Hopefully this leads to Cupid getting a good CEO to run and grow the business. Much remains to be seen still. But the first order of business would be having a concall with the new management (Once setup) and understanding their vision for the business.

Although I’ve been frustrated with the current management for some time now, I have to heartily respect and admire the effort Mr. Garg put in to bring Cupid up to where it is today. It’s a long shot - but it will be good to have Mr. Garg in Cupid in some sort of Advisory capacity to the incoming management.

5 Likes

As a small time retail investor who owns this stock, what wil be the wise decision?

- “I haven’t seen significant returns on my investment, which I initially hoped for in the distant future.”

- “My entire investment strategy was based on the expectation of obtaining USFDA approval.”

- “I’m prepared to hold my investment for the long term in a private entity , rather than selling and realizing a small profit. However, I’m uncertain about the legal implications of this decision.”

2 Likes

I didn’t understand your observation in regards to the legal implications of the transition to a private entity. The new management has no plans of delisting Cupid, as per their press release.

A concall with the new management would be great to understand their plans for the company - in one of the releases, the new owners hinted to the opportunities in a growing domestic market, a place where Cupid never really participated.

2 Likes

Garg informed in concalls that doomestic margins are low…

Hope new management will through some light soon

Understood. Thanks for clearing my misunderstanding

Any relevant information in open offer???

Other than the price

https://www.bseindia.com/xml-data/corpfiling/AttachLive/DD24DF6B-4457-41A2-AFDD-A300599350FA-142313.pdf

1 Like

Thank you for @SirSmartBeta on Twitter for bringing this to my attention.

Over the last 6 months, there has been a suspicious surge in Bulk Deals on Cupid Limited. While the data does contain some well-known investors and smaller private funds, we can also see 4 odd private businesses investing in the firm - put together to a tune of 3%+ of Cupid. The common denominator between these firms is that they’re all from West Bengal.

| Client Name | Address (Tofler) | Directors/Partners | Net Bulk Deal Done in Last 1 Year | % of Ownership in Cupid |

|---|---|---|---|---|

| JAI MAA VINIMAY PVT LTD. | 71 JODHPUR PARKLAKE P S, , KOLKATA, West Bengal. | Narayan Choudhary Ankit Kakarania |

100,000 | 0.75% |

| PLASMA COMMERCIALS PRIVATE LIMITED | ROOM NO.415, 4TH FLOOR, NEW ALIPORE MARKET, BLOCK M, NEW ALIPORE, KOLKATA, Kolkata, West Bengal | Pranay Dhelia Ankush Dhelia |

125,000 | 0.94% |

| RADHARANI SALES PRIVATE LIMITED | 32, EZRA STREET, SUITE NO.554, 5TH FLOOR, KOLKATA, West Bengal. | Sanjiv Kumar Singhania Vivek Singhania |

101,319 | 0.76% |

| GARG BROTHERS PRIVATE LIMITED | Garg Brothers Pvt Ltd is at 180, Rabindra Sarani, KOLKATA, Kolkata, West Bengal | Keshaw Kumar Bubna Madhaw Kumar Bubna Dindayal Bubna Gopal Kumar Bubna |

80,000 | 0.60% |

While this entire thing looks murky, two of them stand out:

- Plasma Commercials is registered in Alipore. You know who else resides in Alipore? Acquirer No. 2 Mr. Aditya Halwasiya (According to the Offer Letter)

- Garg Brothers was registered way back in 1984. Cupid Limited was incorporated in 1993. I wonder if there’s any connection between the Garg Brothers of Cupid Limited and Garg Brothers Private Limited (Based on the list of Directors for Garg Brothers Private Limited, it doesn’t seem so at first glance).

I say ‘murky’ because of the relationship between these companies’ Capital size and the size of their investments in Cupid.

| Client Name | Paid Up Share Capital (a) | Current Stake in Cupid (b) | Investment Size (b/a) |

|---|---|---|---|

| JAI MAA VINIMAY PVT LTD. | ₹ 10,000,000 | ₹ 39,000,000 | 390.00% |

| PLASMA COMMERCIALS PRIVATE LIMITED | ₹ 49,700,000 | ₹ 48,750,000 | 98.09% |

| RADHARANI SALES PRIVATE LIMITED | ₹ 210,000 | ₹ 39,514,410 | 18816.39% |

| GARG BROTHERS PRIVATE LIMITED | ₹ 64,500,000 | ₹ 31,200,000 | 48.37% |

Without throwing stones from the get-go, one of us who attends the first concall with the new management should bring up this subject. If I manage to attend the call, I can bring it up myself. If I don’t, this is a sincere request from my side.

13 Likes