I think that’s extremely unlikely. The Male Condom has been around for a while and its Market Size is quite big. If Big Pharma really had a solution like you’re suggesting, they would have stormed this market a long time ago.

Also, as you have mentioned, there are alternatives for Birth Control (Like Pills), but there is no product that helps in both Birth Control and a prevention against diseases.

Condoms are quite simply the easiest solution to the problem.

FC market has already ‘picked up’. Of course, you cannot compare a market which has been around a hundred and fifty years (Male Condom) to one that’s only been around for 7-8 years (Female Condom). You have to give it time.

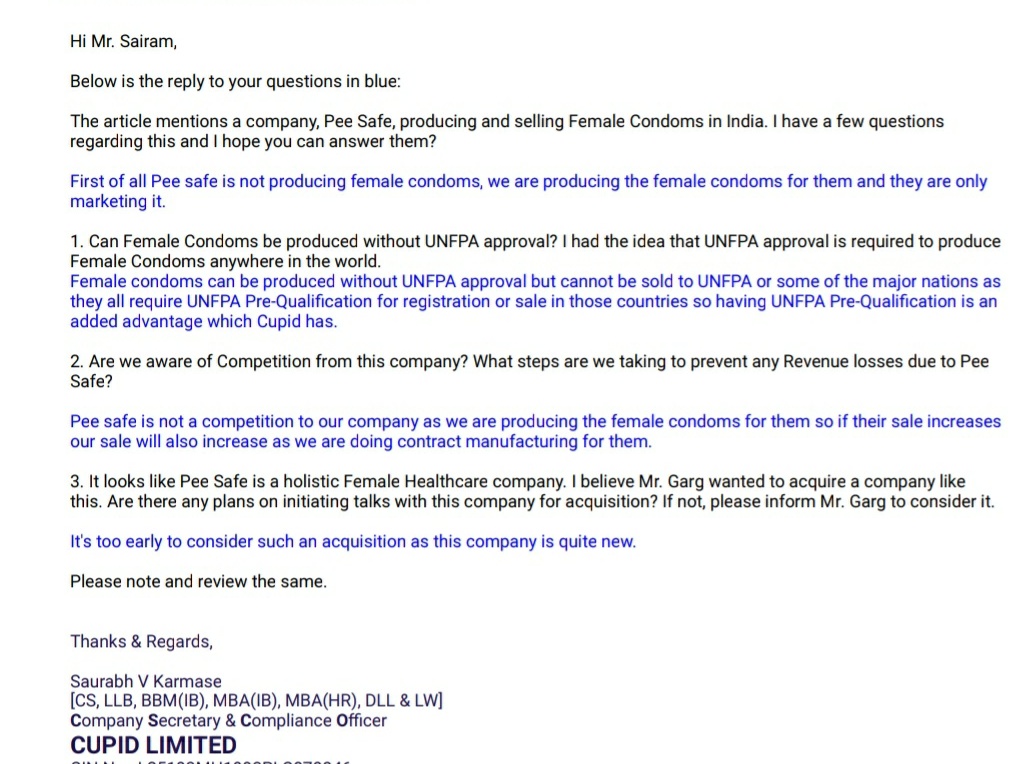

This may be the first time Indian frontline news media is covering female condoms… Good news for companies like Cupid. But seems like there is competition on the horizon

This seems to be a logical move… as all marketing and distribution costs are taken care by peesafe… whereas cupid can manufacture and make healthy margins…

Cupid triggers are - Pee safe may use VC money for marketting b2c which cupid was always vary and build a brand while cupid builds steady profits from contract manufacturing. USA prescription market is second trigger can be game changer in 2-3 years company can build huge profit pool and will have to go for capex if both triggers work out.

Worrying points . 1 No visible succession planning just one man show 2. Despite being in sanitizers before the market curve they could not capitalise on covid 19 , and now at end of pandemic trying to get into testing kits. shows management couldnt capitalise on sanitizer situtation and maybe going for wrong capital allocation.

The next Conference Call has been set for this Thursday.

Unlike most other small companies, we don’t have to speculate or assume risks and opportunities. You can just ask and I’m sure the management will try their best to answer it.

If you’re new to following or tracking Cupid, make use of this opportunity.

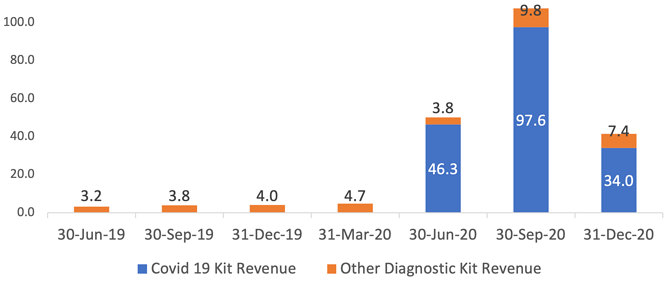

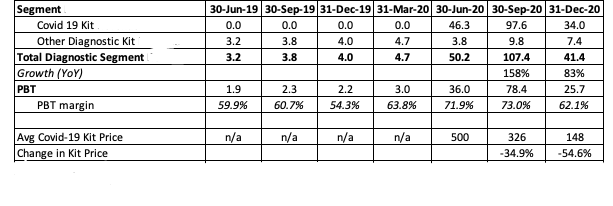

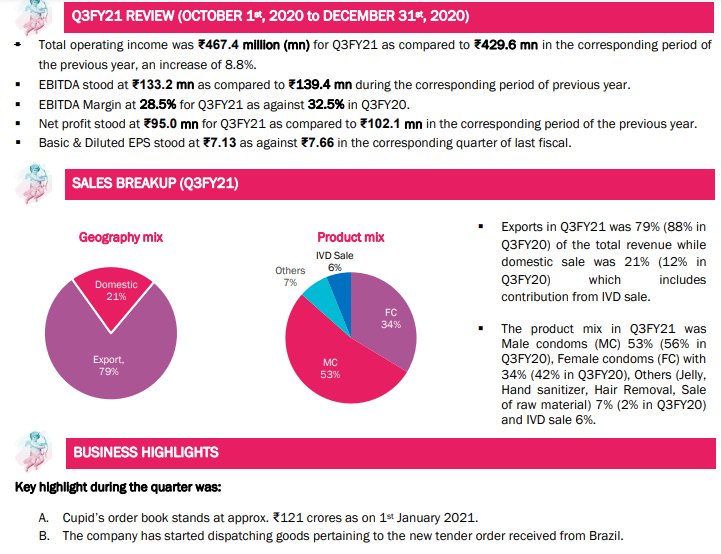

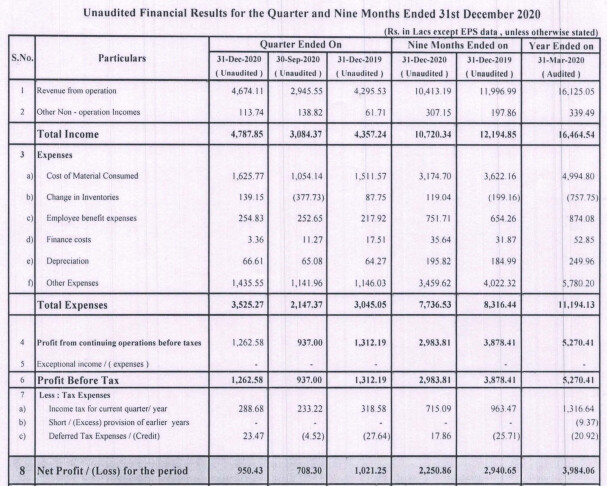

Q3 results are declared with Life time highest revenue of 47.9 Cr & Net Profit of 9.5 Cr. Margin have dipped a bit but product mix could be the reason, let us wait for more details from management in investor presentation / concall tomorrow at 5 PM IST.

Great con call as always. Managed to ask a lot of questions this time

Main udpates are there are 2 big tenders coming up and CUpid expected to win 45 cr each in SA and brazil. However SA tender is very flaky as the economy is in really bad shape. So take it with a pinch of salt.

The devices businesses is expected to do well - we already got the 8cr from UP gov’t already. Talking to large MNCs like Mylan etc to manufacture. Expectation is 50 cr revenue for next year and 15% net margin so 7.5 cr net profit.

Condom business expectation is 150 cr for next yr.

One good news is that management have done a lot of cost control initiatives and productivity enhancement so even with MC the EBITDA margin is 25 - 30% (previously 15% only). So we don’t have to rely a lot on FC for higher margins.

Registered product in 8 new countries like Turkey, Argentina, Peru etc. Not sure how much orders we will get from here.

The US FDA approvals are delayed because of covid. Revenue expected only in 2022 now.

On the Peesafe deal, management wasn’t sure about revenue projection as they are still awaiting details from peesafe. They have supplied them with 1 lakh pieces and I’m guessing based on the feedback that peesafe get from marketing this, they will place further orders. Mr Garg was as usual quite bullish on this but I’m not really sure they level of acceptance of FC in India. Also since peesafe is doing the sales and marketing, net margins are going to be in the region of 10 - 15% only.

Overall I would say things are looking good with margin improvement on MC, devices businesses should hold up ok.

Slight negatives are the lack of visibility on FC and US FDA delay.

Most highlighting was the statement that they are not looking for partnering any strategic investor. They seem to have put a firm full stop on this.

They seem to have put 54 cr cash reserve at bank FDs. They now realize that bank FD returns are too low and want advices from investor to maximize the return. Pls provide them suggestions if any.

No need to expand production lines to produce condoms for next 3 years.

Management has no eye on the share price performance. The body language seems that they dont look at share price as another jewel that needs a care.

Mr Garg has been loosing his audio hearing. Many a times he never heard/understood the question, but went on answering something ir-releveant. Its high time to get his next generation of peers on to the call and let them do the answering

I have emailed investor relations team regarding a buyback. Will keep everyone posted if they respond.

It is true that Mr Garg is unable to hear properly but I also found that people were also asking long-winded questions or on bad lines.

Rather than asking a simple question if Other expenses were going to continue at this level or not, one caller started off with revenue being high and net profit being low etc.

I asked him 6 questions and he answered them all in the first go. I keep it simple, to the point and clear which helps.

Don’t expect him to confirm it with me but I have just explained the benefits of a buyback to him. Most probable response will be that he will think it over. Hope he acts on it.

We have asked him multiple times in recent concalls & every time Mr Garg will respond positively but no action on ground. Being a small company with limited staff, they may have certain limitation but I have taken them as non-aggressive with respect to share holder expectations.

Mr Garg’s response & reaction to shareholders is positive in the concalls / communications but he is very rigid in his actions including search of CEO, buyback, expansion / acquisition suggestions by various stake holders.

We are good till he is able to expand topline / bottomline in limited world of government tender business governed by so many countries.

In the concall, Mr. Garg explicitly said their aim is to maximize Dividends as much as they can. Whereas for Buyback requests, it’s usually “We’ll take a call” or something similar.

I’m not complaining. Dividends are also okay. But Buybacks done at the right time can create far more value. So I’m just a little disappointed that we are not able to take advantage of that.

I have one doubt regarding 2020 annual report of cupid.May i know why this year alone,the company debt has been increased.And Mostly they have invested 11 core in fixed assets and remaining 29 core in other investments.May i know what is that other investments.If any one have idea in that,Please clarify this.