One time loan was taken for working capital requirement of a large order. They had FD of similar amount but interest paid on loan was lower than interest gained on FD. If you check H1 details of current FY, the loan amount is reduced & it should be paid back in this FY itself.

As per Q3 concall, company had 54Cr cash & cash equivalents on 1st Jan2021 in books.

Thank you for the clarification.Still i am having one more doubt.The company has delivered the product to more than 83 countries,But still cupid product’s are not well advertised in india.Because if we think about condoms,mainly come to our mind is MOODS,Kamasutra.Why the management has not concentrating on marketing in india.In interview cupid ceo says that,we are the first indian company producing female condoms in india.But we didn’t see any cupid related advertisement or marketing related things in india.Are the management having lacking of skills in marketing in india.Please share forum point of view here…

The B2C condom market in India is riddled with competition from 15-20 players for a market size of Rs. 1,500 Crores. Apart from the top dogs like Mankind, Skore, HLL Lifecare, TTK etc., the rest of them have sporadic Revenues and Profits. Even for the ones mentioned above, it’s not all rosy. Take the case of Skore, for example. They make about Rs. 15 Crores in Profits. But even they regularly spend Rs. 8-9 Crores on Advertisement Expenditure. So, they must constantly reinvest close to 50% of their Net Profits into Ads just to keep the treadmill running. It’s not worth the effort to try and capture this market.

Wow…Such a detailed review.Now i have some good clarifications about what i had asked the questions before.Thank you so much for your valuable informations.

The board has considered and approved the acquisition of 40% securities (11,65,740 Equity shares

and 18,46,154 Compulsory Convertible Debentures) of Seloi Healthcare Private Limited.

Company has received purchase order from Uttar Pradesh Medical Supplies Corporation Limited for supply of “COVID – 19 Antigen Based Rapid Test Kits” worth INR 10.50 Crore.Press Release - Award of Order

Results out… on the face of it seem disappointing… but debt seems to be paid down… also receivables issue addressed… cashflow for the year seems strong… let’s see how the concall goes…

Just saw on the charts of Cupid that the stock price is stuck in a broad range of 200-260 ever since July 2020 till date with the ocassional whipsaw move a couple of times.

Even before that, it has hardly done enough to deliver a promise of big returns. I think the first impression I had about it being a few tricks pony still remains the same. The only caveat is that they do something about this predicament by proving themselves in the new field of diagnostics they have entered.

Must applaud the patience and persistence of the guys who have kept faith in the manangement and kept holding on. Personally I find it difficult to attach myself to a company if I see no signs of promise after a couple of quarters.

I heard the concall for a few minutes. Few points I would like to mention -

1.) There seems to be no intention to hire a young and capable CEO.

Mr. Omprakash says his team is looking for the right person for this position , and the search is still on.

He says if they won’t be able to get in someone they will select someone internally.

2.) The plan is to venture into test kits not just for covid but for malaria and HIV as well.

New field of highly competitive business with established players already having majority of market share.

Wishful thinking along with it is projections like 50 cr of revenue in 2021-22 and 100 cr in 2022-23.

Hi All, I attended the Q4 FY22 Concall and attempted to summarize as below

• CO. has reported Sales of 41 crs , Npat at 6.4crs which brings FY 21 NPAT at ~29crs ,down from YOY 40Crs. Co has recommended 3.5Rs per share Dividend.

• Clinical Trial in SA for US FDA Approval shall happen in Jan 2022 for Female Condoms

• In Nov 2021 Brazil shall come up with Tender, Cupid had won the Prev tender and can win it again given low cost mfg which shall add to existing Order Bk

• Company faced increase in prices Raw Material for Q4, however it was able to transfer the increased cost to clients

• In Oct 2021, South African Govt may pass on part of their Tender to CUPID cos of Limitation of Capacity of existing local Mfg (potential order of 30 crs for Next 3 years)

• CO. has order book for 113crs + 40 to 50cr approx from IVD diagnostic Kits, aprox net profit of 35-40 crs

• Commercial Production for Diagnostic Kits shall start from July in Nashik.

• Company Plans to Boost Topline by more and more sales of the Kits going fwd. Concerns

• Succession Planning is still a concern as the CEO is 75 yrs plus in Age, and the company is yet to come up with a Successor

• IVD Kits prices are on the decrease as more and more players are stepping in however Cupid is targeting State Govts and Export Orders and is able to fetch repeat order from UP Govt

• Decreasing order book for Condom Biz (without considering potential Tender Wins from Brazil and SA this year)

• Business is Majorly Tender Driven and not via Distributor Channel (whether Existing Condoms Biz or Test Kits Biz) and hence they Rev fluctuates as per the duration of Tenders, though the Co. shall explore Sale via Channels for Test Kits Positives

• Co. is Debt Free. Co. Projects ~170crs Rev (without Tenders) which will give Net Profit of approx. 35-40crs and they project the Rev to grow by 10 -12% a year, at a price of 230, Mcap is 309crs, P/E is under 10.

• Company has 65 crs in Cash (which is appx 50/share Cash) which the co. plans to Reinvest in their Med Device Biz as they see potential Growth and order wins from Tenders relating to Malaria and HIV Kits especially in Africa.

• Co. has expanded their Condoms Mfg Capacity to 560 milion pieces from existing ~500 million pieces. Inferences

• The Comapny’s Rev for first 2 Qtr of FY 22 might not be better than YOY 21, so the stock shall move sideways, until they Fetch Tenders from SA, Brazil which will open only after Oct and Nov Respectively.

• US FDA Clinical Trials can be potential Trigger for the Stock which shall be only Next year i.e Jan 2022

• Orders for State Govt Relating to Test Kits can be triggers for the Stock

• Company seems Fairly Priced, gd for a Risky Bet as the current Tender Driven Biz Model is inherently unstable in terms of Rev

• Stock can be added only once it gets US FDA Approval as that will give it entry in a Bigger Mkt and a stable Rev as it shall market it products in USA and shall be in a duopoly mkt for Female Condoms. OR a Significant Development in Med Device Segment.

Just a naïve question. Veru is selling the female health business which means somebody will buy it. Don’t you think this new buyer may actually focus and re-energize this business more than Veru since Veru’s focus was somewhere else ? If so, it can not be called positive for Cupid IMHO

That’s why I said it’s too early to conclude. In any case - unless someone with an equally low cost production capability purchases Veru-FC, Cupid is in the clear.

I already see a lot of articles popping up, asking Veru-FC Condoms to be kept available to customers. So it would be a great opportunity for Cupid to buy the company for the Brand alone (Although as shown earlier in this thread, Veru-FC2’s Financial Position is in shambles).

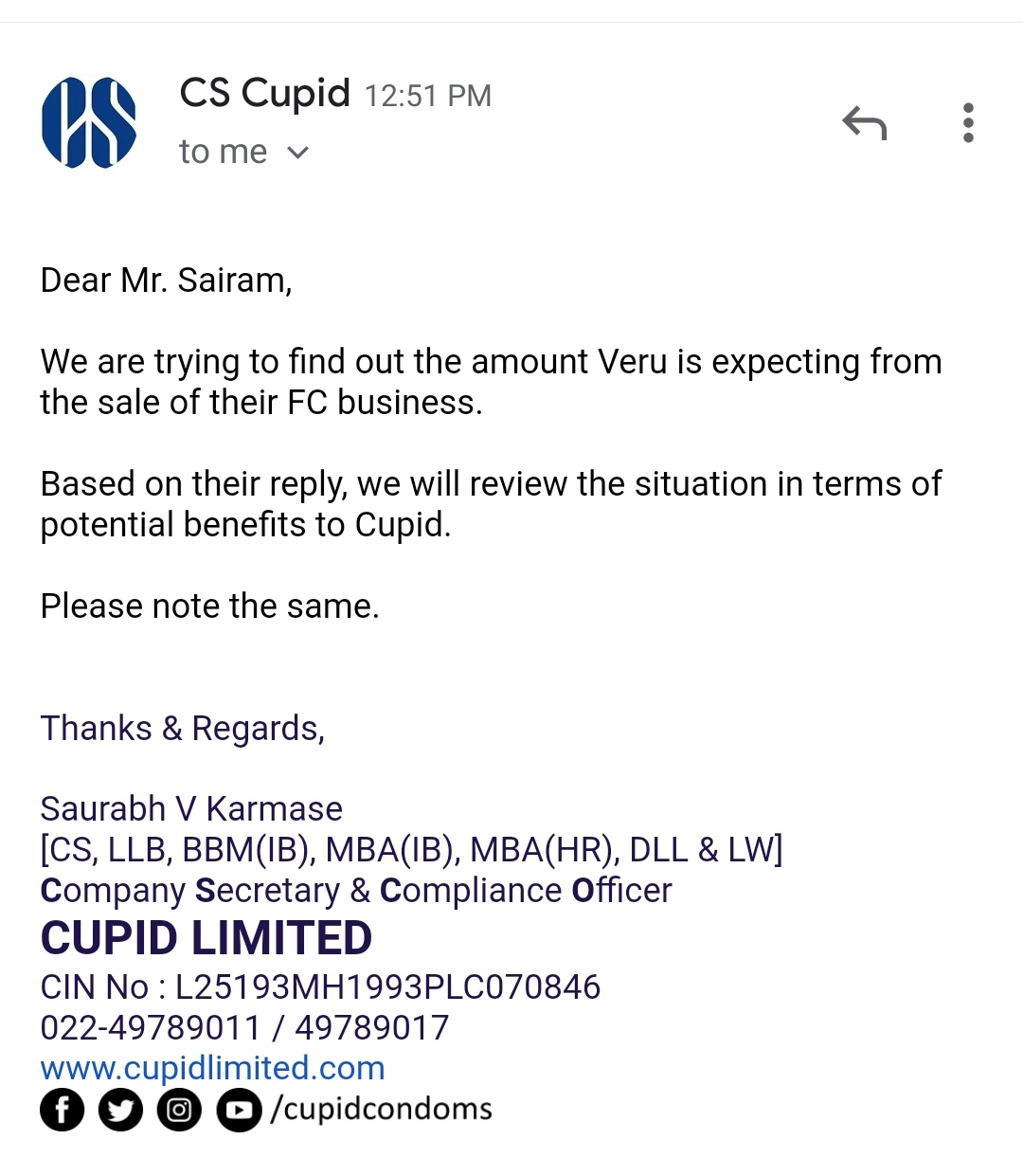

P.S. I have written to the CS about this. Let’s see if we get a good response.

Hi,

I have a doubt regarding the new medical device business.

As discussed in the earlier post the CS of the company had mentioned that the medical device business would be performed under Cupid only.

But few months back, Cupid and Invex health private limited had bought 40% stake in Seloi Healthcare Private Limited each to carry out medical device business.

Also second doubt is that the projection of Rs 50 crore revenue from medical device business is total revenue from the business or 40% share of Cupid (in this case then the total revenue would be Rs 125 crs).

Thirdly, where this Seloi Healthcare Private Limited manufacturing plant based out? As the concall mentions that the work is going on in Nasik for medical devices business. Is this work happening in Cupid’s premises or Seloi Healthcare’s premises?