Investment Summary:

I follow a framework driven approach where I look for companies with strong background, good financial and execution quality reflected through high ROE, ROCE, higher asset turnover, high PAT margin, low debt equity driven businesses with strong management quality available at reasonable valuations. However, sometimes I do break some of the rules if most of the rules are intact and there is genuine case.

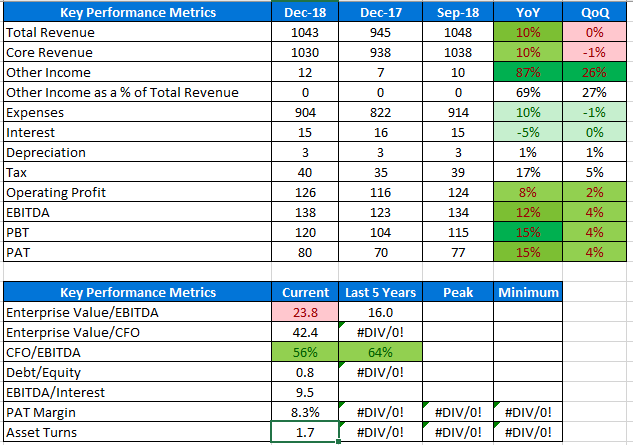

During 2016, while reading an article about the current MD of crompton consumer, Mr. Shantanu Khiosla and subsequently exploring the company, I was impressed by this company during Mar’16 and took a position and have regularly accumulated it. Some of the key numbers are below:

Now coming to business, Crompton Consumer Electric Limited used to be consumer electric business of Crompton greaves present in following businesses:

- Fans

- LED and traditional bulb and fixtures

- Residential Pumps

- Other electric goods like iron box etc.

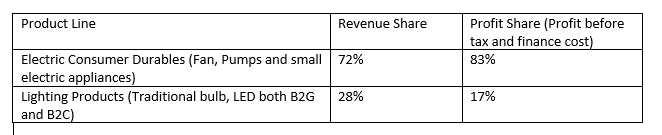

The break up of revenue and profit by product line is as follow:

Company history:

This used to be a part of Crompton greaves. However, in 2015, Avanta holdings acquired consumer electric goods business from Crompton greaves and brought Mr. Shantanu Khosla on board.

Now, here is a brief about Mr. Shantanu Khosla:

A P&G veteran for 30 years, Khosla (a graduate of the Indian Institute of Technology, Mumbai, and Indian Institute of Management, Calcutta,) came on board when the world’s largest consumer company acquired Richardson Hindustan Ltd, known for its Vicks brand, in 1983. It was formally rechristened Procter & Gamble India Ltd in 1985. Today, the Cincinnati, US, headquartered P&G has one wholly-owned company in India, Procter & Gamble Home Products Ltd (PGHP), which sells detergents (Ariel and Tide) and shampoos (Head & Shoulders and Pantene), and two listed companies, Gillette India Ltd, which sells razors like Mach 3 and Gillette, and Procter & Gamble Hygiene and Health Care Ltd (PGHH), which sells feminine hygiene products like Whisper.

After several stints abroad over a decade, in places such as Newcastle (the company’s UK headquarters), Kobe (Japan), Singapore and Kuala Lumpur (Malaysia), Khosla, who joined Richardson Hindustan Ltd as a management trainee in 1983, opted to return to India in 2002. “It was my professional desire to come back to live here and make a difference,” he says.

In the driver’s seat for 10 years, Khosla has grown the India business revenue from $110 million (around Rs.592 crore now) in 2002 to close to $1.5 billion as of June, which roughly translates to 13-fold growth, making it one of the fastest growing consumer companies in India. In the last 10 years, rival HUL grew its revenue more than two-fold, to Rs.23,436.33 crore.

The growth came as P&G, a late entrant, took on HUL, which has been in India since 1933. In the detergent space, the two multinationals have engaged at least twice in price wars which led to deteriorating margins for both. In fact, it’s after the losses incurred in one such price war in 2004-05 that the detergent business moved from PGHH, a listed subsidiary, to an unlisted subsidiary in India, in July 2005.

The losses were no deterrent, however. As recently as 2009-10, HUL and P&G were once again warring for supremacy in the detergent space, which is one of the largest and most penetrated segments in India.

Over the last decade, P&G, which operates in 24 categories globally, has increased its presence from six categories to 14 in India and now plans to bring in the parent’s entire portfolio, with the exception of toilet paper, says Khosla.

In the last three years, it has increased its distribution reach by 60% to nearly six million stores, closing in on the gap with HUL, which reaches a little over seven million stores. It is addressing the perception that it’s relevant just to urban consumers. Close to a fourth of its revenue now comes from rural India, compared with 12% three years ago.

Source: Shantanu Khosla | The Consumer Captain | Mint

Key to note is he has led one of the biggest FMCG operations across the world and in India has beaten his peers in and out where in 10 years he grew revenue 13 times in 10 years against 2 times by closest competitor.

Why Khosla joined Crompton consumer?

I do not have that article but I was drawn to this company when I read an article titled “60s is new 30s for these CEOs” where Khosla was one of them rolling his sleeves to revive Crompton brand. As per article, his interest to take board position was that he has done all sorts of job in FMCG but taking an old brand, which was quite popular but had lost its charm kind of looked challenging

So, the demerged business has a history of 2 years approx. How Mr. Khosla has done so far. In order to decode this, let us see what Mr. Khosla had promised to his shareholders. This was a crisp 1-page communication with a clear cut 5-point agenda:

Now let us look at how he has done against this 5-point agenda in last 2 years:

- Revival of Crompton brand: Visible in higher brand awareness through campaigns (IPL, Test matches) resulting in robust sales and profitability growth

- Innovation:

a. Launch of self-temperature adjusting fan

b. Launch of dustless fans

c. Tie up with an European home automation IoT technology player for home automation - Marketing:

a. Refreshed go to market strategy

b. Channel expansion

c. Higher focus on innovative premium products in fan

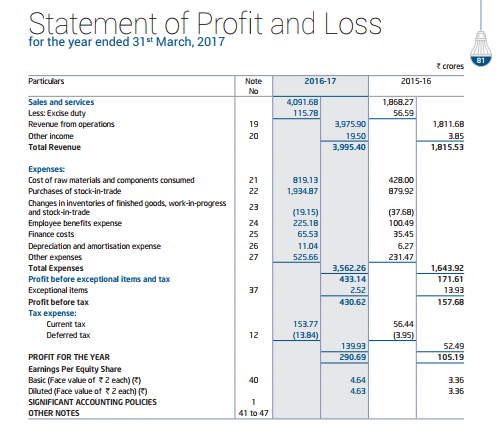

The overall result of these initiatives apart from point 4 and 5 related to supply chain optimization etc. has been: - Revenue growth of 11% considering demonetization and GST headwinds

- 22% of operating profit growth

- PAT margin improvement from 5.8% to 7.3%

- High double-digit growth in premium fan segment snatching market share from competitors (as per con call reports based on 3rd party data)

- Doubling of market share in LED segment (consumer) and now no 2 players in consumer LED segment

- Focus on new products with an objective to be either no 1 or no 2 players

- Conversion of bank loan into NCDs

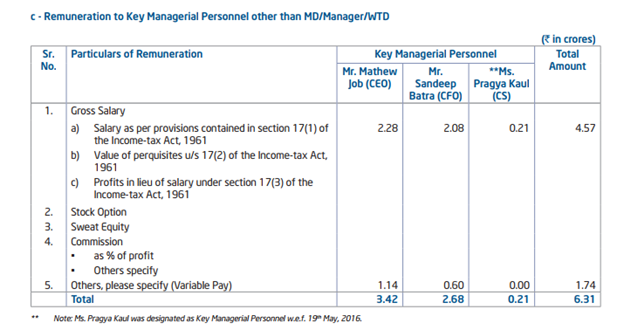

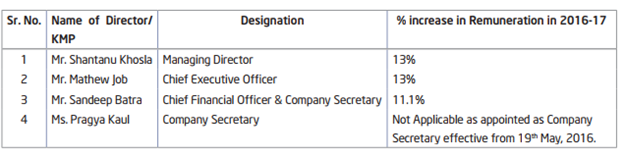

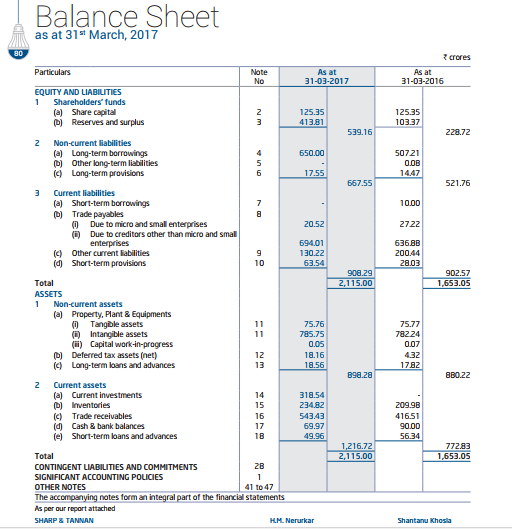

Attaching further numbers about business and management:

As One can see, management salary is 2.5% of PAT which is reasonable and also increase in management remuneration looks reasonable considering the growth they have achieved in business.

Coming to future, this is what I interpret:

- Company is working hard to continue its above market growth rate which means double digit growth

- More supply chain optimization, interest cost reduction and higher focus on premium products should further lead to margin expansion

- Company trying to get into few new segments like ir purifier (still in pilot test mode) with a mandate to be market leader

- Company is active on usage of technology and smart homes and hopefully with a strong management in place, would be able to leverage this opportunity

- Pump business has not done that well but with improvement in real estate and rural climate, hopefully will do better

Strengths:

- Well proven management in the form of Mr. Shantanu Khosla, walking the talk

- Strong performance in topline, bottom line, margin improvement and market share gain

- High quality business with double digit revenue and profit growth, 40%+ ROE and ROCE, 7% free cash flow to sales ratio, comfortable debt coverage position, asset light brand driven business model with efficient working capital management

- Huge market size opportunity ahead with still more than half market belonging to unorganized player and overall average sector growth (across fan, LED and pumps) growing near 10% highlighting long run way ahead

Concerns:

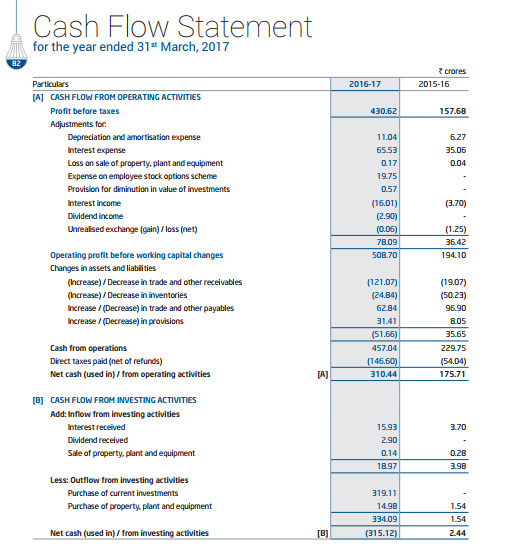

- Debt equity ratio seems a concern at 1.2 but company is generating 300 cr + cash flow from operations and can easily pay 60-70 crores of interest annually on 600 crores of loan and can easily get rid of debt in 4-5 years. This will further improve margins

- Less comparable history: Difficult to compare numbers beyond 2,3 years historic basis and one needs to build his conviction based on recent performance and overall trust on management

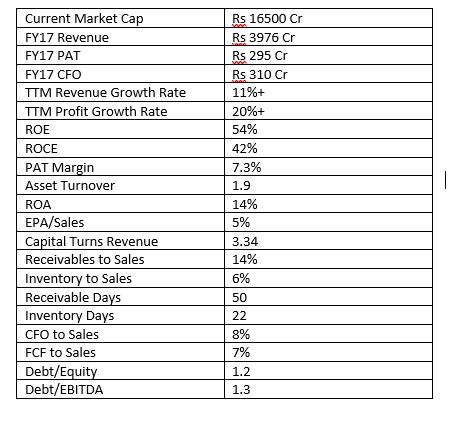

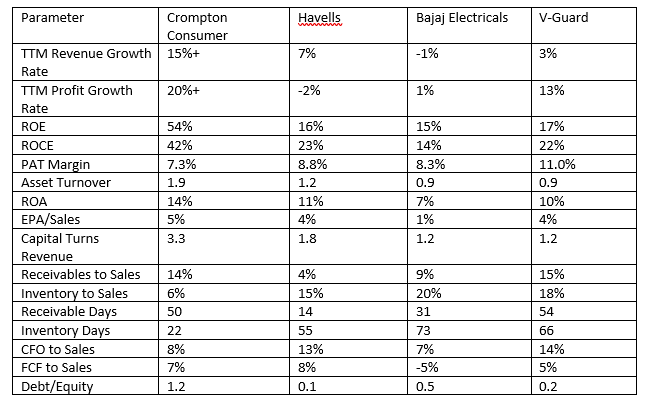

- Valuations: I would leave valuations to everyone to pick what is right valuation for them based on their risk appetite, time frame and valuation framework. However, I would throw some data about company and competitors so that one can access its business and competitive strength along with valuation attractiveness:

Valuation as on 31st March 2017

- Company does face some raw msaterial pricing pressure due to chnge in copper prices but so far has been sable to pass it to consumer due to brand power

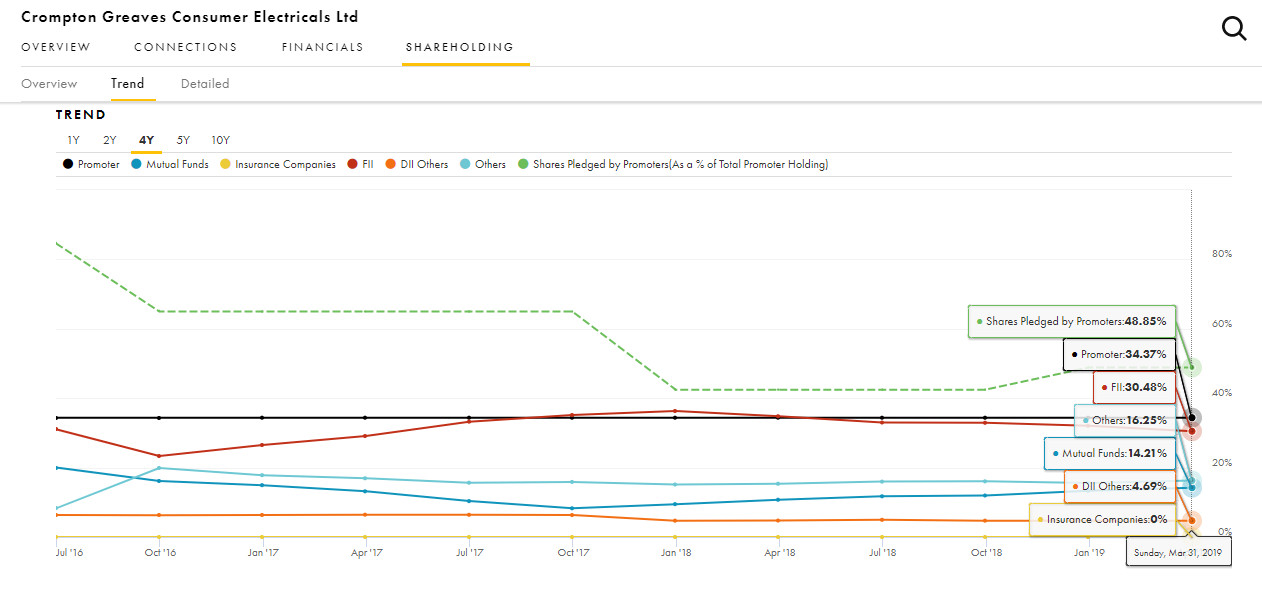

List of marque investors:

Avantha Holdings (Promoter): 34.37%

*MacRitchie Investments Pte. Ltd: 12%

LIC of India Child Fortune Plus Balanced Fund: 4.78%

Smallcap World Fund, Inc: 4.73%

Nomura India Investment Fund: 2.19%

Franklin Templeton Investment Funds: 1.99%

Amansa Holdings Private Limited: 1.85%

Note: Concall transcripts are very detailed and available at company website. Serious investors if find company attractive must go through last 8-10 quarters of concall transcripts to understand business in more detail

Disc: 6% of portfolio with average price of Rs 173