Looking at quarterly numbers for order based companies is not very useful. You should attempt to look at least 1-2 years together. Even Philip Fischer makes a note about this in “Common Stocks and Uncommon Profits”, although I forget the exact quote at this time.

But yes, this does make investing in order based companies slightly more difficult, hence the needs to be careful about what price you pay.

Other expenses include Advertisement, Packing and Material Handling Expenses, Product Registration Fees, Clearing, Freight and Transportation. I assume that expenses on account of Angel Brand Registration in US will be major contributor to this spike in Other Expenses.

Lower Cost of materials against sales could be due to higher shipment of Female Condoms compared to male condoms ( Brazil order execution for Female Condoms)

PAT is higher due to higher share of Female Condoms in total revenues

Press release…

Going forward, we believe that growth of our business will be positively impacted due to increase in demand of condoms worldwide for the prevention of STIs including HIV and for prevention of unintended pregnancies. Moreover, the outlook for Cupid remains positive due to the following reasons:

A. Better margin due to increased production capacity.

B. Increase in demand for Condoms is expected due to increase in international donor funding, higher consumption in lower- and middle-income countries and more funding from National Governments for the prevention of spread of HIV and unintended pregnancies like Brazil, South Africa and India.

Based on the above observations, we expect Cupid to improve its performance in the coming quarters and as such we remain positive on the company’s outlook. Looking at the current scenario, we expect to clock total revenue between Rs. 110 to 120 Cr and Net Profit of approximately Rs. 24 to 27 Cr for FY20. bc820a1b-f5b2-46bf-a1f4-74efbe4c03d4.pdf (522.4 KB)

They came up with revised press release as I could figure out a typo related to confirmed order in hand. Previous release mention different figures at different places. at one place it was 51 Cr whereas same release had 61 Cr at other place. Now it stands corrected

These could be typos and being a company with small workforce, these errors are common BUT when it goes out in public… it carries the reputation, brand value… & such few errors could result in big damage specially in such dynamic & fast moving equity markets.

All transactions happen at market prices, so you can buy anytime from the open market. The seller doesn’t really matter😀.

This was a rather interesting concall.

Key takeaways:

Order book is 163CR of which 61 is confirmed business for the next 2 quarters. For the rest, the company has received POs and despatch schedule. So decent probability that it’ll show up in topline provided the countries don’t face unprecedented budget cuts or other factors. Remain sceptical and track it from quarter to quarter.

Female condoms got sold more, so the materials consumed costs appear lower due to higher selling prices.

FY20 Revenue target 120 cr with ~20% npm. (I’m highly sceptical and prefer to discount the guidance).

No progress in CEO search.

Outstanding order book is mainly Brazilian order. Total order 124 cr; 24 cr executed until June 2019.

Suggested to showcase the company to MFs etc if earnings likely to look up in the coming periods.

Mulling expansion of board.

B2C margins lower. Focus is on B2B and into new territories.

Suggestion to include other key personnel in the earnings concall. Management will look into the suggestion.

Agree, small Typos are perfectly ok - governance issues with companies is bigger worry for me. Cupid has so far lived upto it when it comes to governance. Now, fundamentals also seem to pick up well with possibility of surprise upside on financials.

Discussions in hindsight have different feeling. Just think that if they come up with order in hand of 51 Cr where they have just achieved 34 Cr in a quarter. Orders in hand worth Only 1.5 quarter that too for a company which deals with Govt tenders.

Post correction we know that it was a typo & now it doesn’t hold any impact.

Coming to concall, I have few observations about management specially Mr Garg

He listens each suggestion, let it be from a small retail investor, and responds positively but actions differ, obviously he can’t implement all suggestions but he never opposes any suggestion e.g. some one suggested that explore MF houses for investment & he responded positively, other guy asked for CEO… the response ended with please refer someone whom you know… Another guy asked for expansion plans & suggested to sublet MC and low margin business to small startups … again the response was positive. Having attended few calls, I am sure that very few of above would be even remembered by next concall.

A major update missing in above concall details is about JV in SA. It is another big positive that Cupid has applied for licences to setup production units in SA for both FC & MC. Earlier the discussions with different partners had failed on account of commercial terms. Mr Garg is excited to have this opportunity as he is expecting orders from big distributors in SA, which will be on top of government tenders.

Their online presence has resulted in enquiries from other countries like Yemen, Mangolia, Cameroon etc

This time the concall was more wholesome compared to earlier concalls, which largely focused on Growth and Margin guidances.

Steps are being taken to utilize the 33 Cr Cash Balance on the B/S. The currently proposed options are:

Acquisition of Female Health Startups

More Capex on the lines of automation

More Dividends

I would prefer #1 the most, although I’m not sure acquiring a Startup is a good way to go. But if at all the management decides to do that, I should hope that the management does it after thorough scrutiny. Thankfully, there’s no doubt about the skills of the managements here, just a question of what would fit the organization.

Capex for Automation is the poorest of the lot. For a company its size, investments in automation would be an unnecessary load on the Operating Leverage. Especially since they are in a B2B business, a single lean season can cost a lot of money (Which is what the management indicated as well).

More dividends is always a good option, but it should be considered as a last resort. Buybacks, depsite the new tax, are still better considering the triple taxation on Dividends. Surprised no one suggested this. If I join the next concall, I will most likely suggest this.

While we’re on the topic, here’s an article about the impact Buybacks can have on the returns over time:

I understand (& I have rights to go wrong) that discussion on Cash balance utilization will fall in following

mrai74:

He listens each suggestion, let it be from a small retail investor, and responds positively but actions differ, obviously he can’t implement all suggestions but he never opposes any suggestion

Moving ahead buyback or any other suggestion is always welcome in email to CS. Mr Garg has openly invited shareholders to come with options, which make CUPID better & grow faster.

A rough calculation says that if the amount is used for buyback, it will be enough to buy 20% of total no of shares & approx 40% of floating stocks in open market. As the scrip is already low on volumes, this may dry it up more. Suggestions / discussion are welcome on this aspect.

If you’re confident about the company and the management’s action plan, then drying up of volumes shouldn’t be a big issue. The benefits of a good buyback done at commensurate prices (For instance, at CMP) are far greater than any momentary trouble you may face because of low liquidity.

But if you’re worried about liquidity in the sense that you do not completely trust the future landscape of the company and feel like you have one foot out the door, then it’s a question of conviction and whether you really want to stay invested in Cupid at all.

Edit: Here’s what I was looking for this whole time. An excellent case for why Buybacks are efficient.

I sent a mail to Cupid recently. I’ll try my best to join the next concall and see if we can get any updates on this.

The Mail

I am a shareholder of Cupid Limited. I am writing to this e-mail ID, because I couldn’t find one specifically for the Company Secretary.

This mail is for Mr. Garg / the management team. I was unable to attend the latest concall, but I did go through the concall transcript. Congratulations on an excellent set of results.

In the concall, there was a discussion about the usage of the 33 Cr cash on the Balance Sheet.

I was surprised that nobody mentioned Buybacks. Given the B2B nature of our business and the uneven revenue profile, I think Buybacks can be an excellent tool to boost shareholder value creation.

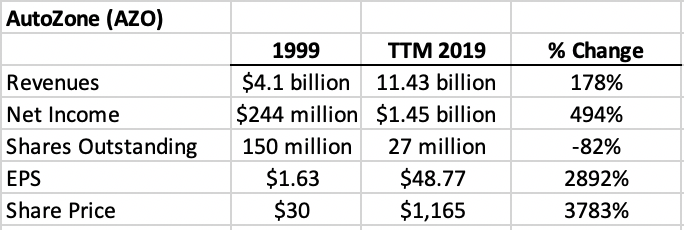

For instance, consider the company AutoZone (AZO) in the US. The company has grown its Net Income at a pace of 8.30% for the 20 years from 1999-2019. However, via Buybacks, AZO was able to reduce their Shares Outstanding by 82% during the same period. In effect, their EPS compounded not by 8.30%, but by an astounding 18.32% and change. Their share price during the same time compounded by almost ~20%. Thus a measly 8.30% growth in Revenues, combined with consistent buybacks throughout the 20-year period ended up compounding the share by almost ~12% extra.

So, I humbly submit to you that the potential for Buybacks in our company is huge. I understand that there may be some constraints. I would personally like to see some standardized way of doing Buybacks:

Announce Buybacks only at a specific price-multiple level (Below 10 P/E, below 2 P/B, below 1 PEG etc)

Utilize some set percentage of existing cash balance for the buyback (Say, every time a buyback is possible, announce it for ~30-50% of cash on books etc)

I understand that the recently introduced Buyback tax may feel like a deterrent, but indeed even after the tax, Buybacks are far more efficient at creating customer value when compared to dividends. (Also because of the fact that there’s a double taxation of Dividends).

I am sure that Mr. Garg / The CFO / Management Team will have a better idea of how to go about doing this. I only ask that my suggestion be considered seriously. A brief study of how AutoZone (AZO) created massive value via buybacks will certainly help my case.