Nice effort… incase you don’t get response, you may try sending to

Saurabh V. Karmase

Company Secretary and Compliance Officer

Email: cs@cupidlimited.com

Nice effort… incase you don’t get response, you may try sending to

Saurabh V. Karmase

Company Secretary and Compliance Officer

Email: cs@cupidlimited.com

Cupid Limited has received valuable repeat order worth INR 4.7 Cr from UNFPA to supply Male Condoms to Mozambique.

Cupid recieved a UNFPA male condom order for 14 Cr. Details on bse.

Receipt of Rs. 4.95 Cr worth orders from UNFPA for supply of Male Condoms to Angola

Sir, Did you received any reply for the email

Nope. I haven’t.

I want to wait for at least one more concall and then ask them either on the concall itself or another mail. I don’t want to pester them to be honest.

Like I said earlier, I will try my best to join the next concall.

Latest Annual Report -

CUPID AR 19 NOTES

Total revenue at 85.47 cr vs 80.6 cr yoy

EBITDA at 23.04 cr vs 28.3 cr yoy

PAT at 15.21 cr vs 17.09 cr yoy

Revenue impacted due to slowdown in female condom orders from Africa .

Business development expenses and lower proporon of higher margin Female Condoms in the total revenue impacted the margins and profitability

Female Condom registraon with Government of Brazil which has put us in favourable posion to win sizable order for Female Condoms from the region.

First shipment of condoms to Brazil

Completed contract with South African government of 3 years for supplying female condoms worth 104 cr.

“Cupid Angel” Trademark has been finally registered with the United States Patent and Trademark Office which would help us to promote and market our Cupid Female Condoms in USA.

Male condoms capacity expanded from 400 million pieces to 560 million pieces ( 40 % capacity increase)

Company exploring business opportunities in South African and Sub Saharan countries.

Male condoms contribute 59 % to revenues, female condoms 40 %, water based lubricant jelly 1 %

Promoter stake has increased from 44.87 % to 45.06 %.

Global condom market expected to grow at a pace of 9.8 % CAGR from 2018-23.

Male condoms have dominated the condoms market uptill now , but female condoms are also catching on.

According to National South African Female Condom Program, around 80% of female prefers Female Condom over other female contraceptives which is driving the sales of Female Condoms in the country.

Female condom being a higher margin product can be a great opportunity for the company going ahead.

Registered with the United States Patent and Trademark Office which would help us to promote and market our Cupid Female Condoms in USA.

Company has primarily been in B2B , looking to enter B2C now

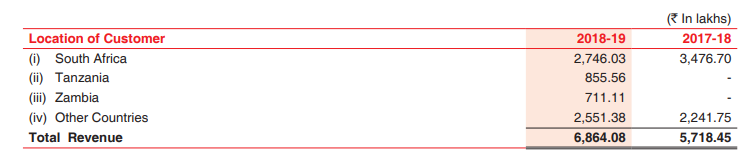

Break up of exports of company

Overall , I believe the numbers of the company and the balance sheet are pretty strong. The company has an OPM in the range of 25- 30 % , with good divindend payout ratios at 20 – 30 % . The company has a cash on balance sheet of 30 cr.

The company is available at PE of 10 , with a divinded yield of 3 % . The company seems to be well poised for growth ahead with expansion plans in place. With female condom opportunity also coming up can expect the margins to go up.

Some observations from annual report 2019

Points #1 & #2 you mention are indeed a little worrying (esp #2, since CEO hasnt been found since long).

I interpret this either as adamance on part of the Mr Garg on trying to find the “perfect CEO” OR his inability to simply to look in the right places…

This esentially makes Cupid a 1 man show

From the various investor concalls, I got the feeling that Cupid has more or less abandoned B2C efforts( at least not pursuing them with same gusto as B2B, which is their bread n butter business anyway.)

Almost every concall has a passing mention on B2C initiatives (like web-based , social media promotions etc) but no nation-wide AD campaigns on TV/radio .

As you mentioned their new products like Jelly lubricants have not taken off at all ( Since even B2B orders havent increased proportionally along with contraceptives).

Not sure if we can extrapolate furture sucess of new upcoming products like hand sanitiser on the same trends or not, time will tell.

Looking at the bright side, a few things to look forward to

As he worked for 10 months, I don’t think it made any bigger impact.

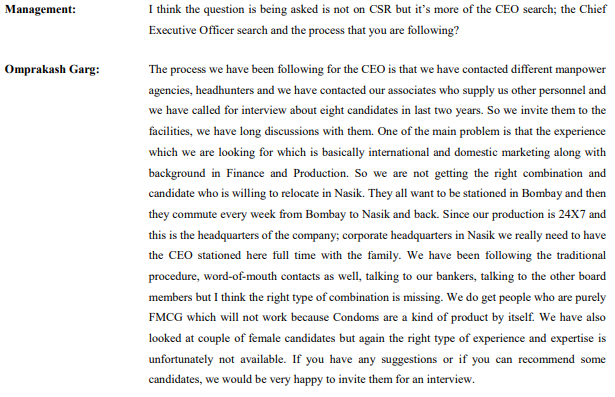

It was raised in last concall & his reponse was following

Ttk healthcare was recently left high and dry when Durex and Kohinoor brand names were lost in a bitter court battle. Today, They have a bigger share than Durex in India and rank second by sales.

Condom is not even their mainstay. Cupid relies on Condoms as it’s main business but struggles. That for me is worrying.

Failing to fill a CEO position for so many years is also a bummer. It’s tough to digest that he cannot find a single able person to run a profitable, growing, high margin company.

I had recently suggested they try promoting menstural cups to govts. Same end users, same buyers, same raw materials. They don’t seem too enthusiastic about this to even try. Neither have we heard much on any other plans. I see a similar future as Coral Labs which is also part of my portfolio. No new expansion and a growth engine that has aged.

If things stay the same, it won’t be long before Cupid’s growth starts to stagnate and that is not good for investors.

Their entry into US markets is a positive, but, everybody wants to sell on the US market. What is Cupid’s strength here?

I am still positive on Cupid for now but have many doubts about the companys future plans.

Based on my earlier interactions from Cupid Management, It is very evident that they are very conservative.

They try minimal risk and maximum business approach. Their concentration is on Tender business and B2C is not their cup of tea, considering the marketing expenses.

Comparing Cupid against TTK is not a wise analysis. it is like comparing VST Industries and ITC. TTK is an established player and manufacturing condoms for ~ 60 years. They are the ones who brought Durex to India. TTK’s focus is entirely on B2C. They have their own brand Skore and they are producing condoms for Durex on a contract basis. Skore itself has close to 20% market share in the Indian B2C market. Further, they have Pharmaceuticals and other industry segments in place.

Very recently Cupid underwent factory expansion, thereby we can’t expect them to dive into new business all of a sudden, given their conservative nature. We need to wait and see how FC works in US markets in 2020.

Of course, Increase in marketing/other expenses(which is inevitable, when they step in new markets) is a worry, but we need to wait for a few more quarters and see how it benefits the sales in the future.

If earning a 30-40% RoCE and having ~40% of the Book in Cash Equivalents is ‘struggling’, I would hate to see your definition of ‘not struggling’.

Like I said long back, Cupid has two distinct phases. Until 2014, they had a bad business model, didn’t have any relationships with their current exports partners and was essentially a part and parcel of the 15-20 condom makers in India (The Condom industry in India is terrible, with abysmal RoCEs).

But post 2015, they got recognized by WHO and started developing their network of export partners / countries. You can see the clear distinction in their P&L and B/S. So you’ve got to treat Cupid as a young business in the B2G/Export industry, but with the knowledge of trail and errors in condom manufacturing.

Your doubts about management succession is well-founded. Every year delayed without a new CEO is in fact stifling. Even the resignation of the other CXOs, I’m sure, has a lot to do with the fact that they have to work out of Nashik and not Mumbai. In my opinion, spending on an office in Mumbai solely for the benefit of a couple CXOs would be a terrible waste of money.

I see those healthy ROCE numbers. That is good. But a healthy ROCE figure will only remain as long as the business model is future proof. Increase in govt orders from Africa and Brazil are a positive but not sustainable in the long term. This is my personal opinion.

Having lots of cash on books is not good either. Definitely not for a small cap fast growing company like Cupid. Dividends, buybacks, expansion, product development, marketing, diversification etc needs money.

What I am saying is, Cupid is a great business as of now. But my confidence in the company to perform the same in the next 5 years is waning unless some things change.

Interim Dividend already?

It looks like the management has decided to pay out most of the cash as Dividends. Not that that’s a bad option - but a buyback is definitely better.

Its regular one which Cupid is giving every year. Hopefully we get 1/- as per last year.

The earnings power has to be strong. Then the quantum of dividend, buy back etc. follows.

I hope they make headway in succession planning.

Excellent Q2 results by Cupid: